Wealth and complexity go hand in hand. The more you’ve built, the more exposure you face-and standard insurance policies rarely account for the nuances of your situation.

At FirstMark Insurance Group, we’ve worked with high-net-worth individuals who discovered gaps in their coverage only when it was too late. A private client protection plan addresses this directly, layering customized coverage across assets, liabilities, and legacy concerns that matter to you.

Why Standard Policies Leave High-Net-Worth Individuals Exposed

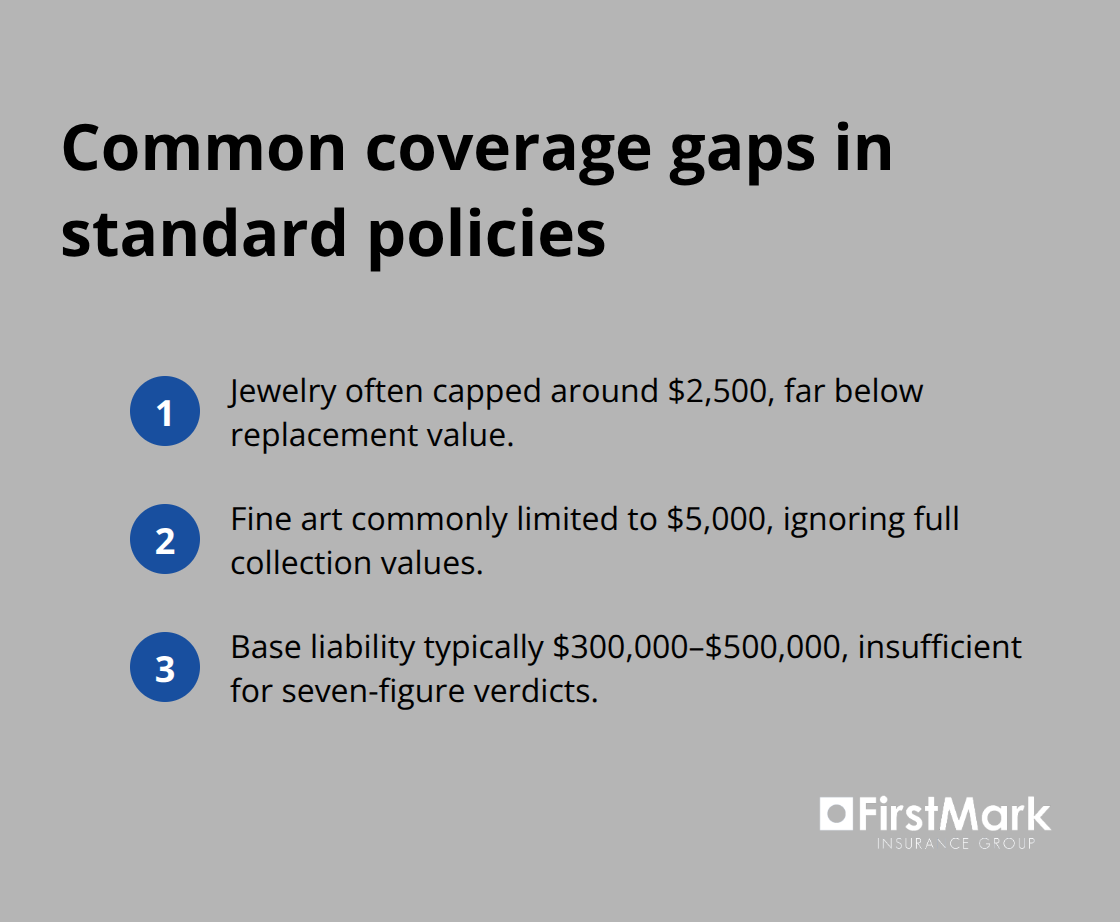

High-net-worth individuals operate in a fundamentally different risk landscape than the average homeowner or business owner. Standard homeowners policies cap coverage on valuables at depreciated values-typically $2,500 for jewelry, $5,000 for art, and similar arbitrary limits that bear no relationship to actual replacement costs. If you own a $150,000 art collection or $80,000 in jewelry, standard coverage leaves you dramatically underinsured. This isn’t a minor gap; it’s a structural failure of conventional policies to address the assets that matter most to you. The same problem extends to liability. A standard homeowners policy provides $300,000 to $500,000 in liability coverage. For someone with substantial net worth, a single lawsuit can exceed these limits by multiples. A jury verdict in a personal injury case can easily reach $2 million or more, and your standard policy stops protecting you long before that threshold.

Multiple Properties Demand Coordinated Protection

Most high-net-worth individuals own more than one property-a primary residence, vacation homes, rental properties, or investment real estate. Standard policies treat each property in isolation, creating coordination problems that expose you to coverage gaps. Your primary home might have adequate protection, but your vacation property in a coastal area faces wildfire or hurricane risk that requires specialized assessment. Your rental property needs different liability coverage than owner-occupied homes. Without a coordinated strategy, you end up with fragmented coverage where one property is overinsured while another is underprotected. A private client protection plan treats your entire portfolio as an integrated system, ensuring consistent protection standards across all locations and accounting for the unique risks each property faces.

Specialized Assets Require Specialized Coverage

Collections-fine art, vintage wine, rare watches, classic automobiles, firearms, or antiquities-cannot be adequately protected under standard policies. These assets require item-level appraisals, specialized valuation experts, and claims adjusters who understand their true value and restoration costs. A standard adjuster cannot properly evaluate a Rolex collection or a wine portfolio. Private client coverage pairs formal appraisals with scheduled endorsements that insure each item at its appraised value, not some arbitrary sub-limit. This approach protects the actual worth of what you own and ensures claims handlers possess the expertise to evaluate your specific assets fairly.

The Liability Exposure Beyond Your Home

Your personal liability extends far beyond property damage. A visitor injured on your property, a defamation claim, or an allegation of false arrest can trigger lawsuits that standard policies either exclude or severely limit. These scenarios (while uncommon) carry devastating financial consequences when they occur. Standard homeowners policies typically cap liability at $500,000, leaving substantial net worth vulnerable to judgment. A comprehensive private client plan layers excess liability coverage that protects your full net worth from high-severity claims, addressing exposures that conventional policies simply ignore.

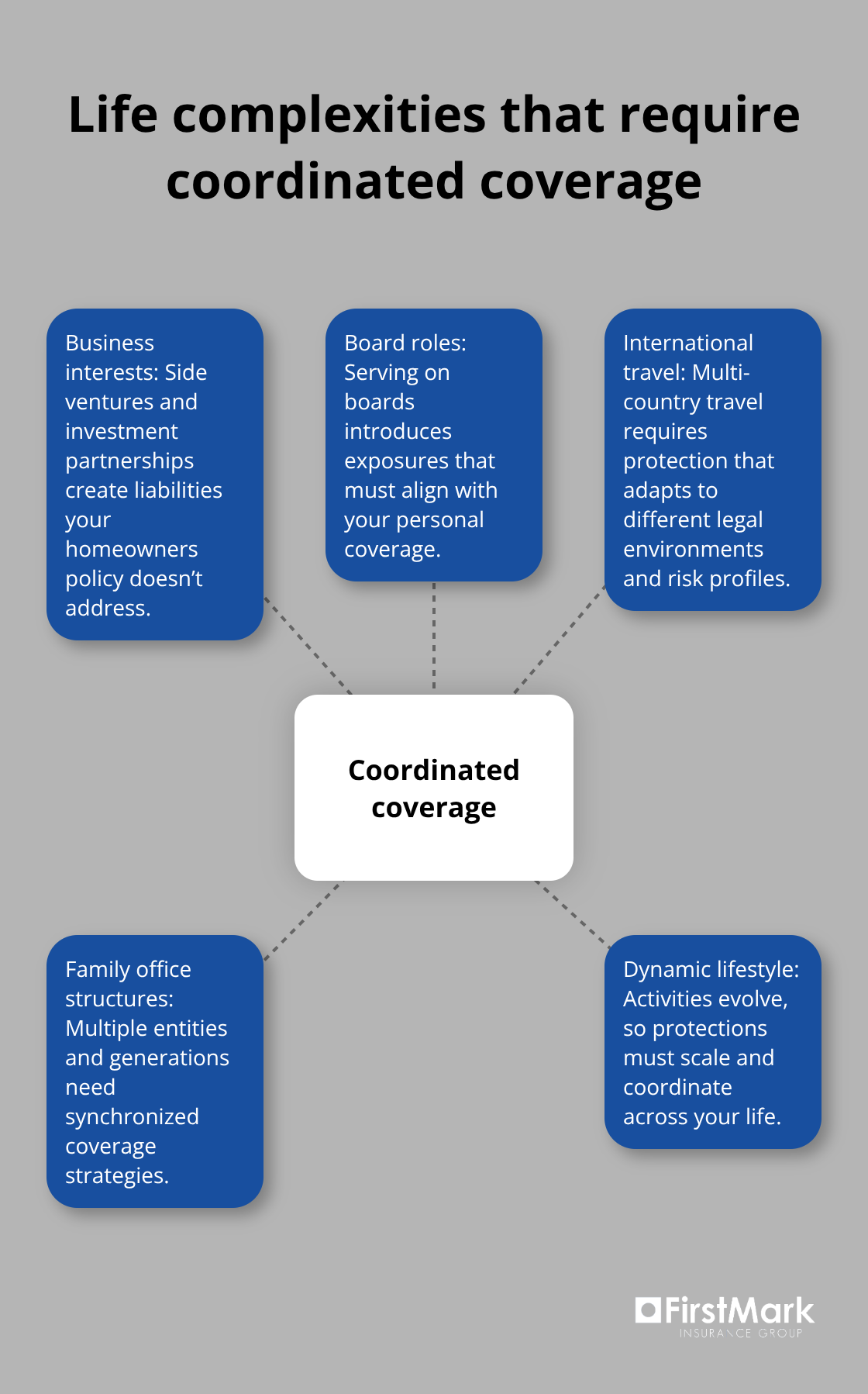

Coordinating Coverage Across Your Life

The complexity multiplies when you factor in business interests, international travel, or family office structures. A side venture, board position, or investment partnership creates liability exposures that your personal homeowners policy doesn’t address. Travel to multiple countries requires coverage that adapts to different legal environments and risk profiles. Family wealth structures demand protection strategies that coordinate across entities and generations. Standard policies were never designed to handle this level of sophistication-they treat your life as a simple, static scenario rather than the dynamic, multifaceted reality you navigate.

This fragmentation explains why high-net-worth individuals need a fundamentally different approach. Rather than purchasing isolated policies that leave gaps, you need a coordinated strategy that addresses your complete risk picture. The next section explores how to build that comprehensive protection strategy across your assets, liabilities, and legacy concerns.

Building Your Complete Protection Strategy

Start with an Honest Asset and Liability Inventory

A comprehensive protection strategy starts with a brutal assessment of what you actually own and what could realistically harm your wealth. Most high-net-worth individuals skip this step, assuming their existing coverage is adequate. It isn’t. The first action is to inventory your assets across all categories: real estate holdings with current valuations, investment portfolios, business interests, collections, vehicles, and any other significant property. Then list your liability exposures-properties you own, business roles you hold, board positions, rental activities, and any other situations where someone could sue you successfully. This inventory becomes the foundation for coordinated coverage that addresses actual risk, not theoretical scenarios.

Layer Coverage Types Strategically Across Your Properties

Asset protection requires you to layer coverage types strategically. Your primary residence needs higher limits than standard policies provide, with replacement cost coverage based on actual rebuilding expenses rather than estimated values. A $3 million home requires $3 million in coverage, not the $1.2 million that standard insurers might offer. Vacation properties in high-risk areas demand specialized assessment-coastal properties face hurricane and flood exposure that requires parametric coverage or separate flood policies, while mountain properties need wildfire protection built into the strategy. Investment real estate requires landlord liability coverage that protects against tenant-related claims, distinct from owner-occupied home coverage. Collections and specialized assets need scheduled coverage with formal appraisals from certified professionals, ensuring each item receives protection at replacement value rather than arbitrary sub-limits.

Protect Your Net Worth from Liability Claims That Exceed Base Limits

Liability management extends beyond property damage into personal liability that most people ignore completely. Your net worth becomes a target in high-severity claims, and standard homeowners policies stop protecting you at $300,000 to $500,000. Excess liability coverage bridges this gap, protecting your full net worth from judgments that exceed base policy limits. If you own a business or hold board positions, that creates separate liability exposure requiring coordination with your personal coverage to avoid gaps or overlapping protection.

Integrate Business, Travel, and Wealth Preservation Across Your Coverage

Business succession and wealth preservation demand integration across multiple coverage types and entities. If you own a business, that asset needs protection through buy-sell agreement funding, key person insurance, and liability coverage specific to your industry. Family office structures require coordinated coverage across multiple properties, entities, and generations. International travel introduces complexity-your U.S. homeowners policy provides minimal protection outside the country, requiring supplemental coverage for properties or extended stays abroad. Estate planning and wealth preservation are reinforced through proper insurance structuring that protects assets for your heirs while managing tax implications. This requires coordination between your insurance advisor and estate planning attorney to ensure coverage aligns with your succession strategy.

Review Your Coverage When Life Changes

Your coverage needs change when you acquire property, start a business, marry, have children, or experience significant changes in net worth. Annual reviews with a specialist advisor who understands your complete situation catch gaps before they become expensive problems. These regular assessments ensure your protection strategy evolves with your life rather than remaining static while your circumstances shift. The next section addresses how to implement this tailored coverage plan and work with specialists who can translate this strategy into actual protection.

Implementing Your Tailored Coverage Plan

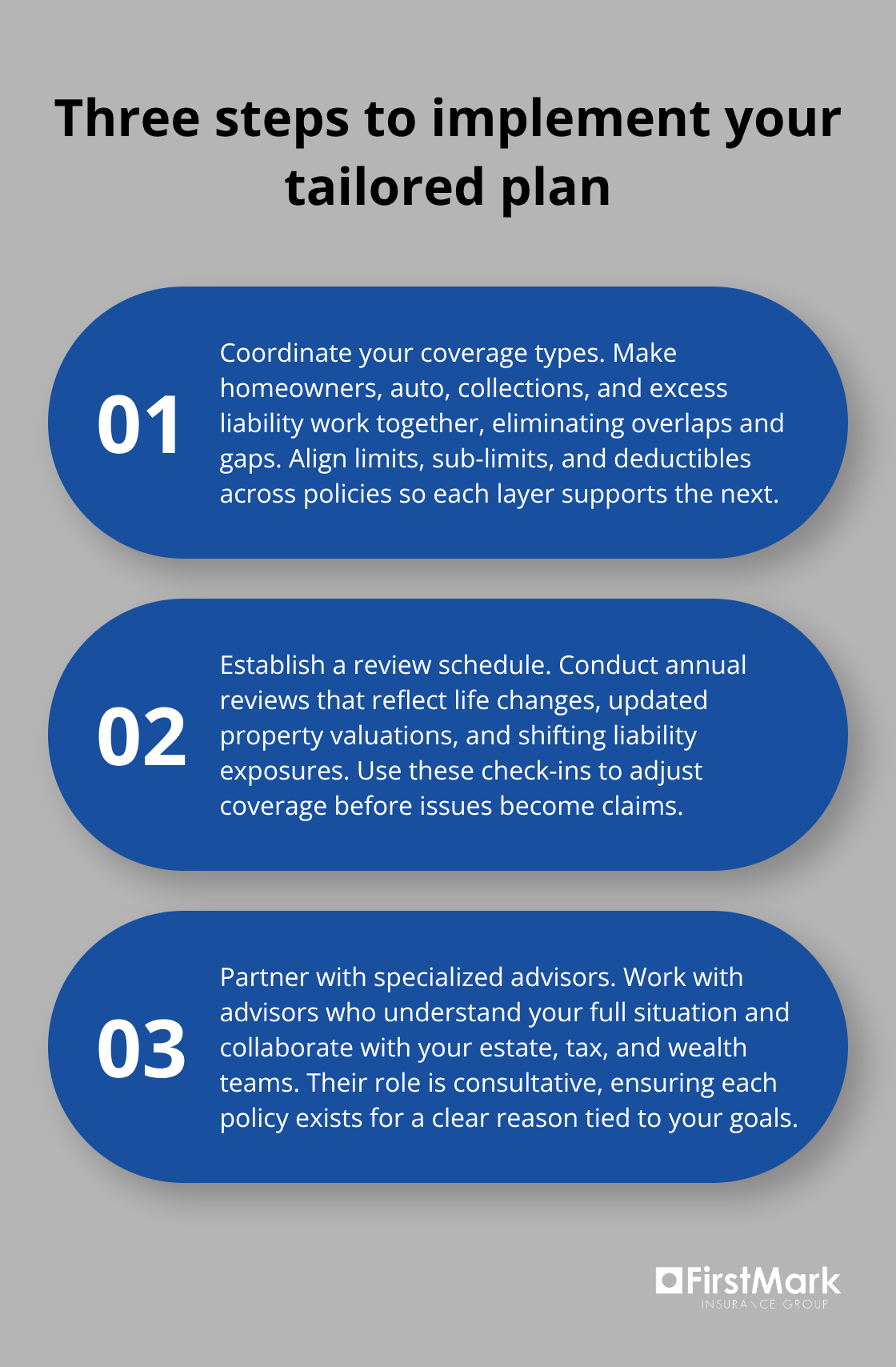

Translating a comprehensive protection strategy into actual coverage requires moving beyond theoretical planning into concrete implementation. The gap between understanding what you need and securing it properly separates those with genuine protection from those with expensive gaps. Implementation demands three specific actions: coordinating your coverage types so they work together rather than against each other, establishing a review schedule that keeps pace with your changing circumstances, and partnering with advisors who grasp the full complexity of your situation rather than selling isolated products.

Map Coverage Across Your Complete Portfolio

Coordination starts with mapping how your coverage types interact across properties and liabilities. Your primary residence needs adequate limits for replacement cost, your vacation property requires specialized assessment for its specific geographic risks, and your investment real estate demands landlord liability protection that differs fundamentally from owner-occupied coverage. When these policies operate independently, overlaps and gaps emerge naturally. A specialist advisor views your entire portfolio as an integrated system, identifying where one policy complements another and where coordination failures leave you exposed.

This coordination extends to collections coverage. If you own art, vintage wine, or classic cars, scheduled endorsements must align with your homeowners limits so that a claim to one policy doesn’t inadvertently reduce coverage elsewhere. The same principle applies to excess liability. Your base homeowners and auto policies create a foundation, but excess liability coverage only works effectively when those underlying limits are properly structured. Many people purchase excess liability without confirming their base limits are adequate, creating a false sense of protection when the foundation itself has gaps. Implementation means confirming each layer connects properly to the layers below and above it.

Establish Annual Reviews That Catch Life Changes

Regular reviews transform a static plan into one that evolves with your life. Your coverage needs shift when you acquire property, experience significant changes in net worth, start a business, or modify how you use existing assets. Annual reviews with an advisor who understands your complete situation catch these changes before they become expensive problems.

During these reviews, confirm that property valuations reflect current replacement costs rather than outdated estimates, verify that collections have been reappraised if their market value has shifted substantially, and assess whether liability exposures have changed based on new business activities or family circumstances. A proper review also addresses emerging risks. If you’ve increased international travel, your existing coverage may not extend adequately beyond U.S. borders, or if you’ve taken on board positions, those create liability that your personal homeowners policy doesn’t address.

Partner With Advisors Who Understand Your Full Situation

Working with specialists means finding advisors who invest time in understanding your specific circumstances rather than applying generic solutions. A true specialist asks detailed questions about how you use your properties, what your collection actually contains, what business interests you hold, and what your family structure looks like. They coordinate with your estate planning attorney, wealth advisor, and tax professional to ensure insurance decisions align with your broader wealth strategy.

This level of engagement requires advisors who view your relationship as long-term and consultative rather than transactional. The advisor should be able to explain not just what coverage you have, but why each piece exists and how it protects specific aspects of your wealth and lifestyle. When you work with an advisor who takes this approach, you gain confidence that your protection strategy reflects your actual circumstances rather than a template applied to thousands of clients.

Final Thoughts

The complexity of your wealth demands a protection strategy that matches its sophistication. A private client protection plan isn’t a luxury-it’s a practical necessity for anyone with substantial assets, multiple properties, or specialized collections. Standard policies were designed for straightforward situations, and applying them to your circumstances leaves gaps that can cost far more than the premium difference between adequate and inadequate coverage.

Proactive planning protects what matters most by addressing exposures before they become claims. When you inventory your assets honestly, layer coverage strategically across properties and liabilities, and establish regular reviews with a specialist advisor, you eliminate the fragmentation that creates vulnerability. This approach transforms insurance from a checkbox on your to-do list into an integrated component of your wealth strategy, ensuring assets transfer to your heirs intact rather than diminished by unexpected losses or liability judgments.

At FirstMark Insurance Group, we’ve spent 30 years guiding families and businesses through these complexities. We understand that your situation is unique, and we work with top insurance providers to build protection strategies that fit your specific needs at the best available pricing. Connect with our team to discuss how a tailored approach transforms your coverage from adequate to genuinely protective.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation