Owning a second home in Washington comes with distinct insurance challenges that many seasonal residents overlook. Standard homeowners policies often leave significant gaps in coverage, leaving your property vulnerable during months when you’re away.

At FirstMark Insurance Group, we’ve guided countless second home owners through the complexities of secondary home insurance in Washington. The right coverage strategy protects your investment while keeping costs reasonable.

What Counts as a Second Home for Insurance Purposes

The distinction between a second home and an investment property matters far more than most Washington owners realize, because it directly determines which insurance policy you need and how much you’ll pay. Insurance companies classify a second home as a residential property you own but don’t occupy as your primary residence, typically used for seasonal living or occasional getaways. The critical detail is occupancy: a second home must be available for your personal use, not primarily rented to tenants. If you rent it out most of the year, insurers will classify it as an investment property, which requires entirely different coverage and costs significantly more.

How Occupancy Shapes Your Coverage Needs

How frequently you occupy your Washington property fundamentally changes what protection you actually need. A lake house you visit every summer weekend faces different risks than a mountain cabin you check on twice a year, and your insurance should reflect that reality. Properties left vacant for extended periods attract higher premiums because insurers know that unoccupied homes face elevated risks of burglary, water damage from undetected leaks, and liability issues that go unnoticed. Many standard homeowners policies include occupancy clauses that limit coverage if the home sits empty for more than 30 consecutive days, which means a policy written for your primary residence won’t adequately protect your seasonal property. When you own property in Washington but spend most of your time elsewhere, you need a policy specifically designed for that occupancy pattern, not a generic homeowners policy adapted to secondary use.

Why Investment Properties Require Different Coverage

The moment you rent out your second home, even occasionally, the insurance landscape shifts dramatically. A property you rent on Airbnb during summer months or lease long-term to tenants requires vacation rental insurance or landlord coverage, not standard second-home insurance. Standard homeowners policies explicitly exclude business-related claims, which means rental income and rental-related damage fall outside your protection entirely. If a guest injures themselves in your rental home or damages the property, your standard policy will deny the claim. Mortgage lenders often require proof of appropriate insurance, and they won’t accept a standard second-home policy if the property generates rental income. The distinction matters because it affects your premium by potentially hundreds of dollars annually and determines whether you have any coverage at all when something goes wrong.

Understanding these classifications sets the foundation for selecting the right policy. The next section examines what standard homeowners policies actually cover and where the gaps appear for Washington seasonal properties.

Coverage Requirements and Gaps for Washington Second Homes

Your primary homeowners policy was designed for a house you occupy year-round, not a property sitting empty for months at a time. That fundamental mismatch creates serious coverage problems. Standard homeowners policies include occupancy clauses that void or severely limit coverage if your home remains vacant for more than 30 consecutive days-exactly the scenario most Washington second home owners face. If your mountain cabin or lake house sits unoccupied through winter or you’re away for an extended stretch, a standard policy may not cover water damage from frozen pipes, theft, or liability claims occurring during those vacant periods. Second home insurance differs from standard homeowners coverage in ways that directly impact what gets paid when something goes wrong, and insurers recognize the heightened risk of unoccupied properties. Your lender likely requires coverage, but they won’t accept a standard policy if vacancy clauses apply. Many second home owners discover this gap only after a loss occurs, at which point the claim gets denied and the financial damage is already done.

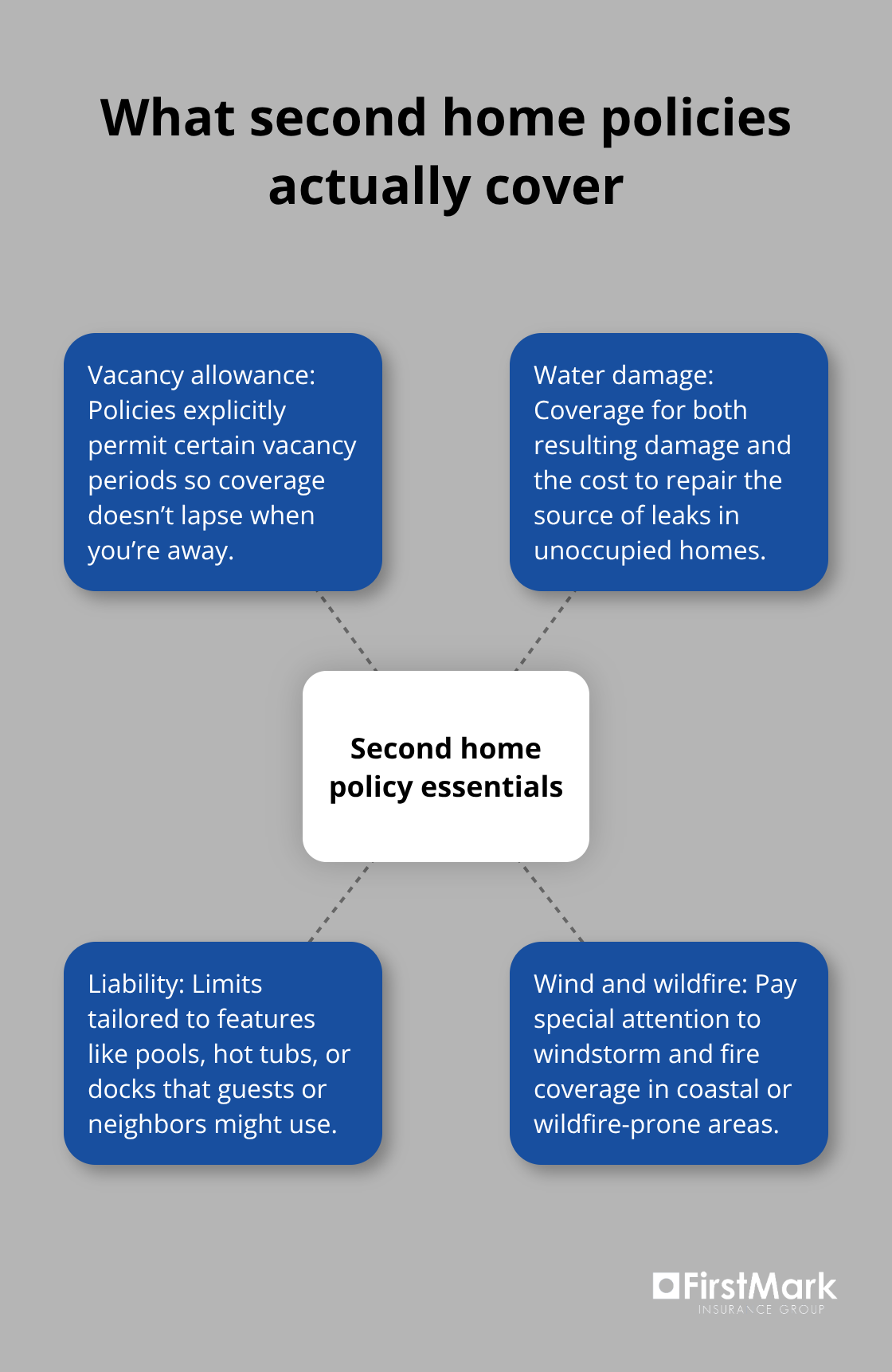

What Second Home Policies Actually Cover

Second home policies explicitly permit vacancy for the periods when you’re not at the property, with clear language about how long the home can sit empty before coverage lapses. Water damage coverage becomes critical because unoccupied homes develop undetected leaks far more often than occupied ones, and you need protection that covers both the damage and the cost to repair the source. Liability coverage should reflect the actual risks at your property, whether that means a pool, hot tub, or a dock on a Washington lake that guests or neighbors might use. If your second home is in a coastal area or wildfire-prone region, windstorm and fire coverage deserve specific attention rather than relying on standard limits.

Comparing Carriers and Coverage Options

The Hartford and Allstate both offer specialized second home policies that address these gaps. Coverage limits matter more than premium alone; a $300,000 dwelling limit might sound adequate until a major loss shows it falls far short of replacement costs in Washington’s appreciated real estate market. Obtaining quotes from three or four insurers annually typically uncovers savings of hundreds of dollars, and rates shift yearly as competitors adjust their pricing to gain business.

Strategies to Reduce Your Premium

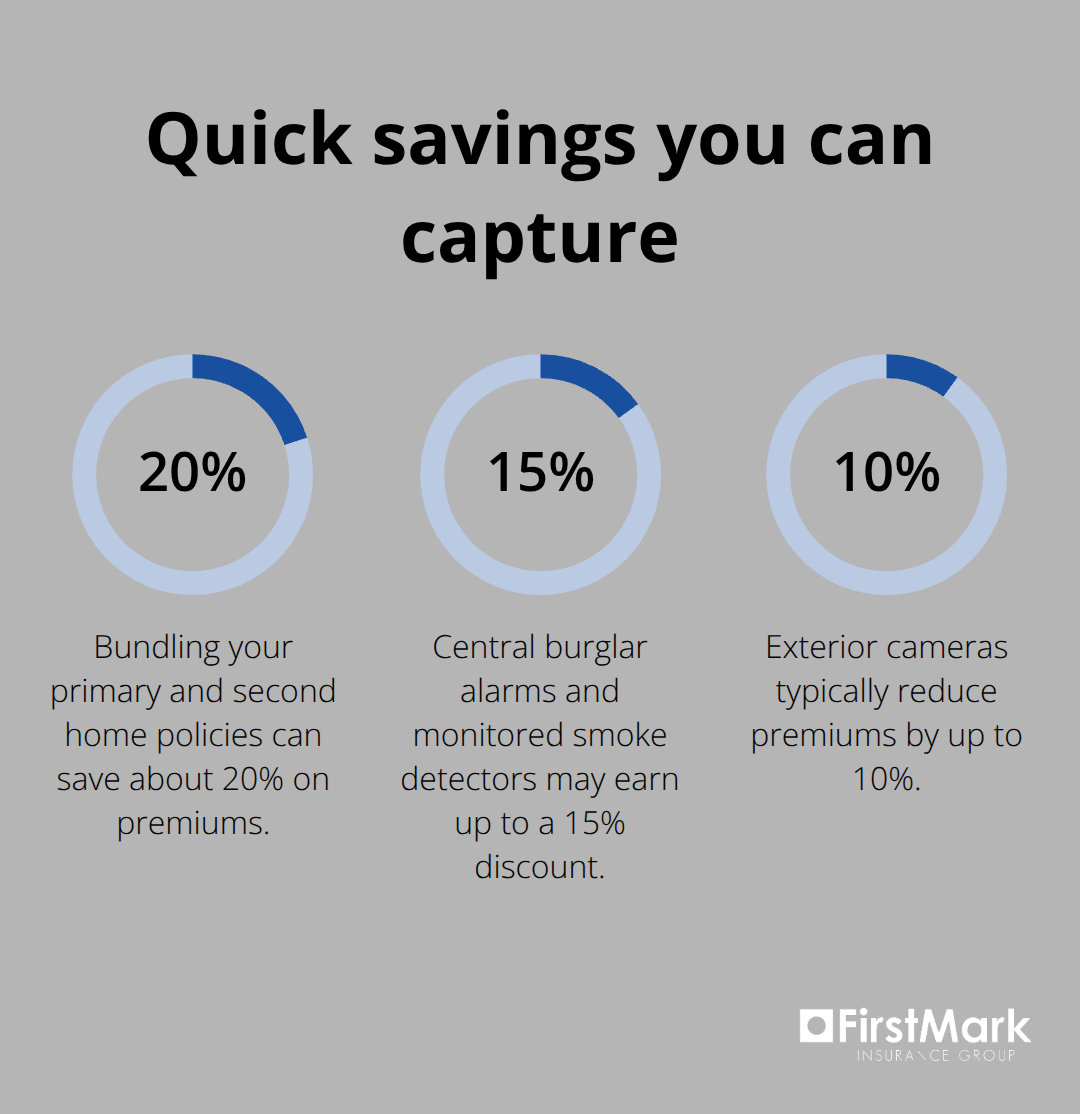

Bundling your primary and secondary home policies together saves approximately 20 percent on premiums, though exact discounts vary by insurer, making it worth shopping multiple carriers to find your best combination rate. Security improvements directly reduce what you pay monthly: installing water-leak sensors, central burglar alarms, smoke detectors, and exterior cameras signals to insurers that you take risk seriously and qualifies you for measurable discounts. If your second home sits in an HOA community, some insurers offer additional discounts that don’t appear unless you mention that detail. Gathering detailed property information before shopping prevents delays and ensures you’re comparing true apples-to-apples pricing across carriers-the year built, square footage, construction type, roof condition, proximity to water, and any recent upgrades all factor into accurate quotes.

Moving Forward With Your Coverage Strategy

The specific protections you select depend on your property’s location, occupancy patterns, and the amenities that create liability exposure. Understanding these gaps and options positions you to make informed decisions about which coverage actually protects your investment. The next section examines the cost factors that shape your premium and reveals which money-saving strategies deliver real value without compromising protection.

What You Actually Pay for a Second Home

Second home insurance costs roughly two to three times more than standard homeowners coverage, and understanding why reveals where you can control expenses without sacrificing protection. The typical second home in Washington is valued around $475,000 according to Redfin data, substantially higher than the average primary residence at approximately $375,000, which alone drives premiums upward. But vacancy is the real cost driver. Insurers charge more because unoccupied homes face documented higher risks of theft, water damage from frozen pipes, and liability claims that go undetected for weeks. A standard homeowners policy averaging $1,754 annually becomes a $3,500 to $5,000 annual expense for second home coverage, depending on location and occupancy patterns. Coastal properties near Puget Sound or wildfire-prone areas east of the Cascades pay significantly more due to weather exposure. Your property’s age matters too-homes built before 1950 cost more to insure than newer construction, and log cabins or historic properties face premium increases of 15 to 25 percent because they present greater loss severity. The distance between your primary residence and second home affects rates as well; a cabin three hours away costs less to insure than one across the state where you visit quarterly.

Where Bundling Delivers Measurable Savings

Combining your primary and secondary home policies under one insurer saves approximately 20 percent on total premiums, though the exact discount varies by carrier and your specific coverage selections. If you also carry auto or umbrella insurance, adding second home coverage to an existing relationship often unlocks additional discounts that stack together. Allstate, The Hartford, and Farmers all offer bundled pricing that rewards consolidation, but you cannot assume one insurer’s bundle discount matches another’s. Shopping three carriers annually takes roughly 90 minutes and typically uncovers $300 to $800 in annual savings through competitive pricing or loyalty discounts you did not know existed. Obtain quotes on your exact property details-square footage, year built, construction materials, roof condition, and proximity to water-because rough estimates produce inaccurate comparisons. Some insurers offer online quote tools that take 15 minutes; others require phone conversations with agents who ask detailed questions about your occupancy schedule and security features. The bundling discount only matters if the base rate is competitive, so resist the temptation to consolidate with your current carrier without shopping alternatives first.

Concrete Actions That Lower Your Premium

Water-leak sensors cost $200 to $400 installed and reduce your annual premium by $150 to $250 at most insurers, delivering payback in under two years while protecting against the most common claim for vacant properties. Central burglar alarms and monitored smoke detectors similarly qualify for discounts ranging from 5 to 15 percent depending on the carrier. Exterior cameras provide visible deterrence and typically earn you a 5 to 10 percent reduction.

Install these measures before obtaining quotes so your premium reflects actual risk reduction rather than potential improvements. If your second home sits within an HOA community, mention this detail explicitly because some insurers offer HOA discounts of 5 to 8 percent that do not appear in standard quotes. Upgrade your roof, replace outdated electrical systems, or install new plumbing in older homes to qualify for additional discounts that justify the upfront investment beyond just improving the property itself. The first 72 hours after you make these improvements matter-notify your insurer immediately so they can adjust your premium, and request a property inspection if the carrier offers one, since documented improvements sometimes unlock discounts that estimates alone cannot secure.

Final Thoughts

Secondary home insurance in Washington requires moving beyond generic homeowners policies to coverage specifically designed for seasonal occupancy. Occupancy patterns determine your coverage needs far more than property type or location alone-a lake house you visit monthly faces different risks than a mountain cabin you check twice yearly. Your lender requires coverage, but they won’t accept a standard policy with occupancy clauses that void protection during vacant periods, which makes second home policies fundamentally different from the coverage protecting your primary residence.

Bundling your policies saves approximately 20 percent on premiums, water-leak sensors and security improvements deliver measurable discounts, and shopping multiple carriers annually typically uncovers hundreds of dollars in savings. Gather your property details, obtain quotes from at least three carriers, and document any security improvements before finalizing coverage. Request bundling discounts explicitly, mention HOA membership if applicable, and plan to re-shop annually because rates shift and new discounts emerge.

At FirstMark Insurance Group, we work with top insurance providers to present you with choices that fit your specific situation at the best available pricing. We take time to understand how you use your Washington property and what protection actually matters for your circumstances. Contact FirstMark Insurance Group to discuss your second home situation and discover coverage that protects your investment without unnecessary expense.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation