Home Insurance That Helps Protect What Matters Most.

We don't just find you the lowest price — we build a policy that holds up when you need it most. Our agents compare options across 20+ top-rated carriers to find you the right coverage at the best value.

THE FIRSTMARK CHALLENGE

A better way to review coverage.

Four simple steps. Zero obligation.

Have A Conversation.

We shop the markets.

Review the results.

You decide.

- Licensed in 39 states

- 20+ Insurance Carriers

- Headquartered in Edmonds, WA

- Independent & Unbiased

A better way to review coverage.

The Firstmark Challenge

Our simple, guided process makes reviewing your insurance easy. We take the time to understand your needs, compare options across top carriers, and present clear results—so you can make a confident decision.

01

Have A Conversation

02

We Shop The Markets

03

Review The Results

04

You Decide!

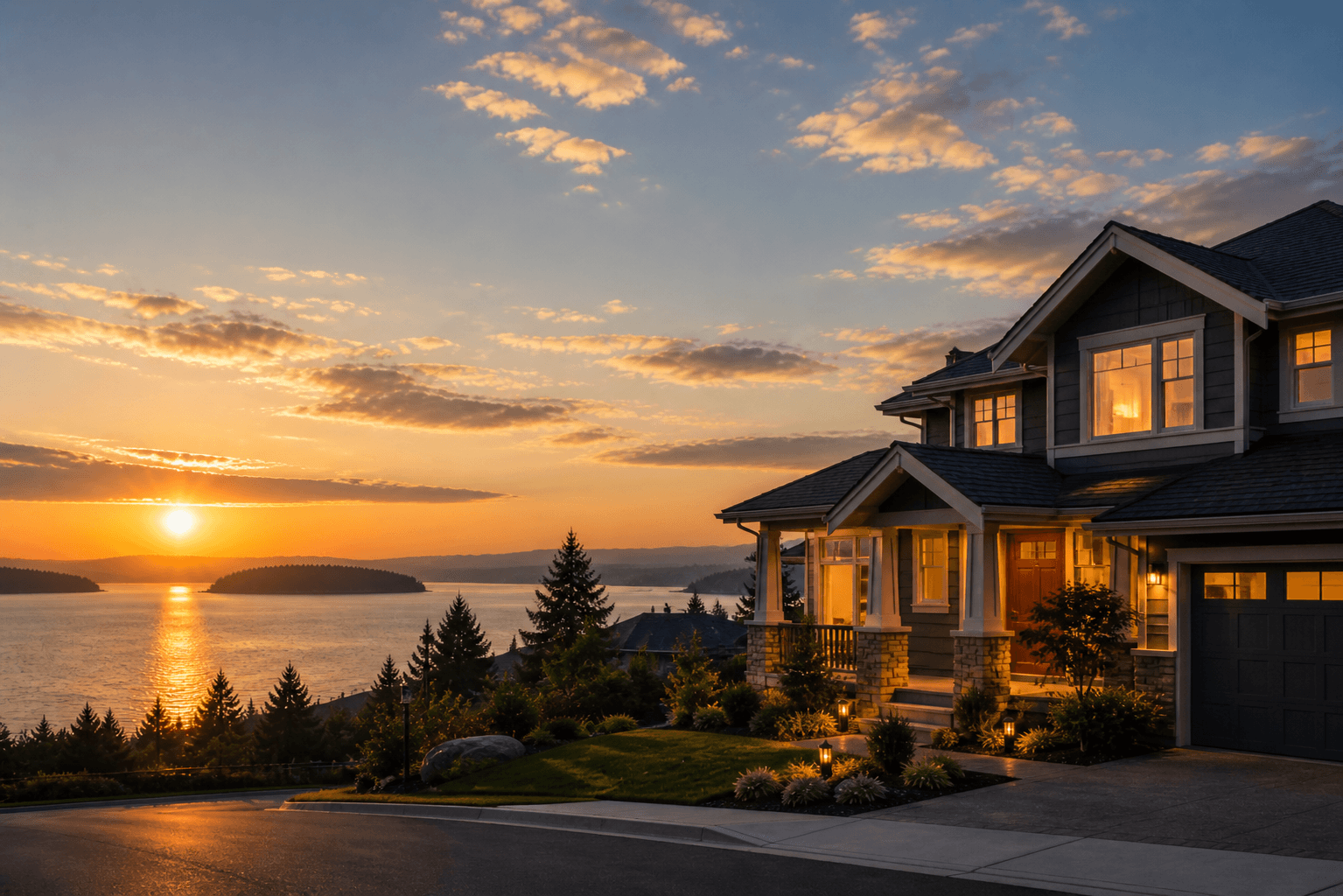

Your Home Is One of Your Biggest Investments—Your Coverage Shouldn’t Be Complicated

With FirstMark Insurance’s dedicated team, you get local experts comparing coverage from over 20 insurance carriers to help protect your home, belongings, and financial stability—with strong coverage and competitive pricing.

Homeowner’s insurance doesn’t just protect your house and property, it also protects your belongings, yourself and your guests. You’ve put a lot of hard work into providing a home for yourself and your family. FirstMark will find the best combination of homeowners insurance coverage, value, and price to protect your hard earned investment.

Standard Coverage

Dwelling

Coverage for your dwelling and attached structures such as garages & decks.

Separate Structures

Coverage for a separate garage, gazebo or a tool shed.

Contents

Your personal property such as furniture, electronics, clothes, and dishware. Some exclusions apply for high-value jewelry, artwork, guns & furs.

Loss of Use

Pays additional costs of living away from your home if you cannot live there due to covered damage.

Liability

Covers lawsuit expenses and damage caused by you or your dependents to third parties or their property.

Medical Payments

Provides no-fault medical coverage and in the event, a friend or neighbor is injured on your premises.

Popular Coverage Options

Identity Recovery

Coverage to help cover the cost of restoring your identity if you’re the victim of identity theft.

Valuable Articles

If you have valuable keepsakes like fine art, jewelry, antiques, and other collectibles, like your wedding ring or your grandmother’s Victorian sideboard and crystal stemware set, you may need extra protection. With valuable articles coverage, belongings you specify are protected by an agreed dollar amount, and there is no deductible.

Equipment Breakdown

Equipment breakdown coverage will replace covered appliances with the same kind and quality in the event of an unexpected mechanical or electrical breakdown not caused by normal wear and tear or corrosion.

Earthquake

Losses caused by earthquakes are excluded by homeowners’ policies, which means your home and contents would not be covered in the event of an earthquake. Do you need an earthquake policy?

Earthquake, Landslide and Flood (DIC Policy)

Losses caused by landslide, earthquake and flood are excluded on all homeowner’s policies. If your home is in the path of a potential landslide, please contact us today so we can discuss the best policy for you.

Water/Sewer Line Coverage

What is water/service line coverage?

Service line coverage is a type of insurance that reimburses you for damage to utility lines that you’re responsible for as the homeowner. It can be packaged with homeowner's insurance for a small additional premium. It provides coverage for common causes of service line failure up to a limit of $12,000, subject to a $500 deductible. Includes repair or replacement with environmentally friendly materials, excavation costs, expediting expenses, and coverage for outdoor property.

How does water/service line coverage work?

As the homeowner, you’re on the hook financially for subterranean lines or pipes running through your property; if your water pipes crack or your power line is severed, it’s your responsibility to fix. Standard homeowners' insurance typically won’t cover broken utility lines, but homeowners have a couple of options for insuring this potentially expensive home maintenance issue — the costs of which run homeowners an average of $2,587, according to one estimate.

Some examples of the types of service lines covered include communications, compressed air, drainage, electrical power, heating, waste disposal and water. This coverage does not include septic systems or on-site wells.

In the event of a line or pipe leak or break or rupture, service line coverage will generally cover the costs of repairing or replacing the line as well as the excavation and landscape restoration after necessary repairs are complete. Another perk of service line coverage is that in many cases you can utilize the same convenient claims service that’s available for standard home insurance claims, such as 24/7 claim reporting, a curated selection of licensed repair companies, in-house claim adjusters, and more.

Among the companies that provide service line coverage, you’ll generally see it offered in amounts of $10,000 and $25,000, although higher and lower coverage amounts may also be an option depending on the carrier.

Home Insurance Discounts & Savings

Get the coverage you need to protect your home and belongings with our customizable Homeowners Insurance options.

Get a Package Deal

Save up to 15 percent when you combine your homeowners and auto policies as a FirstMark Package.

Multiple Policy Discount

Save even more with a multiple policy discount when you also add coverage for your motorcycle, boat, or RV.

Less Than 10 Years Old

Qualify for a newer home discount when your house is less than 10 years old.

Choose a Higher Deductible

A higher deductible will lower how much you pay for your home insurance premium by shifting part of the loss payment to you. For example, if you have a $500 deductible, you’ll need to pay the first $500 of a loss out of your own pocket. A higher deductible will lower your home insurance bill but will also increase how much you’ll end up paying yourself if you file a claim.

FAQs

What is homeowner’s insurance?

Homeowner’s insurance protects one of life’s biggest investments. Should a tree fall through your roof or a fire break out in the kitchen, insurance for your home helps cover the cost to repair or rebuild. It also may cover other buildings on your property like a garden gazebo or storage shed. If the damage is extensive enough to prevent you from living in your home, homeowner’s insurance also helps cover the costs of temporary housing and living expenses.

I’m thinking about buying my first home. Am I required to have insurance?

Lenders almost always require first time buyers to purchase insurance.

Does my home insurance cover damage caused by earthquake or flood?

No. A standard homeowners policy does not generally cover damage caused by earthquake and floods. These sources of damage require additional coverage or a separate policy. If you live in an area that is prone to these types of events, talk an agent about making sure you’re properly covered.

What is the difference between water damage and flood damage?

The damage can be similar but the cause is different.

Water damage is usually caused by water coming from something like a burst pipe, an overflowing toilet, a dishwasher that leaks all over the kitchen floor, or a roof that leaks after a hard rain.

Flood damage is caused by water coming from something like an overwhelmed levee that breaks, a clogged drainage system, a river or lake that overflows or even just the ground being inundated with too much water after a torrential storm. Water seeping into your basement after a heavy rain or winter runoff is usually also considered flood damage.

What is a flood?

A flood is a general and temporary condition where two or more acres of normally dry land or two or more properties are inundated by water or mudflow.

What are home contents?

Home contents are the things inside your home not permanently fixed to the walls, ceiling or floor. Your couch, television, carpet, refrigerator, dining room table and floor lamp are examples of home contents.

We recommend keeping an inventory of your home contents that you can refer to in the event of a claim. Our home inventory app with free cloud storage makes it easy.