Waterfront properties face unique risks that standard homeowners insurance often doesn’t cover. Storm surge, flooding, and coastal erosion can cause devastating financial losses for unprepared property owners.

We at FirstMark Insurance Group see these challenges daily. Understanding waterfront property insurance options protects your investment and provides peace of mind against nature’s unpredictable forces.

What Specific Risks Face Your Waterfront Property

Waterfront properties face three primary threats that can destroy your financial investment within hours. Flood damage represents the most expensive risk, with the National Oceanic and Atmospheric Administration reporting that storm surges push seawater miles inland and affect properties previously considered safe. Standard homeowners insurance excludes flood coverage entirely, which leaves property owners exposed to average flood claims that exceed $42,000 according to FEMA data. Water intrusion damages electrical systems, foundations, and personal belongings while it creates mold problems that persist for years after the initial flood event.

Storm Surge Creates Immediate Destruction

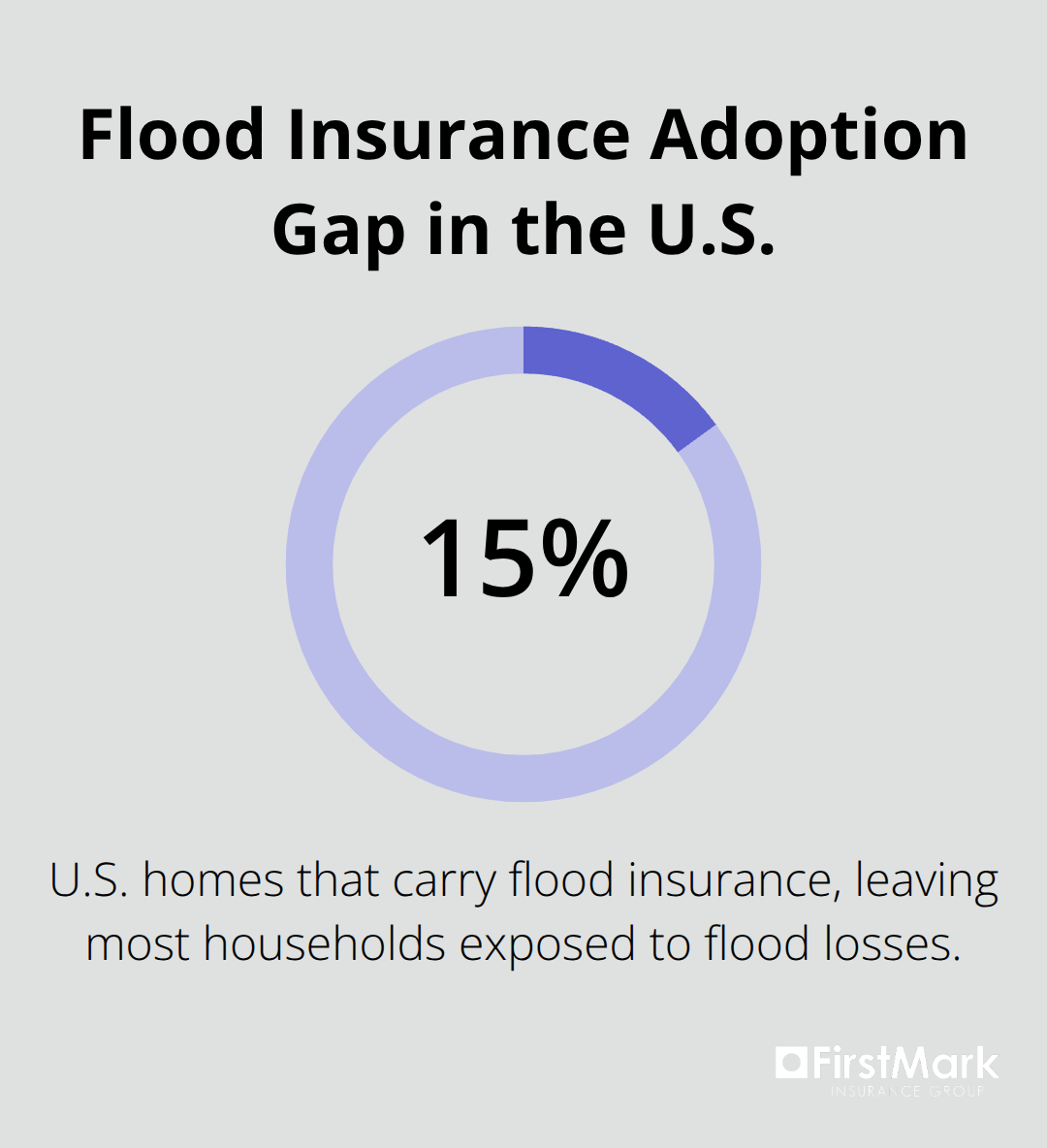

Hurricane storm surge poses the greatest single threat to coastal properties, with Category 3 storms that generate surges exceeding 12 feet above normal tide levels. The Insurance Information Institute reports that only 15% of American homes carry flood insurance, which creates a massive protection gap for waterfront owners. Storm surge arrives faster than most evacuation timelines allow, so preparation becomes the only viable defense strategy. Properties within 500 feet of shorelines face the highest surge risks, while elevation certificates determine your exact vulnerability level and insurance requirements.

Coastal Erosion Undermines Property Values

Coastal erosion permanently reduces property values through foundation damage and land loss that insurance cannot replace. The coastal housing crisis affects waterfront foundations as homes lose value and see their property taxes reduced, potentially impacting the local economy. Properties lose an average of 2-4 feet of shoreline annually in high-erosion zones, with some areas that experience 10+ feet of annual loss. Seawall construction costs range from $150-$800 per linear foot, while emergency repairs after storm damage can exceed $50,000 for typical residential properties.

Climate Change Accelerates Risk Exposure

Climate change increases the frequency and intensity of weather-related losses that affect coastal properties (with 2023 extreme climate events causing upwards of $25 billion in damage). Rising sea levels compound existing flood risks while more intense storms create higher storm surges than historical data predicted. Properties that seemed safe from water damage now face regular flood threats, which makes traditional risk assessment models obsolete for waterfront locations.

These escalated risks require specialized insurance coverage that standard homeowners policies cannot provide.

Which Insurance Policies Actually Protect Waterfront Properties

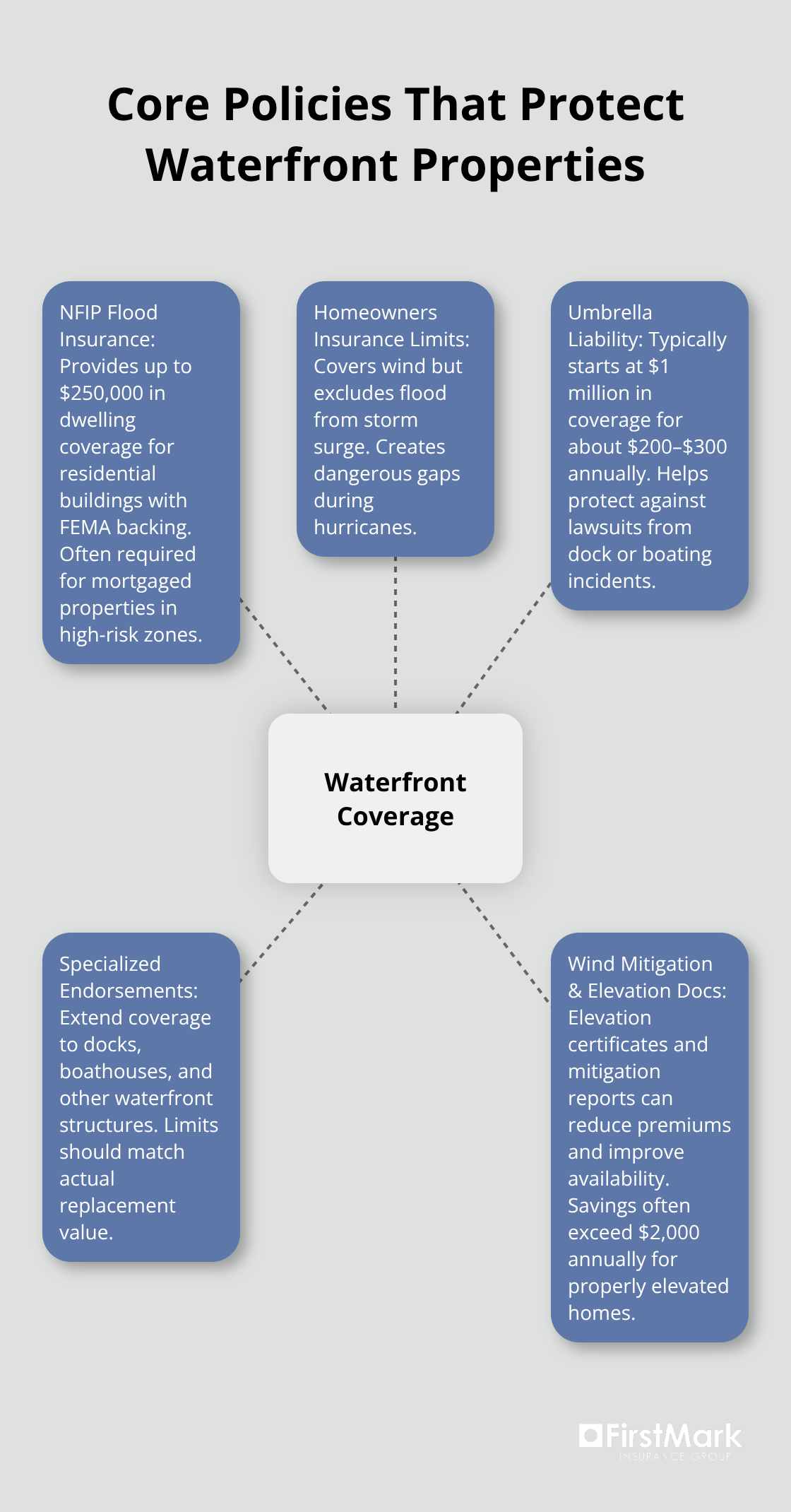

Standard homeowners insurance fails waterfront property owners when they need protection most. These policies explicitly exclude flood damage, which represents the primary threat to coastal properties. The National Flood Insurance Program provides the foundation for waterfront protection and offers up to $250,000 in dwelling coverage for residential buildings and up to $500,000 for non-residential buildings through FEMA-backed policies. NFIP premiums average $888 annually according to FEMA data, but rates vary dramatically based on flood zone classifications and property elevation. Properties in high-risk zones AE and VE face mandatory flood insurance requirements when mortgage lenders finance the purchase, while X-zone properties receive significantly lower rates despite still facing flood risks from extreme weather events.

Homeowners Insurance Creates Dangerous Coverage Gaps

Traditional homeowners policies cover wind damage from hurricanes but exclude water damage from storm surge, which creates dangerous coverage gaps for waterfront owners. Insurance companies have tightened coverage requirements in coastal markets, with numerous insurers exiting Florida over the past three years due to elevated climate risks. Wind mitigation reports become essential for property owners who want to secure coverage and reduce premiums, as these reports demonstrate a property’s resilience against storm damage. Properties without these certifications face limited coverage options and significantly higher premiums, often forcing owners into state-backed insurance programs like Citizens Property Insurance or FAIR Plans that provide basic coverage at elevated costs.

Umbrella Policies Bridge Critical Protection Gaps

Umbrella insurance provides additional liability protection beyond standard homeowners policies, which becomes vital when waterfront properties attract visitors and recreational activities. These policies typically start at $1 million in coverage for approximately $200-300 annually and offer protection against lawsuits from dock accidents, boating incidents, or property-related injuries. Waterfront properties face higher liability exposures due to water access and require coverage that extends beyond basic homeowners limits to protect against catastrophic legal judgments.

Specialized Endorsements Address Unique Waterfront Risks

Secondary structures like boathouses and docks require specialized coverage that standard policies often limit or exclude entirely. Boathouses typically fall under secondary structures coverage, but policy limits may not match the actual replacement value of these expensive structures. Docks present classification challenges as insurers treat permanent structures differently from seasonal installations, with coverage limits that should align with the dock’s actual value. Property owners must work with experienced agents to verify adequate coverage for all waterfront amenities and structures that add significant value to their investment.

The cost of these comprehensive insurance solutions varies dramatically based on specific risk factors that affect each waterfront property differently.

What Drives Your Waterfront Insurance Costs

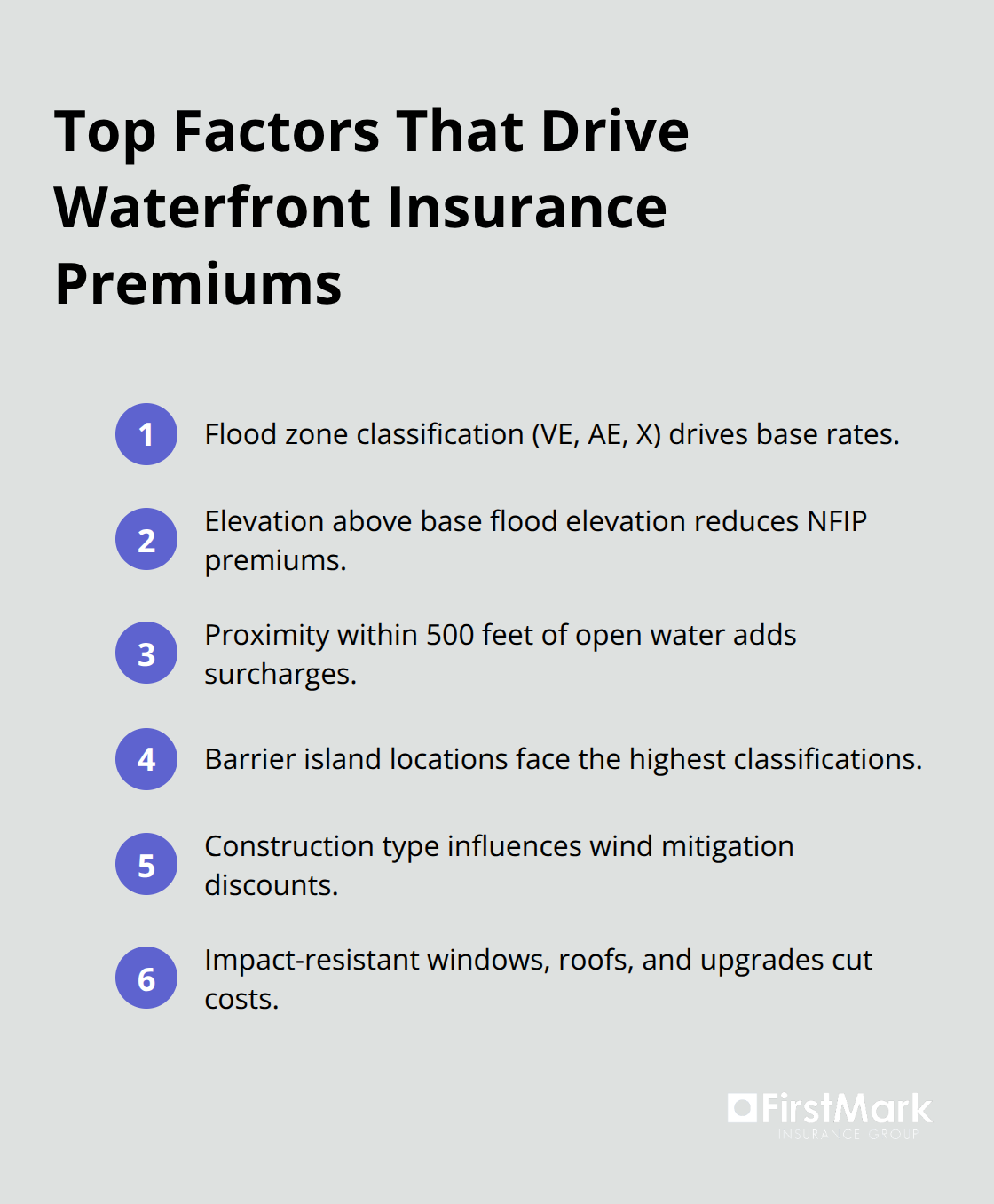

Insurance companies calculate waterfront property premiums through precise risk assessment formulas that examine flood zone classifications, property elevation, and construction materials. Properties in flood zone VE face the highest insurance premiums due to extreme wave action exposure, while AE zones experience moderate flood risks that still require mandatory coverage for mortgaged properties. Elevation certificates reduce insurance costs significantly when properties sit above base flood elevation levels, with annual savings that often exceed $2,000 for properly elevated structures. Construction materials directly impact wind mitigation discounts, as concrete block construction receives better rates than wood frame structures in coastal environments.

Premium Calculations Start with Location Analysis

Insurance underwriters analyze historical storm data, proximity to water bodies, and local building codes to establish base premium rates for each property location. Properties within 500 feet of open water face surcharge penalties that increase premiums by 25-40% compared to inland locations, while structures on barrier islands experience the highest rate classifications due to evacuation limitations and storm exposure.

Recent legislative actions in Florida impact insurance availability and costs (which makes location-specific rate analysis essential for accurate premium estimates). Wind mitigation reports demonstrate structural resilience through features like reinforced windows, updated seawalls, and impact-resistant materials that qualify for premium discounts from 10-45% based on specific upgrades installed.

Construction Upgrades Deliver Measurable Premium Reductions

Seawall reinforcements, elevated foundations, and hurricane systems provide concrete premium reductions that insurance companies calculate through standardized discount schedules. Properties with elevation certificates that show structures above base flood elevation receive NFIP premium reductions that average $1,200-$3,500 annually based on the elevation differential achieved. Impact-resistant windows and doors qualify for wind mitigation discounts, while newer roof installations with proper hurricane clips and enhanced attachment methods reduce wind coverage premiums substantially.

Mitigation Investments Pay for Themselves

These mitigation investments typically pay for themselves within 3-7 years through reduced insurance costs while they increase property values and improve storm survival rates for waterfront structures. Hurricane straps, reinforced garage doors, and secondary water barriers create additional premium discounts that compound over time (with some properties achieving total premium reductions exceeding 50% through comprehensive upgrades). Properties that combine multiple mitigation features often qualify for preferred underwriter programs that offer better coverage options and more competitive rates than standard coastal policies provide.

Final Thoughts

Waterfront property insurance demands a strategic approach that combines NFIP flood coverage with comprehensive homeowners policies and umbrella protection. Property owners who obtain elevation certificates and wind mitigation reports achieve premium reductions that frequently exceed $2,000 annually. These documents prove property resilience and unlock significant cost savings while they provide better coverage options.

Experienced agents help waterfront owners navigate complex insurance markets and secure appropriate coverage at competitive rates. We at FirstMark Insurance Group specialize in waterfront property insurance and work with multiple carriers to find coverage solutions that match your specific coastal property needs. Our team understands the unique challenges that waterfront properties face and helps clients prepare for changing market conditions.

Climate change reshapes coastal risk profiles and forces annual policy reviews to maintain adequate protection (as properties once considered safe now face regular flood threats). Insurance companies continue to exit high-risk markets while they tighten coverage requirements for remaining policies. Proactive waterfront owners anticipate these changes and maintain comprehensive coverage through market fluctuations to protect their valuable investments.