Business Interruption Insurance That Keeps You Running

When your operations pause, your expenses don’t. Business Interruption Insurance helps replace lost income and cover ongoing costs, so you can stay afloat and get back to business faster.

THE FIRSTMARK CHALLENGE

A better way to review coverage.

Four simple steps. Zero obligation.

Have A Conversation.

We shop the markets.

Review the results.

You decide.

- Licensed in 39 states

- 20+ Insurance Carriers

- Headquartered in Edmonds, WA

- Independent & Unbiased

A better way to review coverage.

The Firstmark Challenge

Our simple, guided process makes reviewing your insurance easy. We take the time to understand your needs, compare options across top carriers, and present clear results—so you can make a confident decision.

01

Have A Conversation

02

We Shop The Markets

03

Review The Results

04

You Decide!

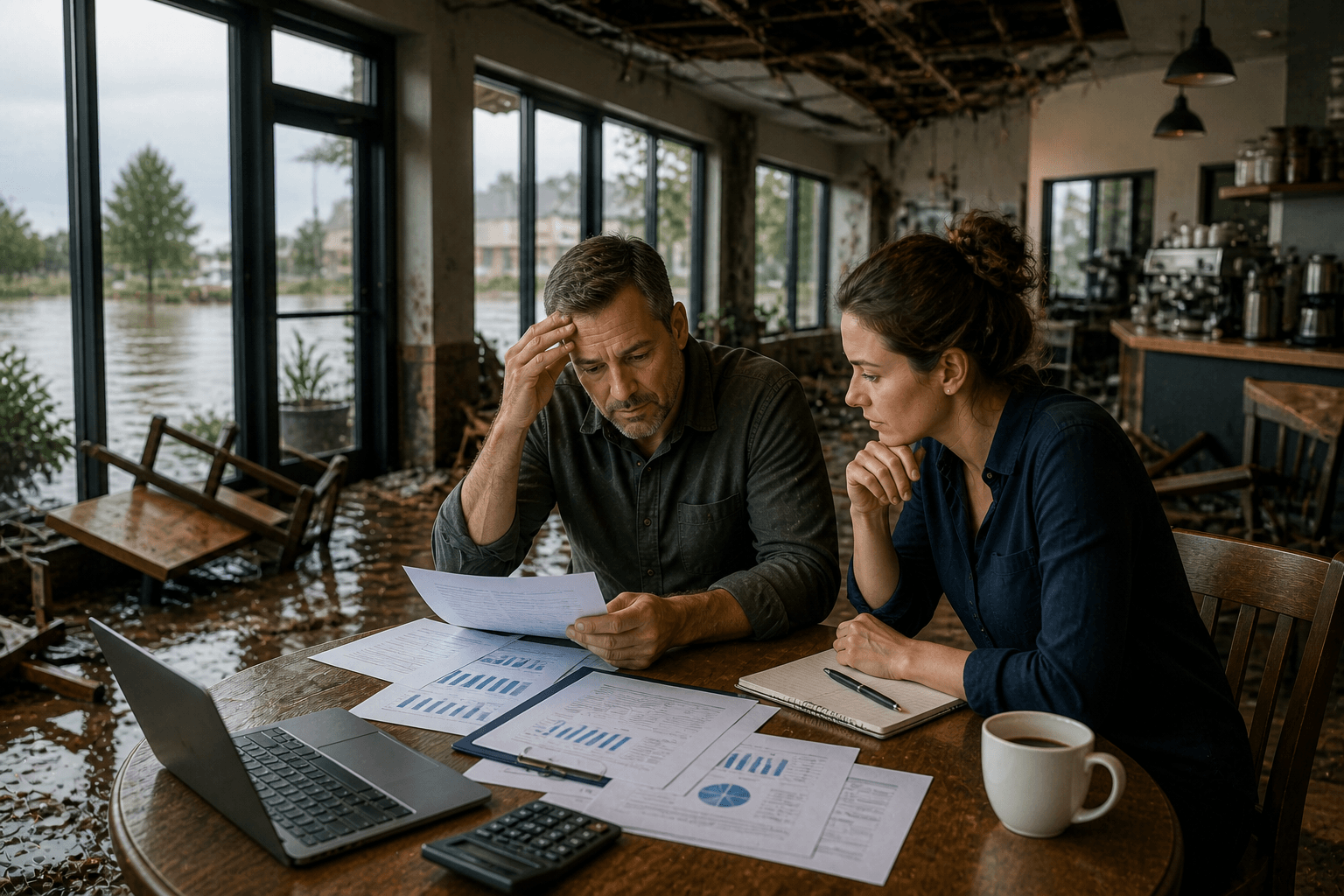

When Business Slows Down—Your Protection Shouldn’t

With FirstMark Insurance’s dedicated team, you get local experts comparing options from over 20 insurance carriers to build business interruption insurance that helps replace lost income, cover ongoing expenses, and keep your business moving forward—delivering strong protection with great coverage and pricing.

Why having Business Interruption Insurance is Important

Business Interruption Insurance—often referred to as Income Protection—provides crucial financial support when a business cannot operate due to a covered event. When unexpected damage or disruptions force a temporary shutdown, this coverage helps replace lost income and pay ongoing expenses such as payroll, rent, utilities, loan payments, and other essential operating costs. By maintaining cash flow during downtime, businesses can stay stable, retain key staff, and resume operations more smoothly.

How Business Interruption Coverage Works

Business interruption insurance is typically triggered when direct physical damage occurs to insured property, making it impossible to conduct normal business activities. Covered events may include fires, wind and storm damage, vandalism, or certain types of equipment breakdown, depending on the policy. Once triggered, the policy compensates the business for income lost during the restoration period—the time it takes to repair or rebuild the damaged property.

In addition to lost income, coverage often includes:

- Extra Expense Coverage: Reimbursement for additional costs incurred to keep the business running or reduce downtime—such as renting a temporary workspace, relocating operations, or leasing replacement equipment.

- Ongoing Fixed Costs: Payment for essential expenses that continue despite the shutdown, including taxes, salaries, insurance premiums, and utilities.

- Possible Civil Authority Coverage: In some policies, income loss may be covered if access to your business is restricted by a local government order due to damage in the surrounding area.

However, it’s important to note that business interruption insurance does not typically cover losses from pandemics, utility failures, or power outages unless these risks are specifically added by endorsement.

Why Adequate Coverage Matters

Calculating proper coverage limits is essential. Businesses must evaluate financial statements, historic income patterns, seasonal fluctuations, and future projections to determine how much income would need to be replaced during a prolonged shutdown. Underinsuring can leave a business vulnerable, while accurate planning ensures a smooth recovery process.

A Key Part of Disaster Recovery Planning

Business interruption insurance is a foundational element of a strong disaster recovery plan. Without it, companies may struggle to cover expenses during extended closures, risking layoffs, lost customers, and long-term financial damage. With the right policy in place, businesses can stabilize quickly, rebuild confidently, and return to full operations without losing momentum or market share.