Business lawsuits can devastate companies financially, with average commercial liability claims reaching $54,000 according to recent industry data. Standard business insurance policies often fall short when facing major legal judgments.

A business insurance umbrella policy provides additional liability protection beyond your primary coverage limits. We at FirstMark Insurance Group see too many businesses operating without this safety net, leaving their assets vulnerable to catastrophic losses.

How Does Business Umbrella Insurance Actually Work

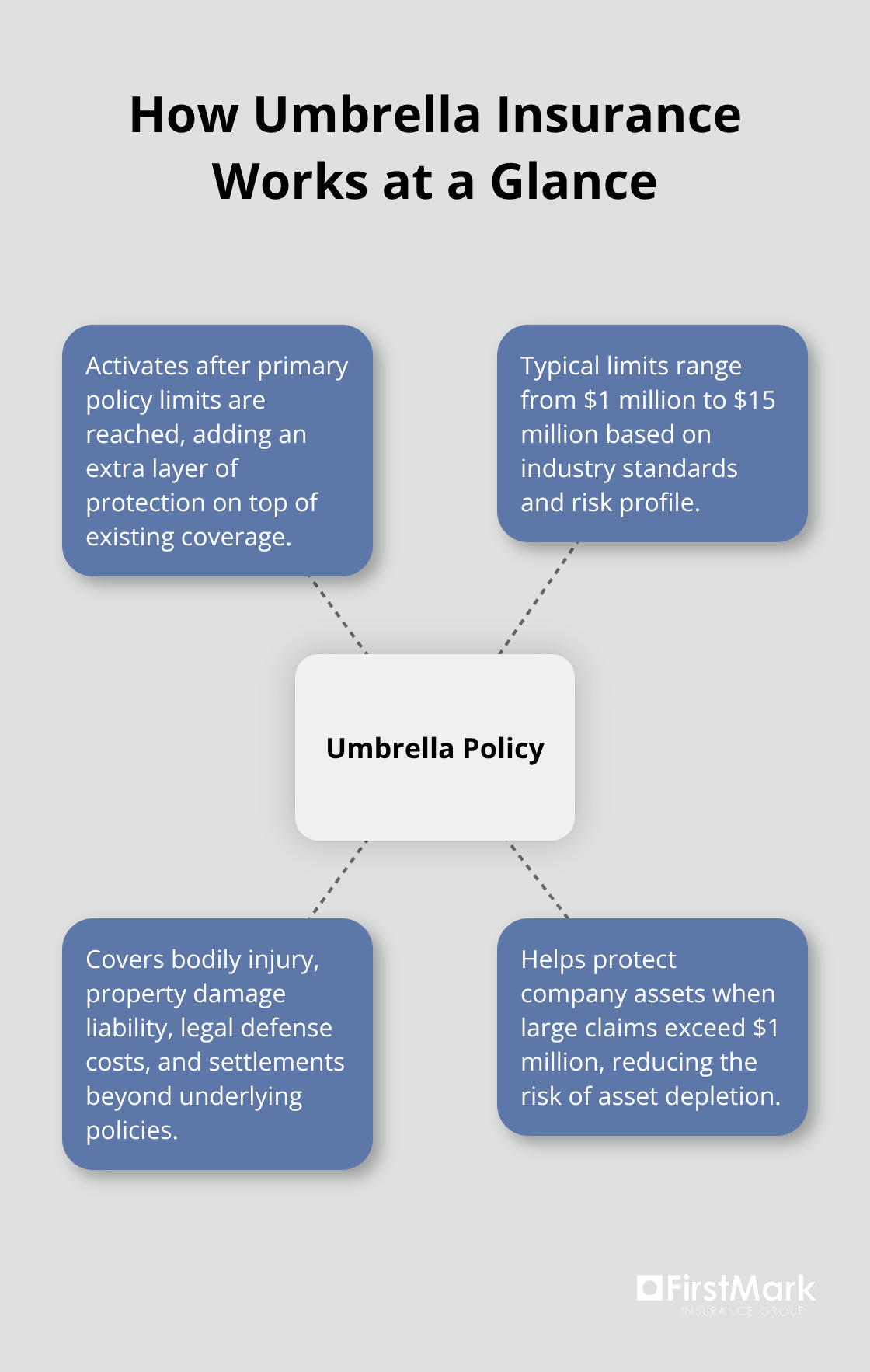

Business umbrella insurance activates when your primary liability policies reach their limits and provides additional coverage that ranges from $1 million to $15 million according to industry standards. The policy covers bodily injury claims, property damage liability, legal defense costs, and settlements that exceed your general liability, commercial auto, or employer liability limits. Hartford data shows that businesses frequently face claims that exceed $1 million, which makes umbrella coverage essential for protection of company assets from complete depletion.

Coverage Beyond Standard Policies

Commercial umbrella insurance extends protection across multiple underlying policies simultaneously, unlike excess liability insurance that only supplements one specific policy. The coverage includes medical expenses from customer injuries, attorney fees from product liability lawsuits, and damages from advertising injury claims. Small business insurance costs an average of $249 per month for comprehensive coverage including business owners policy and commercial auto insurance. The policy excludes professional liability claims, employee injuries that workers compensation covers, intentional misconduct, and damage to your own business property.

Integration with Existing Business Insurance

Your umbrella policy requires underlying coverage like general liability insurance with minimum limits, typically $1 million per occurrence. The umbrella coverage kicks in seamlessly when primary policy limits are exhausted and creates a continuous protection layer without coverage gaps. Insurance companies require businesses to maintain specific underlying policy limits before they issue umbrella coverage, and the umbrella policy terms may be broader than your primary policies, which potentially covers claims that underlying policies exclude.

Cost Factors and Premium Structure

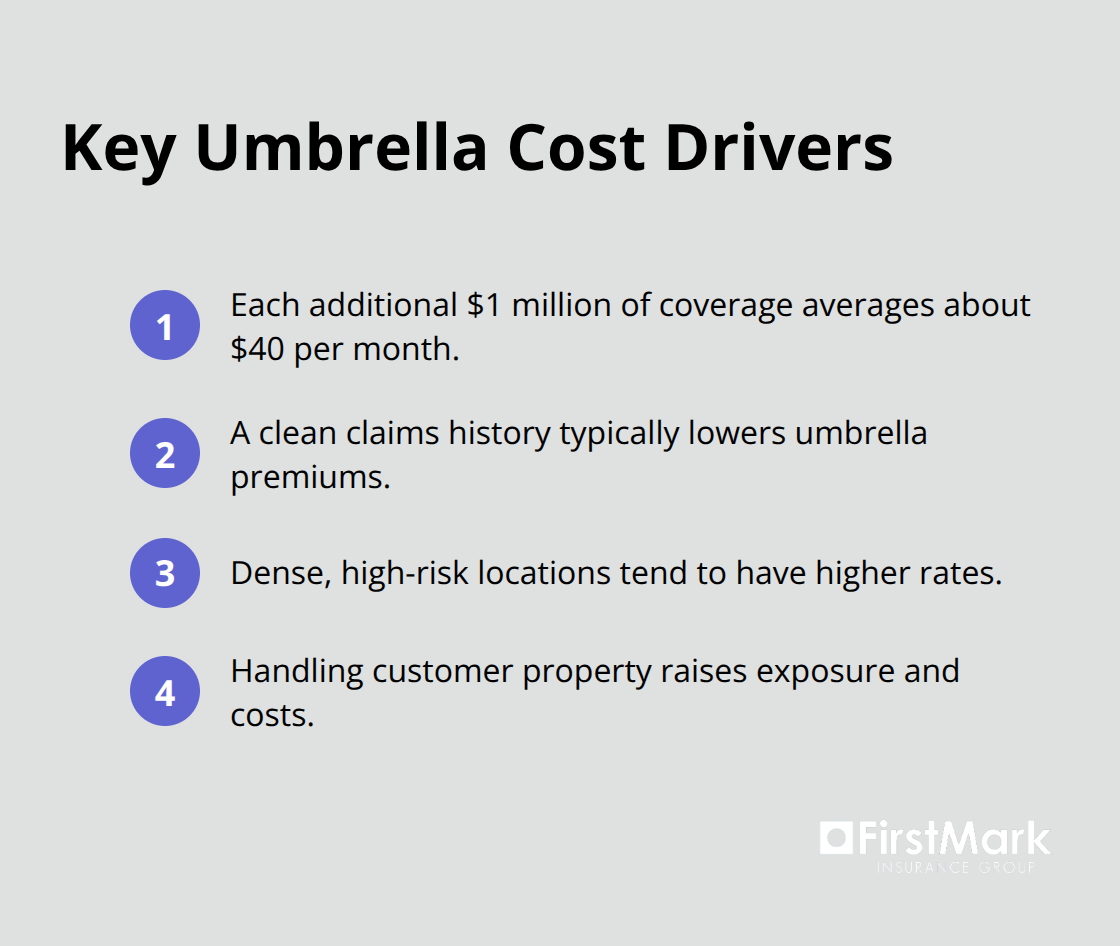

Each additional $1 million of coverage typically costs about $40 per month according to industry data. Previous claims history significantly influences the cost of umbrella insurance, with fewer claims that lead to lower premiums. Business location affects rates (densely populated areas often have higher premiums due to increased risk), and companies that handle customer property frequently face higher premiums due to increased potential for property damage lawsuits.

These cost considerations become particularly important when you evaluate whether your current coverage adequately protects your business assets and revenue streams.

When Your Business Needs Umbrella Coverage

Construction companies face lawsuits that can reach substantial amounts according to industry reports, while restaurants deal with slip-and-fall claims that regularly occur. Manufacturing businesses that operate heavy machinery see property damage claims when accidents occur. These industries cannot afford to operate without umbrella coverage because a single incident can bankrupt the business when primary insurance limits prove insufficient.

High-Risk Industries That Require Extra Protection

Contractors who work on multi-million dollar projects face the highest liability exposure, with general contractors experiencing higher claim rates than other business types according to recent data. Healthcare practices that treat patient injuries need umbrella coverage because malpractice settlements often reach significant amounts, and professional liability policies may not cover all aspects of a claim. Transportation companies with commercial fleets face vehicle accident claims for serious injuries (fleet operators consider umbrella coverage mandatory rather than optional).

Asset Protection Thresholds That Trigger Coverage Needs

Businesses with substantial assets need umbrella coverage because liability judgments can seize company assets, personal guarantees on business loans, and future revenue streams. Real estate companies that own multiple properties face tenant lawsuits when serious injuries occur on their premises. Technology companies with valuable intellectual property and high revenue streams become attractive lawsuit targets and require umbrella protection against claims that could drain company resources.

Revenue-Based Risk Exposure Factors

Companies with higher annual revenue attract larger lawsuit settlements because plaintiffs’ attorneys target businesses with deeper pockets. Service businesses that interact with customers daily face higher liability risks (customer injuries on premises account for a significant portion of commercial liability claims). Professional service firms often face claims that exceed their errors and omissions coverage limits, particularly when client losses involve substantial financial damages.

The amount of coverage your business needs depends on specific risk factors and industry standards that vary significantly across different sectors.

How Much Umbrella Coverage Does Your Business Need

You must calculate your business risk exposure based on total asset value, annual revenue, and industry-specific liability patterns. Businesses with assets that exceed $1 million should carry at least $2 million in umbrella coverage according to insurance industry standards. Companies that generate over $5 million annually face higher lawsuit targets and typically need coverage limits that reflect their increased exposure. Manufacturing businesses with heavy machinery operations require $3-5 million minimum due to severe injury potential, while professional service firms need coverage equal to their largest client contract value plus 50% buffer.

Risk Assessment Beyond Basic Formulas

Your geographic location significantly impacts coverage needs, with businesses in California and New York that face 40% higher liability claims than national averages. Companies with frequent customer interactions need coverage amounts that reflect their daily foot traffic volume – retail stores with 500+ daily visitors should carry minimum $3 million limits.

Contract requirements often dictate coverage amounts, with many commercial clients that demand $2-5 million umbrella policies from vendors. Construction companies that work on projects over $10 million must carry umbrella coverage that matches the project value. The average monthly premium for $1 million umbrella coverage costs $75 for small businesses (each additional million adds approximately $40 monthly).

Industry-Specific Coverage Standards

Healthcare practices need umbrella coverage equal to three times their annual malpractice insurance limits because medical liability claims often exceed primary coverage. Transportation companies with commercial fleets require $5 million minimum coverage due to severe accident potential on highways. Technology companies with substantial intellectual property should carry coverage equal to their annual revenue because patent disputes can result in massive settlements. Restaurant chains need $2 million per location minimum due to food poisoning liability and slip-fall incidents that occur frequently in food service environments (these claims often exceed standard general liability limits).

Asset Protection Calculations

You should evaluate your business assets that include real estate, equipment, inventory, and accounts receivable when you determine coverage amounts. Professional practices with high-value equipment need coverage that protects against total asset loss from a single liability claim. Service businesses with valuable client databases require protection against lawsuits that could force asset liquidation to pay judgments.

Final Thoughts

You must evaluate your business insurance umbrella policy needs through a systematic approach that examines your total assets, annual revenue, and industry-specific risks. Start by calculating your current liability exposure across all business operations, then compare this against your existing policy limits to identify potential gaps. Document all high-risk activities, customer interaction levels, and contractual requirements that may demand specific coverage amounts.

Professional insurance agents become essential when you navigate the complexities of umbrella coverage selection. We at FirstMark Insurance Group help businesses find ideal coverage for their specific needs through comprehensive risk analysis. Professional agents can analyze your risk profile, recommend appropriate coverage limits, and structure policies that provide comprehensive protection without unnecessary costs.

Adequate umbrella coverage extends far beyond immediate lawsuit protection and preserves business continuity during legal challenges. Proper coverage protects personal assets from business liability claims and provides peace of mind that allows you to focus on growth rather than potential financial devastation. Businesses with sufficient umbrella protection maintain their competitive advantage and avoid the operational disruptions that inadequate coverage creates when major claims arise (these disruptions can permanently damage company reputation and market position).