Your vehicle’s insurance needs change with the seasons, yet most drivers keep the same coverage year-round. At FirstMark Insurance Group, we’ve seen how seasonal vehicle insurance can cut costs while keeping you protected when it matters most.

Whether you store a classic car in winter or drive a motorcycle only in summer, adjusting your coverage prevents overpaying for protection you don’t need. This guide walks you through the practical steps to align your policy with how you actually drive.

When Your Driving Changes, Your Coverage Should Too

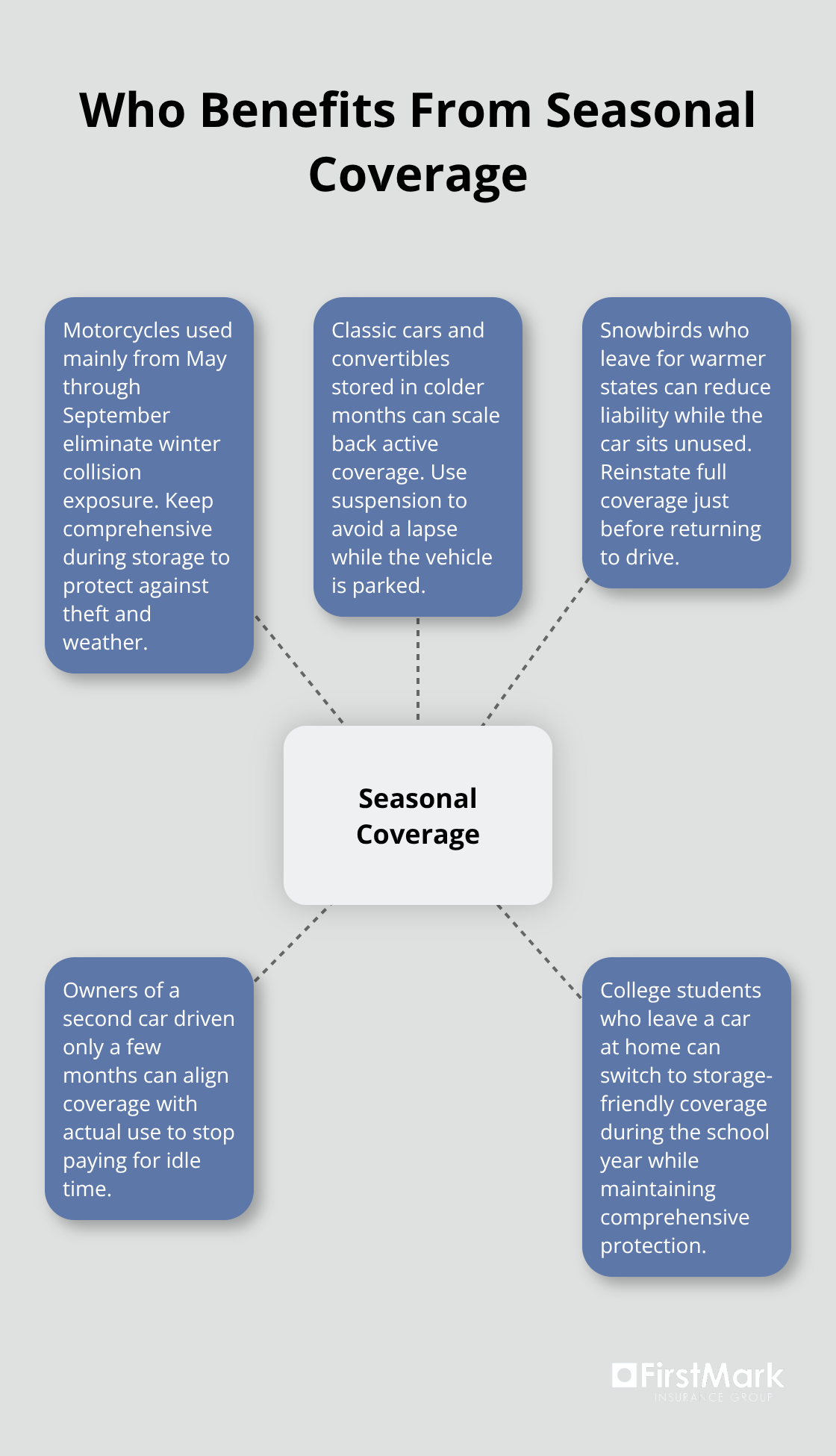

Your insurance costs money whether you drive your vehicle or it sits parked in a garage. Most drivers pay for full coverage year-round even when they only use their car seasonally, which wastes hundreds of dollars annually. The reality is that your actual risk changes dramatically across seasons. A motorcycle that only runs from May through September carries zero collision risk during winter months. A snowbird who leaves for Florida in November doesn’t need the same liability protection while the car sits unused. According to The Zebra’s analysis of over 83 million insurance quotes across the U.S., switching from full coverage to liability-only can reduce your annual premium by roughly $960 to $1,160 depending on your deductible choice. That’s $80 to $100 monthly in savings simply by matching your coverage to your actual usage patterns.

Vehicles Built for Seasonal Use

Convertibles, motorcycles, RVs, and classic cars are the obvious candidates for seasonal adjustments, but many standard vehicles qualify too. If you own a second car that you drive only during certain months, or if you’re a college student who leaves your car at home during the school year, seasonal coverage makes financial sense. The key question isn’t whether seasonal insurance exists-it does-but whether your specific situation justifies the adjustment. You need to assess honestly how many months you actually drive the vehicle and how many months it sits unused. If you anticipate not driving the car for four months or longer, seasonal coverage typically delivers real savings. Some insurers allow you to suspend coverage during non-use months rather than cancel completely, which prevents the insurance gap penalty that affects future rates. The process matters: canceling your policy creates a lapse in your insurance history that raises premiums when you reinstate, while suspension keeps your continuous coverage record intact and avoids these penalties.

The Numbers Behind Seasonal Savings

The math depends on your current full-coverage premium and your state’s requirements. If you’re paying $1,554 annually for full coverage with a $1,000 deductible, that breaks down to $129 monthly. During months you don’t drive, you might reduce to liability-only at approximately $50 monthly. Over six months of non-use, that’s $474 saved compared to $774 in full coverage costs. Your actual savings vary based on your location, vehicle type, age, and driving record, which is why comparing quotes for both seasonal and annual options is essential. Some insurers require formal declaration of which months the vehicle will be active, and failure to disclose accurately can affect claims. Your lender or leasing company may also restrict coverage changes-if you financed the vehicle, the loan agreement typically requires comprehensive and collision coverage regardless of seasonal use. Before you commit to seasonal adjustments, verify what your lender allows and whether your state permits coverage suspension for non-use periods.

Getting Started With Your Agent

An insurance agent can review both seasonal and annual options to identify the genuine savings available for your specific vehicle and usage pattern. Your agent explores offerings from top insurance providers to present you with choices that fit your requirements at the best available pricing. The conversation with your agent should address your actual driving habits, storage plans, and any lender restrictions that apply to your vehicle. This foundation sets you up to make adjustments that reduce costs without creating coverage gaps or violating loan agreements.

How to Adjust Coverage Across Different Seasons

Spring and Summer: Preparing for Active Driving

Spring and summer driving patterns demand different protection than the rest of the year. When temperatures rise and you drive more frequently, your exposure to certain risks increases significantly. Long-distance road trips become common, which means your vehicle faces extended highway exposure, potential tire blowouts from heat stress, and overheating risks that don’t occur during winter storage.

Before a summer road trip, review your policy specifically for long-distance coverage and confirm that roadside assistance is included if you plan to travel far from home. Hot weather can cause tire failures and engine problems that liability-only coverage won’t protect against, so maintaining comprehensive and collision coverage during these months makes financial sense. If you rent a vehicle for summer travel, check whether your existing auto policy or credit card provides rental car coverage before accepting the rental company’s expensive add-ons-the cost difference matters, as rental companies charge $25 to $40 daily for damage coverage that your own policy might already cover.

Fall: Shifting Your Protection Strategy

Fall transitions require you to shift your thinking toward weather preparation rather than summer leisure. As temperatures drop, rain, sleet, and early snow create hazardous driving conditions that increase collision risk substantially. This is when skimping on collision coverage becomes genuinely dangerous, not just financially risky.

Your deductible choice matters more during fall and winter than any other season because accident likelihood rises with weather unpredictability. Choosing a $500 deductible instead of $1,000 costs roughly $200 annually according to The Zebra’s analysis, but that protection pays for itself in a single weather-related accident claim.

Winter Storage: Maximizing Savings Without Sacrificing Protection

Winter storage periods represent your biggest opportunity for cost reduction without sacrificing necessary protection. If your vehicle sits parked for 30 days or longer, contact your agent immediately about suspension options rather than waiting until spring. Suspending coverage during storage can reduce your premium by more than 50% compared to maintaining full coverage on an unused vehicle.

However, suspension doesn’t mean dropping all protection-maintain comprehensive coverage while the car is parked to protect against theft, fire, vandalism, and weather damage. This approach costs roughly $30 to $40 monthly while providing genuine protection for a stored vehicle, compared to $129 monthly for full coverage.

The Critical Difference: Suspension Versus Cancellation

The critical detail most drivers miss is the difference between suspension and cancellation. Suspending your policy preserves your continuous coverage record and avoids insurance penalties when you reinstate. Canceling instead creates a lapse that insurers penalize with higher future premiums, potentially costing you far more than you saved during storage.

Your lender’s requirements matter here-if you financed or leased the vehicle, your loan agreement likely requires comprehensive coverage even during non-use periods, so verify this before adjusting anything. File any claims promptly during seasonal transitions to ensure smoother processing and continued protection without delays.

Transitioning Back to Active Driving

When reinstating coverage for spring driving, schedule the reinstatement date to align with when you actually plan to drive, not weeks earlier. Many insurers allow you to arrange automatic reinstatement on a specific date so you don’t forget and accidentally drive uninsured. Your agent can walk you through the reinstatement process and help you restore the coverage levels that match your spring and summer driving patterns, setting you up to avoid the common mistakes that cost drivers money and protection throughout the year.

Common Mistakes People Make With Seasonal Insurance

Most drivers who switch to seasonal coverage make one critical error: they treat the transition date as a formality rather than a strategic moment that requires active management. The biggest mistake happens when drivers adjust coverage in the wrong direction at the wrong time. You reduce to liability-only in November to save money during winter storage, which makes sense, but then you forget to reinstate collision coverage in April before you actually drive again. That gap between suspension and reinstatement is when accidents happen. According to The Zebra’s data on over 83 million quotes, collision claim costs far more than the premiums you saved by skipping coverage for a few weeks.

Underestimating Weather Risks During Transition Seasons

Fall and spring aren’t low-risk periods-they’re transition zones where temperature swings, rain, and early or late snow create unpredictable driving conditions. Drivers often keep liability-only coverage during these months to stretch their savings, then file collision claims they expected to cover themselves when a wet road causes an accident. The math doesn’t work. A $500 deductible costs roughly $200 more annually than a $1,000 deductible according to The Zebra’s analysis, but one weather-related accident wipes out years of that savings.

Skipping the Policy Review Before Making Changes

Drivers never actually review their policy documents before making changes. Your loan agreement likely requires comprehensive and collision coverage year-round, even during storage periods. Your state may have specific rules about what coverage suspension requires. Your storage location and conditions affect what comprehensive coverage you truly need. Without reviewing these details with your agent, you might make changes that violate your loan terms, create unintended coverage gaps, or fail to protect your vehicle adequately.

Timing Your Transitions Correctly

Contact your agent at least two weeks before any coverage change-before you park the vehicle for winter and before you take it out of storage in spring. This timing gives your agent space to confirm that your changes comply with loan requirements, align with state regulations, and actually deliver the savings you expect. When you reinstate coverage, set it to activate on the exact date you plan to drive, not days earlier. Many drivers set reinstatement dates weeks in advance out of caution, which wastes premium dollars on coverage sitting unused. Your agent can schedule automatic reinstatement on a specific date so you don’t accidentally drive uninsured while waiting for coverage to activate.

Verifying Loan and State Compliance

During the conversation about seasonal adjustments, ask your agent explicitly what happens during the transition period and whether your lender allows the specific changes you want to make. The critical question to ask your agent is straightforward: does this adjustment comply with my loan agreement and state requirements? If your agent hesitates or gives a vague answer, that’s a signal to dig deeper before proceeding.

Filing Claims at the Right Time

If you file a claim during a transition period when coverage is changing, processing delays become more likely because the claim straddles two different policy periods. File any claims promptly before you make coverage changes to avoid complications that could delay payment or create disputes about which policy period covers the loss.

Final Thoughts

Seasonal vehicle insurance works when you treat it as an active strategy, not a passive decision. The real savings come from matching your coverage to your actual driving patterns throughout the year, which requires honest conversations with your insurance agent about when you drive, where you store your vehicle, and what your lender requires. Most drivers waste hundreds of dollars annually by maintaining full coverage on vehicles they barely use during certain months, yet switching from full coverage to liability-only during storage periods saves $80 to $100 monthly, and suspending coverage entirely can cut your premium by more than 50% when your vehicle sits parked for extended periods.

Contact an insurance agent and walk through your specific situation: which months you actually drive, which months the vehicle sits unused, and what coverage your loan agreement demands. Your agent explores offerings from top insurance providers to present you with seasonal options that fit your needs at the best available pricing. Your agent can verify that any changes comply with your state’s requirements and your lender’s restrictions, schedule automatic reinstatement dates so you never accidentally drive uninsured, and confirm that you maintain adequate protection during transition seasons when weather risks spike.

Don’t wait until you’re about to park your vehicle for winter or pull it out of storage in spring to have this conversation. Reach out to FirstMark Insurance Group today to explore how seasonal adjustments can protect your vehicle year-round while keeping your premiums aligned with your actual risk.