Washington sits on one of the most seismically active regions in the United States, making earthquake insurance a practical consideration for homeowners. The earthquake insurance cost in Washington varies significantly based on where you live, your home’s value, and the coverage you choose.

At FirstMark Insurance Group, we’ve helped thousands of Washington residents understand their earthquake insurance options and find affordable protection. This guide breaks down the real costs, shows you how rates differ across the state, and reveals concrete ways to reduce your premiums.

What Drives Your Earthquake Insurance Price in Washington

Your earthquake insurance premium in Washington depends on three primary factors that insurers analyze before quoting you a price. Location, home value, and deductible selection each play a distinct role in what you’ll pay annually for coverage.

Location and Seismic Risk Zone

Where your home sits within the state’s seismic zones matters significantly. Properties in areas closer to active faults like the Puget Sound fault zone cost substantially more than homes in lower-risk regions. The Washington Geological Survey identifies numerous active fault zones across the state, and insurers price coverage based on the likelihood of ground shaking in your specific location. A home in Seattle or Tacoma will cost more to insure than an identical home in Spokane, simply because of proximity to seismic activity.

Your Home’s Value Determines the Coverage Amount

Your home’s replacement cost is the second major driver of your premium. Earthquake insurance companies calculate what it would cost to rebuild your home at current market prices and building code standards. A $400,000 home requires significantly more coverage than a $250,000 home, which means higher premiums. The Washington State Department of Insurance notes that insurers may require a property inspection to verify the home’s condition and construction materials before issuing a quote. This inspection also confirms whether your foundation is bolted to the structure and whether interior walls are properly braced-upgrades that can reduce your costs. Newer homes built to current earthquake codes often qualify for better rates than older homes, though modern construction standards don’t eliminate the need for coverage.

Deductibles Create the Biggest Cost Variation

The deductible you choose has the most dramatic impact on your premium amount. Washington earthquake policies typically carry deductibles between 10% and 25% of your coverage limit, according to the Washington State Department of Insurance. Selecting a 20% deductible instead of a 10% deductible can cut your annual premium roughly in half, but you’ll absorb more of the loss when a quake strikes. For a $300,000 home with a 15% deductible, you’d pay $45,000 out of pocket before insurance kicks in. Your coverage limits also matter; selecting $200,000 in dwelling coverage costs less than $350,000, but you risk being underinsured if a major earthquake causes substantial damage.

Understanding these three factors positions you to make informed decisions about your coverage. The next section reveals what Washington homeowners actually pay in premiums across different counties and home types, so you can benchmark your own quote against real market rates.

What You’ll Actually Pay for Earthquake Insurance in Washington

Premium Ranges Across Washington Counties

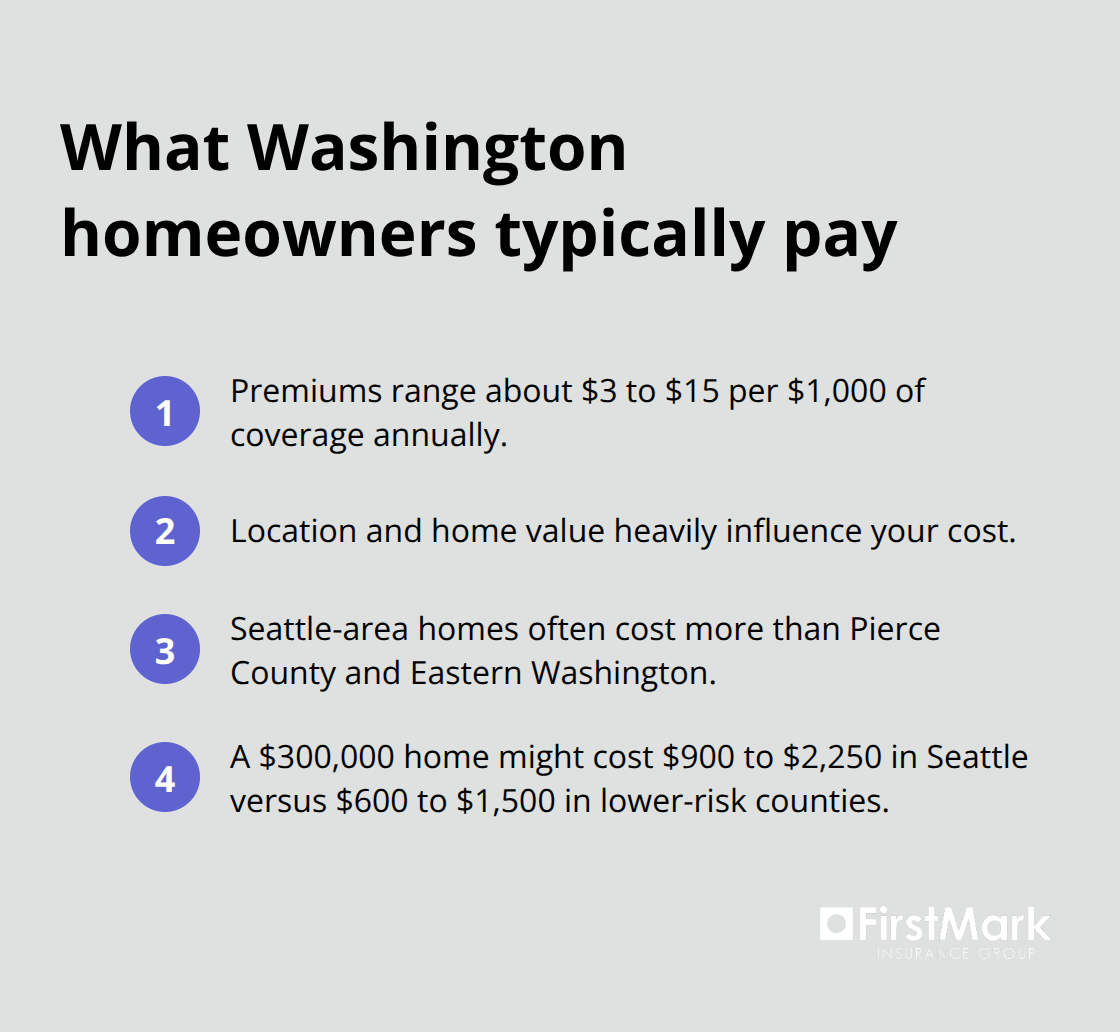

Washington homeowners face premiums ranging from about $3 to $15 per $1,000 of coverage annually, according to industry data. Your actual cost depends heavily on where in the state you live and what your home is worth. King County properties near Seattle typically cost more than Pierce County homes, which cost more than properties in Eastern Washington counties like Spokane.

A $300,000 home in Seattle might cost $900 to $2,250 annually for earthquake coverage with a $1,000 deductible, while the same home in a lower-risk county could run $600 to $1,500.

Insurers price based on fault proximity, historical seismic activity, and soil composition. The variation isn’t random-each factor directly influences your premium. A home built in 2010 with modern foundation bolting and wall bracing qualifies for better rates than a 1970s home that requires retrofits, sometimes saving you 20 to 30 percent on premiums.

How Your Deductible Shapes Your Final Cost

Your deductible choice creates the biggest price swing in earthquake insurance. Jumping from a 10 percent deductible to a 20 percent deductible can cut your premium roughly in half, though you absorb substantially more risk upfront. This trade-off forces you to weigh immediate savings against potential out-of-pocket expenses when an earthquake strikes.

Washington’s Underpenetrated Insurance Market

Washington’s earthquake insurance market remains underpenetrated despite the state’s seismic risk. According to FEMA data, only 11.3 percent of Washington residents carried earthquake coverage as of 2017, making Washington second only to California in total earthquake insurance policies but still vastly underinsured relative to risk. This contrasts sharply with states like Missouri, which saw coverage drop from 60 percent in 2000 to 11.4 percent by 2021 as premiums rose and insurers tightened availability.

How Washington Rates Compare Nationally

Washington homeowners pay more than residents in low-risk states like Texas or Florida, where earthquake insurance costs $1 to $3 per $1,000 of coverage if available at all. The Pacific Northwest’s active seismic zones justify the higher costs, yet many Washington homeowners skip coverage entirely, betting against a major quake. That gamble carries real financial consequences; the 2001 Nisqually earthquake near Seattle caused damage estimated between $500 million and $4 billion, demonstrating what happens when thousands of uninsured homes sustain simultaneous damage.

Getting Multiple Quotes Reveals Significant Price Differences

Comparing quotes across multiple insurers reveals significant price differences for identical properties and coverage. You should obtain three to five quotes before deciding rather than accepting the first quote offered. This approach takes time but often uncovers savings that justify the effort. The next section shows you concrete strategies to reduce your premiums without sacrificing the protection your home needs.

How to Reduce Your Earthquake Insurance Premium

Reducing your earthquake insurance cost starts with understanding which levers you actually control. The deductible you select creates the most immediate savings opportunity, but retrofitting your home and bundling policies offer longer-term cost advantages that compound over time. Evaluating all three strategies together rather than in isolation often yields better results than any single approach.

The Deductible Trade-Off

Raising your deductible from 10 percent to 20 percent typically cuts your annual premium roughly in half, according to industry pricing data. For a $300,000 home, this shift might save you $400 to $600 yearly. The catch is straightforward: you’ll absorb more of the earthquake damage upfront before insurance coverage begins. A 20 percent deductible on a $300,000 home means you pay $60,000 out of pocket before the insurer contributes anything.

This strategy works well if you have substantial savings set aside for emergencies and can genuinely afford that deductible without financial strain. If a major earthquake strikes tomorrow and you lack $60,000 in liquid savings, a high deductible becomes a liability rather than a savings tool. Start with an honest assessment of your emergency fund, then select a deductible that balances premium savings with financial reality.

Seismic Retrofits Deliver Measurable Premium Reductions

Foundation bolting, interior wall bracing, and water heater strapping reduce your earthquake risk enough that insurers lower premiums, according to the Washington State Department of Insurance. The upfront retrofit cost typically ranges from $3,000 to $7,000 depending on your home’s age and construction type. A 1960s home requires more extensive work than a 2005 home built to modern codes.

Calculate whether the premium savings over five to seven years justify the retrofit investment. If your insurer requires a property inspection before issuing a quote, they’re already flagging which retrofits matter most for your specific home. Prioritize those upgrades first. Some retrofits also improve home safety during earthquakes beyond just lowering insurance costs, which adds value beyond the premium reduction alone.

Bundling Coverage Creates Overlooked Savings

Combining your earthquake insurance with homeowners, umbrella, or other policies through a single insurer frequently unlocks multi-policy discounts ranging from 10 to 20 percent. Many Washington homeowners overlook this option because they’ve held their homeowners policy with one company for years and assume switching would be complicated. Requesting a bundled quote takes minutes and often reveals substantial savings you weren’t receiving.

The bundled approach also simplifies your coverage management since one insurer handles multiple policies and one renewal date consolidates your administrative burden. When you contact insurers for earthquake insurance quotes, specifically ask about bundling discounts on your entire policy portfolio rather than just the earthquake component.

Final Thoughts

Washington’s earthquake risk demands that homeowners take action rather than hope for the best. The earthquake insurance cost in Washington reflects genuine seismic danger, and only 11.3 percent of residents carried coverage as of 2017, leaving most homes vulnerable to catastrophic losses. The 2001 Nisqually earthquake caused damage estimated between $500 million and $4 billion, proving that uninsured damage can devastate your finances and your home.

You control three levers that directly reduce what you pay for coverage. Raising your deductible from 10 percent to 20 percent cuts your premium roughly in half, while retrofitting your foundation and bracing interior walls saves you 20 to 30 percent over time. Bundling earthquake insurance with your homeowners policy unlocks multi-policy discounts ranging from 10 to 20 percent, and comparing three to five quotes from different insurers reveals significant savings opportunities that accepting a single offer would hide.

We at FirstMark Insurance Group work with top insurance providers to present you with choices that fit your requirements at the best available pricing. Contact us to explore your earthquake insurance options and find coverage that protects your home without straining your budget.