General liability insurance isn’t optional for Washington contractors-it’s a business requirement that protects you, your team, and your clients from the financial fallout of accidents and injuries on the job site.

At FirstMark Insurance Group, we’ve worked with builders across Washington who discovered that the right WA contractor general liability coverage makes the difference between a manageable claim and a business-threatening loss. This guide walks you through what coverage actually protects you, why it matters for your licensing and client relationships, and how to select a policy that fits your operation.

What General Liability Actually Protects

Three Core Areas of Coverage

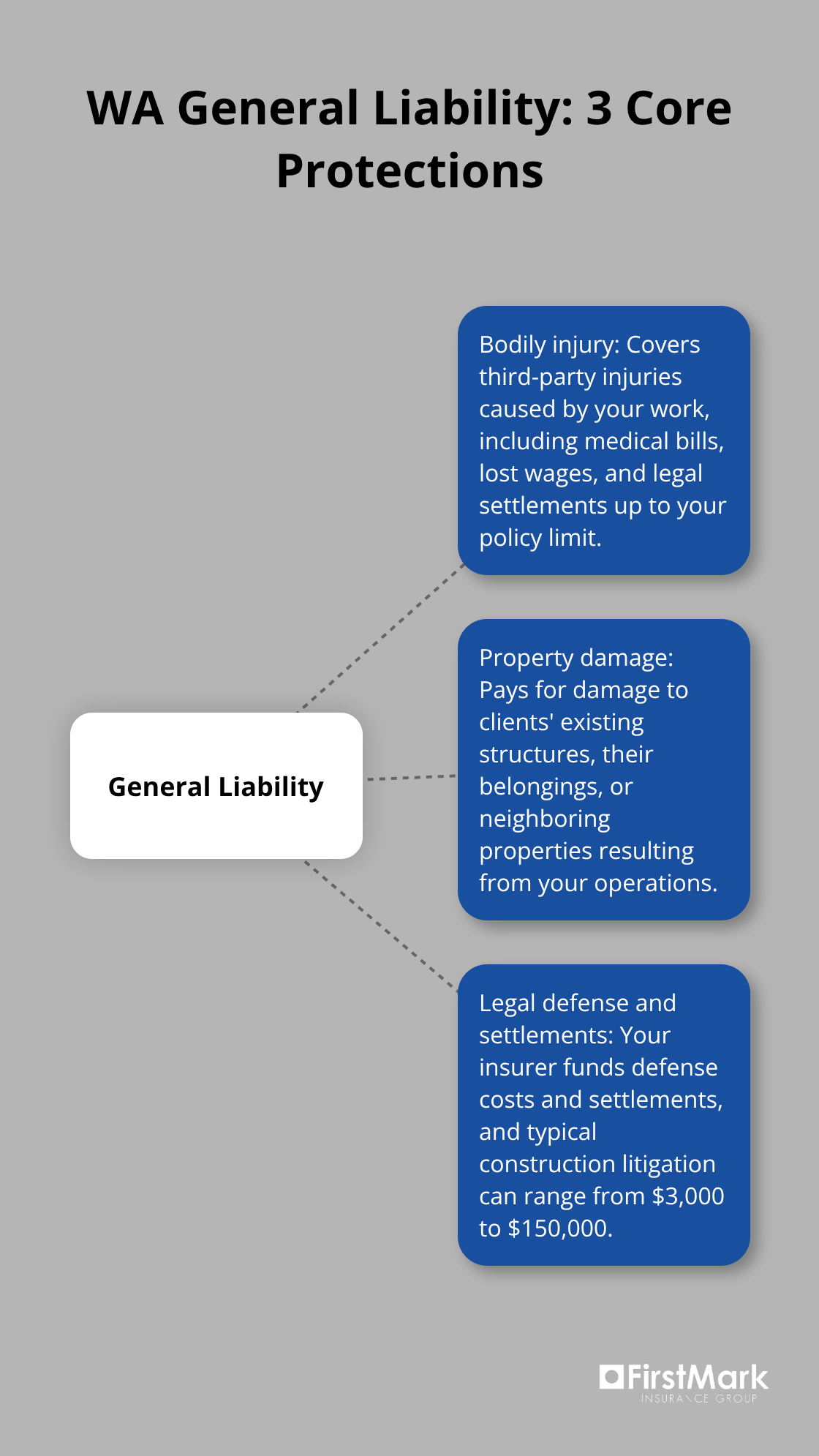

General liability insurance covers three distinct areas of financial exposure that appear regularly on Washington job sites. First, it protects you when a third party-a homeowner, a passerby, a vendor-suffers bodily injury because of your work. If a crew member’s ladder damages a neighbor’s fence or a falling tool strikes someone on an adjacent property, your GL policy covers medical expenses, lost wages, and legal settlements up to your policy limit. Washington’s state minimum is $250,000 per occurrence, according to the Department of Labor & Industries, though most established contractors carry $1 million or higher because client contracts frequently demand it.

Second, GL covers property damage caused by your operations. A concrete saw that cuts through an underground electrical line, a dropped roofing nail that punctures a skylight, or water damage from temporary work-these all fall under property damage coverage. Your policy protects you against claims for damage to the client’s existing structures, their belongings, or neighboring properties.

Legal Defense and Settlement Protection

Third, your insurer pays legal defense costs and settlements directly, protecting your business assets when claims arise. This matters because litigation for contract disputes in construction ranges from $3,000 to $150,000, according to industry data, and your GL policy absorbs those costs before they touch your operating account.

Critical Coverage Gaps

What GL does not cover is equally important. Standard policies exclude damage to work you’ve already completed, which is why completed operations coverage exists as a separate add-on. They also exclude professional services or design work-if you provide project management or architectural advice, you need professional liability coverage on top of GL.

Pollution and environmental liability gaps are common too; renovations involving lead paint, asbestos, or contaminated soil require a separate Contractor’s Pollution Liability endorsement.

Many Washington contractors overlook these gaps until a claim arrives, then discover their coverage stops short. The safest approach is to review your specific trade’s exposures with your agent and confirm that endorsements like installation floaters, products-completed operations coverage, and pollution liability are in place before you bid the next job. Once you understand what your GL policy actually covers and where the gaps live, you can move forward with confidence-and that confidence matters when your clients ask about your coverage limits and your ability to protect their property.

Why GL Insurance Isn’t Optional in Washington

Registration and Legal Requirements

Washington’s Department of Labor & Industries requires all contractors to register before performing any work, and that registration hinges on two things: a surety bond and $250,000 general liability insurance with a minimum of $250,000 per occurrence. This requirement exists because L&I’s verification tool lets homeowners confirm your registration status, bond standing, and active coverage in seconds. Clients increasingly use it before hiring. If your coverage lapses, your registration becomes invalid immediately, and you cannot legally perform work until coverage is restored. Operating without it exposes you to civil penalties up to $5,000 per violation according to L&I, plus unlimited personal liability for any claims that occur.

Client and Vendor Expectations

Beyond the legal mandate, your clients and vendors expect proof of coverage. General contractors typically face contracts demanding $1 million to $2 million in coverage, especially on residential projects over $1,000 or commercial work between $1,000 and $60,000. Clients ask for certificates of insurance before work begins, and many require your company to be named as additional insured on your policy. If you cannot produce current coverage, you lose the bid. Vendors and subcontractors also protect themselves by verifying your insurance status before they show up on your job site, so gaps in coverage damage your reputation with the supply chain you depend on.

The Financial Reality of Claims

A single serious injury on a job site can exceed your annual revenue. Litigation for construction disputes ranges from $3,000 to $150,000, and that’s before medical bills, lost wages, or property damage claims stack up. A homeowner who suffers a permanent injury from your work can pursue claims that dwarf the project value. Without GL coverage, those costs come directly from your bank account and personal assets. With coverage, your insurer handles defense costs, settlements, and judgments up to your policy limit, keeping your business intact and operational.

Cost Versus Risk

The cost of GL insurance for small Washington contractors typically runs $3,000 to $8,000 annually for a basic package-a fraction of what a single claim can cost. That investment protects not just your current jobs but your ability to bid future work, since clients and insurers alike view uninsured contractors as high-risk partners. Understanding these requirements and their financial implications sets the stage for selecting the right policy limits and endorsements that match your specific operation.

How to Choose the Right GL Policy for Your Business

Map Your Actual Exposure

Start by mapping your actual exposure rather than accepting a generic quote. A specialty contractor doing interior finish work faces different risks than a general contractor managing multiple trades on a residential renovation, and your policy should reflect that difference. Review your past three years of projects and note which ones involved high-value materials, work near occupied spaces, or extended timelines.

If you regularly install finished goods like cabinets or flooring, you need installation floaters that cover the value of materials while they’re being fitted. If you do renovations in homes built before 1978, lead-based paint liability should be on your radar. If your work touches soil or involves demolition, pollution coverage becomes essential.

Understand What Competitors and Clients Expect

The Department of Labor & Industries verification tool shows what competitors carry, and while you shouldn’t match coverage blindly, seeing that established contractors in your area carry $1 million limits tells you what clients expect. Start with Washington’s $250,000 state minimum only if you handle very small projects under $10,000; most residential work over $1,000 and commercial projects between $1,000 and $60,000 encounter client contracts demanding $1 million.

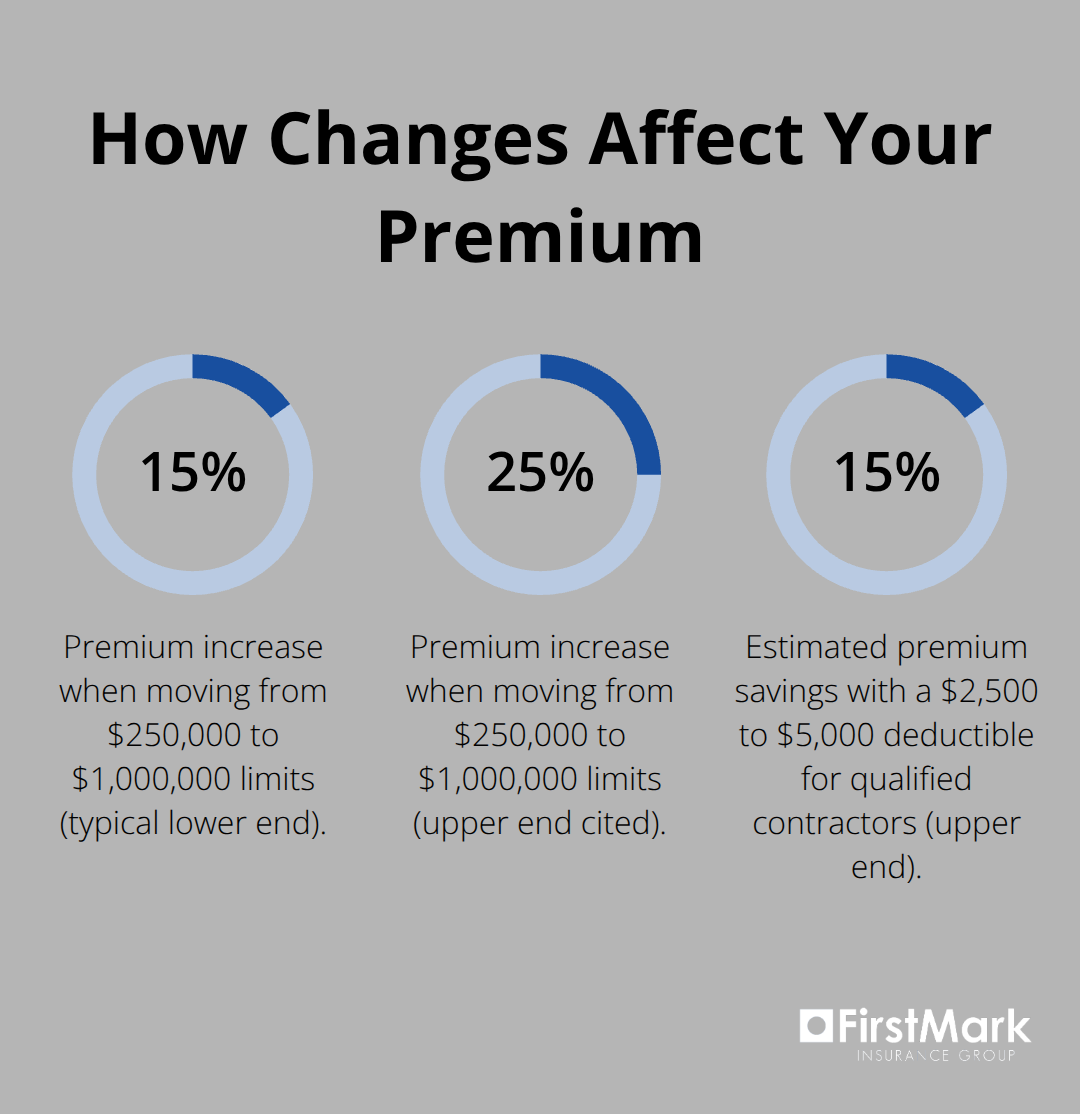

Request quotes at multiple limits-$250,000, $500,000, and $1 million-from at least three carriers to see how premium increases. Many contractors find the jump from $250,000 to $1 million costs only 15 to 25 percent more annually, making the higher limit worth the investment.

When comparing quotes, verify that carriers are licensed in Washington and that they clearly itemize what endorsements are included. A $3,000 quote that excludes completed operations coverage is more expensive than a $4,200 quote that includes it, because you’ll add that endorsement anyway once a client requests it.

Choose Deductibles That Match Your Cash Flow

Deductibles directly affect your out-of-pocket exposure during claims, so choose them strategically rather than defaulting to whatever the quote shows. A $1,000 deductible is standard and appropriate for most contractors because it keeps premiums reasonable while protecting you from minor incidents.

Moving to a $2,500 or $5,000 deductible saves 10 to 15 percent on premiums, but only if your cash flow can absorb that cost when a claim lands. Contractors with thin margins or inconsistent revenue should stick with $1,000 rather than gamble on savings. Conversely, if you have strong reserves and handle larger projects regularly, a $2,500 deductible makes financial sense. Verify that your chosen limit applies per occurrence, not in aggregate, because aggregate limits can exhaust quickly if you face multiple claims in one year.

Select Carriers and Endorsements With Care

Once you’ve narrowed carriers to two or three based on limit options and deductible structures, ask each agent directly: What endorsements does my trade typically need that aren’t in the base policy? A contractor specialist who understands your specific work-whether you’re a roofer, HVAC installer, or general contractor-will identify gaps faster than a generalist.

Request that your policy language include an additional insured endorsement covering your clients, because most contracts require it and adding it upfront costs nothing compared to amending it later. Confirm that the carrier will notify you before canceling or non-renewing so you have time to secure replacement coverage before L&I registration lapses. That single notification requirement has prevented countless contractors from losing their license.

Final Thoughts

Your WA contractor general liability coverage requires attention beyond the initial purchase. As your business grows and your project types shift, your policy must adapt to match your current operation, not last year’s work. Schedule a coverage review with an agent who understands contractor requirements specific to your trade, bring your past three years of project summaries and any client contracts that specify insurance demands, and confirm that your endorsements, deductible, and carrier notifications align with your actual exposure.

Treat your GL policy as a living document that you update when you add new services, hire subcontractors, or bid projects with unusual exposures like lead paint or contaminated soil. Contact your agent immediately when circumstances change rather than waiting for renewal, verify that subcontractors name you as additional insured before they arrive on site, and ask whether your current endorsements cover new work or whether you need temporary riders. These actions separate contractors who operate with confidence from those who discover gaps during claims.

We at FirstMark Insurance Group work with Washington contractors to align your coverage with your actual business needs and keep your protection current throughout the year. Reach out to discuss how your WA contractor general liability policy can support your growth and protect what you’ve built.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation