Running a contracting business in Seattle means navigating strict regulatory requirements that go beyond just having a license. Missing even one compliance obligation can expose your business to significant financial and legal risk.

At FirstMark Insurance Group, we work with contractors daily who face confusion about what coverage they actually need and which requirements apply to their specific operation. This guide breaks down the essential Seattle contractor insurance requirements and licensing rules so you can protect your business properly.

Washington State Contractor License Requirements

Understanding Your Contractor Classification

Washington’s Department of Labor & Industries classifies contractors into two categories, and this distinction determines your licensing path, bonding requirements, and what work you can legally perform. General contractors hire subcontractors across multiple trades, while specialty contractors restrict their work to their registered specialty and cannot hire subcontractors. L&I regulates 63 contractor specialties, ranging from roofing and painting to HVAC and tree removal. Your first step involves determining which classification matches your operation, because misclassifying yourself creates immediate compliance problems.

The Registration Process and Timeline

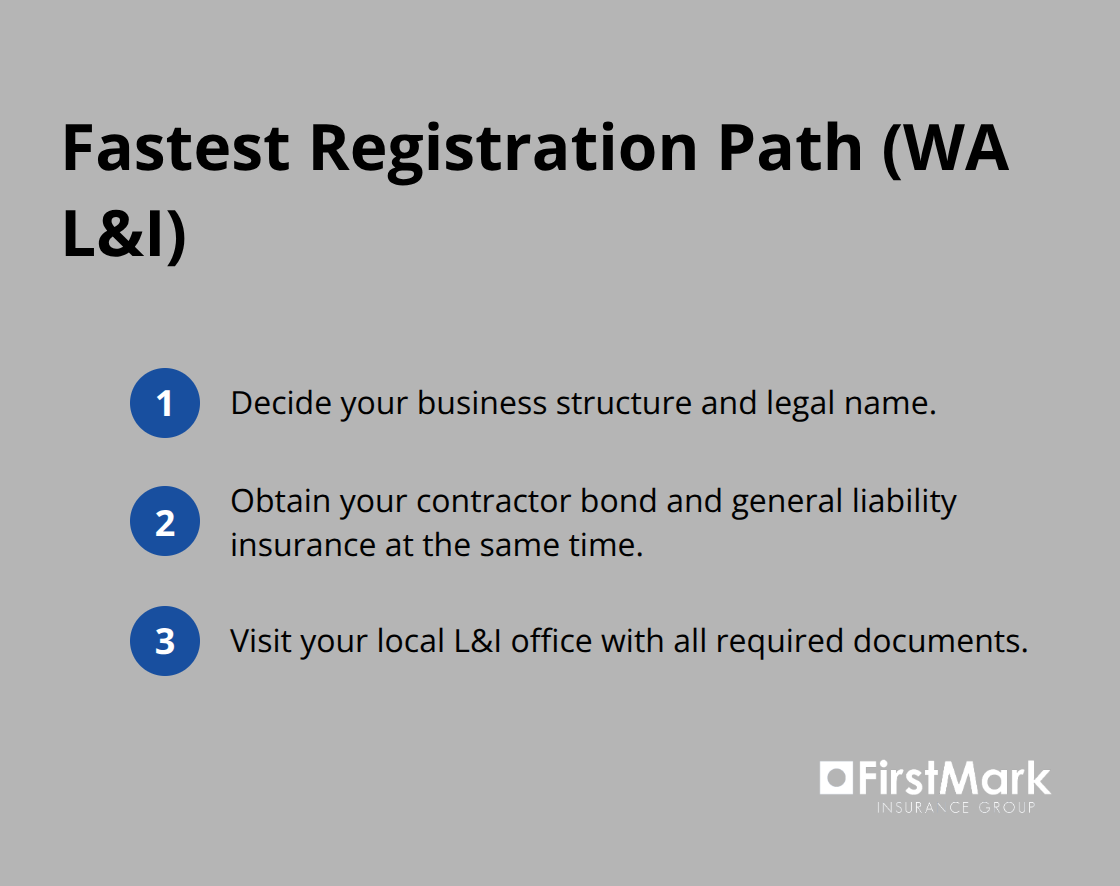

To register, you must file a Department of Revenue business registration, obtain a contractor bond, carry general liability insurance, complete the Application for Contractor Registration (Form F625-001-000), and pay a $141.10 fee. The bond amount differs by classification: general contractors need a $30,000 continuous bond, while specialty contractors need $15,000. General liability insurance must cover $200,000 in public liability and $50,000 in property damage, or a combined single limit of $250,000. Both the bond and insurance must list L&I as the certificate holder and use your exact registered business name.

Many contractors waste time on the registration process because they apply before securing their bond and insurance. The fastest path follows three steps: decide your business structure and name, obtain your bond and insurance simultaneously, then visit your local L&I office with all documents. Mailed applications typically take three to four weeks to process, but you’ll receive your registration card in about two weeks.

Bond and Insurance Documentation Requirements

Your bond and insurance must arrive before the filing date on the bond itself, and the original bond must bear the bonding company’s seal. For insurance certificates, submit them via US mail, a designated insurer portal, or in person-email and fax are not accepted. After registration, display your contractor registration number on all business communications and advertising so customers can verify your status using L&I’s Verify a Contractor tool.

Renewal, Suspension, and Reinstatement

Renewal requires the same $141.10 fee, and you must renew before your current registration expires. If your bond or insurance cancels or lapses, L&I may suspend your registration and send certified notice within two days. Reinstatement requires proof of correction and a $66.60 reinstatement fee, which you can submit online or in person. An Assignment of Account serves as an alternative to a bond if you fund it with cash, a certificate of deposit, time deposit, or money market account at a Washington state bank.

Additional Licensing and Subcontractor Responsibilities

Some activities demand additional licensing beyond L&I registration-lead-based paint work requires compliance with the Washington Department of Commerce Lead Paint Program, and pesticide application requires a Washington Department of Agriculture license. The Model Disclosure Statement Notice to Customer applies to residential jobs of $1,000 or more and commercial projects between $1,000 and $60,000. Contractors bear responsibility for safety obligations of both employees and subcontractors on job sites, and this responsibility extends to verifying that your subcontractors carry adequate workers’ compensation coverage and maintain current registration status. Understanding these subcontractor obligations sets the foundation for the insurance coverage you must carry to protect your business.

Insurance Coverage Seattle Contractors Must Carry

General Liability: Your Foundation Against Claims

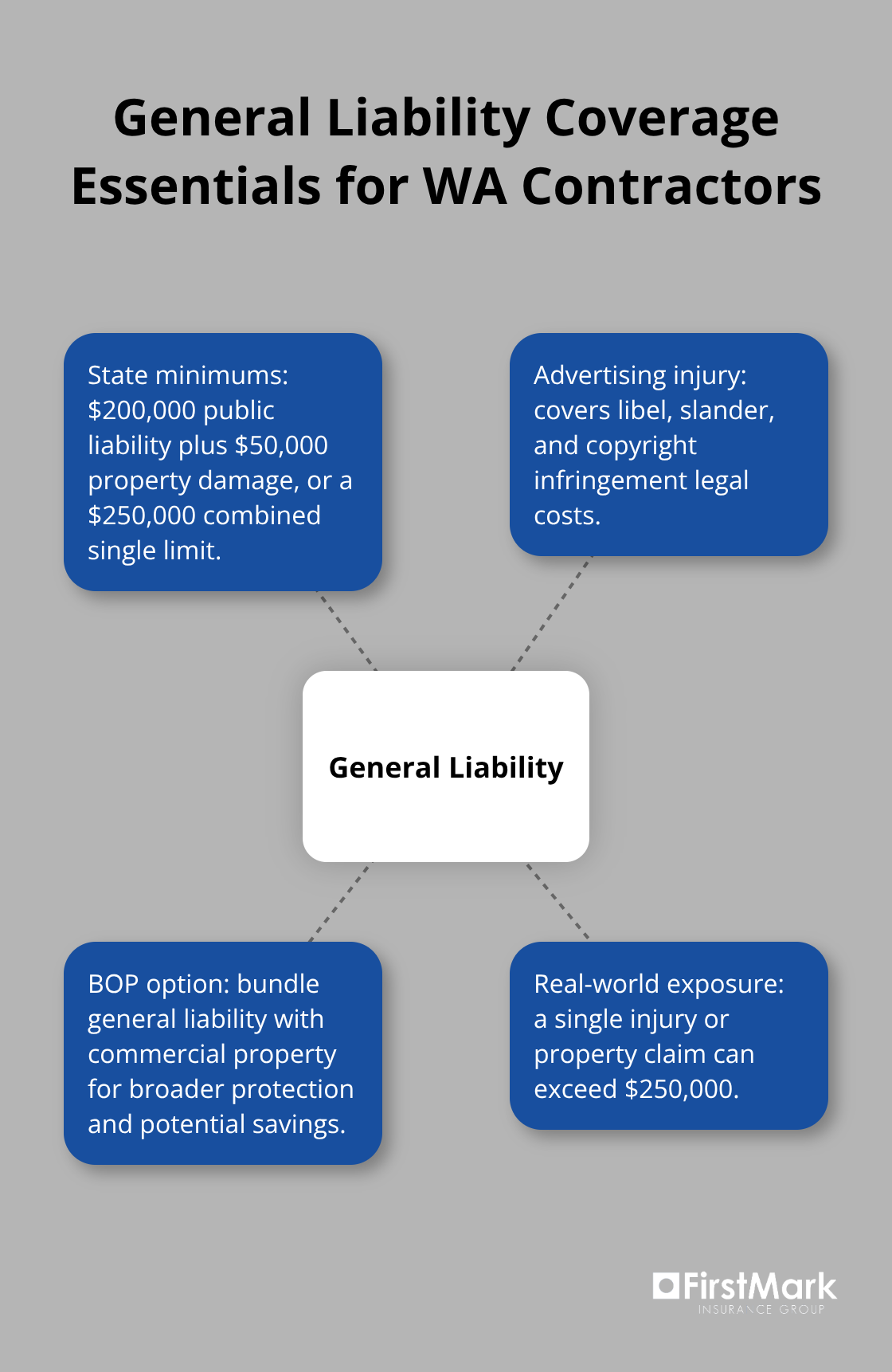

General liability insurance forms the foundation of contractor protection in Washington, and the state mandates specific minimums that apply whether you’re a general or specialty contractor. You need either $200,000 in public liability coverage paired with $50,000 in property damage, or a combined single limit of $250,000-this isn’t negotiable if you want to stay registered with L&I. The practical reality is that these minimums often fall short of actual exposure. A single injury claim or property damage incident on a residential project can easily exceed $250,000, leaving your personal assets vulnerable.

Contractors who carry exactly the state minimum frequently face significant out-of-pocket costs when claims arise. General liability policies covering advertising injuries protect you against legal costs from libel, slander, or copyright infringement claims-exposures many contractors overlook until they face a lawsuit. Many contractors bundle general liability with commercial property coverage through a Business Owner’s Policy, which typically costs less than purchasing policies separately while providing broader protection for your office, equipment, and inventory.

Workers’ Compensation: Understanding Your Obligations

Workers’ compensation insurance in Washington operates differently than most states because the system uses a monopolistic state fund rather than private insurers, meaning you cannot shop rates between carriers. If you have employees, you must carry coverage through the Washington state fund-there’s no alternative option. You become liable for unpaid workers’ compensation premiums if you fail to report workers who should be covered, and penalties plus interest compound quickly.

The Personal Labor Test helps determine if someone qualifies for an exemption: if a worker brings their own employees or equipment and you don’t control them, they may not require coverage. However, if the worker fails this test, you must apply a six-part test (seven parts for construction work), and all parts must be true for exemption to apply. For construction specifically, the worker must be properly registered as a contractor or hold a valid electrical contractor license.

Commercial Auto and Equipment Protection

Commercial auto insurance minimums in Washington require $25,000 for injuries to one person, $50,000 for injuries to multiple people, and $10,000 for property damage. If your company owns vehicles, this coverage is mandatory; if you lease or use non-owned vehicles, a hired and non-owned auto policy fills critical gaps that standard commercial auto policies exclude. Tools and equipment insurance protects your investment in equipment valued under roughly $10,000 and under five years old, covering replacement or repair costs from fire, vandalism, and theft-essential coverage for contractors who depend on specific tools to complete jobs.

Professional Liability for Design-Build Work

Professional liability insurance, often called errors and omissions coverage, protects your business if you’re sued for design mistakes or workmanship defects. This coverage becomes increasingly important if you perform design-build work where professional services overlap with construction activities. Many contractors underestimate this exposure until a client alleges that your design recommendations or plan modifications caused financial loss. The gap between contractors who need this coverage and those who actually purchase it remains significant, leaving many businesses exposed to claims that general liability policies explicitly exclude.

Understanding these insurance requirements sets the stage for recognizing which compliance mistakes contractors make most often-and how those mistakes create unnecessary risk for your operation.

Common Compliance Mistakes Contractors Make

Underestimating Your Coverage Needs

Most contractors carry the state minimum coverage limits and assume that satisfies their compliance obligations. This approach creates dangerous exposure because Washington’s minimum requirements of $200,000 for public liability and $50,000 for property damage rarely cover the actual cost of a serious injury or property damage claim on a construction site. A single incident involving multiple workers or significant property damage exhausts these minimums within days of a claim filing, leaving your business responsible for costs beyond the policy limit.

Contractors operating in Seattle’s competitive market often compete on price, which means cutting corners on coverage limits to reduce premium costs. This false economy backfires when a claim arrives and you discover that your insurance covers only a fraction of the damages. The gap between what your policy pays and what you owe becomes your personal liability. Try carrying at least $500,000 to $1,000,000 in combined coverage for projects involving multiple workers or high-value properties, particularly in residential work where jury awards tend to be substantial.

Adding a commercial umbrella policy extends protection beyond your base policy limits at a reasonable cost and provides the security that your business won’t be decimated by a single claim. This additional layer of protection addresses the reality that construction claims frequently exceed state minimums.

Failing to Update Policies as Your Business Evolves

A critical mistake occurs when contractors fail to update their policies as their business changes. You add employees, hire subcontractors, expand into design-build work, or start using specialized equipment, but your insurance remains unchanged from when you first registered. Workers’ compensation coverage fails to capture all reportable workers, leaving you liable for unpaid premiums plus penalties and interest that compound monthly.

Professional liability coverage gaps emerge when you perform design work without realizing that your general liability policy excludes professional services. Equipment coverage doesn’t reflect your current tool inventory, creating uninsured losses when theft or damage occurs. These gaps accumulate silently until a claim arrives and exposes what your policy actually covers versus what you assumed it covered.

Neglecting Subcontractor Verification

Many contractors neglect to verify that subcontractors maintain current workers’ compensation coverage and valid L&I registration before they begin work on your projects. Washington law makes you responsible for your subcontractor’s safety obligations and unpaid workers’ compensation premiums, meaning you face liability even when the subcontractor fails to maintain required coverage.

This responsibility extends beyond a simple phone call. You need documented proof that each subcontractor carries active coverage and holds current registration status. Failing to collect this documentation before mobilization creates exposure that your own insurance may not cover, since you knowingly allowed an uninsured or unregistered contractor to work on your project.

Building a Compliance Review Process

An annual insurance review prevents the costly surprises that emerge when claims arrive and you discover coverage gaps. Examine your current operations, confirm that all workers are properly reported, verify subcontractor compliance documentation before they mobilize to a job site, and adjust coverage limits and policy types to match your actual business activities. This discipline addresses the reality that construction businesses change constantly, and your insurance must evolve with those changes.

The review process should include a conversation with your insurance agent about any new services you offer, equipment you’ve acquired, or changes in your workforce composition. These conversations identify coverage gaps before they become expensive problems and ensure that your policies reflect your actual operation rather than your operation from two or three years ago.

Final Thoughts

Staying compliant with Seattle contractor insurance requirements means understanding that licensing, bonding, and coverage work together to protect your business and your clients. You need current L&I registration with proper bonding, general liability insurance meeting state minimums, workers’ compensation coverage for your employees, and verification that your subcontractors maintain their own compliance. Beyond these baseline requirements, your business likely needs additional protection through commercial auto insurance, tools and equipment coverage, and professional liability insurance if you perform design work.

The contractors who avoid costly surprises are those who review their coverage annually, update policies when their business changes, and document subcontractor compliance before work begins. This discipline addresses the reality that construction businesses change constantly, and your insurance must evolve with those changes to match your actual operations. An annual review with your insurance agent identifies coverage gaps before they become expensive problems and confirms that your policies reflect your current work rather than your operation from years past.

Your next step is straightforward: schedule a conversation with our team at FirstMark Insurance Group to review your current coverage against your actual operations. We’ll identify gaps, confirm that your limits match your exposure, and help you understand how your policies protect your business when claims arrive. Visit FirstMark Insurance Group to connect with an agent who can guide you through the specific coverage your contracting business needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation