A general liability policy in Seattle isn’t optional-it’s the foundation of responsible business ownership. Whether you operate a small service company or manage a larger enterprise, this coverage protects you from the financial devastation that comes with bodily injury claims, property damage lawsuits, and legal defense costs.

At FirstMark Insurance Group, we’ve helped countless Seattle business owners understand exactly what their general liability coverage does and doesn’t protect. The right policy can mean the difference between weathering a claim and facing business-threatening expenses.

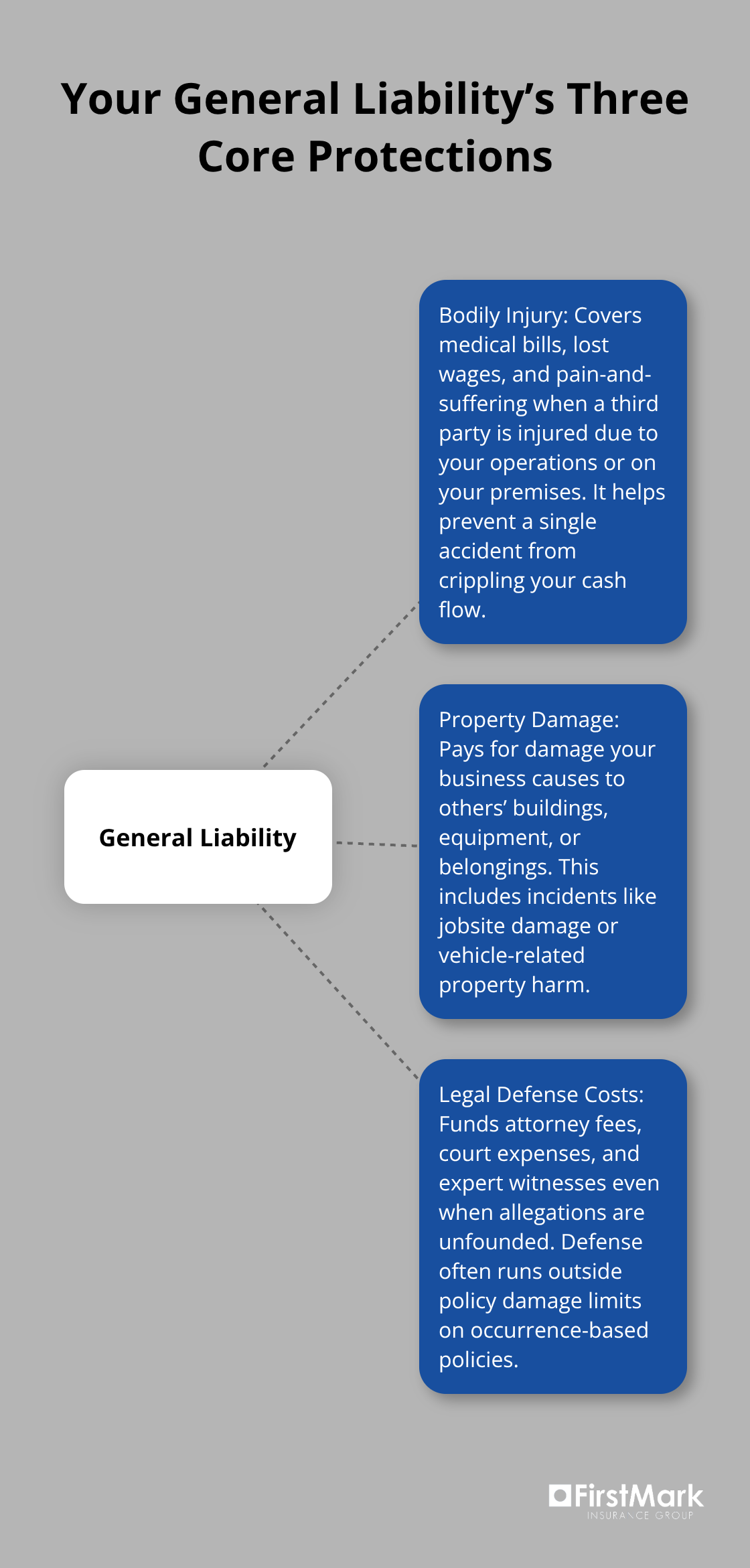

What Your General Liability Coverage Actually Covers

Three Core Protections Your Policy Provides

A general liability policy protects you from three critical financial exposures that can devastate a Seattle business. First, bodily injury claims cover medical expenses, lost wages, and pain-and-suffering damages when someone is injured on your property or due to your business operations.

Second, property damage liability pays for harm your business causes to someone else’s building, equipment, or belongings-a contractor accidentally damages a client’s roof or a delivery service hits a parked car. Third, your policy covers legal defense costs, including attorney fees, court expenses, and expert witness fees, which typically range between $162 and $392 per hour and often run separately from your damage limits on occurrence-based policies. These three pillars form your primary shield against lawsuits that could otherwise drain your business cash flow immediately.

The Real Cost of Claims in Today’s Market

The National Small Business Risk Index reports that the average business liability claim now costs $97,200, up 18 percent since 2022. This dramatic increase reflects rising medical expenses, higher legal defense fees, and larger court awards for bodily injury damages. A slip-and-fall in a Seattle retail space that might have cost $30,000 five years ago can now approach $100,000 when emergency care, imaging, surgery, and ongoing treatment are factored in. If your general liability limit sits at $1 million per occurrence-the standard for many small Seattle businesses-a single claim consuming $97,200 leaves you $902,800 in remaining protection. However, if you face two moderate claims or one severe claim approaching your limit, your coverage erodes quickly. This reality means your policy limits must reflect current claim costs, not outdated assumptions about what injuries cost.

Third-Party Requirements Shape Your Coverage Decisions

Seattle contractors, vendors, and service providers regularly encounter client requests for certificates of insurance listing the client as an additional insured on your general liability policy. This isn’t bureaucratic friction-it’s a contractual protection mechanism. King County procurement requirements mandate $1 million per occurrence and $2 million aggregate limits with the county named as additional insured. Cannabis businesses in Washington must carry $1 million minimum coverage with the state named as additional insured. When a client or vendor requires additional insured status, your policy must explicitly grant it through an endorsement; a standard policy without this addition won’t satisfy their risk management requirements, and you’ll lose the contract. During policy reviews, we frequently identify businesses that carry adequate limits but lack the endorsements their contracts actually require-a gap that can cost you opportunities before a claim ever occurs.

Why General Liability Insurance Matters in Seattle

Washington State Requirements Protect Your License and Operations

Washington State imposes specific liability insurance requirements depending on your industry, and ignoring these regulations creates serious consequences. The Washington Department of Labor & Industries requires contractors to maintain at least $200,000 in public liability and $50,000 in property damage coverage, or $250,000 combined single limit-minimums that reflect the state’s assessment of construction-related exposure. Cannabis businesses operating in Washington face even stricter requirements: $1,000,000 minimum coverage with the state named as additional insured. If you operate in a regulated industry and lack mandated coverage, you face license suspension, contract termination, and personal liability for injuries or damage your business causes. These aren’t theoretical penalties-they’re enforcement actions that shut down operations immediately.

Rising Claim Costs Demand Adequate Coverage Limits

Your actual risk exposure almost certainly exceeds what the state requires. The average business liability claim now costs $97,200 according to the National Small Business Risk Index, representing an 18 percent jump since 2022. That single claim could consume 20 percent of a $500,000 policy limit or wipe out most of a $250,000 combined single limit. Medical costs drive this increase relentlessly: emergency care, diagnostic imaging, surgical intervention, and ongoing physical therapy for a slip-and-fall injury in a Seattle retail or restaurant environment routinely exceed $50,000 before any pain-and-suffering component enters the settlement. Your general liability policy shields you from these escalating costs by transferring the financial burden to your insurer rather than forcing you to liquidate business assets or personal savings.

Client Contracts Require Specific Endorsements and Limits

Client contracts and vendor relationships now demand proof of insurance as a condition of doing business. King County procurement requirements mandate $1,000,000 per occurrence and $2,000,000 aggregate limits-standards that exceed many small business policies. When a property manager, general contractor, or corporate client requires your business to carry additional insured endorsements naming them on your policy, that requirement is non-negotiable. Without the endorsement, your policy provides no coverage for claims the client initiates against you, and the client won’t sign the contract.

Seattle businesses often carry adequate limits but miss critical endorsements like liquor liability for hospitality venues, products-completed operations for retailers, or additional insured provisions for contractors. These gaps emerge during contract negotiations and cost you revenue before any claim occurs. Your policy must align with how you actually operate and who actually requires coverage. A pressure-washing operation serving commercial clients faces entirely different endorsement requirements than a software consulting firm, yet both operate in Seattle.

Alignment Between Contracts and Coverage Prevents Operational Gaps

The competitive pressure to secure contracts means you cannot afford to overlook coverage gaps after signing agreements. During annual reviews, verify that every client contract specifying insurance requirements appears in your current policy endorsements. If your contract requires $1,000,000 limits but your policy carries $500,000, you’re operating below your client’s minimum standard. If your contract names the client as additional insured but your policy lacks that endorsement, your coverage doesn’t activate when the client files a claim.

These operational realities make general liability insurance far more than regulatory compliance-it’s the practical foundation that allows your Seattle business to win contracts, retain clients, and operate without catastrophic financial exposure when injuries or damage occur. The next step involves assessing your specific industry risks and determining which coverage limits and endorsements actually protect your operations.

Choosing the Right Coverage for Your Seattle Operation

Map Your Actual Business Exposures

Start with your actual operations, not industry averages. A pressure-washing contractor, a restaurant owner, and a software consultant all operate in Seattle, yet their liability exposures differ dramatically. Your first step is identifying exactly what could go wrong in your business. Does your work involve customer foot traffic in wet conditions? Do you handle food preparation or serve alcohol? Do you operate equipment that could damage client property? Do you employ subcontractors who work on client sites? Are you required to carry specific endorsements by contract? These questions reveal your real risk profile far better than generic industry classifications. Document your answers because they directly determine which coverage limits and endorsements actually protect your operation versus which ones you’re paying for unnecessarily.

Set Your Coverage Limits Based on Three Concrete Factors

Once you understand your exposures, determine your coverage limits by examining three concrete factors: your annual revenue, your worst-case loss scenario, and your client contract requirements. The standard $1 million per occurrence limit works for many Seattle small businesses, but not all. A restaurant with 150 daily customers faces higher slip-and-fall frequency than a consulting firm with five employees. A contractor working on high-value residential projects needs higher limits than one performing minor repairs. King County procurement mandates $1 million per occurrence and $2 million aggregate, which immediately sets your minimum if you pursue government contracts. Review your three largest client contracts and note their specific coverage requirements; if two clients require $1 million limits, that becomes your practical baseline regardless of whether your industry typically carries less.

Compare Quotes and Understand What Drives Your Renewal Price

Compare quotes from at least two carriers before renewal, requesting identical coverage specifications so you can actually compare pricing. When renewal rates spike, ask your carrier specifically what changed and present any risk improvements you’ve implemented. Carriers recognize measurable safety investments: documented safety protocols, quarterly site inspections, employee training records, and corrective action documentation can yield meaningful premium reductions when properly documented. When a carrier raises your renewal price significantly, request a detailed breakdown of what triggered the increase. Present competitive quotes from other carriers to encourage price reconsideration. This approach shifts the negotiation from passive acceptance to informed discussion about your actual risk profile and the investments you’ve made to reduce exposure.

Final Thoughts

Your general liability policy Seattle businesses rely on must evolve as your operations and claim costs change. The average liability claim now costs $97,200-up 18 percent since 2022-which means your coverage limits from three years ago likely fall short of today’s reality. Review your current policy limits against your three largest client contracts and verify that your endorsements match what those contracts actually require; gaps in additional insured status or limits below contractual minimums create operational exposure before any claim ever occurs.

Schedule a policy review within the next 60 days if you haven’t examined your coverage in over a year. Gather your client contracts, note their specific insurance requirements, and confirm your current policy satisfies those terms. If your limits lag behind client demands or your endorsements don’t align with your actual business operations, contact your insurance advisor immediately to close those gaps.

We at FirstMark Insurance Group work with Seattle business owners to align their general liability coverage with how they actually operate and what their clients require. Contact us today to review your current protection and ensure your policy keeps pace with rising claim costs and evolving contract requirements.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation