Construction projects in Seattle face distinct risks that standard property insurance simply doesn’t address. Weather, theft, and liability exposures can derail timelines and drain budgets if left unprotected.

Seattle builders risk insurance is designed specifically for these challenges. We at FirstMark Insurance Group help contractors and builders understand what coverage truly matters for their projects.

Why Seattle Construction Sites Face Unique Risks

Weather Threats to Exposed Work

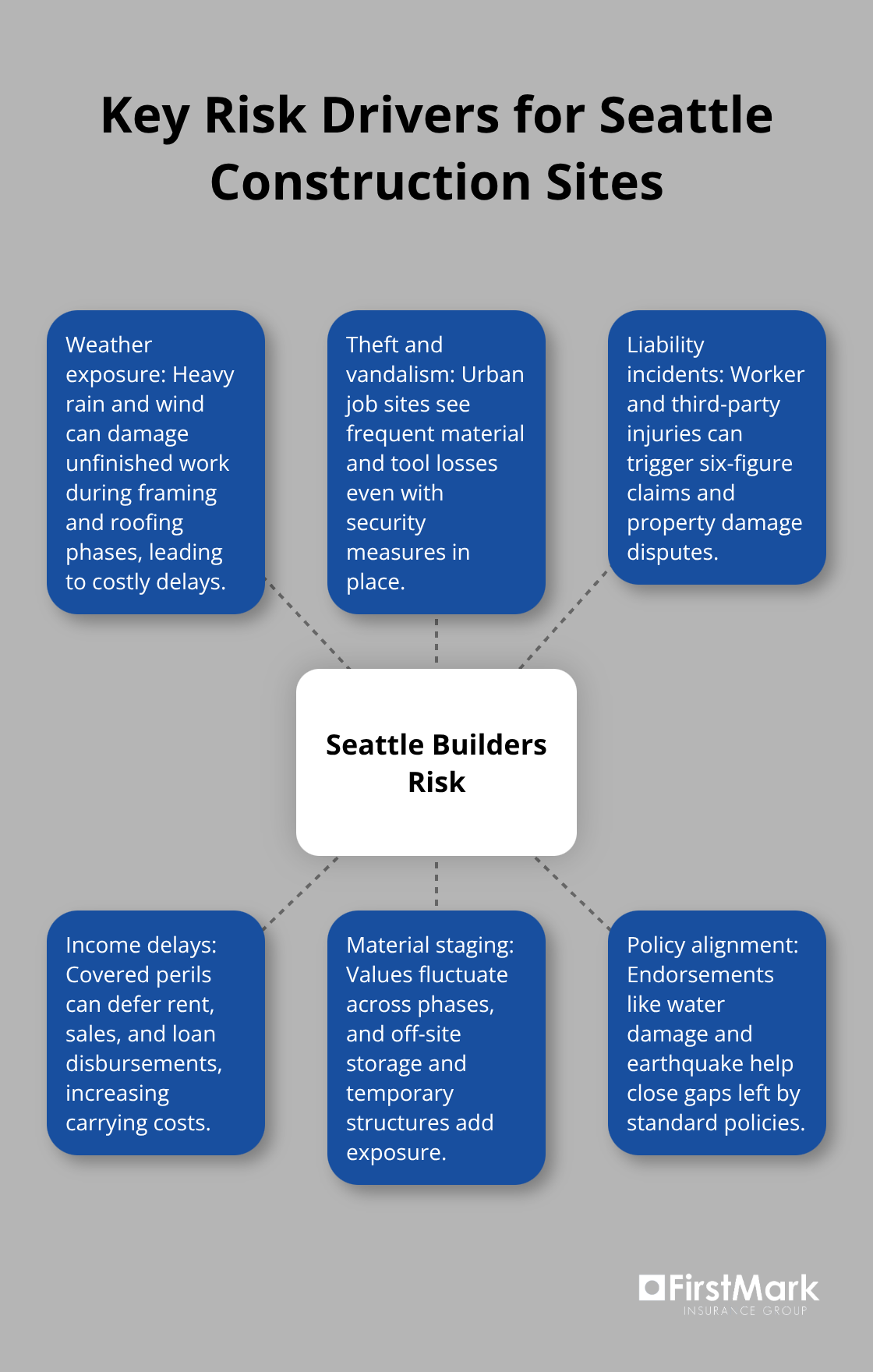

Seattle’s weather patterns create immediate threats to exposed construction work. The annual precipitation in Seattle is projected to increase from about 35.4″ to about 38.0″, and during roof installation or early-stage framing, water intrusion becomes a genuine concern that standard property policies won’t address. Heavy downpours damage building wrap, saturate temporary insulation, and compromise structural integrity before weather-resistant barriers are in place. Wind events compound this exposure-Seattle experiences regular windstorms that tear through partially installed materials and topple temporary structures. A single weather event during vulnerable construction phases delays projects by weeks and racks up unexpected costs for water damage remediation, material replacement, and labor extensions.

Builders risk insurance covers sudden weather damage, but gradual seepage from poor drainage or delayed roof work typically falls outside standard policies unless you add a water damage endorsement. This distinction matters enormously in Seattle’s climate.

Theft and Vandalism in Urban Job Sites

Equipment and material theft at Seattle job sites occurs frequently, particularly in dense urban neighborhoods like Capitol Hill, Ballard, and SoDo where staging space is cramped and after-hours security becomes difficult. Construction theft losses in Washington state reached significant levels in recent years, with copper wiring, power tools, and newly installed fixtures disappearing regularly from unattended sites. Vandalism adds another layer-broken windows, graffiti, and deliberate damage to newly installed systems occur frequently enough that contractors factor replacement costs into budgets.

Builders risk policies include theft and vandalism as standard coverages, protecting materials on-site and at temporary storage locations like Tukwila facilities. Proper site security reduces claims but doesn’t eliminate risk entirely, which is why coverage confirmation matters before work begins.

Liability Exposure from Worker and Third-Party Injuries

Worker injuries introduce liability exposure that extends beyond your direct payroll. If a subcontractor’s employee sustains injury on your site, or if your crew damages newly installed glazing or mechanical systems during installation, liability claims can quickly exceed $100,000. Third-party injury claims from delivery vehicles hitting pedestrians, equipment in confined spaces causing accidents, or after-hours access incidents create financial exposure that demands comprehensive liability protection alongside builders risk coverage. Understanding these overlapping risks shapes how you structure your insurance program and which endorsements you need to protect your project fully.

What Builders Risk Insurance Actually Covers

Materials and Equipment Protection

Materials on a Seattle construction site face constant exposure to weather, theft, and damage from adjacent work. Builders risk insurance protects the physical assets you’ve invested in before they become part of the finished building. This includes lumber, drywall, mechanical equipment, electrical fixtures, and materials in transit to your job site. Coverage extends to temporary structures like scaffolding and protective enclosures that shield work in progress. In Seattle’s dense urban neighborhoods, materials stored in temporary facilities outside the city boundaries also receive protection if theft or weather damage occurs.

The standard policy includes fire, lightning, theft, vandalism, collapse, and debris removal at no extra cost. Water damage coverage requires an endorsement in most cases, which you should strongly consider given Seattle’s rainfall patterns and the frequency of weather-related delays during roofing and insulation phases. Material costs drive project budgets significantly, and a single weather event that damages newly installed insulation or framing can consume 5 to 10 percent of your project timeline and budget. Confirm that your policy specifies coverage limits matching your actual material value on-site, not just the total project cost.

Liability Protection for Third-Party Claims

If a delivery vehicle damages a neighboring property or a subcontractor’s worker sustains injury on your site, liability claims can reach six figures within days. Your general liability policy may not cover all scenarios depending on how coverage is written. Builders risk policies often include provisions that address third-party injury and property damage claims that arise directly from construction activities. This protection separates from your standard liability coverage and fills gaps that emerge when accidents occur on active job sites.

Income Protection During Project Delays

Weather events, accidents, or other covered perils delay project completion and defer rental income, occupancy dates, or sales timelines. Builders risk policies often include provisions for loss of income when these delays occur. A three-week weather delay on a commercial project means lost tenant revenue, deferred loan disbursements, and extended carrying costs that quickly exceed the builders risk premium. This coverage addresses the financial reality that construction delays cost money beyond just materials and labor extensions.

Assess your income exposure honestly during the underwriting process. Projects under $5 million typically qualify for streamlined online quoting with minimal documentation, while larger projects benefit from a detailed conversation about your specific timeline and revenue dependencies. You should quantify these soft costs so your coverage reflects the actual financial impact of delays specific to your project and market conditions.

Choosing Coverage Limits That Match Your Exposure

Unlike general liability, which covers injuries or third-party claims, builders risk addresses the property itself. The distinction matters because underinsurance leaves gaps that claims won’t fill. Your policy should reflect the total value of materials, equipment, and temporary structures on-site at any given time, not a flat percentage of project cost. This approach prevents the frustration of discovering mid-project that your limits fall short of actual losses.

As your project progresses and material values fluctuate, your coverage limits should adjust accordingly. Early framing phases carry different exposure than later mechanical and finishing work. A policy that remains static throughout construction often misaligns with your actual risk profile. Discussing these phases with your insurance partner ensures that coverage evolves with your project schedule and protects your investment at every stage.

Selecting the Right Coverage for Your Seattle Project

Map Your Project Timeline Against Seattle’s Weather Exposure

Start by documenting your project timeline against Seattle’s weather patterns and your material staging plan. Projects running September through March face elevated rain and wind risk, which directly affects both your coverage needs and premium costs. Record when materials arrive on-site, when weather-vulnerable phases occur (roofing, insulation, mechanical rough-in), and when temporary structures come down. This timeline becomes your underwriting foundation.

Insurance carriers price builders risk based on project duration, construction type, and whether you’re building new or renovating a 70 to 100-year-old Seattle building that commonly uncovers rot, outdated wiring, and foundation weaknesses. A six-month project carries different exposure than an 18-month renovation, and your policy should reflect that distinction. Projects under $5 million often qualify for streamlined online quoting with minimal back-and-forth, while larger projects demand a detailed conversation about phasing, soft costs, and income protection. Underestimating your actual material value or timeline creates coverage gaps that emerge during claims.

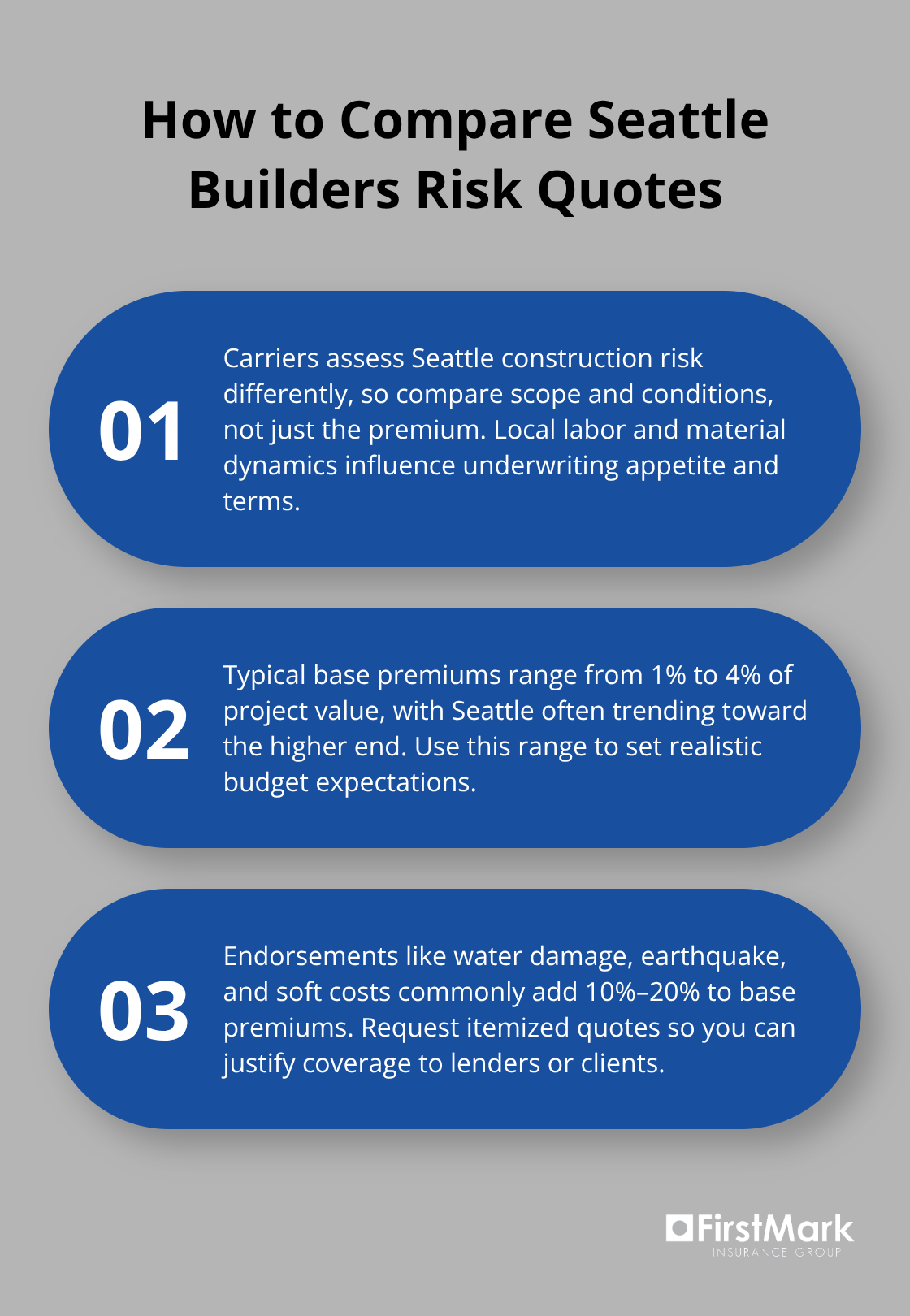

Compare Quotes Across Multiple Carriers

Comparing quotes across multiple carriers reveals how differently insurers view Seattle construction risk. Nationwide, Tokio Marine HCC, Zurich, Travelers, and Hiscox each apply different underwriting criteria and pricing formulas. Standard coverage costs typically range from 1 to 4 percent of project value, but Seattle’s labor and material costs often push premiums toward the upper end.

Water damage endorsements, earthquake coverage, and soft-cost protection add 10 to 20 percent to base premiums but address genuine Seattle exposures that standard policies exclude. Request quotes that itemize each endorsement so you understand what you’re paying for and can justify costs to your lender or client. Avoid quotes that list only a total premium without breaking down coverage components-that approach hides whether your policy actually includes water damage protection or leaves it excluded.

Verify Coverage for All Financially Impacted Parties

Your policy must name all financially impacted parties: the owner, general contractor, lender, and relevant subcontractors. A policy that covers only the GC creates disputes when material damage or theft claims arise and the owner discovers they lack direct coverage. This naming requirement protects everyone involved and prevents coverage gaps that surface after losses occur.

Review Exclusions and Optional Coverages Carefully

Review exclusions carefully, particularly around gradual water intrusion, earthquake (which requires a separate endorsement in Washington), and materials stored off-site. A policy that covers materials at your Tukwila storage facility protects your supply chain, but only if the endorsement is explicitly added. Ask your carrier whether collapse, ordinance or law, and debris removal come standard or require additional cost. These coverages matter on Seattle projects where older buildings generate hidden structural issues and cleanup costs spike after weather events or accidents.

Final Thoughts

Your Seattle builders risk insurance protects more than materials and equipment-it protects your project’s financial stability and your reputation for delivering on schedule. Start by documenting your project timeline, material staging plan, and income dependencies before requesting quotes. This foundation lets carriers understand your specific exposure and price accordingly, and when quotes arrive, compare them across multiple carriers to verify that each endorsement addresses a genuine Seattle risk.

Confirm that all financially impacted parties receive naming on the policy so coverage gaps don’t emerge after losses occur. Schedule regular policy reviews at major milestones-when material values peak, when weather-vulnerable phases begin, and when project scope changes. These conversations prevent the frustration of discovering mid-project that your limits no longer match your exposure (a common problem that costs contractors thousands in uninsured losses).

Working with an insurance partner who understands Seattle construction makes this process straightforward. We at FirstMark Insurance Group have spent 30 years guiding contractors and builders through insurance complexities specific to Pacific Northwest projects, and we compare offerings from top carriers rather than steering you toward a single insurer. Your Seattle builders risk insurance should reflect your actual needs and budget constraints, with coverage that evolves as your project progresses.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation