High net worth insurance provides specialized coverage for individuals with significant assets and complex financial situations. Standard homeowners and auto policies often fall short when protecting luxury homes, expensive collections, and substantial wealth.

We at FirstMark Insurance Group see clients regularly underestimate their coverage gaps until it’s too late. This comprehensive guide explains who needs enhanced protection and why traditional policies won’t suffice.

What Makes High Net Worth Insurance Different

High net worth insurance targets individuals with liquid assets that exceed $1 million, according to Federal Reserve data that shows comprehensive information on families’ balance sheets and financial characteristics. Standard homeowners policies typically cap personal property coverage at $300,000 to $500,000, while high net worth policies offer $2 million or more.

The coverage extends beyond basic protection to include guaranteed replacement cost coverage, which means your luxury home gets rebuilt to original specifications regardless of construction cost increases. Standard policies often exclude flood damage, kidnap protection, and coverage for art collections worth over $2,500 per item.

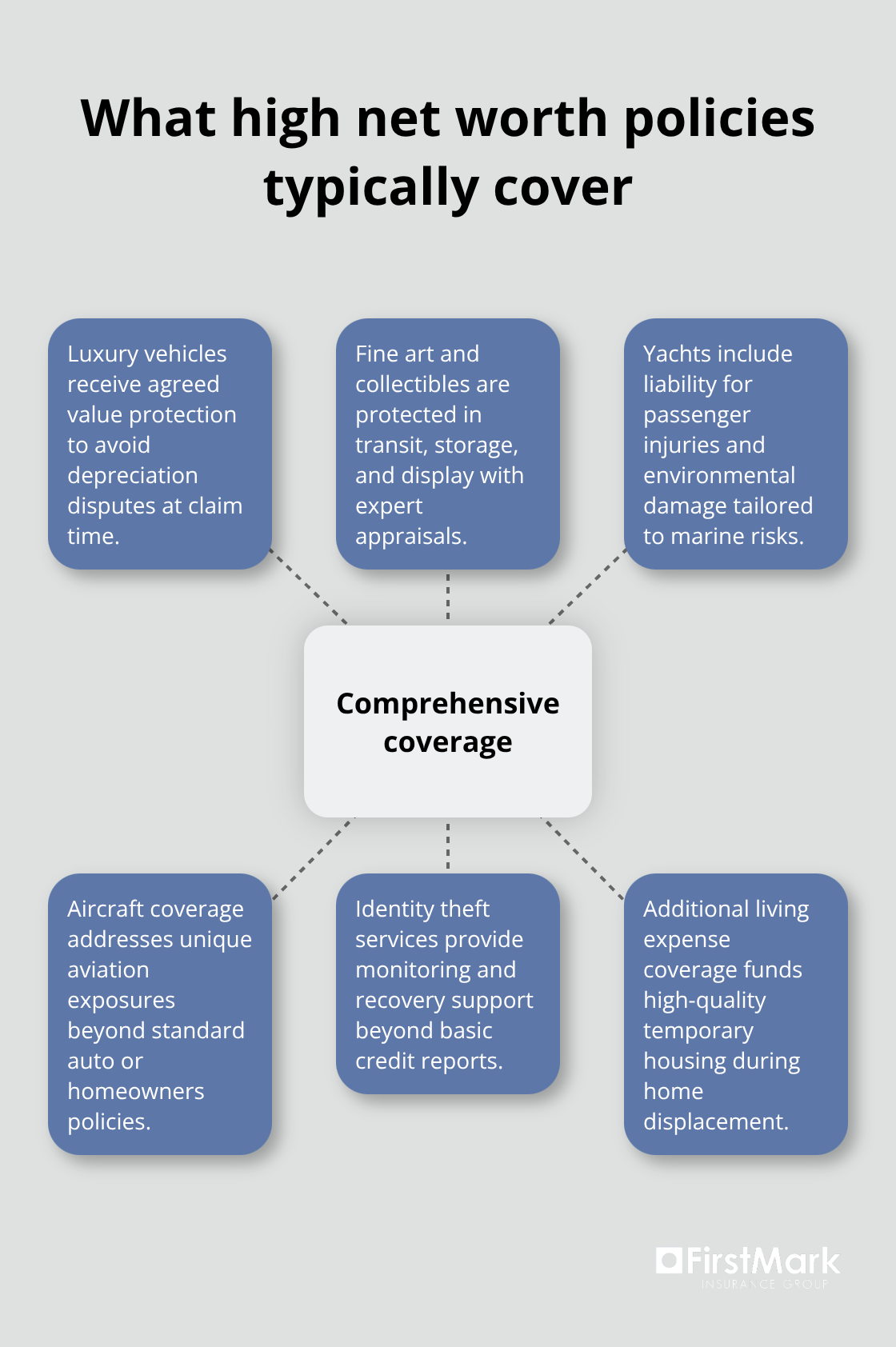

Coverage That Matches Your Assets

High net worth policies cover luxury vehicles with agreed value protection, which prevents depreciation disputes when claims occur. Fine art and collectibles receive specialized coverage that protects them during transit, storage, and display, with expert appraisers who handle valuations.

Yacht insurance includes comprehensive liability for passenger injuries and environmental damage, while aircraft coverage protects against unique aviation risks. Identity theft protection and additional expenses for alternative accommodations during home displacement complete the comprehensive approach.

These policies cost two to three times more than standard coverage, with premiums that often reach $5,000 to $15,000 annually for properties valued at $2 million or higher.

Specialized Services Beyond Basic Coverage

Risk management assessments identify vulnerabilities in your security systems, while concierge claims teams provide dedicated adjusters who understand luxury assets. Many carriers offer real-time weather alerts and emergency response coordination (features rarely found in standard policies).

Personal liability coverage extends to $10 million or more, which protects against lawsuits that target your wealth. The key difference lies in personalized service – you receive direct access to underwriters who understand unique risks like wine cellars, home theaters, and historical property maintenance requirements.

This level of specialized protection becomes even more important when you consider the specific circumstances that make high net worth insurance necessary.

Who Should Consider High Net Worth Insurance

High net worth insurance becomes necessary when your liquid assets exceed $1 million, but the real trigger point often occurs much earlier. Homeowners with properties valued above $750,000 frequently discover standard policies leave them exposed to significant gaps. The Federal Reserve Survey shows that households with net worth above $1.2 million represent the top 10 percent of wealth distribution, and these individuals face unique risks that mass market insurance cannot address.

Asset Value Thresholds That Demand Specialized Coverage

Your home’s replacement cost determines coverage needs more accurately than purchase price. Properties with custom features, historical significance, or luxury amenities require guaranteed replacement coverage that standard policies exclude. Vehicle collections worth more than $100,000 need agreed value protection to prevent depreciation disputes during claims. Art collections, jewelry, and collectibles that exceed $10,000 per item require specialized coverage with expert appraisers who understand market values.

Professional Risk Exposure Requires Enhanced Protection

Business owners, executives, and public figures face heightened liability risks that standard umbrella policies cannot handle. Medical professionals, attorneys, and financial advisors with personal wealth above $2 million become targets for litigation that seeks damages beyond professional liability coverage. Real estate investors with multiple properties need coverage that protects rental income and addresses landlord liability across different jurisdictions (particularly complex in states with varying tenant protection laws).

Lifestyle Factors That Increase Insurance Requirements

International travel, multiple residences, and recreational activities like aviation create coverage gaps in standard policies. Wine collections, home theaters, and pools add property values that exceed typical coverage limits. Domestic staff, frequent parties, and security systems introduce liability exposures that require specialized attention and coverage adjustments.

The global high net worth population reached 22 million in 2022 according to Capgemini research, which demonstrates the scale of individuals who need this protection. Anyone with combined assets and future income exceeding $500,000 should consider umbrella protection, especially those with additional risk factors. These coverage requirements translate into specific benefits and features that make high net worth insurance worth the additional investment.

What Premium Benefits Justify Higher Costs

High net worth insurance delivers coverage limits that extend far beyond standard policies, with personal property protection that reaches $5 million to $10 million compared to typical $300,000 caps. These policies provide guaranteed replacement cost coverage that rebuilds luxury homes to original specifications without depreciation calculations or construction cost limitations. Coverage includes specialized protection for wine collections up to $500,000, fine art with no per-item limits, and jewelry coverage that extends worldwide without the requirement that items remain in safes. Personal liability protection reaches $25 million or higher, which becomes essential when lawsuits target substantial assets.

Dedicated Support Teams Transform Claims Experience

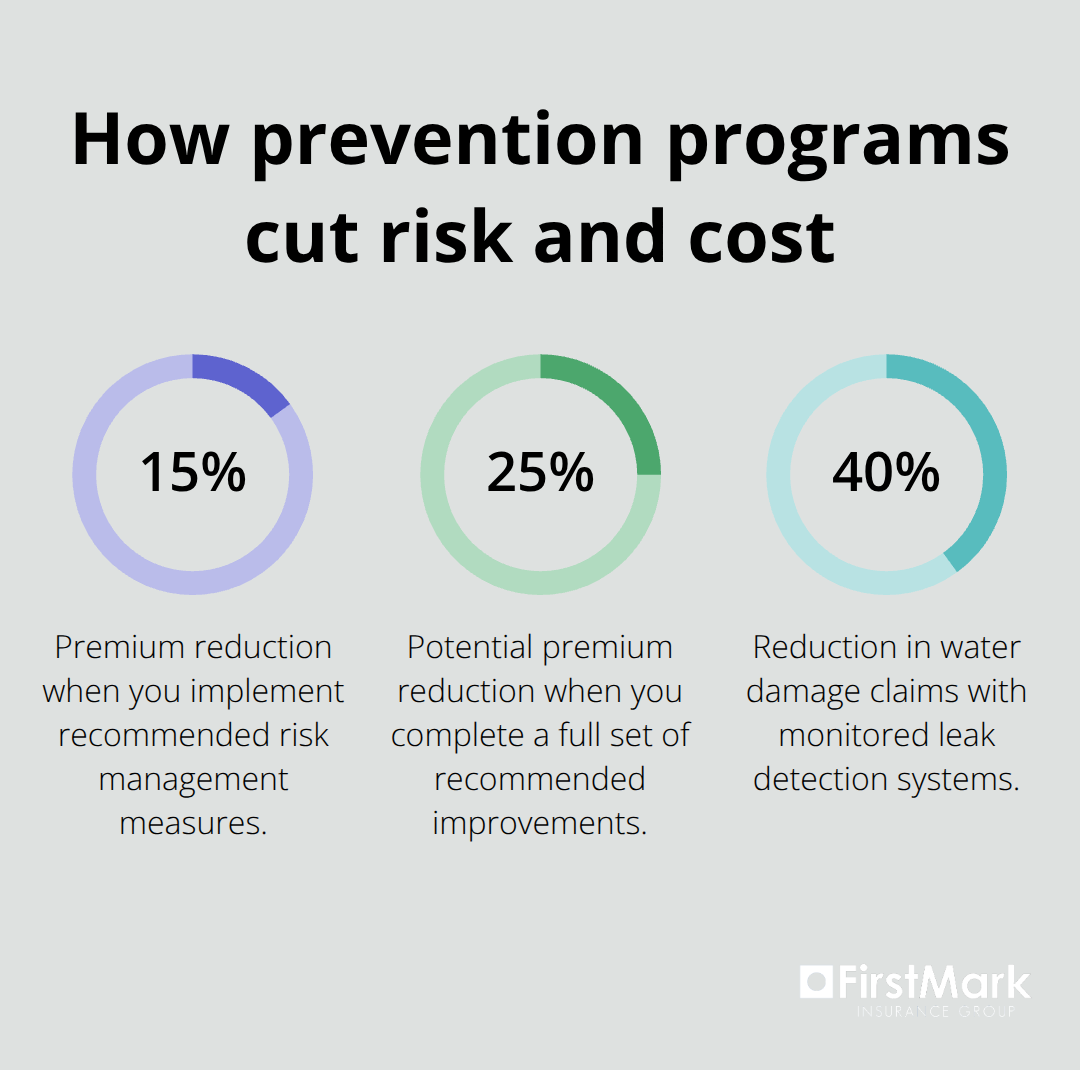

Claims processes through high net worth carriers provide dedicated adjusters who understand luxury asset valuations and specialized repair requirements. These teams coordinate with approved contractors who work exclusively on high-value properties and maintain relationships with expert appraisers for art, antiques, and collectibles. Average claim resolution times drop from 45 days with standard carriers to 21 days with specialized insurers. Risk management services include annual property inspections, security system evaluations, and personalized recommendations that can reduce premiums by 15 to 25 percent when you implement them.

Proactive Protection Prevents Costly Losses

Risk assessment programs identify vulnerabilities before losses occur, which includes water damage prevention systems that monitor pipes and foundations for early leak detection. Weather services provide real-time alerts for severe conditions, while emergency response coordination connects policyholders with vetted contractors during disasters. Identity theft services extend beyond credit reports to include social media oversight and dark web surveillance, with dedicated recovery specialists who handle restoration processes. These prevention services often save more than their cost through avoided claims with studies that show 40 percent reduction in water damage claims when you install monitoring systems.

Final Thoughts

High net worth insurance protects assets that standard policies cannot adequately cover, with specialized coverage for luxury homes, collections, and substantial wealth. The protection becomes necessary when liquid assets exceed $1 million or when property values reach $750,000, though lifestyle factors and professional risks often create coverage needs at lower thresholds. Enhanced coverage limits, guaranteed replacement costs, and dedicated claims support justify premium costs that range from $5,000 to $15,000 annually.

Risk management services and proactive protection programs prevent losses while specialized adjusters understand luxury asset valuations and complex repair requirements. These features deliver value that extends beyond basic coverage through personalized service and expert knowledge. The investment in high net worth insurance provides peace of mind that matches the scale of your assets (particularly important when standard policies leave significant gaps).

Professional guidance becomes essential when you evaluate coverage gaps and compare specialized carriers. We at FirstMark Insurance Group help families navigate insurance complexities and find coverage that matches specific needs. Start by reviewing current policy limits against actual asset values, then consult with specialists who understand high net worth insurance requirements.