Personal umbrella insurance provides extra liability protection beyond your standard home and auto policies. This additional coverage protects your assets when accident costs exceed your primary insurance limits.

We at FirstMark Insurance Group see many people confused about what is personal umbrella insurance and whether they need it. The answer depends on your assets, lifestyle, and potential liability risks.

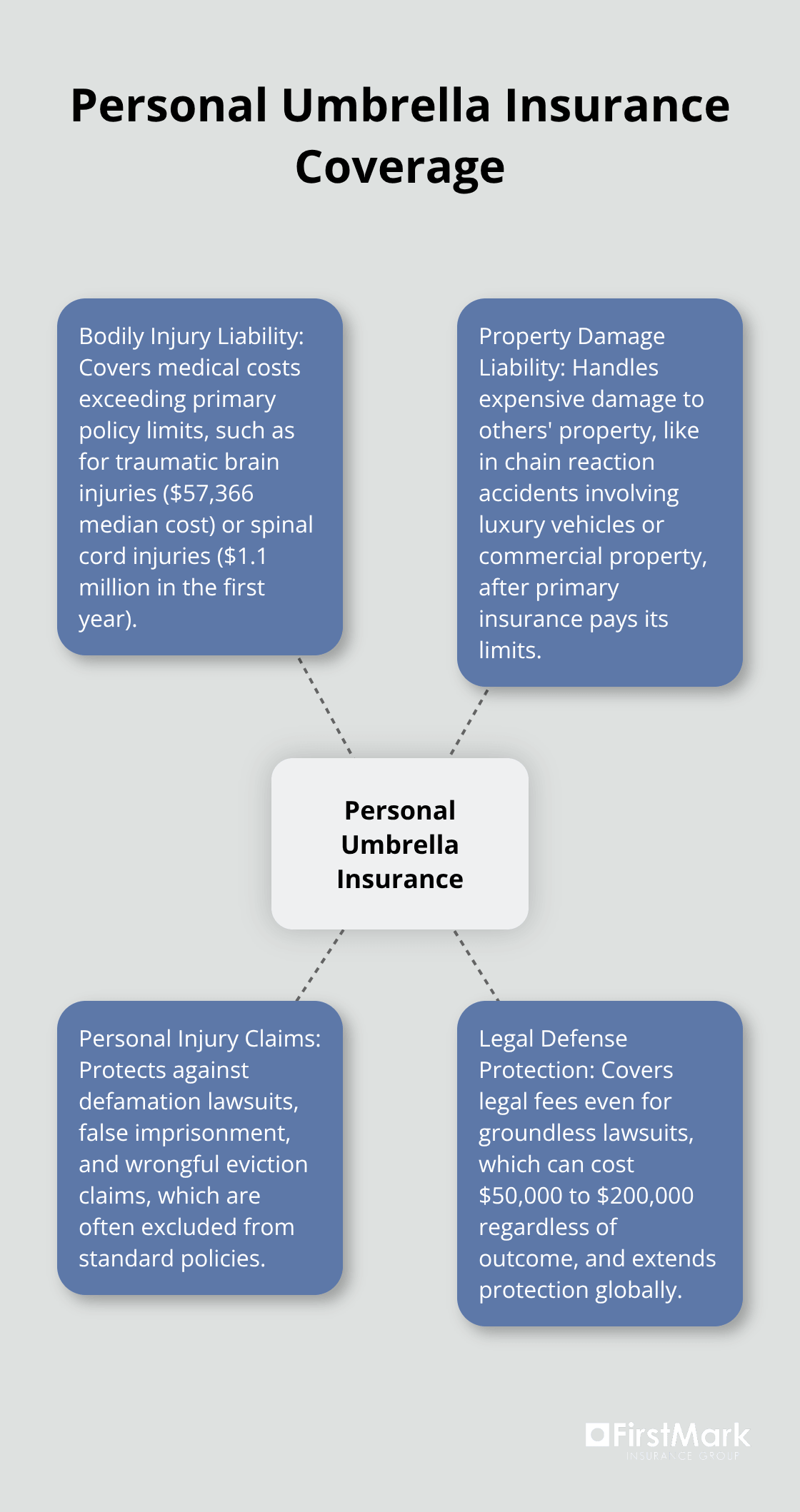

What Personal Umbrella Insurance Covers

Personal umbrella insurance steps in when your regular insurance falls short, but the coverage extends far beyond simple accident protection. The Insurance Information Institute reports that umbrella policies typically cover bodily injury claims at $1 million, which becomes vital when medical bills from serious accidents can easily reach $500,000 or more.

Bodily Injury Liability Protection

Your umbrella policy activates when someone suffers injuries that exceed your primary policy limits. Medical costs for traumatic brain injuries can result in significant expenses, with median costs reaching $57,366 according to recent data, while spinal cord injuries can cost $1.1 million in the first year alone. The policy covers these expenses when your auto or homeowners insurance reaches its maximum payout.

Property Damage Liability Coverage

Property damage coverage kicks in when you accidentally cause expensive damage to someone else’s property. Chain reaction accidents involving luxury vehicles or commercial property can generate claims exceeding $1 million. Your umbrella policy handles these costs after your primary insurance pays its limits (typically $300,000 to $500,000).

Personal Injury and Defamation Claims

The most overlooked aspect of umbrella coverage involves personal injury claims that standard policies exclude entirely. These policies protect against defamation lawsuits, false imprisonment, and wrongful eviction claims. According to the National Association of Insurance Commissioners, personal injury claims now represent a substantial portion of umbrella insurance payouts, with the other liability claims-made and occurrence line showing significant growth to $114.6 million.

Legal Defense Protection

Umbrella policies cover legal fees even when lawsuits prove groundless, which matters because major liability claims cost $50,000 to $200,000 to defend regardless of the outcome. The coverage extends globally, protecting you from incidents anywhere in the world.

Understanding these coverage areas helps you evaluate whether umbrella insurance fits your specific situation and risk profile.

When You Need Personal Umbrella Insurance

Your net worth determines your umbrella insurance needs more than any other factor. The Insurance Information Institute data shows that anyone with assets exceeding $500,000 should seriously consider umbrella coverage, but the real threshold sits much lower when you factor in future income potential. A surgeon who earns $400,000 annually faces decades of income at risk, which makes a $2 million umbrella policy worth $150 annually a smart investment.

High-net-worth individuals with multiple properties, investment portfolios, or business interests become prime lawsuit targets. Umbrella policies protect these accumulated assets from complete liquidation when standard coverage falls short.

High Net Worth Individuals and Asset Protection

Wealthy individuals face unique liability risks that standard insurance cannot address. Investment portfolios, real estate holdings, and business ownership create multiple attack points for aggressive attorneys. A single serious accident can wipe out decades of wealth accumulation without proper umbrella protection.

Personal injury case settlements have been steadily rising, with an average settlement amount of $113,391 based on data from 2016 to 2023. Standard homeowners policies typically cap liability at $300,000 to $500,000, which leaves substantial gaps in protection for affluent families.

Homeowners with Swimming Pools or Trampolines

Swimming pool accidents generate some of the most expensive liability claims in homeowners insurance. The Consumer Product Safety Commission reports approximately 390 pool-related deaths annually among children under 15, with each wrongful death lawsuit averaging $1.2 million in settlements.

Trampoline injuries send 100,000 people to emergency rooms yearly according to the American Academy of Pediatrics. Paralysis cases from trampoline accidents reach $3 million in damages, far beyond what standard homeowners policies cover.

People in High-Risk Professions

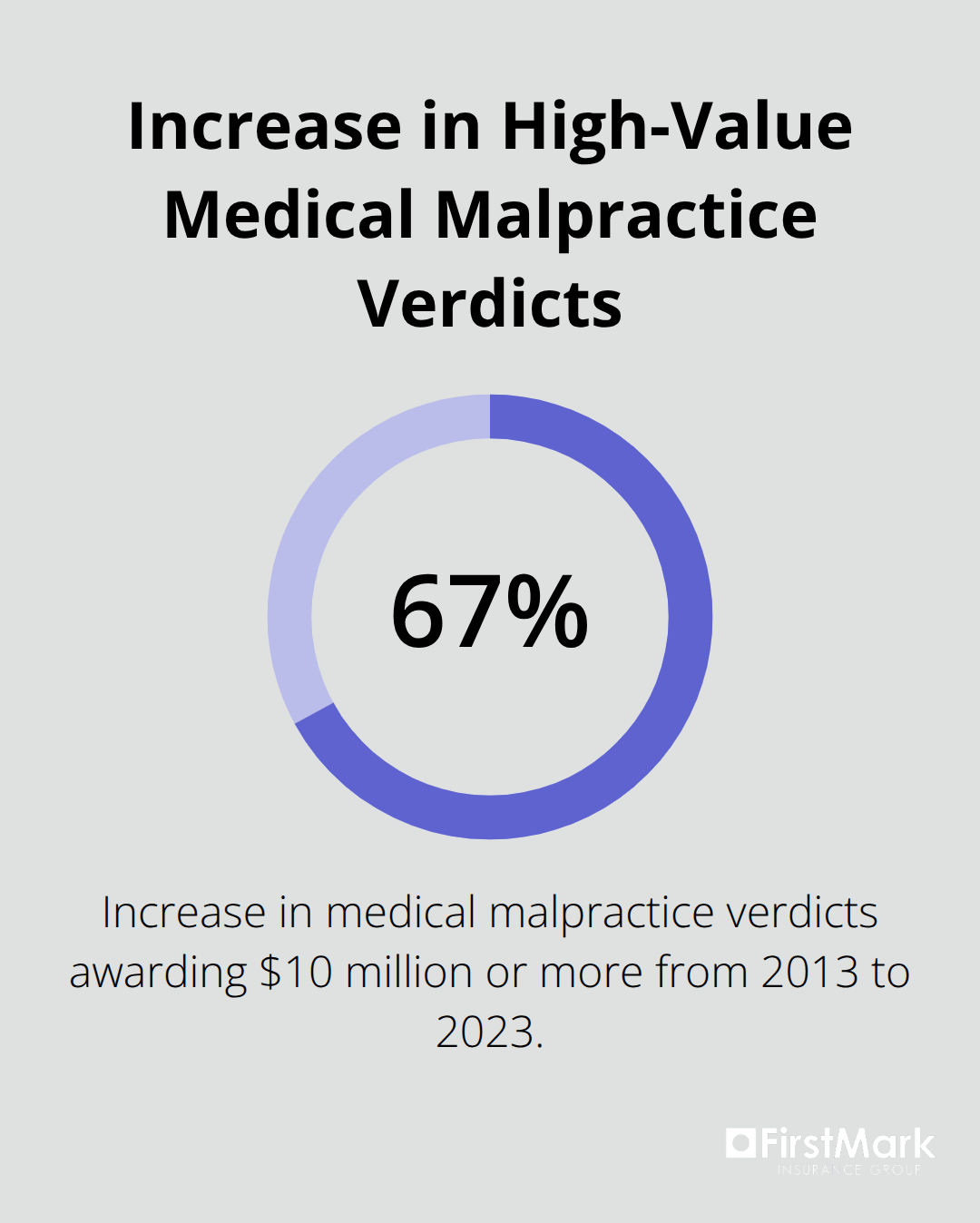

Doctors, lawyers, real estate agents, and business executives face elevated lawsuit risks that make umbrella insurance essential rather than optional. Medical malpractice attorneys increasingly target physicians’ personal assets when professional liability limits fall short of jury awards, with the American court system seeing a roughly 67% increase in medical malpractice verdicts awarding $10 million or more from 2013 to 2023.

Real estate professionals who handle million-dollar transactions encounter contract disputes that can escalate into personal liability claims. Corporate executives deal with employment decisions, board responsibilities, and public visibility that expose them to defamation and wrongful termination lawsuits.

These profession-specific risks highlight why umbrella coverage becomes more important as your career advances and your liability exposure grows.

How Personal Umbrella Insurance Works

Personal umbrella insurance operates as a secondary layer that activates only after your primary insurance policies reach their maximum limits. When a liability claim exceeds your homeowners policy limit of $300,000, your umbrella coverage immediately steps in to handle the remaining costs. This seamless transition protects you from massive out-of-pocket expenses that could bankrupt most families.

Coverage Kicks In After Primary Policy Limits

Your umbrella policy waits in the background until your primary insurance exhausts its limits. The system works automatically without gaps in protection. When someone files a lawsuit against you for $800,000 and your homeowners insurance covers only $500,000, the umbrella policy handles the remaining $300,000 plus all legal fees.

Typical Coverage Amounts and Cost Structure

Umbrella policies begin at $1 million and increase in million-dollar increments up to $10 million or more. Most insurers require minimum underlying coverage of $300,000 on homeowners and $500,000 on auto policies before they issue umbrella protection. Commercial insurance rates have shown mixed trends, with rates moderating in recent quarters.

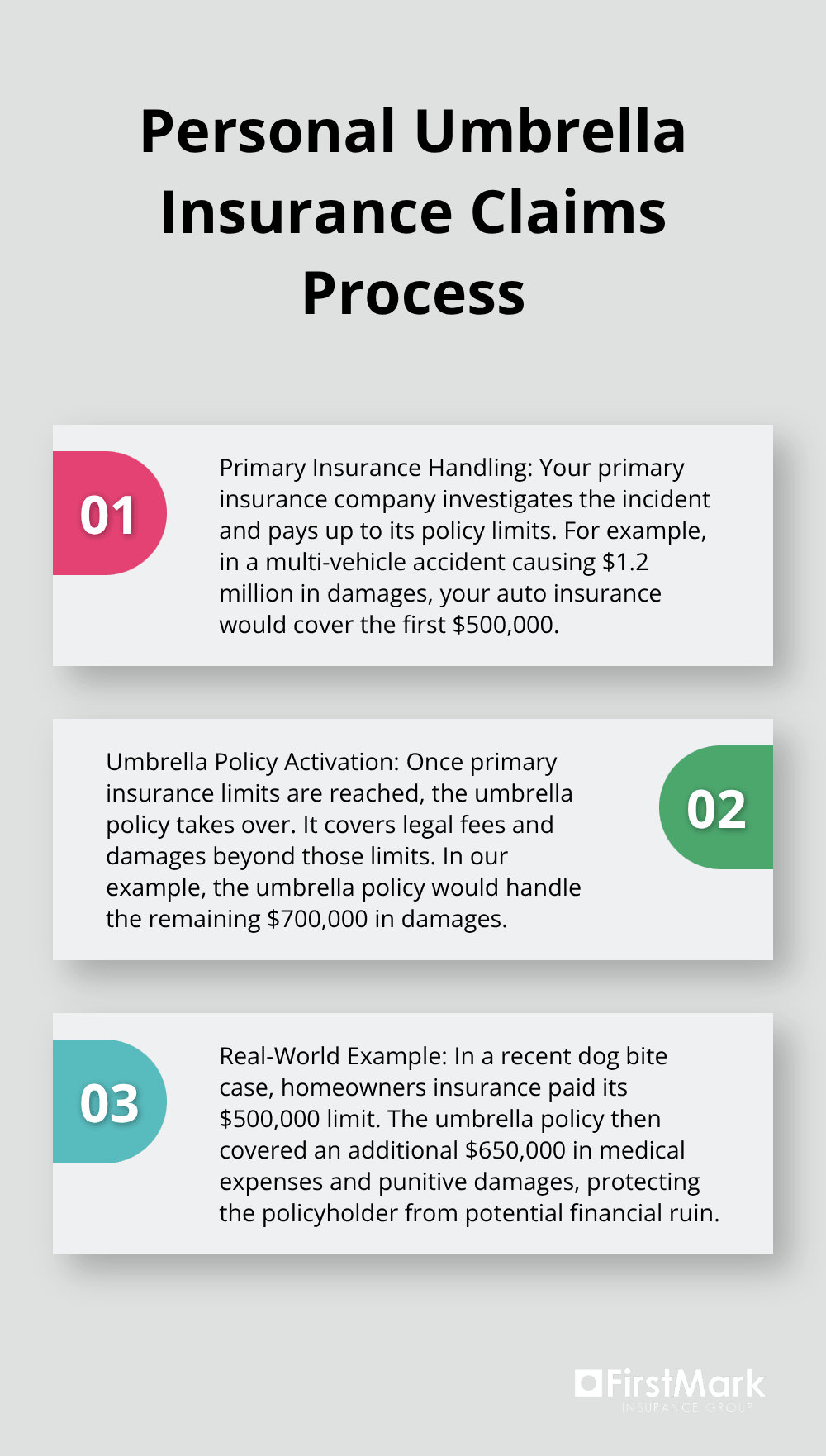

Claims Process and Real-World Examples

When an incident occurs, your primary insurance company handles the initial investigation and pays up to its policy limits. The umbrella insurer then takes over the claim and covers legal fees plus damages beyond those limits. In a recent dog bite case, homeowners insurance paid its $500,000 limit while the umbrella policy covered an additional $650,000 in medical expenses and punitive damages.

Consider a multi-vehicle accident where you cause $1.2 million in damages. Your auto insurance covers the first $500,000, which leaves you responsible for $700,000 without umbrella protection. That amount would force most people into bankruptcy, while a $1 million umbrella policy would handle the entire remaining balance.

Final Thoughts

Personal umbrella insurance provides millions in additional liability coverage for just a few hundred dollars annually. It covers legal defense costs even for groundless lawsuits, which can cost $50,000 to $200,000 regardless of outcome. The policy also protects against personal injury claims like defamation that standard policies exclude entirely.

You need to assess your total assets and liability exposure honestly to determine if you need coverage. Calculate your net worth with home equity, investments, and retirement accounts included. Anyone with combined assets and future income exceeding $500,000 should consider umbrella protection (especially pool owners, pet owners, and high-profile professionals who face elevated lawsuit risks).

We at FirstMark Insurance Group help families navigate insurance complexities and find coverage that fits their specific needs. Our team explores options from top providers to match your unique risk profile with appropriate protection levels. Contact us to discuss what is personal umbrella insurance and whether it makes sense for your situation.