General liability claims in Seattle cost businesses an average of $50,000 to $100,000 in legal fees alone, even when they’re found not at fault. That’s why Seattle general liability insurance isn’t optional-it’s a business essential.

At FirstMark Insurance Group, we’ve helped hundreds of Seattle business owners understand what coverage actually protects them. The right policy shields your company from bodily injury claims, property damage lawsuits, and the legal costs that follow.

What Your General Liability Policy Actually Covers

Bodily Injury Claims and Medical Expenses

General liability insurance in Seattle protects your business against three categories of real-world claims that can drain your cash reserves quickly. Bodily injury claims occur when someone suffers an injury on your premises or because of your operations-a customer slips on a wet floor at your retail location, a client trips over equipment at your job site, or a third party sustains an injury connected to your work. Your policy pays medical bills, hospital costs, rehabilitation expenses, and lost wages for the injured party, plus your legal defense costs if the claim goes to court. These aren’t hypothetical scenarios; they’re everyday risks Seattle businesses face. Slip and fall claims average between $10,000 and $50,000 in total costs.

Property Damage and Repair Costs

Property damage claims cover situations where your business operations damage someone else’s property. You might accidentally damage a client’s flooring during an installation, your equipment might cause harm to a neighboring business, or your service might create structural damage to a building. The policy covers repair costs, replacement value, and your legal defense expenses. These claims happen more often than many business owners realize, particularly in construction, installation, and service-based industries across the Seattle area.

Product Liability and Completed Operations Coverage

Product liability and completed operations coverage extend protection beyond your immediate premises. If you manufacture or sell a product that injures someone after they purchase it, product liability covers the claim. Completed operations coverage protects you after you’ve finished a job-if your electrical work causes a fire six months later, or your plumbing installation leads to water damage, this coverage responds to those claims. Many Seattle contractors overlook this aspect until a problem surfaces.

Understanding Defense Costs and Legal Expenses

Legal defense costs sit outside your policy limits in most cases, meaning your insurer pays lawyers, court fees, and expert witnesses separately from your coverage limit. This distinction matters significantly because a defended lawsuit easily reaches substantial legal expenses before any settlement is paid. Understanding how your policy structures these costs helps you plan for the financial realities of a claim.

With these coverage categories in mind, the question shifts to why Seattle businesses specifically need this protection and what obligations drive the decision to carry a policy.

Why Your Seattle Business Needs This Coverage

Contractual Obligations Lock You Into Coverage

General liability insurance isn’t a nice-to-have in Seattle-it’s a requirement embedded in how business actually works here. Landlords won’t lease space without proof of coverage. Clients won’t sign contracts. General contractors won’t hire subcontractors. The Washington Office of the Insurance Commissioner confirms that while state law doesn’t mandate general liability for most businesses, contractual obligations and lease requirements make it unavoidable in practice. Licensed contractors face explicit minimum coverage requirements, and local municipalities impose their own thresholds. A Certificate of Insurance, issued by your policy, becomes the currency of trust in Seattle business relationships. Without it, you’re locked out of opportunities before risk even enters the picture.

Claims Cost Far More Than Most Owners Expect

General liability claims in Seattle range from $50,000 to $100,000 in legal fees alone, even when your business is found not at fault. Legal defense costs typically sit outside your policy limits, meaning your insurer covers attorney fees separately from your coverage limit-a distinction that matters when you’re facing $100 to $500 per hour in legal expenses according to industry standards. A single slip-and-fall claim averages $10,000 to $50,000 in total costs. A product liability claim or a completed operations issue can exceed six figures. Without insurance, these costs come directly from your operating capital, your reserves, or forced asset sales.

Coverage preserves your business operations

With coverage in place, your policy responds up to your limits, preserving cash flow and operational continuity. Your policy protects not just your balance sheet but your ability to operate, hire employees, and serve clients without constant financial vulnerability hanging overhead.

Determining Your Coverage Needs Requires Professional Guidance

The financial consequences of operating without coverage are severe enough to threaten business survival. Your specific exposure depends on your industry, location, revenue, and the contracts you sign with clients and landlords. Understanding what coverage limits you actually need-and how to structure that protection-requires more than a quick online quote.

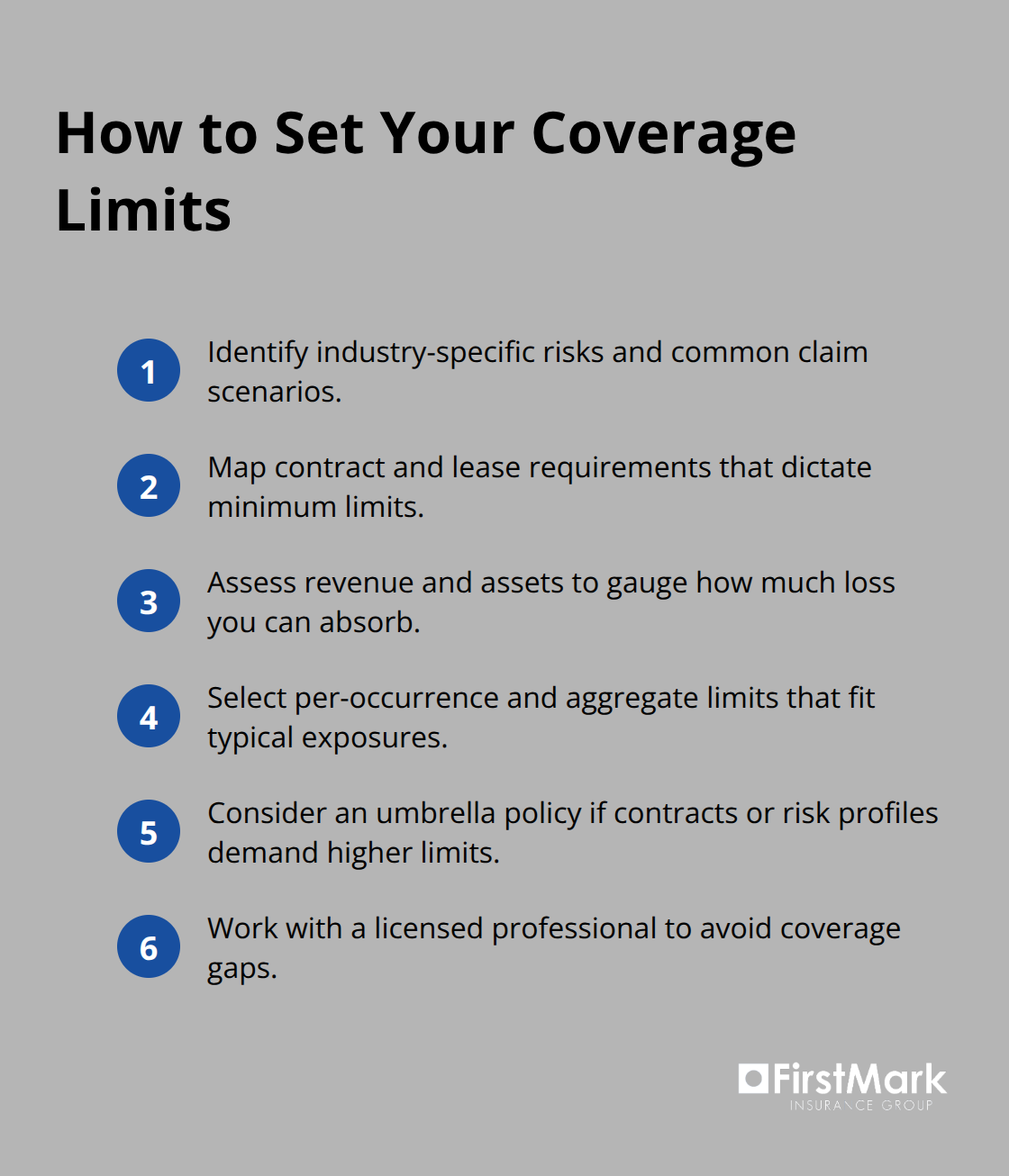

How to Choose the Right Coverage Limits for Your Seattle Business

Your Industry Determines Your Actual Exposure

Your industry shapes your liability exposure more than anything else. A Seattle coffee shop faces slip-and-fall claims and product liability from beverages, while a plumbing contractor faces completed operations exposure that can emerge months after a job finishes. The Hartford’s 2026 analysis found that general liability costs in Washington range from $19 per month for drone operators to $1,046 per month for pressure washing services, reflecting how dramatically risk varies by sector. Your specific industry determines not just your premium but your actual coverage needs.

Construction trades, HVAC contractors, and installation services typically need $1 million to $2 million per occurrence because a single job can create years of tail exposure. Service businesses and retail operations often operate effectively with $1 million per occurrence. Cannabis businesses in Washington face a state-mandated minimum of $1 million, according to WAC 314-55-082.

Before you think about numbers, identify exactly what your business does and what could go wrong. A claim from your work might surface six months or two years later. That’s not theoretical-it’s why contractors in Seattle specifically need coverage that extends beyond the day the job ends.

Your Revenue and Assets Shape Your Financial Capacity

Your revenue and assets determine your financial capacity to absorb a claim, which directly shapes how much coverage you actually need. A business with $500,000 in annual revenue cannot absorb a $250,000 settlement the same way a $5 million business can. Most Seattle businesses carry $1 million per occurrence and $2 million aggregate limits because that range protects typical operations without overextending premiums.

However, if your contracts require higher limits-and many large clients and municipalities do-your coverage must match those requirements or you cannot bid the work. Review every client contract, lease agreement, and vendor relationship you have; these documents tell you exactly what limits your business must carry to operate.

Your assets matter too. If you own your building, vehicles, and significant equipment, a liability claim that exhausts your coverage limit leaves you personally exposed.

Professional Guidance Prevents Coverage Gaps

An insurance professional reviews your actual contracts, understands your industry-specific exposure, and recommends limits based on what you do rather than generic benchmarks. They verify that your coverage limits match your contractual obligations and your financial exposure. They also identify whether you need additional protections like umbrella policies for extra limits or professional liability coverage for service-based work.

FirstMark Insurance Group brings 30 years of experience guiding businesses through these decisions. We explore offerings from top insurance providers and present you with choices that fit your requirements at the best available pricing. Getting coverage decisions wrong means either paying for protection you don’t need or carrying limits that don’t actually shield your business when a claim surfaces.

Final Thoughts

Seattle general liability insurance protects your business from the financial devastation that follows a single claim. Claims cost far more than most owners expect, contractual obligations make coverage non-negotiable, and your specific industry determines exactly what limits you need. The right coverage preserves your ability to operate, serve clients, and build your business without constant financial vulnerability.

Securing the right coverage starts with understanding your actual exposure. Review your client contracts, lease agreements, and vendor relationships to identify what limits those documents require. Assess your industry risk honestly-a contractor’s exposure differs fundamentally from a retail business’s exposure. Calculate your financial capacity to absorb a claim if one surfaces, and these steps clarify what protection your business actually needs.

Contact FirstMark Insurance Group today to review your current coverage or explore options if you’re operating without protection. We’ve spent 30 years guiding Seattle businesses through these decisions and present you with choices that fit your requirements at the best available pricing. We help you find the coverage that matches your actual exposure and contractual obligations, delivering the peace of mind that allows you to focus on growth rather than risk management anxiety.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation