Choosing the right insurance protection for your business means understanding what coverage you actually need. A business owners policy and general liability insurance serve different purposes, and picking between them can significantly affect your bottom line.

At FirstMark Insurance Group, we help business owners cut through the confusion. The right choice depends on your specific industry, size, and risk profile.

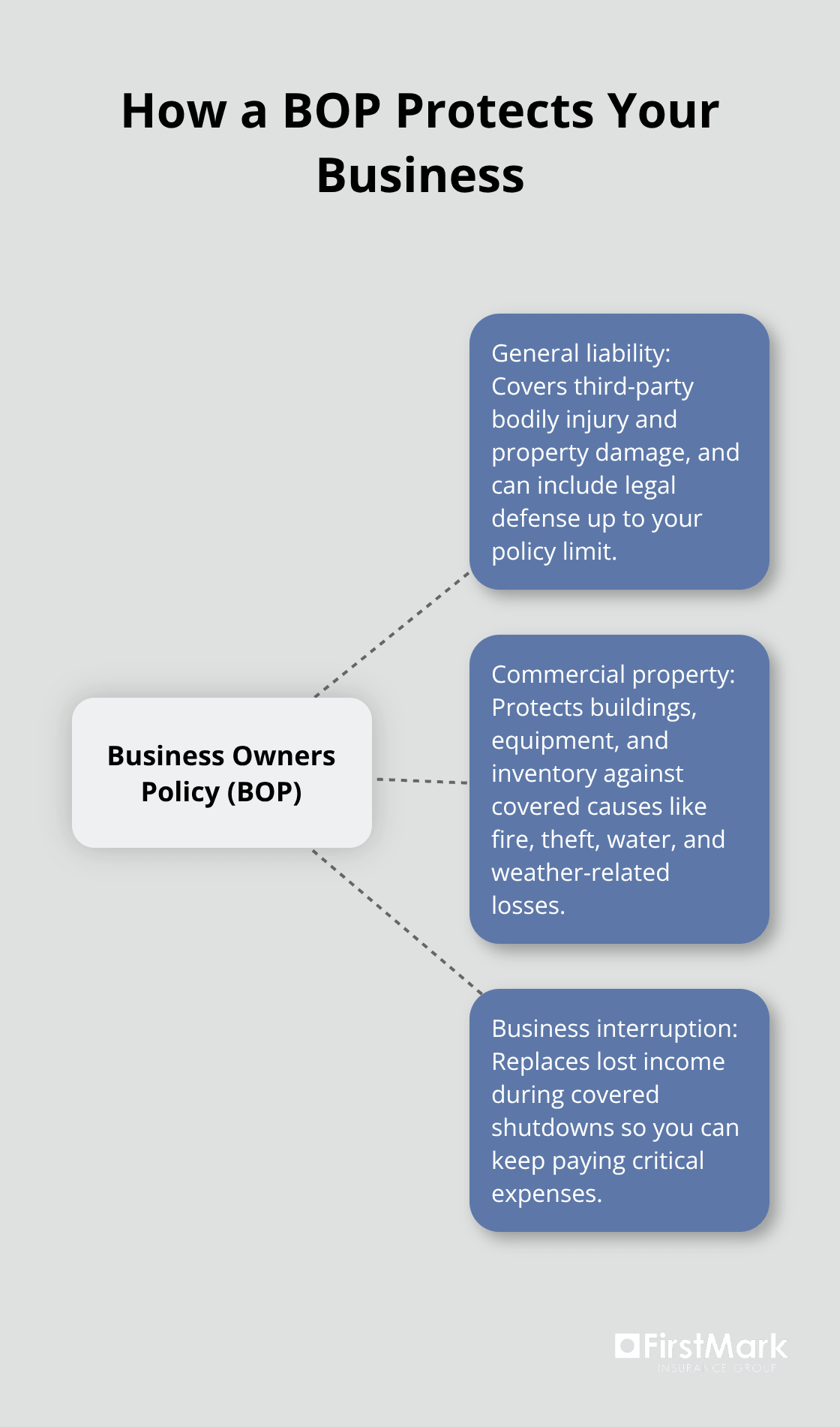

What is a Business Owners Policy

A Business Owners Policy bundles three essential protections into a single package: general liability coverage, commercial property insurance, and business interruption coverage. This combination addresses the most common risks that small businesses face. General liability covers third-party bodily injury and property damage claims, commercial property protects your physical assets like equipment and inventory, and business interruption replaces lost income if a covered event forces temporary closure. This structure combines core coverages into one convenient policy, which is exactly why many small business owners prefer it. The bundling approach works because these three exposures typically occur together-when a water pipe bursts, it damages your property, disrupts operations, and creates liability if someone gets hurt.

Three Core Components Working Together

Your physical location and equipment face constant risk. A retail shop with inventory, a café with kitchen equipment, or a light manufacturing facility with machinery all carry significant property exposure that general liability alone won’t cover. Commercial property insurance within a BOP protects against fire, theft, water damage, and weather-related losses. When a backroom leak destroyed a retail shop’s inventory, the property coverage paid out $12,000 in replacement costs, while a general liability-only policy would have left that loss completely unprotected. Business interruption coverage proves equally practical-it replaces your income during shutdown periods. A small café that upgraded from general liability to a BOP recovered about $8,500 in lost revenue after equipment breakdown forced a three-day closure. Without this coverage, that revenue simply disappears. The combination of these three protections means you protect your assets and your income simultaneously, rather than choosing between them.

Pricing and Practical Savings

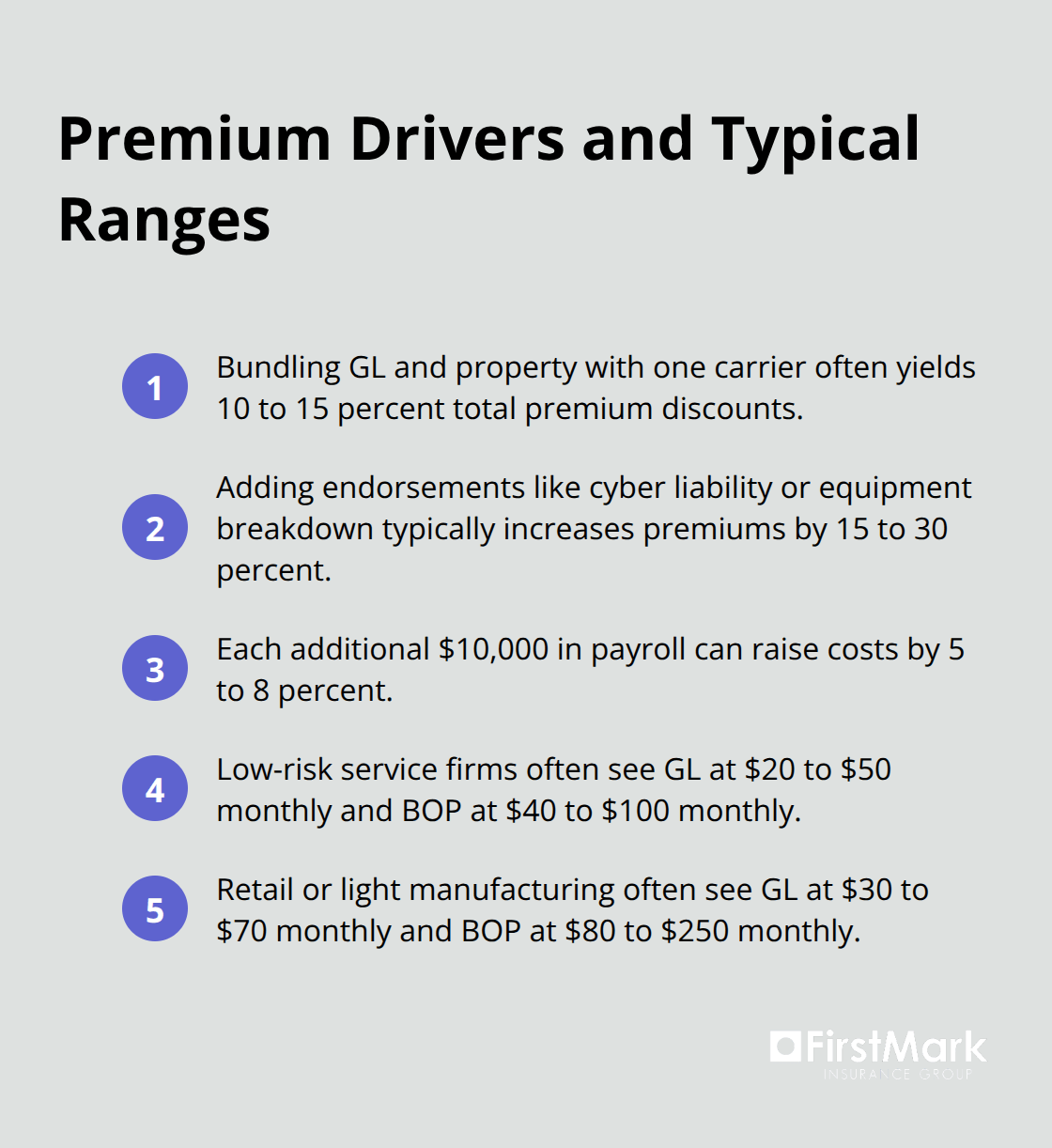

The cost advantage of bundling is substantial. A BOP typically costs around $57 per month, compared to buying general liability at $42 monthly and commercial property at $67 monthly separately. That difference equals roughly $52 per month or $624 annually in your favor. Bundling into a BOP yields 10 to 15 percent total premium discounts when you consolidate coverage with a single carrier. Cost ranges vary by industry-a low-risk service firm might see GL at $20 to $50 monthly with a BOP at $40 to $100 monthly, while retail or light manufacturing jumps to GL at $30 to $70 monthly and BOP at $80 to $250 monthly. Your actual premium depends on your industry classification, geographic location, payroll size, and chosen coverage limits.

Adding endorsements for extra protection like cyber liability or equipment breakdown typically raises premiums by 15 to 30 percent, and each additional $10,000 in payroll can push costs up by 5 to 8 percent. Most business owners underestimate how much a single property claim or revenue loss would cost-having both protections bundled at a lower price point makes practical sense for anyone with a physical location, owned equipment, or inventory at risk.

Who Should Consider a BOP

Small businesses with physical locations benefit most from a BOP structure. If you operate a storefront, office, warehouse, or any space where you own or lease equipment and inventory, a BOP addresses your actual risk profile. Lease agreements and lender requirements often mandate property and interruption coverage, and a BOP satisfies these obligations in a single policy. Service-based businesses with minimal physical assets may find general liability alone sufficient and more cost-effective. However, even service firms that maintain office equipment, client meeting spaces, or specialized tools should evaluate whether property protection makes financial sense. The decision ultimately rests on whether you have assets worth protecting and whether a temporary shutdown would create significant revenue loss. Understanding your specific exposure helps determine which policy structure aligns with your business operations and financial priorities.

Understanding General Liability Insurance

What General Liability Actually Covers

General liability insurance protects you against claims from third parties who claim your business caused them harm. A customer trips on your shop floor and breaks their leg-that’s bodily injury coverage. An employee damages a client’s computer during a service call-that’s property damage coverage. Someone claims your advertisement infringed their copyright-that’s advertising injury coverage. These three categories form the backbone of general liability and address real exposures that most businesses face. General liability covers third-party bodily injury, third-party property damage, and advertising injury, which means your own property damage and employee injuries fall outside this protection. This distinction matters because many business owners assume general liability covers everything until a claim reveals otherwise. The policy also pays legal defense costs, settlements, and judgments up to your chosen limit, so even frivolous claims won’t drain your personal resources immediately.

Real Claims That Trigger Coverage

Premises liability claims occur when a customer slips on a wet floor and suffers injury. Product liability claims arise when a defective item you sold causes harm to the buyer. Motor vehicle accidents involving your business vehicle activate coverage for third-party injuries and property damage. These scenarios represent genuine exposures that most businesses encounter at some point.

Coverage Limits and Deductibles Shape Your Protection

You choose a limit-say $1 million per occurrence-which caps what the insurer pays for any single claim. A deductible is what you pay first before coverage kicks in, typically ranging from $500 to $2,500 depending on your policy. Lower deductibles mean higher premiums, while higher deductibles reduce your monthly cost but increase your risk if a claim happens.

Critical Coverage Gaps That Create Real Problems

General liability alone creates significant problems because it doesn’t cover your own property, your lost income during a shutdown, or employee injuries. A light manufacturer facing an $18,000 equipment repair after a fire receives zero dollars from general liability because that damage affects their own property. A service business forced to close for two weeks due to a covered event gets no income replacement. These gaps aren’t minor oversights-they represent the exact situations that threaten business survival. The financial exposure you face without property and income protection is substantial and cannot be ignored.

Why These Gaps Matter for Your Bottom Line

When a water pipe bursts in your office, general liability won’t pay for the damaged equipment or furniture. When a fire forces you to relocate temporarily, general liability won’t replace the revenue you lose during the shutdown. When an employee gets injured on the job, general liability won’t cover their medical costs or lost wages. These three scenarios happen regularly across small businesses, and general liability leaves you completely exposed in each situation. Understanding what falls outside your coverage helps you recognize whether additional protections make financial sense for your specific operation. The question isn’t whether these risks exist-they do-but whether you can afford to absorb the financial impact if they occur. This reality is exactly why many business owners explore bundled coverage options that address multiple exposures simultaneously rather than relying on a single policy that leaves critical gaps unprotected.

Which Policy Protects Your Business Better

Understanding the Core Protection Difference

The fundamental difference between a BOP and general liability comes down to what happens when disaster strikes your business. General liability covers third-party claims only, meaning if someone else sues you for injury or property damage, you’re protected up to your policy limit. A BOP covers those same third-party claims but adds protection for your own physical assets and lost revenue during shutdowns. This distinction determines whether you absorb catastrophic costs yourself or transfer them to an insurer.

Real Scenarios That Reveal Coverage Gaps

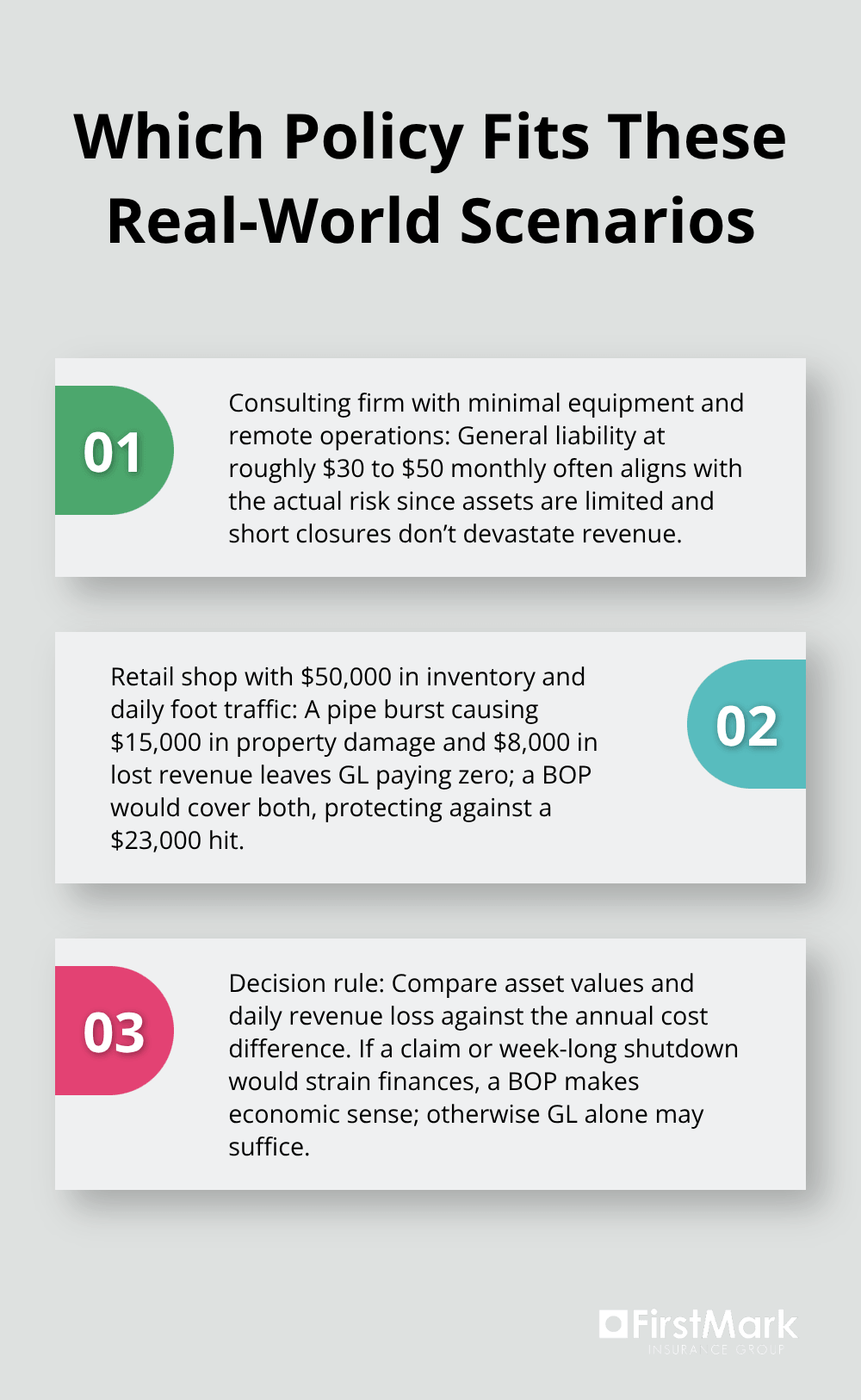

Consider a consulting firm operating from a leased office with minimal equipment and no inventory. General liability at $30 to $50 monthly handles their actual risk exposure because they have few assets to protect and a temporary closure wouldn’t devastate revenue since most work happens remotely. Now consider a retail shop with $50,000 in inventory, owned display equipment, and daily foot traffic. A water pipe burst causes $15,000 in inventory damage and forces a five-day closure costing $8,000 in lost revenue. General liability pays zero dollars. A BOP would have covered both losses completely if your business is unable to operate due to coverage property damage, like fire damage.

The cost difference between these scenarios is roughly $52 monthly or $624 annually, yet that BOP would have protected against a $23,000 loss. This is why the decision isn’t about choosing the cheaper option-it’s about matching coverage to your actual business structure and financial vulnerability.

How Industry Type Shapes Your Coverage Needs

Premium costs shift dramatically based on your industry and assets. A service-based business with no physical location might find general liability sufficient at $20 to $50 monthly, making the additional $20 to $50 monthly BOP cost unnecessary. A retail operation faces completely different economics, with general liability at $30 to $70 monthly proving inadequate while a BOP at $80 to $250 monthly becomes financially rational when you calculate potential property and income losses. Light manufacturing businesses particularly benefit from BOP coverage since equipment failures and facility shutdowns create dual exposures that general liability ignores. Bundling GL and property with the same carrier yields 10 to 15 percent total premium discounts, meaning you often pay less for comprehensive protection than you would for general liability alone when you factor in the real cost of uninsured losses.

Calculating Your Actual Financial Exposure

Your specific numbers matter more than generic premium comparisons. A business that generates $10,000 daily revenue faces $50,000 in losses for every five days of shutdown, which exceeds the annual cost difference between policies within weeks. Similarly, a manufacturing facility with $200,000 in equipment faces catastrophic exposure without property coverage. Your decision should rest on calculating your actual asset value and daily revenue impact, then comparing those figures against the annual premium difference between policies. If a single property claim or week-long shutdown would strain your finances significantly, a BOP makes economic sense regardless of the monthly premium. If you operate with minimal assets and your business can sustain temporary disruptions, general liability alone might suffice for your specific situation.

Final Thoughts

The choice between a business owners policy vs general liability insurance depends entirely on your business structure, assets, and financial vulnerability. If you operate a physical location with equipment, inventory, or leased space, a BOP provides comprehensive protection that general liability cannot match-addressing property damage, income loss, and liability claims in one policy, often at a lower total cost than purchasing coverage separately. Service-based businesses with minimal physical assets and the ability to sustain temporary disruptions may find general liability alone sufficient while keeping premiums lower.

Your insurance requirements shift as your business grows and evolves. A startup operating from home might function effectively with general liability, but adding office space or equipment changes that equation entirely. Reviewing your coverage annually ensures your protection keeps pace with your business changes rather than leaving you exposed to new risks you didn’t anticipate.

The practical next step involves calculating your actual financial exposure by determining your total asset value, estimating your daily revenue, and considering how long your business could survive a facility shutdown. We at FirstMark Insurance Group help business owners navigate this decision with clarity, working with top insurance providers to present coverage options that fit your requirements at the best available pricing. Contact us to discuss your specific situation and explore the protection that makes sense for your business.