Running a contracting business in Washington means navigating complex insurance requirements that vary by project type and location. Professional contractors insurance in Washington isn’t optional-it’s a legal requirement that protects your business, your team, and your clients.

At FirstMark Insurance Group, we work with local contractors daily to build coverage that matches their actual risk exposure. This guide walks you through what you need to know to operate with confidence.

What Coverage Do Washington Contractors Actually Need

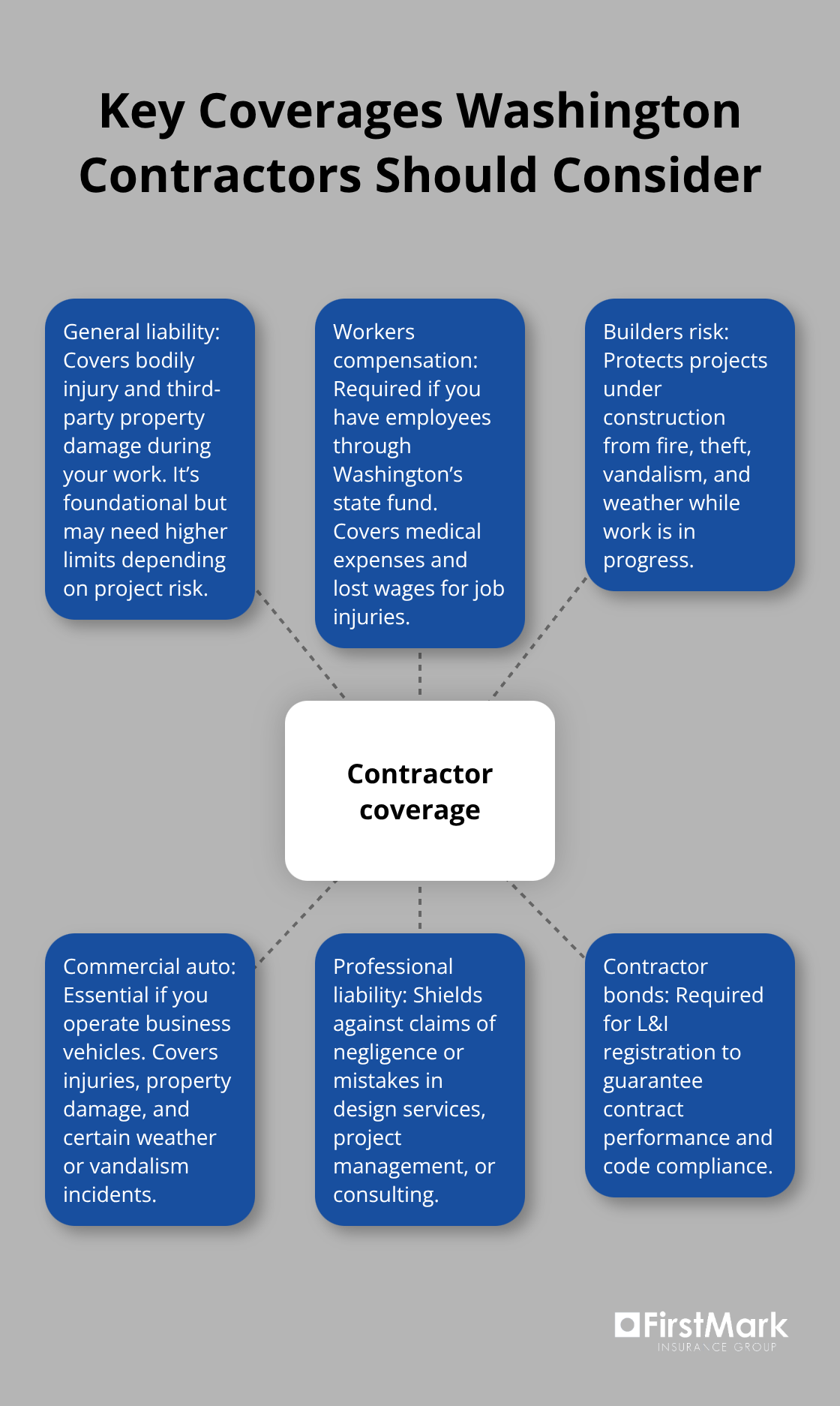

General liability insurance forms the foundation of any contractor’s coverage in Washington, but it’s far from the complete picture. This policy covers bodily injury and third-party property damage that occur during your work-a client injured at a job site or damage to a neighbor’s fence during a project. Washington requires contractors registering with the Department of Labor & Industries to carry at least $200,000 in public liability and $50,000 in property damage coverage, or $250,000 combined single limit.

However, the actual coverage mix depends entirely on your specific work. A painter needs different protection than an electrician, and a general contractor coordinating multiple trades faces risks that specialty contractors don’t encounter.

The mandatory policies for Washington contractors

Workers compensation stands as a legal requirement if you have employees. Washington operates a monopolistic state fund for workers compensation, meaning you must carry coverage through the state system. According to the Washington Department of Labor & Industries workers compensation requirements, this covers medical expenses and lost wages for employees injured on the job and protects your business from employee lawsuits. The baseline premium hovers around $750 annually, though actual costs vary significantly by job classification and business size. Beyond workers compensation and general liability, builders risk insurance protects your projects during construction. This covers damage from fire, theft, vandalism, and weather events while work is in progress. Commercial auto insurance becomes essential if you operate business vehicles, covering injuries, property damage, and incidents from weather or vandalism.

Coverage gaps that expose your business to risk

Professional liability insurance, also called errors and omissions coverage, protects against claims of negligence or mistakes in your work. If you provide design services, project management, or construction consulting, this coverage becomes non-negotiable. Many contractors overlook this thinking their general liability covers professional mistakes-it doesn’t. Equipment and tools insurance pays to repair or replace tools lost, stolen, or damaged at worksites, typically covering tools under five years old and valued under around $10,000 per item. Contractor bonds, required for L&I registration, guarantee contract performance and adherence to codes. General contractors need a $30,000 bond; specialty contractors require $15,000.

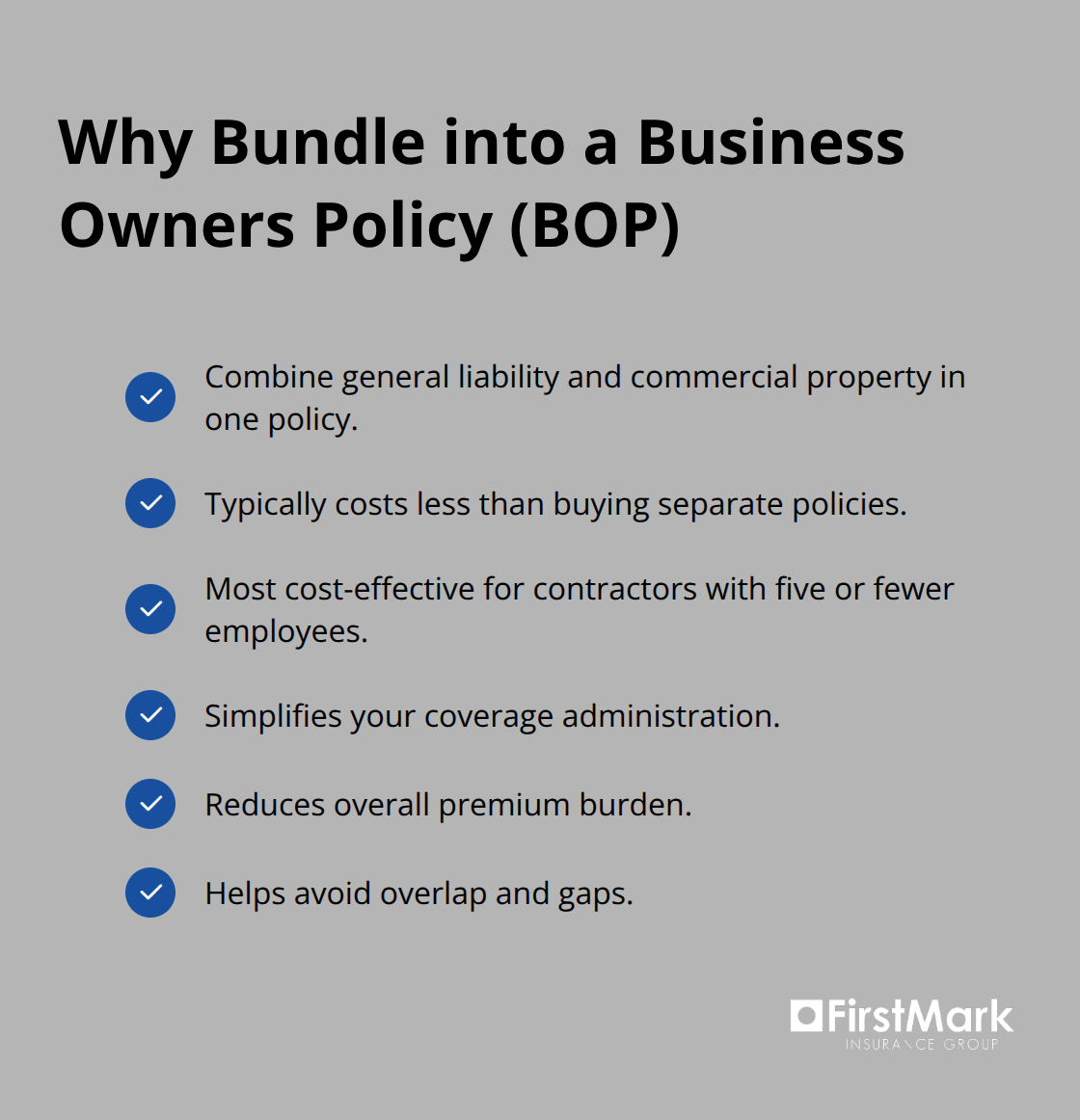

Bundling policies for cost efficiency

Combining general liability with commercial property coverage into a Business Owners Policy typically costs less than purchasing policies separately, making it the most cost-effective approach for contractors with five or fewer employees. This bundled approach simplifies your coverage while reducing your overall premium burden. Understanding which policies work together helps you build a program that protects your operations without unnecessary overlap or gaps.

The specific combination of coverage you need depends on your trade, project scope, and whether you hire subcontractors or employees. Your next step involves assessing your actual risk exposure and comparing how different providers structure their offerings for Washington contractors.

What Washington Contractors Must Know About L&I Registration and Compliance

Meeting L&I Registration Requirements

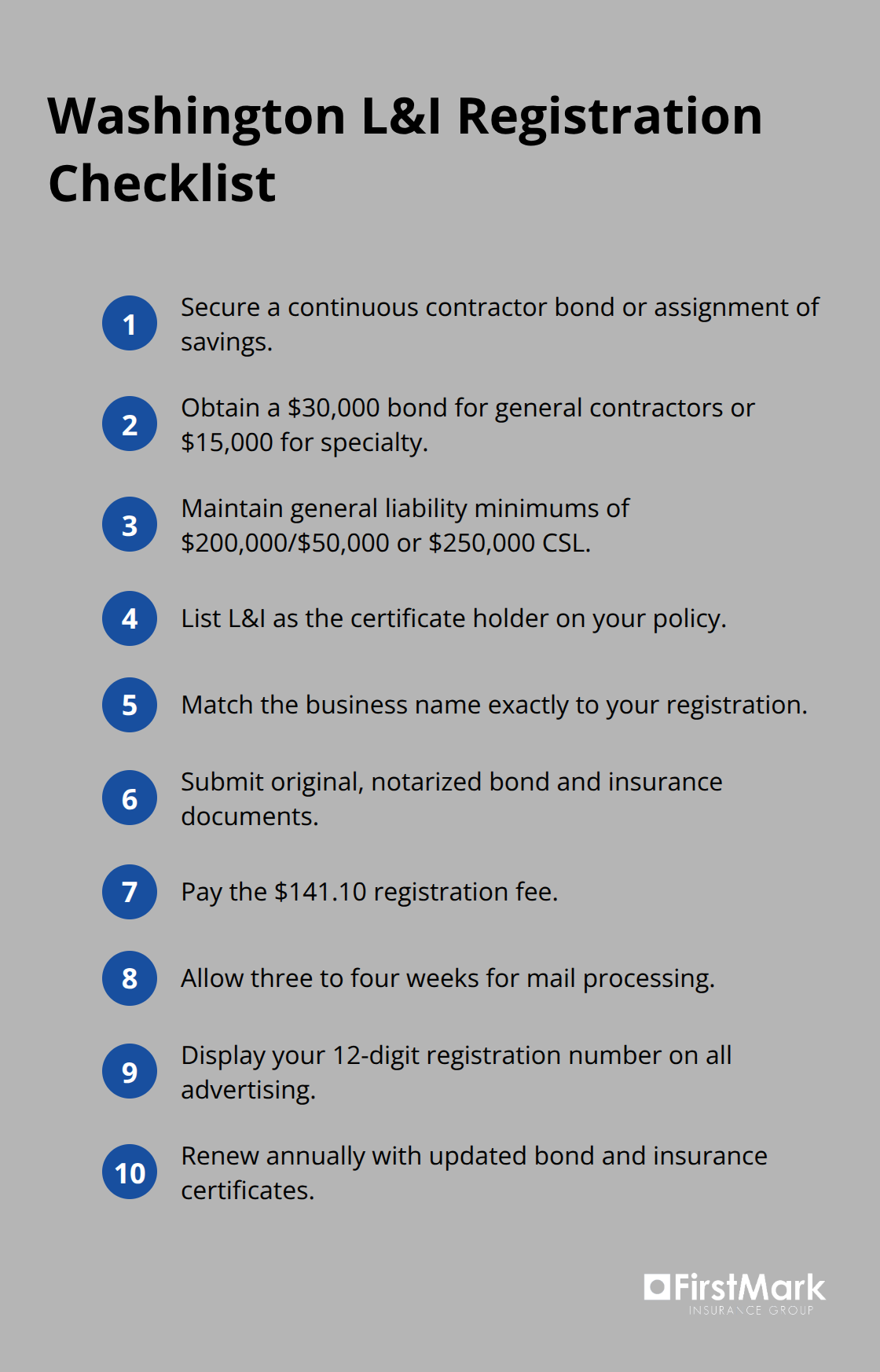

Washington’s Department of Labor & Industries sets strict requirements that contractors cannot ignore without jeopardizing their ability to operate legally. Registration with L&I is mandatory for all contractors, and the process demands more than just filling out a form. You need proof of a continuous contractor bond or an assignment of savings account before you can even apply. General contractors must secure a $30,000 bond; specialty contractors need $15,000. The bond guarantees that you’ll complete work according to contract terms and comply with building codes.

Beyond bonding, L&I requires general liability insurance with a minimum of $200,000 public liability and $50,000 property damage coverage, or $250,000 combined single limit. Your policy must list L&I as the certificate holder, and the business name on your insurance documents must match your registration exactly. Original bond and insurance documents are required-photocopies won’t work, and signatures must be notarized. The registration fee is $141.10, with processing taking three to four weeks for mail submissions.

Displaying Your Registration and Managing Renewals

Once registered, you must display your 12-digit registration number on all advertising and communications. Renewal happens annually with the same $141.10 fee, and you’ll need to submit updated bond and insurance certificates showing at least $250,000 combined single limit coverage. Failing to renew on time or allowing your bond or insurance to lapse will suspend your registration and halt your ability to bid on projects.

Understanding Washington’s Workers Compensation System

Workers compensation in Washington operates differently than most states because it’s a monopolistic state fund. If you have even one employee, you must carry coverage through Washington’s state system-you cannot purchase workers compensation from a private insurer. Sole proprietors with no employees can skip this requirement, but the moment you hire anyone, coverage becomes mandatory. Non-compliance can suspend your L&I registration and jeopardize your contracting license.

Navigating Building Code and Environmental Compliance

Building code compliance ties directly to your insurance and bonding obligations. Washington requires disclosure statements for residential projects valued at $1,000 or more and commercial projects between $1,000 and $60,000. If you’re renovating pre-1978 residential or child-occupied facilities, you must contact the Washington Department of Commerce Lead Paint Program before starting work. Pesticide application requires separate licensing through the Washington Department of Agriculture. These regulatory layers mean your insurance program must align with your specific work scope, and staying current with all requirements protects both your license and your business operations.

Matching Coverage to Your Actual Contracting Work

The Gap Between Minimum Coverage and Real Protection

The gap between minimum legal coverage and adequate protection is where most Washington contractors make costly mistakes. You could meet L&I registration requirements with the bare minimum $250,000 combined single limit general liability and still face significant exposure on a single project. A concrete contractor whose work causes structural damage to an adjacent building, or an electrician whose wiring error leads to a fire months after completion, quickly exhausts basic coverage limits. The real work starts when you honestly assess what your specific trade actually risks.

Understanding Risk Exposure by Trade Type

A roofing contractor faces wind and weather damage claims that a painting contractor never encounters. A general contractor managing multiple subcontractors carries coordination risks that a specialty contractor performing single-trade work avoids entirely. Start by listing every potential claim that could arise from your work-not just during the project, but years afterward through completed operations coverage. Then compare that exposure against what different quotes actually offer in terms of limits, deductibles, and endorsements.

How Premium Costs Reflect Your Actual Risk

According to Insureon, average monthly premiums for Washington general contractors run around $115 for general liability and $163 for commercial auto, but these figures only establish a baseline. Your actual premium depends on your construction type, revenue, claims history, workforce size, and the specific limits you select. A contractor with a clean five-year claims history and smaller projects will pay substantially less than one managing large commercial builds or carrying previous loss experience.

Comparing Quotes Reveals Critical Differences

Comparing multiple quotes reveals how differently insurers structure contractor programs in Washington, and this variation matters enormously. One provider might bundle general liability with commercial property at a significant discount, while another treats them as separate policies with higher combined costs. Request quotes that specify identical coverage limits and deductibles so you can actually compare apples to apples-don’t let quote variations hide in different policy structures or endorsement combinations. Ask each provider explicitly about completed operations coverage duration, professional liability limits if applicable, and whether your contractors bond integrates into the program or requires separate procurement.

Choosing a Provider Who Understands Your Market

Insurance isn’t a commodity product where the lowest premium wins. A cheap policy that excludes your specific risk exposure or carries low limits on completed operations leaves you exposed precisely where you need protection most. The contractor who takes time to assess actual risk, requests detailed quotes addressing that risk, and chooses a provider who understands Washington’s regulatory environment and local market conditions protects both their operations and their growth trajectory.

Final Thoughts

Professional contractors insurance in Washington protects far more than your balance sheet-it protects your ability to operate legally and build a sustainable business. The Department of Labor & Industries sets minimum coverage thresholds for good reason, but honest risk assessment reveals where you actually need stronger limits and additional endorsements. A $250,000 combined single limit satisfies L&I registration, yet it won’t cover a major claim on a significant project, leaving you exposed precisely where protection matters most.

Your next step involves gathering information about your business-your trade type, annual revenue, number of employees, and typical project scope-then requesting detailed quotes from multiple providers. Specify identical coverage limits across all quotes so you can compare how different insurers structure their professional contractors insurance Washington programs. Ask about completed operations duration, professional liability limits if applicable, and how contractor bonds integrate into the overall program, ensuring transparent comparison reveals which provider offers genuine protection at fair pricing.

We at FirstMark Insurance Group work with Washington contractors to build coverage that matches your actual risk exposure. Contact us to discuss your professional contractors insurance needs and secure the protection your business deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation