A million dollar business insurance policy isn’t a luxury-it’s a necessity for companies with real assets and real exposure to liability claims. Most business owners underestimate how quickly a single lawsuit or property loss can exceed standard coverage limits.

We at FirstMark Insurance Group help businesses understand exactly what protection they need and what gaps exist in their current policies. This guide walks you through the coverage types, who actually needs this level of protection, and how to select the right limits for your operation.

What Million Dollar Policies Actually Cover

The Three Core Coverage Types

A million dollar business insurance policy isn’t one monolithic product-it’s a combination of distinct coverage types working together to protect different aspects of your operation. General liability forms the foundation, covering bodily injury and property damage claims that arise from your normal business activities, plus any associated legal fees, judgments and settlements. If a client slips in your office and sues for $800,000 in medical bills and lost wages, general liability pays those costs up to your policy limit, plus legal defense expenses that don’t count against that limit.

Property coverage protects the physical assets that make your business run-buildings, equipment, inventory, and improvements you’ve made to leased spaces. For a manufacturing operation with $1.2 million in machinery or a retail location with $900,000 in inventory, property insurance replaces these items at replacement cost rather than depreciated value, which matters enormously when you rebuild after a fire or weather event. Professional liability and errors and omissions coverage protects service-based businesses where mistakes have financial consequences. A consultant who provides incorrect advice costing a client $750,000 in lost revenue, an accountant whose tax error creates a $600,000 liability, or an IT firm whose security oversight leads to a breach-these scenarios require E&O coverage because general liability explicitly excludes professional errors.

How These Coverages Work Together

The interaction between these three coverage types is where million dollar protection becomes genuinely valuable. A restaurant fire triggers property coverage for the building and equipment damage, general liability for injuries to customers caught in the evacuation, and business interruption coverage for lost revenue during reconstruction. Real claims data shows the need for layered protection: the average slip-and-fall settlement exceeds $1.2 million when serious injuries occur, property damage from equipment failures or environmental incidents regularly reaches $2.3 million, and professional liability claims in high-value industries average $1.4 million across multiple incidents.

Matching Coverage to Your Industry

Your industry classification heavily influences which coverages matter most and how much protection you actually need. Construction operations face different exposures than consulting firms, and a restaurant’s risk profile differs entirely from a software company’s. The million dollar threshold works well for businesses with substantial assets, multiple employees, and significant revenue exposure, but the right combination of general liability, property, and professional liability must match your specific operation.

Finding the Right Balance for Your Business

Paying for coverage you don’t need wastes money; ignoring coverage you do need creates catastrophic gaps. This is why comparing quotes from multiple carriers and working with an agent to customize your specific protection matters far more than simply buying the highest limits available. Your next step involves assessing your actual risk exposure and understanding which coverage types address your most significant liabilities.

Who Actually Needs Million Dollar Coverage

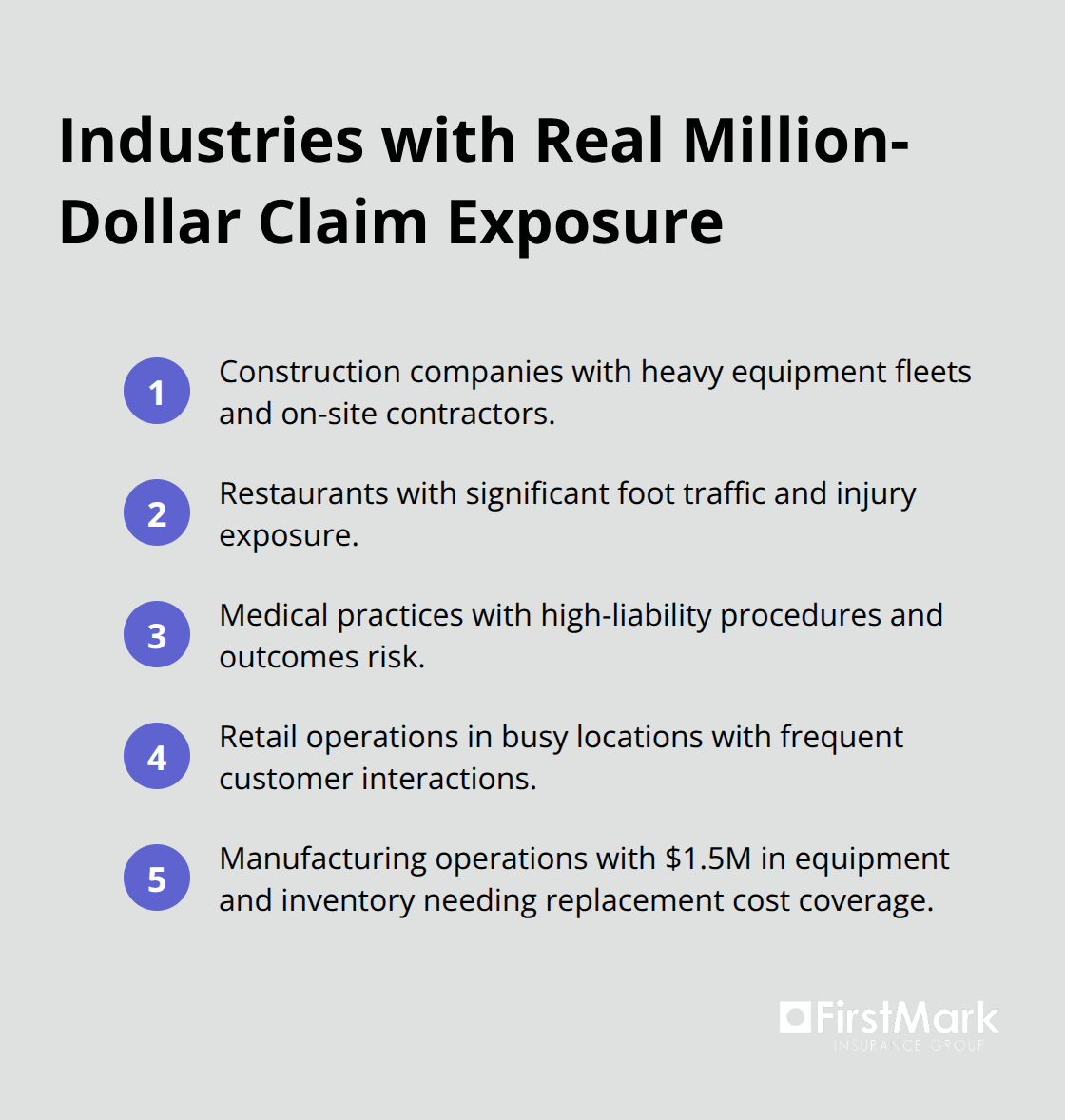

Industries with Genuine Million-Dollar Claim Risk

Construction companies with heavy equipment fleets, restaurants with significant foot traffic, medical practices with high-liability exposure, and retail operations in busy locations face real million-dollar claim risk. A single serious injury lawsuit in a high-traffic restaurant settles for amounts ranging from $10,000 to $50,000 for moderate cases, with severe cases involving hospitalization commanding significantly higher settlements. Construction sites with multiple employees operating expensive machinery create exposure that regularly exceeds standard $1 million limits, especially when third-party contractors work on-site. Manufacturing operations housing $1.5 million in equipment and inventory need property coverage that matches replacement costs, not depreciated values.

Professional Service Firms and Liability Exposure

Professional service firms including accountants, consultants, IT security providers, and medical professionals operate in a different risk category entirely. An accountant’s tax error costs a client $600,000 in penalties. A consultant provides flawed strategic advice that costs a client $750,000 in revenue. An IT firm’s security failure leads to a $1.4 million breach. These aren’t worst-case scenarios-they represent documented claim patterns that demand professional liability coverage with adequate limits.

How Revenue Size and Employee Count Drive Exposure

Your revenue size and employee count directly correlate with claim frequency and severity. Businesses generating $5 million to $25 million in annual revenue typically carry substantially higher exposure than smaller operations because they handle more client relationships, larger contracts, and more complex operations. A company with 50 employees faces dramatically different third-party injury risk than a five-person operation. Multi-location businesses compound exposure exponentially-each location represents a separate opportunity for property damage, customer injuries, or operational disruptions.

The Underinsurance Crisis Among Small Businesses

About 29 to 35 percent of small businesses with 1 to 50 employees carry no general liability coverage at all, according to data from NEXT Insurance and Hiscox. This underinsurance crisis leaves thousands of operations vulnerable to catastrophic losses. Most businesses that examine their risk exposure-their total assets, their annual revenue, their employee count, their claims history-discover that standard $1 million general liability limits leave dangerous gaps. A single catastrophic event doesn’t care whether you thought you needed higher limits.

Conducting Your Risk Assessment

Any business with substantial assets, multiple employees, significant revenue, or operation in a higher-risk industry should complete a formal risk assessment before settling on coverage limits. This assessment identifies your actual exposures, your most likely claim scenarios, and the specific coverage types that protect your operation. Your industry classification code, annual payroll, property values, and claims history all feed into determining whether million-dollar limits represent adequate protection or unnecessary expense for your specific situation. Once you understand your true exposure level, the next step involves selecting the right policy structure and comparing options across multiple carriers to find the coverage that matches both your needs and your budget.

How to Select the Right Coverage Limits for Your Operation

Document Your Assets and Calculate Replacement Costs

Start with what you actually own and what you actually do. Pull your last three years of tax returns to confirm your annual revenue figure, then list every asset your business depends on: buildings, equipment, inventory, vehicles, technology systems. Calculate replacement costs for these assets at current 2026 prices, not what you paid five years ago. Construction and labor costs continue rising through 2025, so a $500,000 piece of machinery today might cost $575,000 to replace.

Identify Your Highest-Risk Operational Areas

Next, identify where your business faces the greatest exposure. A restaurant owner should analyze foot traffic volume and injury patterns; a construction firm should map equipment hazards and third-party contractor exposure; a professional services firm should review past client disputes and potential claim scenarios. This isn’t theoretical work. A manufacturing operation with $1.2 million in machinery absolutely needs property coverage matching that replacement cost. A consultant handling million-dollar client contracts needs professional liability limits reflecting those contract values. A retail location in a high-traffic area needs general liability covering realistic injury settlement amounts, which average approximately $55,056 based on documented cases.

Request Quotes from Multiple Carriers Using Identical Parameters

Once you understand your exposures, obtain quotes from at least three carriers using identical coverage parameters. This matters because premiums for the same $1 million general liability policy vary dramatically across insurers. Chubb, Hiscox, Travelers, Next Insurance, and The Hartford all serve small and mid-sized businesses, but their pricing and coverage terms differ based on their risk appetite and underwriting criteria. Request quotes for your base coverage (general liability at $1 million per occurrence/$2 million aggregate, property coverage at your replacement cost value, and professional liability if applicable), then request quotes adding higher limits to see how costs scale. A $2 million per occurrence/$4 million aggregate general liability policy typically costs roughly $550 annually versus $504 for the $1 million version, so the cost difference for doubling protection often surprises business owners.

Compare Policy Language and Coverage Terms Across Carriers

Compare specific policy language, not just price. Some carriers exclude certain industry-specific risks that others cover. Some offer better legal defense cost provisions where defense expenses don’t count against your limit. Some provide superior endorsement options for specialized equipment or business interruption coverage. After narrowing to two or three carriers, contact a licensed agent who can explain exclusions, verify coverage applies to your specific operations, and identify any gaps between what you think you’re covered for and what the policy actually covers.

Work with an Agent to Determine Your Optimal Policy Structure

An agent also helps determine whether bundling general liability with property coverage into a Business Owners Policy saves money (typically 10 to 15 percent versus separate policies) or whether your operation needs a Commercial Package Policy with additional endorsements. This consultation costs nothing and prevents catastrophic coverage mistakes far more expensive than any premium difference between carriers.

Final Thoughts

Selecting adequate coverage limits for your business comes down to three concrete factors: your total asset value, your annual revenue, and your industry’s inherent risk profile. A $1 million business insurance policy works well for operations with substantial exposure, but only if the specific coverage types match your actual liabilities. A construction firm with $1.5 million in equipment needs property limits reflecting that replacement cost, while a professional services firm handling seven-figure client contracts needs professional liability matching those contract values.

Your coverage needs shift as your business evolves. Construction and labor costs continue rising, which means replacement costs for your property increase annually. Your business grows, adding employees and locations that expand your exposure, and your claims history changes over time. This is why you should review your policy at least annually rather than assuming yesterday’s protection covers today’s risks.

We at FirstMark Insurance Group work with top insurance providers to present you with coverage options that fit your specific needs at the best available pricing. Document your assets and replacement costs, identify your highest-risk operational areas, and contact us to request quotes from multiple carriers using identical parameters.