Construction projects in Washington face unique risks that standard property insurance won’t cover. Builders risk insurance WA protects your investment from weather damage, theft, and other losses that occur during the building process.

At FirstMark Insurance Group, we’ve seen how the right coverage prevents financial setbacks that can derail projects. This guide walks you through what you need to know to protect your construction venture.

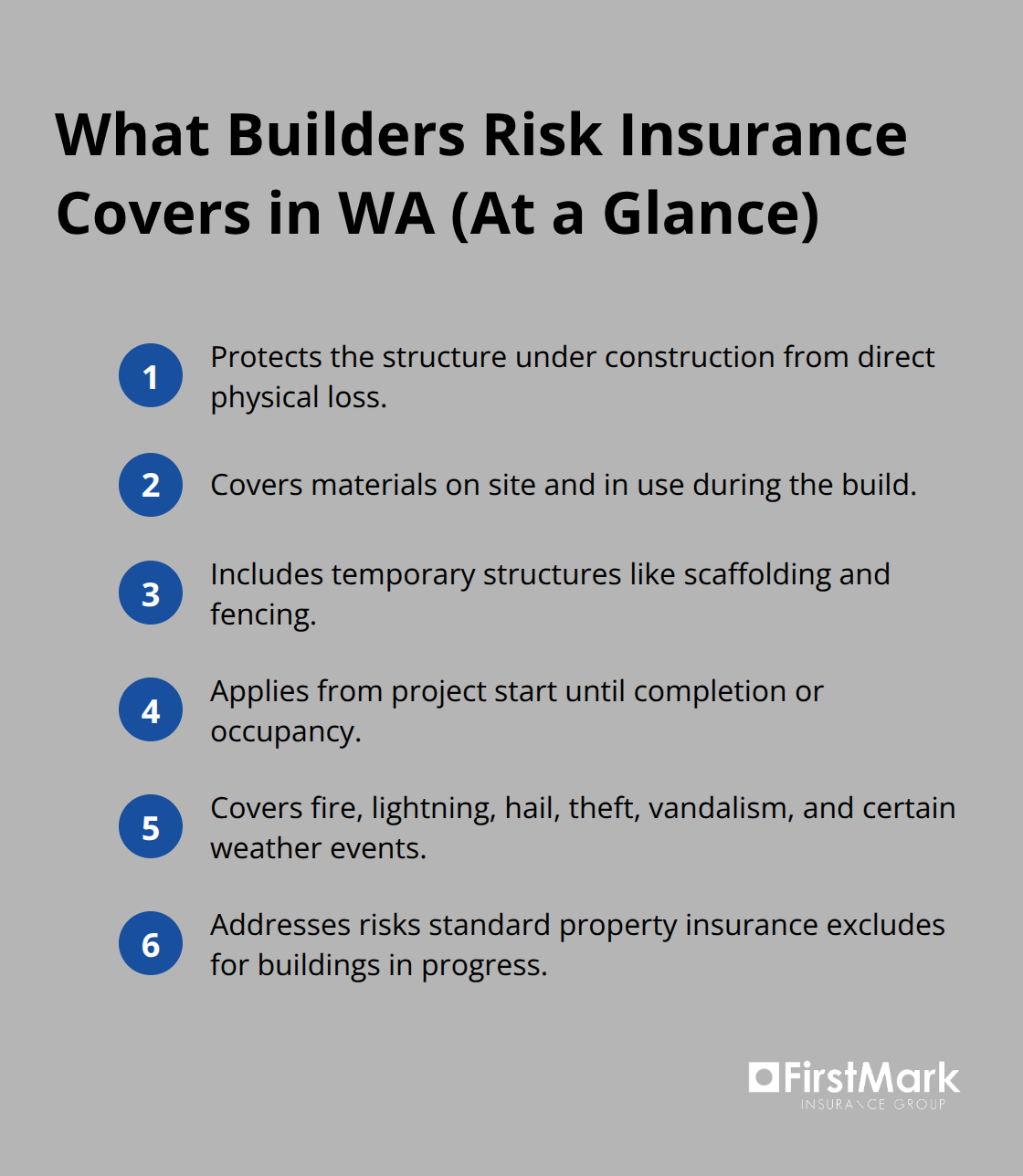

What Builders Risk Insurance Actually Covers

Builders risk insurance protects the physical structure under construction, materials on site, and temporary structures like scaffolding and fencing from direct physical loss. This coverage applies from the moment construction begins until the project reaches completion or occupancy. The policy covers damage from fire, lightning, hail, theft, vandalism, and weather events-perils that standard property insurance excludes for buildings still in progress. In Washington, where winter storms and wildfire risk are persistent concerns, this distinction matters significantly.

What the Policy Actually Includes

The coverage extends to materials and supplies in transit to the job site, construction plans and blueprints stored on location, and valuable papers related to the project. If your project includes expensive permanently installed systems or machinery, equipment breakdown coverage can be added as an endorsement to protect those assets during the construction phase. Most builders risk policies operate on an all-risk or open-peril basis, meaning coverage applies to any direct physical loss unless specifically excluded in the policy language.

What Stays Excluded

Common exclusions include wear and tear, faulty workmanship, earthquakes, and floods-perils that typically require separate endorsements or policies. The policy also covers soft costs when construction delays occur, including additional loan interest, lost rental income, and real estate taxes that continue accumulating while the project sits idle.

Soft Costs Add Up Faster Than You Expect

Debris removal costs can represent a significant portion of loss recovery, making adequate coverage for this exposure non-negotiable. When a covered loss delays your project, soft cost coverage reimburses expenses that continue regardless of construction progress. If your project is financed, lender requirements typically mandate builders risk coverage with specific limits tied to the total construction cost.

Washington contractors often underestimate how quickly soft costs accumulate; a single weather delay of 30 days on a $2 million project can generate $15,000 to $25,000 in additional financing costs alone. Your policy limits should reflect the full construction value plus a reasonable cushion for soft costs, not just the hard construction expenses. Coinsurance clauses in builders risk policies penalize underinsurance, so conservative valuation protects you from bearing unexpected loss costs yourself.

Protecting All Parties Involved

The policy should clearly identify all interested parties-the property owner, general contractor, subcontractors, lenders, and any design professionals-as additional insureds to prevent coverage gaps. This step matters because it establishes who holds protection if a loss occurs, and it clarifies responsibilities across your entire project team. Understanding these coverage details positions you to evaluate whether your current policy aligns with your project’s actual exposures and financial requirements.

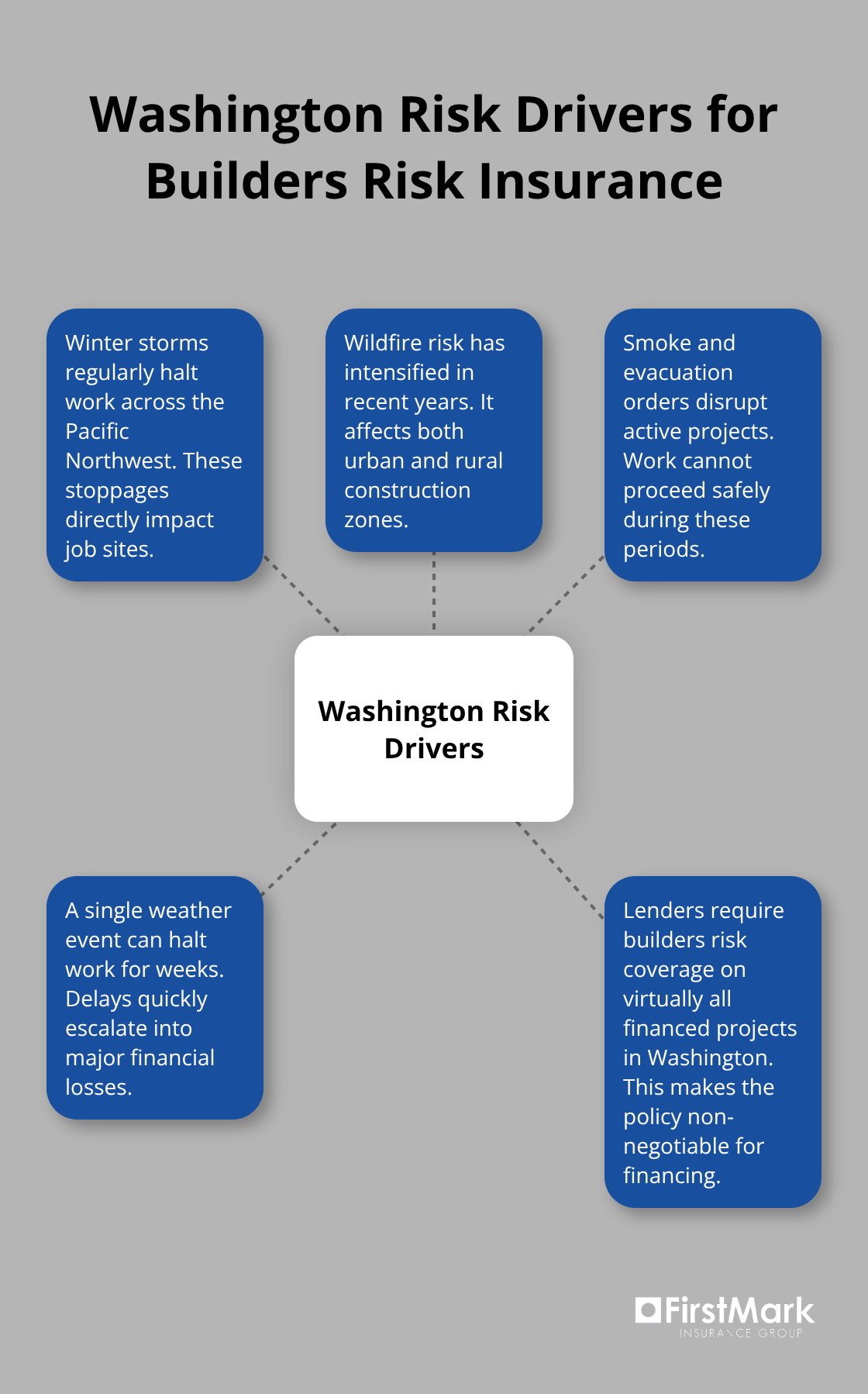

Why Washington Builders Need This Coverage Now

Washington’s construction environment demands builders risk insurance for reasons that go far beyond standard property protection. The state experiences persistent weather threats that directly impact job sites: winter storms regularly halt work across the Pacific Northwest, and wildfire risk has intensified significantly in recent years, affecting both urban and rural construction zones. According to the National Interagency Fire Center, Washington experienced wildfires in recent years, with smoke and evacuation orders disrupting active projects.

A single weather event can halt work for weeks, transforming what seemed like manageable delays into substantial financial hemorrhages. Lenders recognize these realities and now require builders risk coverage on virtually all financed projects in Washington, making the policy a non-negotiable component of project financing rather than an optional protection layer.

Construction Delays Cost More Than Weather Damage

When construction stops, expenses don’t. A project worth $2 million financed at current rates can accumulate $15,000 to $25,000 in additional financing costs during a 30-day weather delay alone. This calculation excludes real estate taxes, permit extension fees, and lost rental income if the property was intended to generate revenue. Builders who underestimate soft cost exposure frequently discover mid-project that their coverage falls short of actual expenses. Your builders risk policy should include soft cost coverage that reflects not just hard construction expenses but the full financial exposure of project interruption. Washington’s competitive construction market means delays translate directly into margin erosion; projects that slip schedules often face subcontractor availability issues and material price increases that compound the original delay’s cost.

Legal and Contractual Realities Shape Coverage Requirements

Washington state law RCW 48.30.270 prohibits public construction bidders from being forced to use a specific insurer for builders risk coverage, protecting competitive fairness in public works. However, this protection doesn’t eliminate the requirement for coverage itself; it simply means you retain the freedom to select your insurer. Private projects and lender requirements typically impose specific coverage minimums tied to total construction cost, with many lenders demanding limits at 100 percent of the project value plus soft costs. The coinsurance clause standard in builders risk policies penalizes underinsurance aggressively, meaning if you report a $2 million project value but it actually costs $2.5 million, the insurer can reduce claim payments proportionally. Contractors who fail to account for this provision often discover during claims that they’re bearing significant loss costs themselves.

How Underinsurance Creates Hidden Exposure

Underreporting your project value creates a dangerous gap between what you think you’re protected for and what you actually recover. The coinsurance penalty applies to all losses, not just catastrophic ones, so even a moderate claim can result in substantial out-of-pocket costs if your reported value falls short. Conservative valuation protects you from this exposure; list your total construction cost plus a reasonable cushion for soft costs, not just the hard construction expenses. Many contractors overlook this detail until a loss occurs, at which point the financial impact becomes unavoidable. Your policy limits should reflect the full financial exposure of your project, including all costs that continue if work halts.

Selecting Coverage That Matches Your Project Reality

Understanding your contract obligations and lender requirements before purchasing coverage prevents expensive gaps at the moment you need protection most. Work with an insurance professional who can assess your specific project exposures, timeline, location, and financing structure to recommend appropriate limits and endorsements. The right coverage aligns with your actual financial exposure, not just the construction contract value, and accounts for the unique risks that Washington’s environment presents to active job sites.

Common Claims and How to Avoid Them

Weather stops work on Washington job sites regularly, and when it does, the financial damage extends far beyond the immediate weather event itself. Winter storms, heavy rain, and wind events cause direct physical damage to structures and materials, but the real cost emerges in project delays and the soft costs that accumulate while work halts. A roofing contractor experienced a three-week weather delay on a Seattle-area project; the direct storm damage to temporary structures totaled $18,000, but the delay itself cost an additional $22,000 in extended financing, permit fees, and subcontractor schedule adjustments.

Weather-Related Damage and Soft Cost Exposure

Your builders risk policy must include soft cost coverage that reflects realistic delay scenarios for your specific project location. Washington’s winter weather window from November through March creates concentrated risk periods when major delays become statistically likely rather than merely possible. Document your project timeline conservatively and try to ensure your soft cost limits account for delays of at least 30 to 60 days, depending on seasonal construction windows. This isn’t theoretical protection; it’s the difference between absorbing a manageable insurance deductible and facing tens of thousands in uninsured expenses.

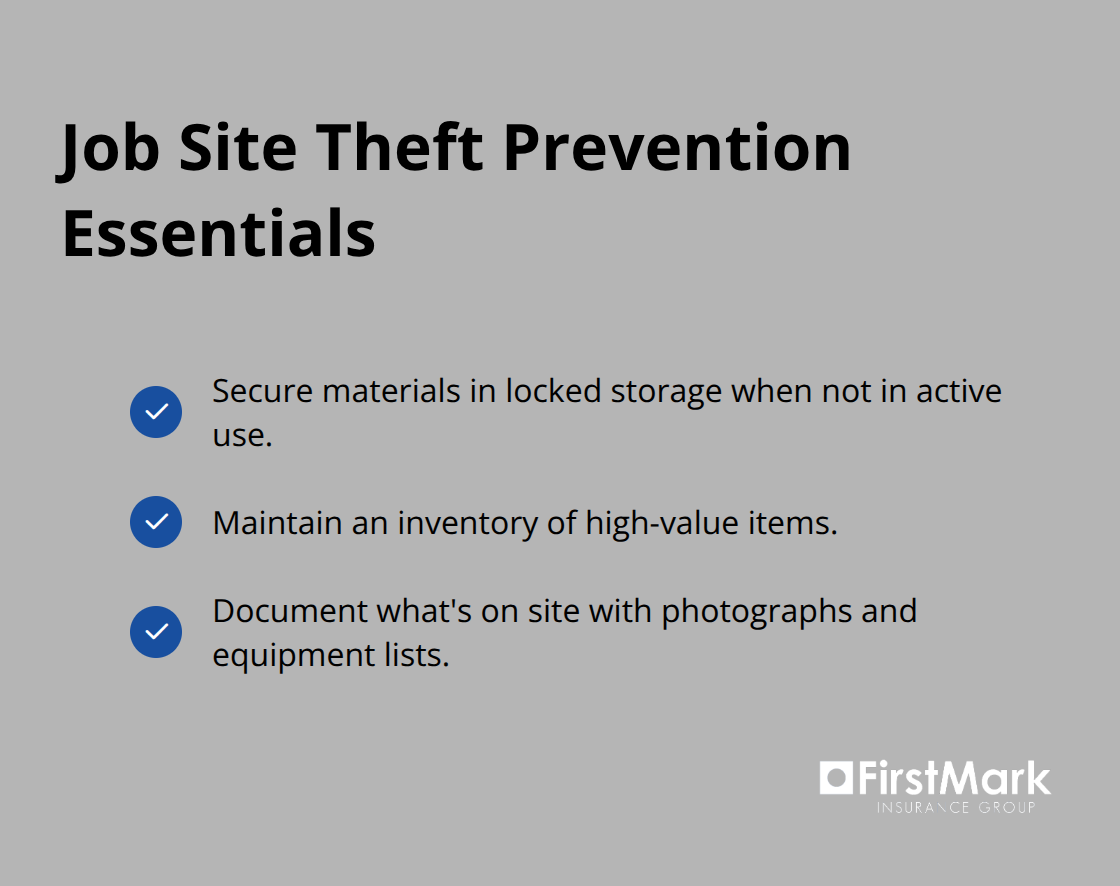

Theft on Job Sites and Material Loss

Theft and material loss on active job sites represents a persistent and often underestimated exposure that claims data confirms repeatedly. The Construction Industry Safety Coalition reports that construction theft costs the industry billions annually, with job site theft incidents increasing in urban areas across the Pacific Northwest. Copper wire, electrical components, tools, and finished materials disappear from unsecured sites with regularity, and the replacement cost often exceeds the original material expense due to project delays and expedited procurement fees.

Your builders risk policy covers theft of materials and supplies on site, but the coverage works effectively only when you implement basic site security practices that reduce claim frequency and demonstrate reasonable loss prevention efforts. Secure materials in locked storage when not in active use, maintain an inventory of high-value items, and document what’s on site through photographs and equipment lists. Contractors who experience multiple theft claims often find that insurers increase premiums or reduce coverage limits on future policies, making loss prevention economically essential beyond just the immediate claim.

Contractor Negligence and Workmanship Issues

Workmanship issues and contractor negligence create a different category of claims exposure that builders risk policies explicitly exclude. Faulty installation, design errors, and work that fails to meet code requirements fall outside builders risk coverage because the policy covers direct physical loss from external perils, not losses resulting from how work was performed. A concrete contractor who poured a foundation with insufficient reinforcement discovered mid-project that the structural deficiency required complete removal and replacement; the builders risk policy provided no coverage because the loss resulted from the contractor’s negligence rather than an external peril.

This exposure requires separate professional liability or errors and omissions coverage, not builders risk insurance. The distinction matters because contractors who confuse these coverage types often discover mid-claim that their builders risk policy won’t cover losses they assumed were protected. Maintain quality control processes that catch errors before they become costly structural problems, and ensure that your subcontractors carry appropriate liability coverage for their specific work.

Final Thoughts

Builders risk insurance WA protects your construction investment from the specific threats that Washington’s environment presents. Weather delays halt work for weeks, theft strikes active job sites, and soft costs accumulate relentlessly while projects sit idle-standard property insurance ignores all three exposures. Contractors who carry appropriate builders risk coverage avoid the financial setbacks that derail timelines and erode margins.

Calculate your total construction cost conservatively, including hard expenses plus a realistic cushion for soft costs if delays occur. Identify all parties who need protection as additional insureds: your lender, general contractor, subcontractors, and design professionals involved in the project. Verify that your policy limits align with your contract obligations and lender requirements, accounting for the coinsurance clause that penalizes underinsurance-many contractors discover mid-claim that their coverage falls short of actual expenses.

Working with an insurance professional who understands Washington’s construction environment transforms this process from a compliance checkbox into genuine risk management. At FirstMark Insurance Group, we assess your actual exposures, timeline, location, and financing structure to recommend limits and endorsements that protect your investment appropriately. Contact FirstMark Insurance Group to discuss your builders risk insurance needs and secure coverage that reflects your project’s true financial exposure.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation