Construction projects in Washington face unique risks that standard property policies simply don’t address. We at FirstMark Insurance Group see builders regularly discover gaps in their coverage only after losses occur-a costly mistake.

Your Washington builders risk coverage needs regular evaluation as projects evolve and material costs shift. The difference between adequate protection and financial exposure often comes down to policy details most builders overlook.

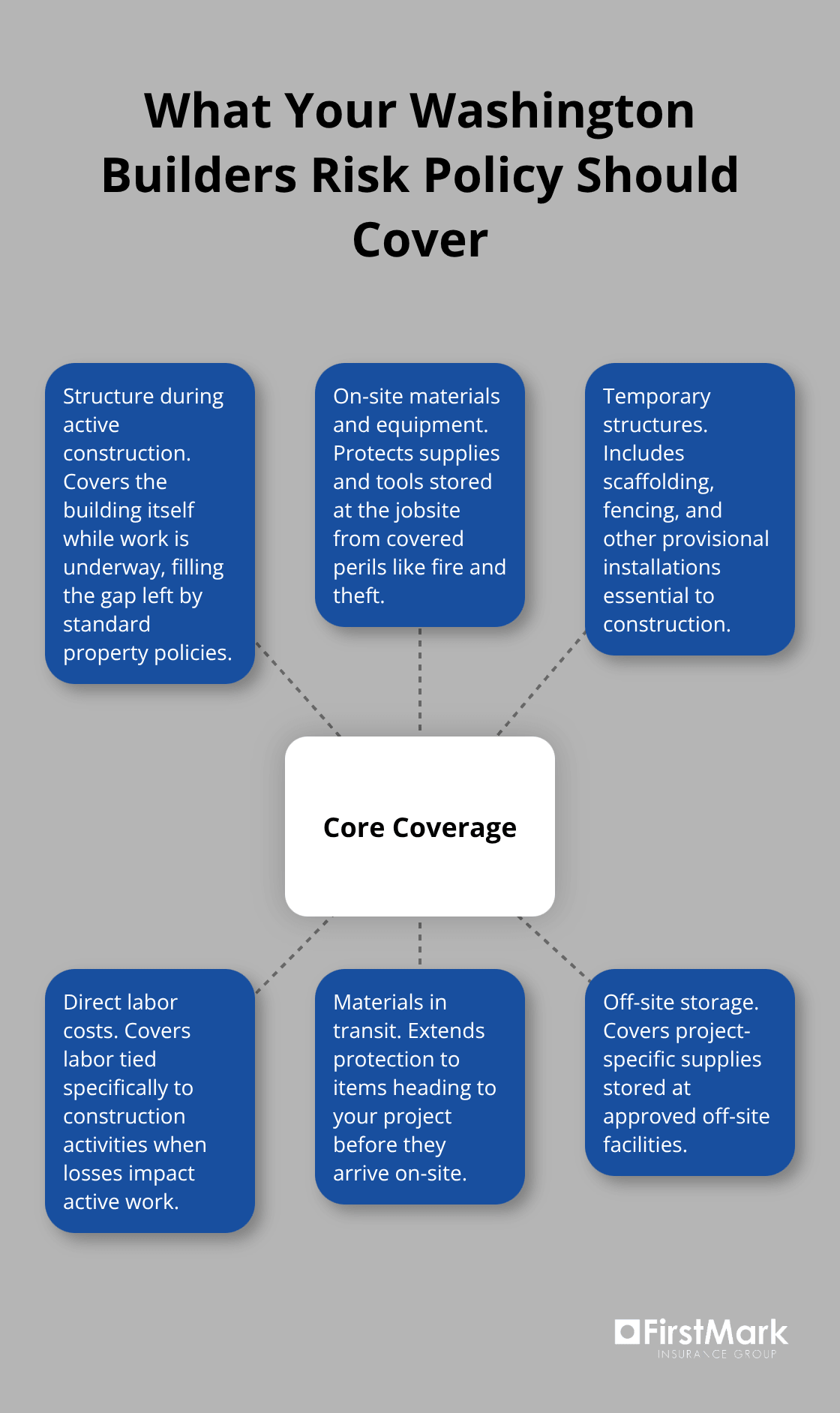

What Your Builders Risk Policy Actually Protects

Builders risk coverage in Washington addresses three categories of loss that standard property insurance ignores completely: active construction exposure, temporary site conditions, and materials before integration into the structure. Understanding exactly what your policy covers separates smart risk management from expensive surprises. Your policy should cover the building structure itself during active construction, all materials and equipment stored on-site, temporary structures like scaffolding and fencing, and labor costs tied directly to construction activities. Coverage extends to materials heading to your project and off-site storage facilities holding project-specific supplies.

This breadth matters because a single theft or weather event can wipe out weeks of material procurement and delay your timeline significantly.

Fire and Weather Losses Hit Hard in Washington

Fire represents one of the largest construction-site perils in our state, yet many builders assume standard coverage applies during active work. Your builders risk policy covers fire damage to the structure, materials, and equipment on-site-protection your general liability policy won’t touch. Western Washington’s weather patterns create additional exposure: 60 mph windstorms regularly damage temporary roofing and unsecured materials, while the region’s heavy rainfall drives water damage and mold growth within 48 hours of exposure. Most policies exclude mold by default, but adding a resultant mold endorsement costs roughly 0.15% to 0.25% of your insured value and prevents catastrophic claims. Earthquake and landslide risk exists throughout Washington; earthquake buybacks typically run 0.25% to 0.40% of insured value and should be non-negotiable for projects in seismic zones. Hail and ice storms compound weather risk, particularly for partially enclosed structures where temporary protection fails under heavy loads.

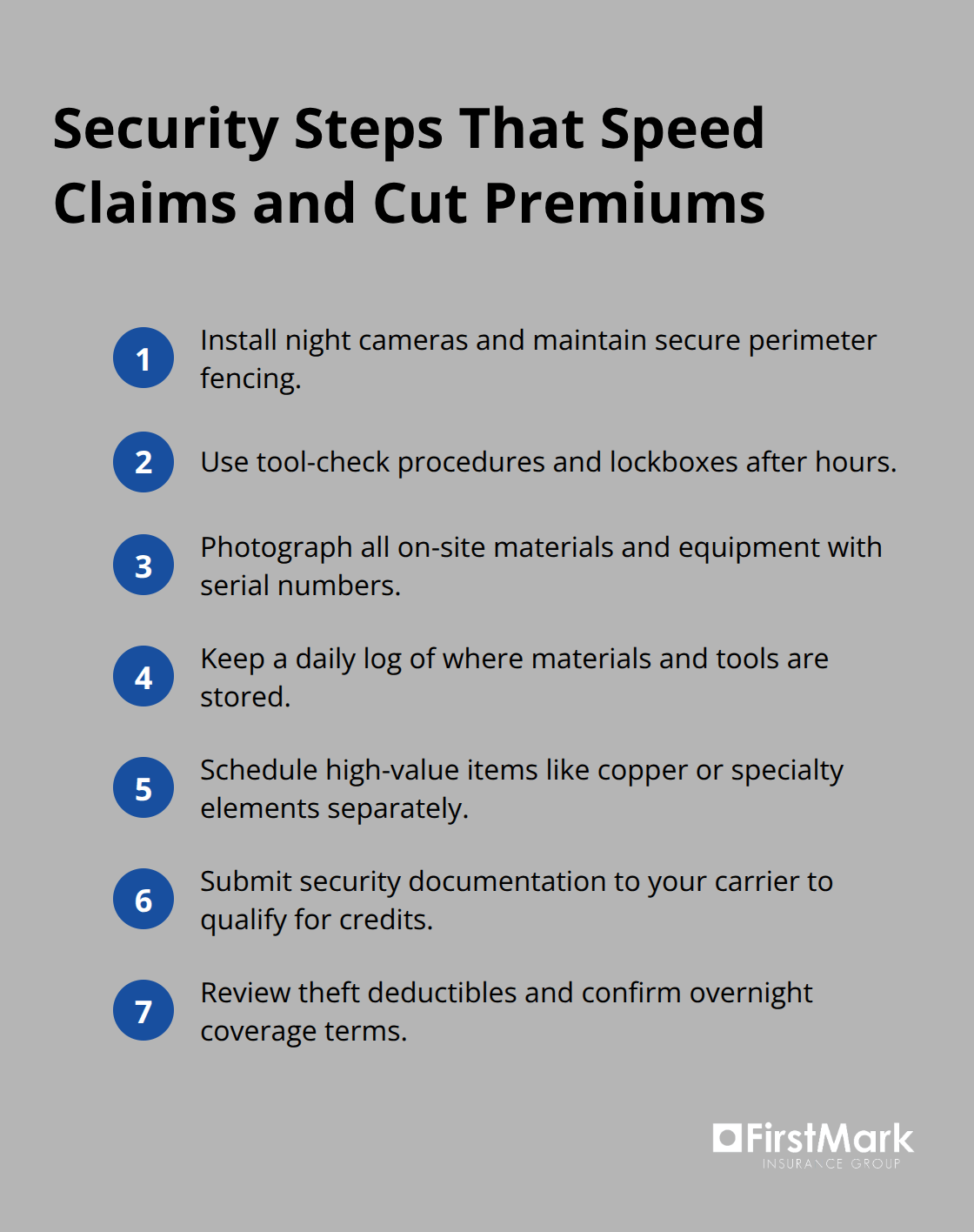

Theft and Security Coverage Requires Precision

Theft and vandalism drive a substantial share of construction claims, yet many policies impose strict limits on high-value materials and equipment unless specifically endorsed. Your coverage should extend to tools, materials, and equipment left on-site overnight, with deductibles typically running $5,000 for theft events. Projects with robust security-night cameras, secure fencing, tool-check procedures-often qualify for premium credits between 5% and 15%, making security investments pay for themselves quickly. Document all on-site materials with photos and serial numbers before losses occur, photograph security measures in place, and maintain a daily log of what’s stored where. This documentation accelerates claims processing and prevents disputes over what was actually on-site when theft or vandalism occurred.

High-value materials like copper, specialized equipment, or architectural elements warrant separate scheduled coverage under your policy to avoid coinsurance penalties.

Coverage Gaps Emerge When You Stop Looking

Most builders think their policy covers everything on-site, but exclusions and limits create real exposure. Equipment exclusions often apply to machinery used for construction purposes rather than materials being constructed into the building. High-value materials face sub-limits that fall short of actual project costs, leaving you responsible for the difference. Your policy’s coverage limits may not reflect current material inflation or scope changes that occurred after binding. These gaps don’t announce themselves-they surface during claims when it’s too late to add protection. Working with an insurance professional who understands Washington construction risks helps identify what your current policy actually covers versus what it leaves exposed.

Where Your Builders Risk Policy Leaves You Exposed

Equipment exclusions in Washington builders risk policies create the first major gap most contractors encounter. Insurers distinguish sharply between machinery used for construction purposes and materials that become part of the finished structure. A concrete mixer, scaffolding system, or temporary power generator typically falls outside coverage because these items serve the construction process rather than the building itself. When a $15,000 compressor gets stolen or damaged, your policy won’t cover it. Equipment used in fire prevention or site operations often carries exclusions.

High-Value Materials and Sub-Limit Traps

High-value materials present a second exposure layer that catches builders off-guard. Copper wiring, specialty architectural elements, and engineered materials frequently hit sub-limits far below their actual cost. A project might carry $5 million in total coverage, but copper components face a $50,000 sub-limit despite representing $200,000 of project value. Theft claims on high-value materials then leave you absorbing the difference out-of-pocket. Coverage terms have tightened across the region in recent years, reducing limits on specialized materials.

Material Inflation and Underinsurance Penalties

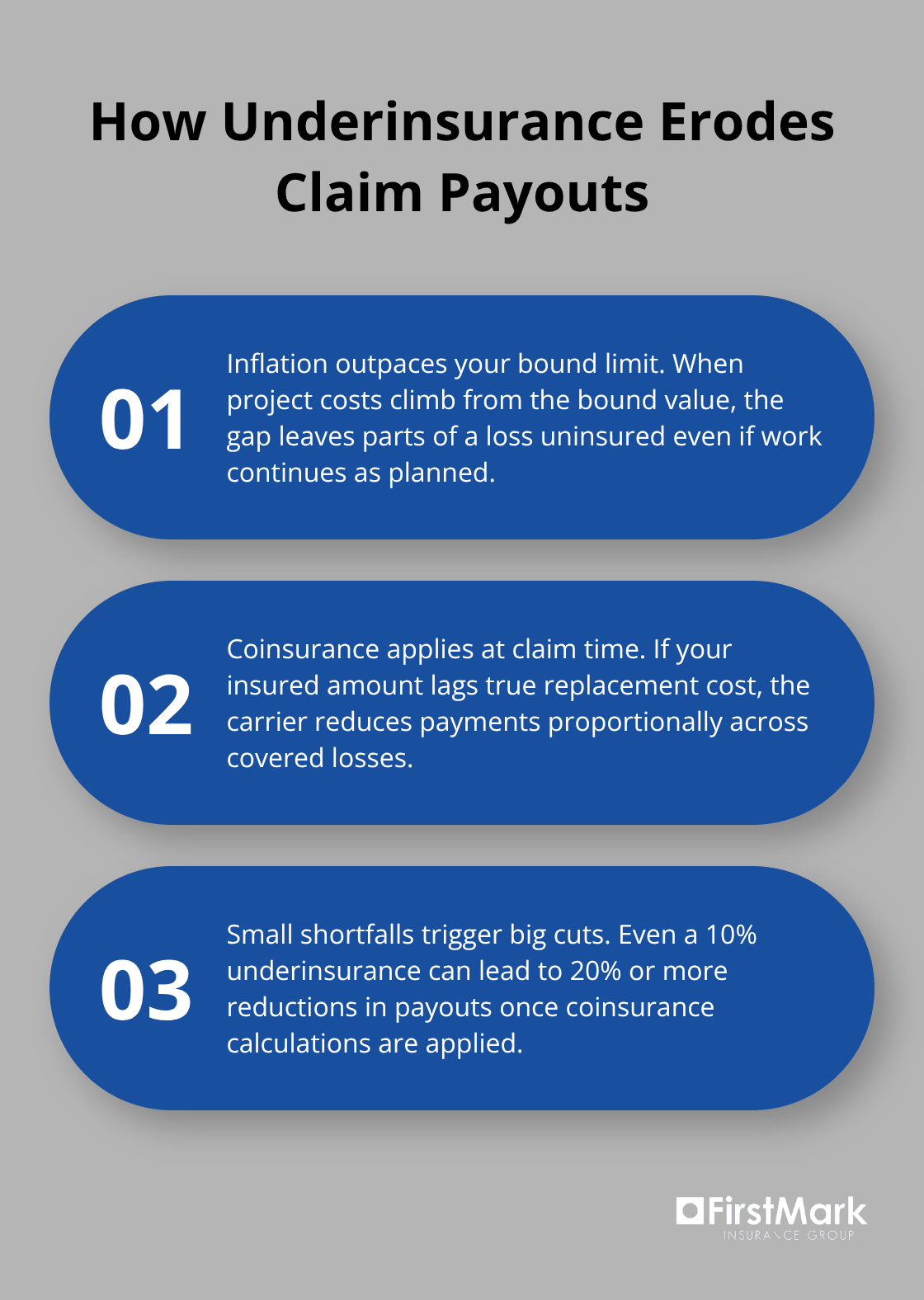

Material inflation since 2023 compounds coverage problems further. Your policy’s coverage limit might have been appropriate when you bound it, but current lumber prices, steel costs, and labor rates have climbed substantially. A $3 million project valued at binding now costs $3.4 million to complete, yet your policy remains at the original limit. Coinsurance penalties then apply at claim time, reducing what the carrier actually pays. Most policies require you to insure at replacement cost in full; underinsuring by even 10% can trigger coinsurance calculations that slash claim payments by 20% or more.

Seismic, Mold, and Soft-Cost Gaps

Projects in seismic zones face additional gaps unless earthquake coverage is explicitly purchased. Earthquake buybacks typically run 0.25% to 0.40% of insured value-a modest cost relative to potential loss, yet many builders skip this endorsement. Your current policy almost certainly excludes mold damage unless you’ve specifically added a resultant mold endorsement, leaving water damage exposure incomplete given Western Washington’s rainfall patterns. Similarly, soft-cost coverage for delays, permit fees, and loan interest often requires separate endorsement. If project delays push your completion date past your loan deadline, those interest costs mount rapidly.

Taking Action Before Groundbreaking

Start with a detailed project inventory: list every material type, equipment category, and high-value item expected on-site, then cross-reference your policy language against that list. Identify which items carry sub-limits and whether those sub-limits match actual costs. Request a completed-value analysis from your agent showing exactly what your insured amount should be under current market conditions, factoring in material inflation since binding. For projects over $5 million, this analysis becomes non-negotiable-underinsurance at that scale creates devastating claim outcomes. Confirm whether your policy includes soft-cost coverage and what specific costs it addresses; if gaps exist, add endorsements covering architectural fees, permit costs, and interest charges. Add earthquake coverage if your project sits in a seismic zone, and purchase mold endorsement if water damage exposure exists. Document your policy’s exact start and end dates, then verify these align with your actual groundbreaking and substantial-completion timelines. Many builders discover mid-project that their coverage ended weeks before actual completion, leaving final phases exposed. Request written confirmation of what equipment and machinery are excluded, then determine whether separate inland marine or equipment coverage makes sense for expensive tools or machinery. Review your policy language line-by-line with your agent at least 30 days before groundbreaking-enough time to add endorsements or adjust limits without delaying your project start.

How to Evaluate and Update Your Current Policy

Start with Your Actual Project Completion Value

Your project’s actual completion value forms the foundation for all coverage decisions, yet most builders rely on outdated figures that no longer reflect current costs. Elevated material and labor costs have rendered many insured property values outdated, prompting valuation disputes and potential coverage gaps. Pull your most recent project estimate and compare it line-by-line against your policy’s insured amount. If your estimate shows $3.2 million in total project cost but your policy covers only $3 million, you’re already underinsured before groundbreaking. The coinsurance penalty for this gap means the carrier reduces claim payments by roughly 6% across the board, turning a $100,000 loss into a $94,000 payment.

For projects exceeding $5 million, request a completed-value analysis from your agent that factors in current material pricing and realistic labor costs. This analysis should become your baseline for determining coverage limits. Washington projects in seismic zones need particular attention since earthquake coverage requires separate purchase; skipping this $15,000 to $25,000 endorsement on a $10 million project creates exposure that a single seismic event could devastate. Similarly, soft-cost coverage for extended loan interest, permit delays, and architectural adjustments rarely comes standard; Seattle’s Master Use Permits averaged $46,000 in processing fees during 2023, yet most builders don’t include permit-delay costs in their coverage calculations.

Identify High-Value Materials and Sub-Limit Exposure

Theft and high-value material sub-limits deserve equal scrutiny during your policy review. Copper components on a commercial project might represent 6% of total value but carry sub-limits covering only 2% of their actual cost, leaving significant exposure if theft occurs. Your agent should provide a written breakdown of which materials face sub-limits and whether those limits match your actual project costs. Request that your agent confirm in writing whether your policy covers labor costs, materials in transit, and off-site storage, since gaps in these areas surface most commonly during actual claims.

Align Coverage with Project Location and Type

Project location and construction type fundamentally shape which endorsements matter most. Western Washington projects face windstorm exposure that justifies 60 mph wind-rated temporary roofing and documented high-wind response plans; carriers often credit premiums 5% to 15% for robust security measures like night cameras and tool-check procedures, so calculating the ROI on security improvements against premium savings makes financial sense. Flood zones require explicit water-damage coverage with resultant mold endorsement since mold begins within 48 hours of moisture exposure and standard policies exclude it entirely. Commercial projects with temporary signage, fencing, or equipment storage face different exposure profiles than residential new construction, yet many builders apply identical coverage templates across different project types.

Schedule a Detailed Policy Review with Your Agent

Schedule a detailed conversation with your agent at least 30 days before groundbreaking where you walk through your specific project-location, timeline, material types, equipment on-site, and parties with financial interest in the project. This conversation should produce a written summary identifying exactly which endorsements apply, which items carry sub-limits, what equipment remains excluded, and whether additional inland marine coverage makes sense for expensive tools or machinery. Verify your policy’s exact start date aligns with when materials actually arrive on-site, not just your contract signing date-binding coverage 30 days before groundbreaking locks in rates while providing buffer time for endorsement adjustments. Document this conversation and your agent’s recommendations, then revisit the policy if project scope changes significantly mid-construction since material additions or timeline extensions may trigger coverage adjustments.

Final Thoughts

Your Washington builders risk coverage demands attention before groundbreaking, not after losses occur. The policy review process-comparing your insured value against current project costs, identifying sub-limit exposure on high-value materials, confirming endorsements for earthquake and mold coverage, and verifying start and end dates-takes a few hours but prevents financial exposure that could exceed six figures on a single claim. Material costs shift, scope expands, timelines slip, and what seemed adequate coverage at binding may leave gaps by mid-construction.

Pull your current builders risk policy, gather your most recent project estimate, and schedule a conversation with an insurance professional who understands Washington construction risks. That conversation should produce a written summary of exactly what your policy covers, which items carry sub-limits, what equipment remains excluded, and whether additional endorsements make sense for your specific project. Binding your coverage 30 days before groundbreaking provides buffer time for adjustments without delaying your start date.

We at FirstMark Insurance Group have guided construction professionals through this process for years, helping them navigate the complexities of Washington builders risk coverage and find protection that actually matches their project exposure. Contact us today to schedule your policy review and align your coverage with your actual project value and risk profile.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation