General liability coverage in Washington protects your business from financial losses due to bodily injuries, property damage, and legal expenses. Without proper coverage, a single incident could threaten your company’s stability.

At FirstMark Insurance Group, we help Washington business owners understand exactly what their policies cover and identify gaps that could leave them exposed. The right limits depend on your industry, operations, and risk profile.

What General Liability Actually Covers

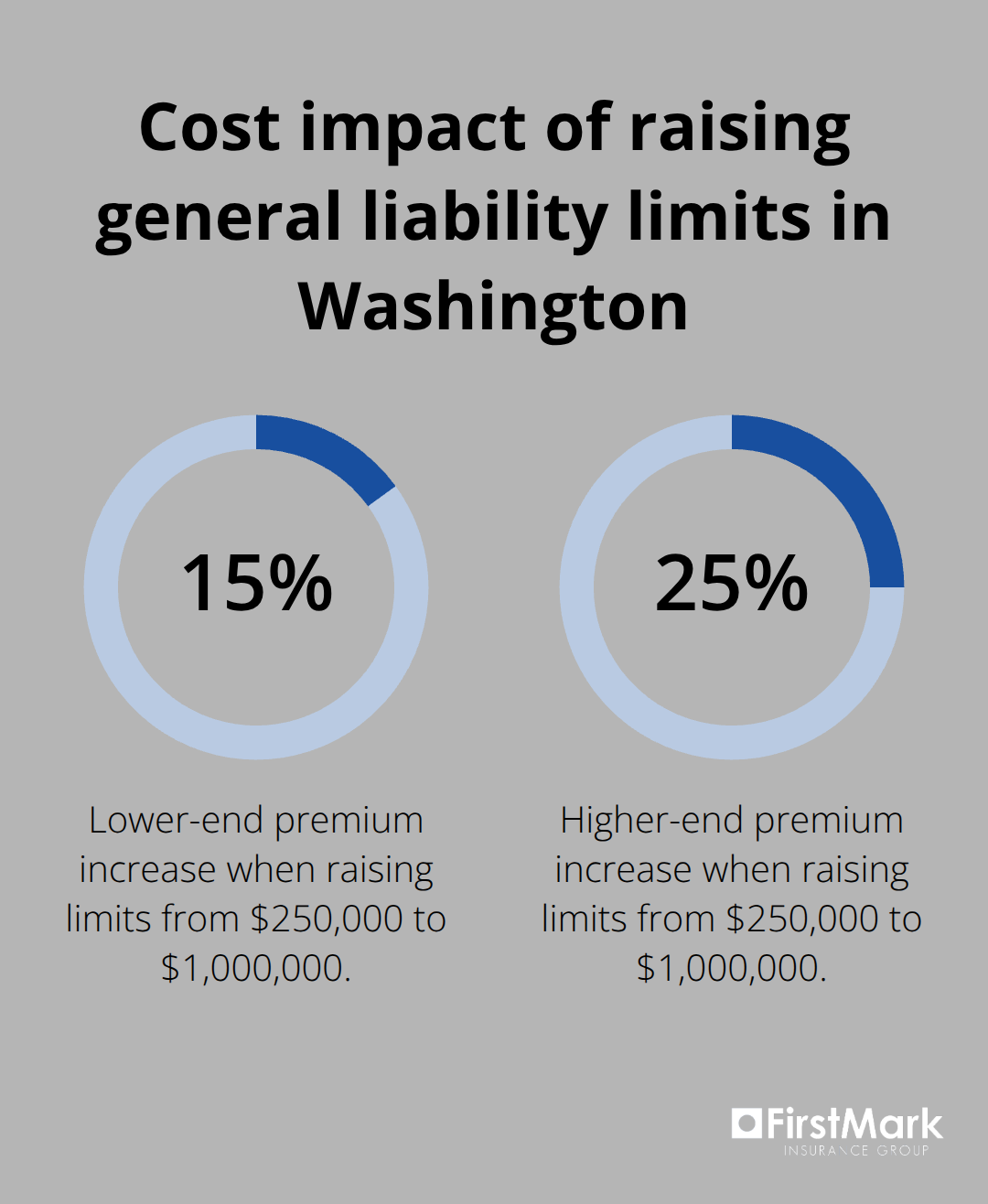

General liability coverage protects your Washington business against three core financial exposures: injuries to third parties on your property or caused by your operations, damage you cause to someone else’s property, and the legal costs to defend yourself when claims arise. When a customer slips on your floor and breaks an arm, or your contractor accidentally damages a client’s kitchen cabinet during installation, general liability steps in to cover medical expenses, repair costs, and attorney fees up to your policy limit. Washington state requires contractors to carry at least $250,000 in coverage per occurrence, but most clients and bid requirements demand $1,000,000 or higher. The difference in premium between $250,000 and $1,000,000 in limits typically runs 15–25%, making the upgrade affordable relative to the actual risk exposure you face. A single serious injury claim can easily exceed $100,000 once medical costs, lost wages, and settlement negotiations conclude, which is why underinsuring creates real financial jeopardy for your business assets.

How Medical Payments Coverage Works

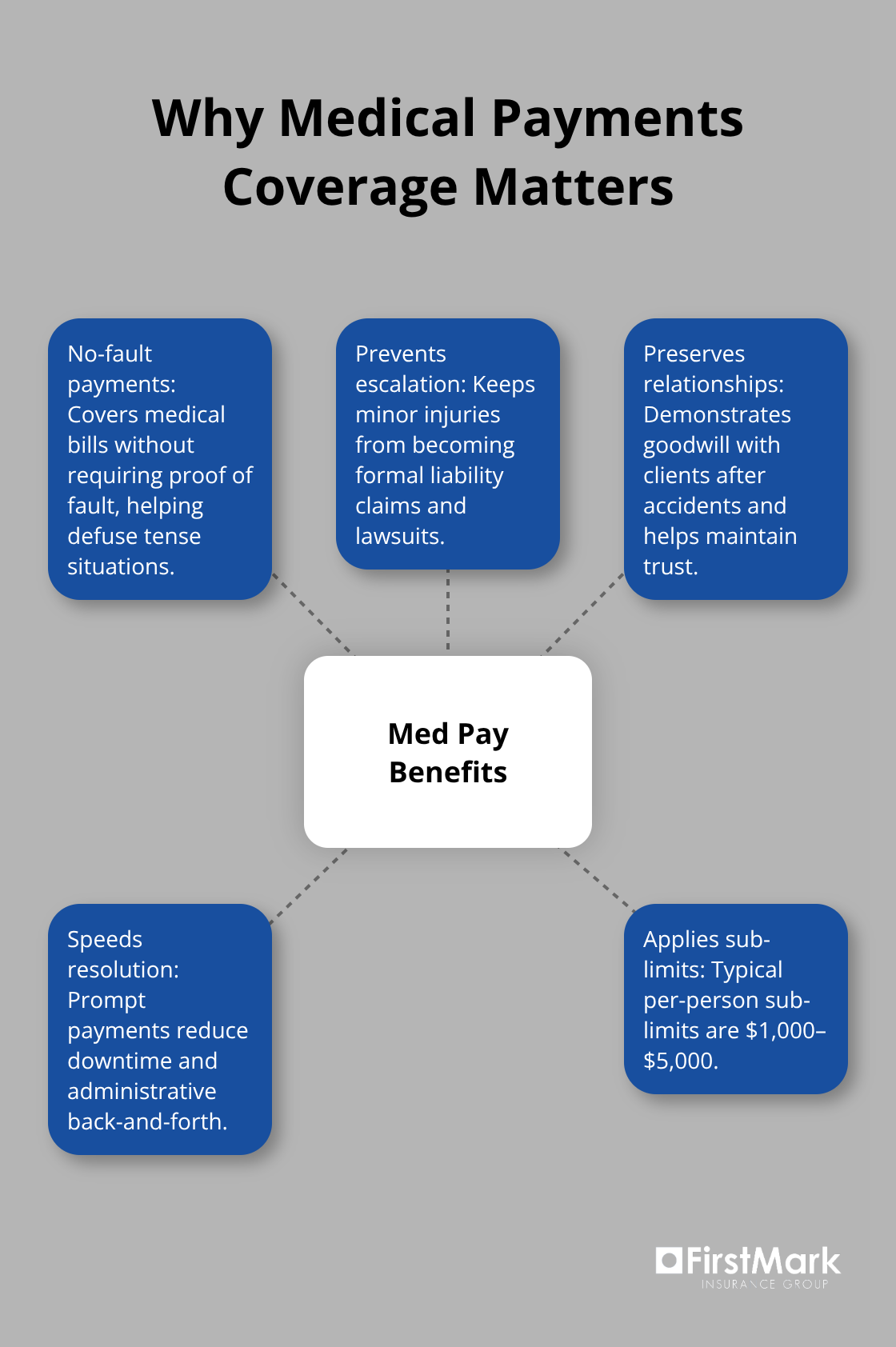

Medical payments coverage within your general liability policy pays injured parties’ medical bills without requiring them to prove fault. These payments typically come from a separate sub-limit of $1,000–$5,000 per person. This feature prevents minor injuries from becoming formal claims and keeps relationships intact with clients. You avoid the friction and expense of a drawn-out dispute over who caused the accident.

The injured party receives prompt payment for their treatment, and your business moves forward without the damage to reputation that contested claims create.

Defense Costs Operate Outside Your Policy Limit

Defense costs work differently than most business owners expect. The insurance company covers your legal fees and court expenses in addition to any settlement or judgment up to your limit-not from within it. Construction disputes in Washington average $3,000 to $150,000 in litigation costs alone, so this distinction matters significantly when you face a lawsuit. Some policies cap defense costs or include them within the limit itself, which substantially reduces your actual protection. When you review quotes from carriers, explicitly ask whether defense costs are additional or included, and request written clarification on your renewal documents. This single question can reveal thousands of dollars in hidden exposure or protection depending on how your policy is structured.

Washington-Specific Requirements and Regulations

Washington state mandates that contractors register with the Department of Labor & Industries and carry minimum surety bond requirements, but these floor requirements fall short for most real-world operations. The state’s L&I registration system verifies your coverage online in seconds, and if your policy lapses, your registration becomes invalid immediately-you cannot legally work until coverage is restored, with penalties reaching $5,000 per violation plus unlimited personal liability exposure. However, state minimums exist only to satisfy registration; actual client and vendor requirements drive coverage much higher. King County procurement rules push minimums to $1,000,000 per occurrence and $2,000,000 aggregate for county work, and private clients commonly demand identical limits before signing contracts. Cannabis businesses face the strictest mandate at $1,000,000 minimum, with Washington named as an additional insured.

How Location and Industry Shape Your Rates

General liability rates in Washington vary dramatically by industry and location. Seattle software consultants pay roughly $25–$40 monthly, while pressure washing operations run $1,000 or more monthly, reflecting real loss data and injury exposure differences. Urban counties like King and Pierce typically see 30–50% higher premiums than rural areas due to larger verdict pools and higher claim costs-a city-based contractor often faces materially different pricing than a rural counterpart with identical business profiles. The Washington Insurance Commissioner reported that general liability renewal rates rose 3.28 percentage points in 2025, the largest increase among tracked commercial lines, driven partly by Washington’s pure comparative negligence standard, which can raise settlements and claim costs substantially.

Claims History Determines Your Renewal Costs

A single serious claim, such as a $250,000 bodily injury settlement, can raise your renewal premiums by 20–40% for three to five years. This reality makes risk prevention your most cost-effective strategy. Documented safety programs yield 5–15% underwriting discounts from carriers like The Hartford and ERGO NEXT, but you must share written protocols, quarterly jobsite inspection records, subcontractor compliance documentation, and training records with your carrier 60–90 days before renewal.

Industry Risk and Environmental Factors

Industry risk level matters significantly: roofing, construction, and venues hosting public events carry higher injury exposure and property damage potential, translating to steeper premiums. Washington’s seismic risk and wet climate add underwriting complexity for certain operations, particularly those with outdoor work or equipment exposure.

Coverage Gaps That Leave You Exposed

Completed operations coverage is commonly excluded from basic general liability policies and typically requires a separate endorsement-if your work involves finished goods installation like cabinetry or flooring, you need installation floaters to cover material value during fitting. Renovations in pre-1978 homes demand lead-based paint liability coverage, and work near soil or involving demolition requires pollution liability endorsement. These gaps exist because standard general liability explicitly excludes pollution and environmental claims, creating real exposure if your operations involve contaminated materials or soil disturbance. Understanding these exclusions now prevents costly surprises when you file a claim or renew your policy, which is why the next section walks you through selecting limits that actually match your business exposure.

How to Choose the Right Coverage Limits

Map Your Past Projects and Client Requirements

Start by reviewing three years of your past projects, contracts, and incidents to understand what limits clients actually demand and what exposures you genuinely face. Request certificates of insurance from your five largest clients and note the minimum limits they require-most Washington businesses discover that their actual market demands far exceed state minimums. Software consultants operating in Seattle might reasonably carry $500,000 limits, but if you bid on King County projects or work for larger general contractors, you’ll find higher limits are standard expectations, not optional upgrades.

Calculate the True Cost of Higher Limits

The premium difference between $250,000 and $1,000,000 in limits typically runs only 15–25% annually, making the jump economically sensible when your exposure justifies it. Request quotes at multiple limits from at least three carriers licensed in Washington so you can see the actual cost curve and make an informed decision rather than guessing. Many business owners underbuy coverage to save $1,500 annually, then face a $100,000 claim that exhausts their limit-a false economy that exposes your personal assets when judgments exceed your policy.

Understand How Industry and Location Affect Your Rates

Industry classification drives pricing more than any other factor: roofing and construction operations face steeper premiums than professional services because injury exposure and property damage potential are objectively higher based on loss data. Urban location matters significantly too-King County and Pierce County businesses typically pay 30–50% more than rural Washington counterparts with identical operations, reflecting larger verdict pools and higher claim costs in populated areas.

Review Quotes for Hidden Cost Drivers and Coverage Details

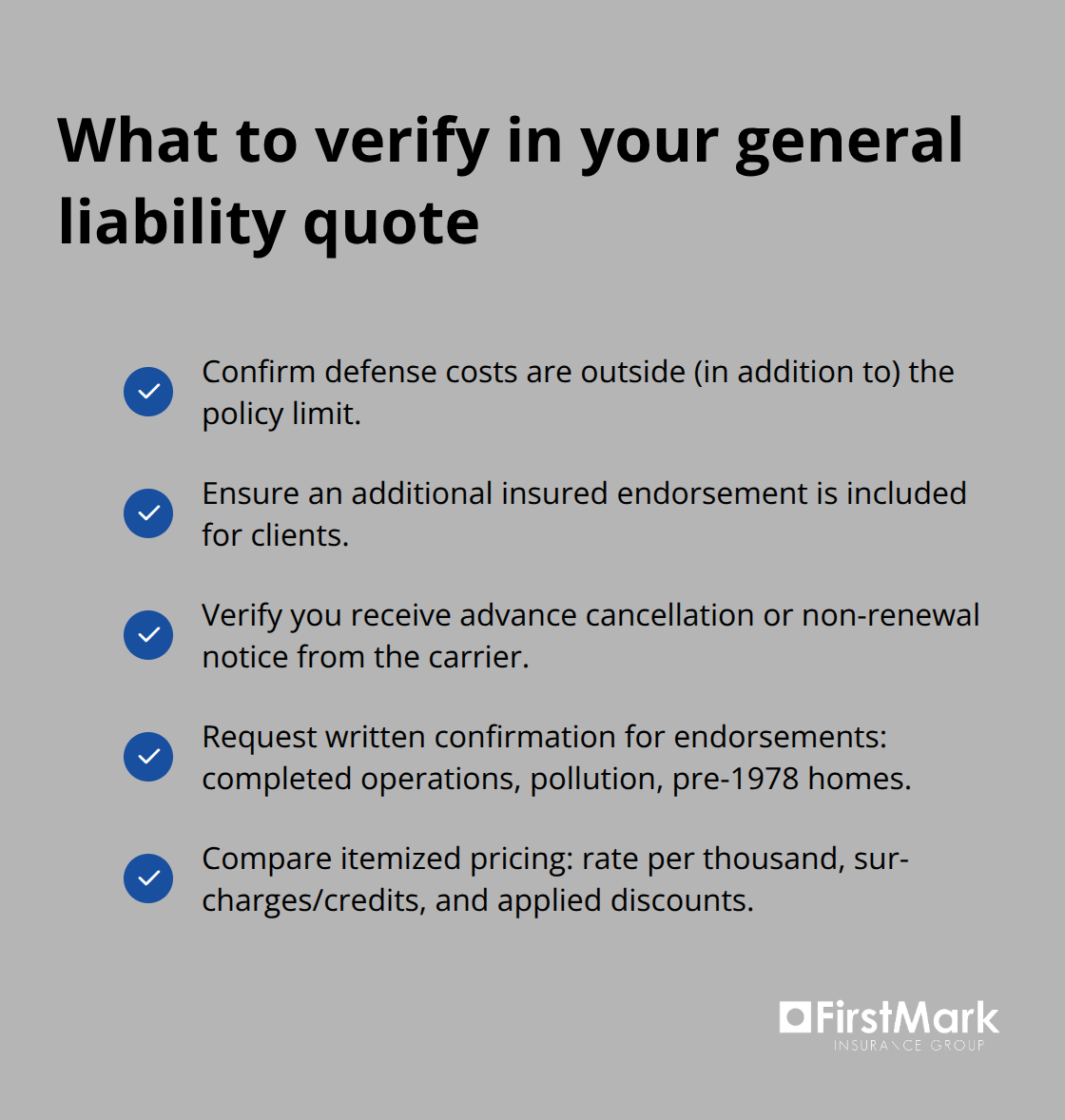

Your next step is requesting detailed renewal quotes that itemize rate per thousand of revenue, claims surcharges or credits, and every discount applied, then comparing the actual cost drivers across carriers rather than just the bottom-line premium. Confirm that defense costs are additional to your limit, not included within it, because this distinction can mean tens of thousands of dollars in actual protection when you face litigation. Ensure your policy includes an additional insured endorsement for clients and that your carrier will notify you before cancellation or non-renewal so you’re never caught without coverage. If your work involves completed operations, pollution exposure, or pre-1978 homes, request written confirmation that necessary endorsements are included in your quote-a cheaper proposal missing required coverage creates exposure when claims arise.

Schedule Your Coverage Review Before Renewal

Schedule your coverage review 60–90 days before renewal, when you have time to negotiate or shop alternatives before your policy term ends. This timing allows you to compare options and make changes without rushing into renewal at the last moment.

Final Thoughts

General liability coverage in Washington protects your business from the financial devastation that a single serious claim can trigger. The three core protections-bodily injury coverage, property damage liability, and legal defense costs-form the foundation of responsible risk management, but only when your limits match your actual exposure and your policy includes the endorsements your operations demand. State minimums exist as a floor, not a ceiling; your real coverage needs depend on your industry, location, client requirements, and the specific hazards you face on every project.

The cost of general liability coverage in Washington reflects genuine risk differences across industries and regions. A software consultant in Seattle operates in a fundamentally different risk environment than a roofing contractor in King County, and your premium reflects that reality. What matters most is that you carry adequate limits before a claim arrives, because underinsuring creates the illusion of savings until the moment a judgment exceeds your policy limit and your personal assets become exposed.

Schedule your coverage review 60 to 90 days before renewal so you have time to compare quotes, negotiate with carriers, and make informed decisions rather than rushing into renewal at the last moment. Gather your current policy documents and three years of project records, then reach out to FirstMark Insurance Group to discuss your coverage with someone who understands Washington’s regulatory environment and has access to multiple carriers. The right general liability coverage in Washington isn’t about the lowest premium-it’s about protecting your business with confidence.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation