Small businesses face complex risks that can threaten their operations and financial stability. A single incident could result in property damage, liability claims, or lost revenue.

We at FirstMark Insurance Group know that understanding Business Owners Policy coverages helps protect your company from these threats. This comprehensive guide breaks down each coverage component and shows you how to build the right protection for your business.

What Does a Business Owners Policy Actually Cover

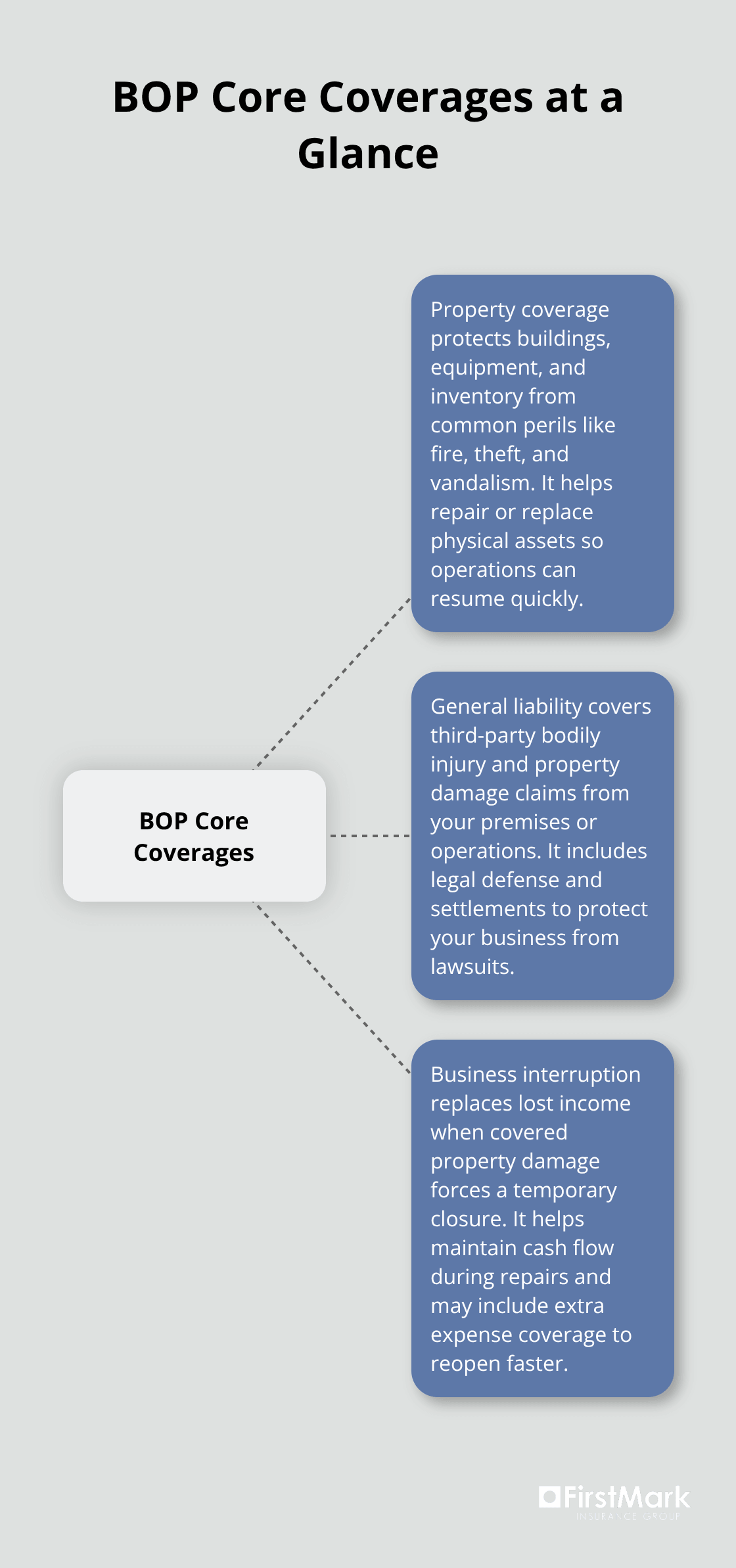

A Business Owners Policy packages three essential coverages that small businesses need most: commercial property insurance, general liability protection, and business interruption coverage. The Insurance Information Institute reports that this approach reduces costs by approximately 15-20% compared to separate policies. Property coverage protects your building, equipment, and inventory from risks like fire, theft, and vandalism.

General liability shields you from third-party claims when someone gets injured on your premises or your business operations damage someone else’s property.

Core Protection Components

Business interruption coverage replaces lost income when covered property damage forces you to temporarily close. This protection typically covers up to 12 months of lost revenue, which helps maintain cash flow during repairs. Most policies include extra expense coverage that pays for temporary relocation costs and expedited repairs to get your business operational faster.

Eligibility Requirements for BOP Coverage

Small businesses with fewer than 100 employees and less than $5 million in annual revenue qualify for BOP coverage. Retail stores, restaurants, professional offices, and service businesses benefit most from this protection. Commercial property insurance premiums have increased significantly, making BOP coverage an attractive option for most small operations. Businesses that operate from physical locations face higher risks and should prioritize BOP coverage over home-based businesses with minimal equipment.

Premium Factors That Drive Your Costs

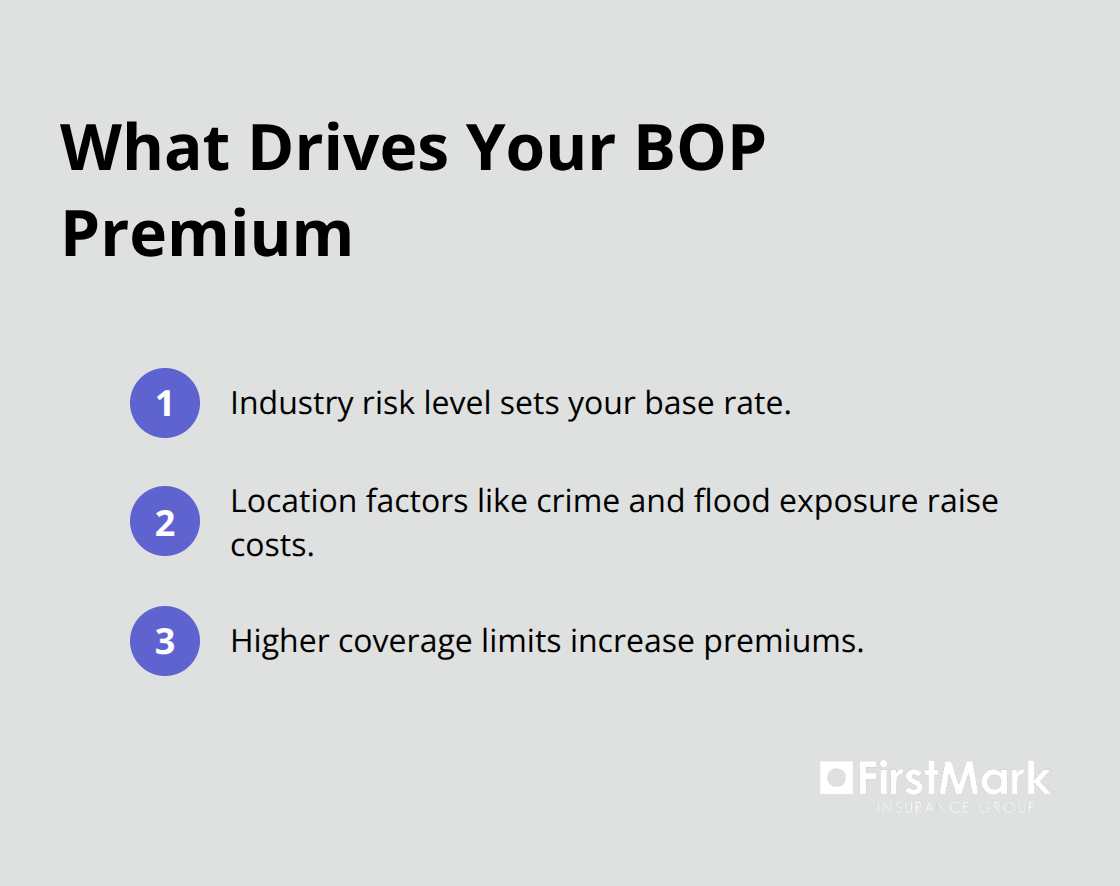

Your industry classification determines your base premium rate, with restaurants and construction companies that pay 40-60% more than office-based businesses. Location matters significantly – businesses in high-crime areas or flood zones face premium increases of 25-50%. Your coverage limits directly impact costs, with most small businesses that choose $1 million in liability coverage and $500,000 in property protection (these amounts provide adequate protection for typical small business operations).

These foundational coverages form the backbone of business protection, but many companies need additional specialized coverage to address modern risks and industry-specific exposures.

What Protection Does Each BOP Component Provide

Property Coverage Protects Your Physical Assets

Property coverage within your BOP protects buildings you own or rent, plus business personal property like equipment, inventory, and furniture. Named-peril coverage protects against specific risks including fire, lightning, windstorm, hail, explosion, riot, aircraft, vehicles, smoke, vandalism, sprinkler leakage, sinkhole collapse, and volcanic action. Special form coverage costs 15-25% more but covers all risks except those specifically excluded. Most policies cover business personal property within 100 feet of your premises, which protects equipment stored in nearby parking areas or temporary locations.

Your coverage limit should equal your property’s replacement cost, not its depreciated value. Small businesses often face challenges with inadequate property coverage when market solutions prove insufficient for their specific risks. We recommend annual property appraisals for businesses with equipment worth more than $100,000. Ordinance and law coverage adds 10-15% to your premium but pays for building code upgrades required during repairs after covered losses.

General Liability Stops Lawsuits From Destroying Your Business

General liability coverage pays legal defense costs and settlements when third parties sue your business for bodily injury or property damage. The average liability claim costs $45,000 according to the Insurance Information Institute, with legal defense costs that average $15,000 even for frivolous lawsuits. Standard policies provide $1 million per occurrence and $2 million aggregate limits. Professional service businesses should choose $2 million per occurrence because client contracts often require higher limits.

This coverage includes premises liability for injuries on your property, products liability for harm caused by items you sell, and completed operations liability for work you perform at other locations. Personal and advertising injury protection covers claims for libel, slander, copyright infringement, and wrongful eviction. Medical payments coverage automatically pays up to $10,000 per person for injuries on your premises without proof of negligence.

Business Interruption Coverage Replaces Lost Income

Business interruption insurance replaces net income lost when covered property damage forces you to suspend operations. Standard policies cover up to 12 months of lost income based on your previous year’s financial records. Extra expense coverage pays additional costs to minimize business interruption, including temporary relocation expenses, overtime labor, and expedited equipment replacement. Civil authority coverage pays for income losses when government orders prevent access to your business due to nearby property damage.

The median business interruption claim lasts 90 days according to Allianz Global Corporate, which makes this coverage essential for businesses that cannot operate without their physical location. Extended business income coverage continues payments for up to 60 additional days after repairs finish while you rebuild customer base and restore normal operations.

These core protections handle most common business risks, but modern companies face additional threats that require specialized coverage options beyond standard BOP components.

What Additional Protections Should You Add to Your BOP

Standard BOP coverage creates significant gaps that modern businesses cannot ignore. Cyber liability insurance has become mandatory for businesses that store customer data or process payments electronically. Data breaches create substantial financial impacts on organizations, with legal fees alone that average $52,000 per incident. Professional liability coverage protects service-based businesses from errors and omissions claims, with the average claim that costs $75,000 in legal defense and settlements. Equipment breakdown insurance covers mechanical failures not included in standard property coverage, which protects against losses that average $18,000 per incident according to Hartford Steam Boiler.

Cyber Protection Covers Digital Business Risks

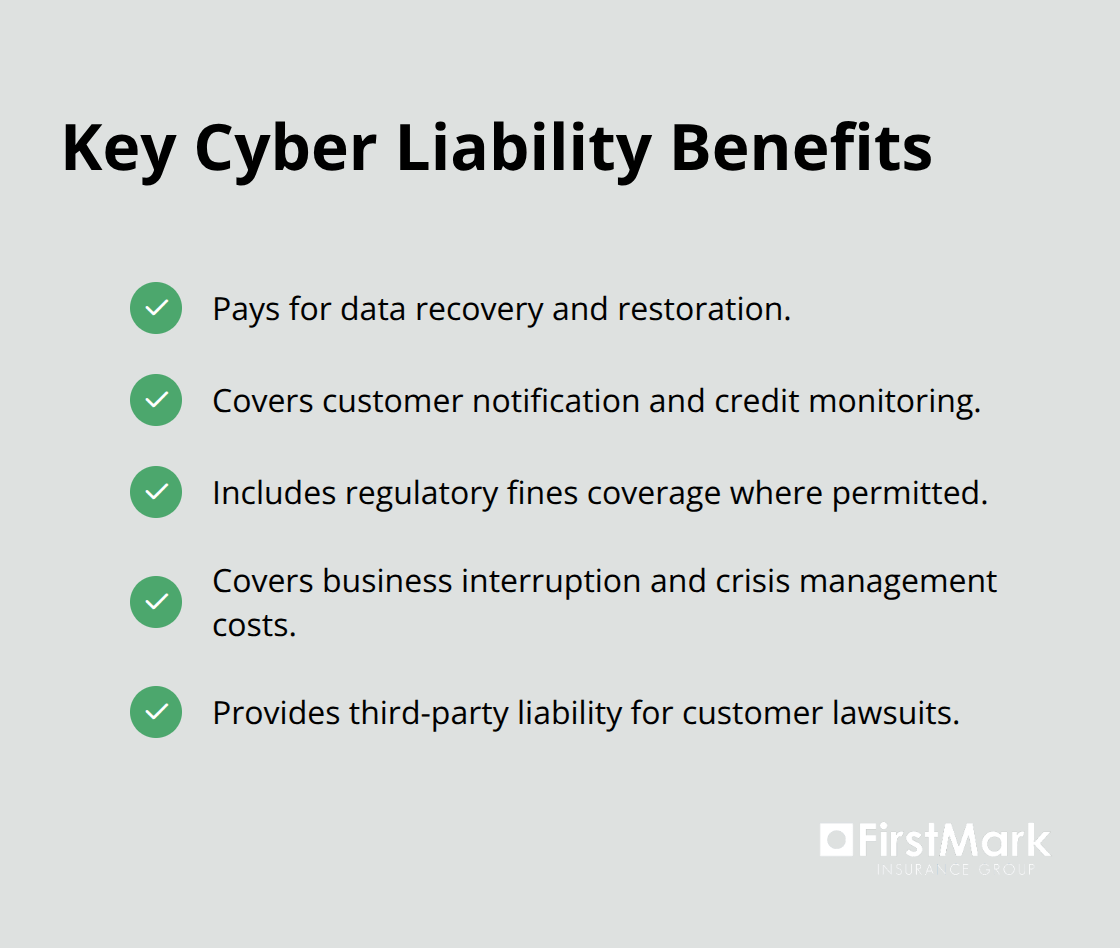

Cyber liability insurance pays for data recovery, customer notification, credit monitoring services, and regulatory fines after data breaches. Ransomware attacks cost small businesses an average of $84,116 according to Sophos, which makes this coverage essential for any business with digital operations.

Coverage should include first-party costs for business interruption, data restoration, and crisis management plus third-party liability for customer lawsuits. Most policies provide $1 million in coverage for $1,500-$3,000 annually (professional service firms need higher limits because client contracts often require $2-5 million in cyber coverage).

Professional Liability Protects Service Providers

Professional liability insurance covers mistakes, missed deadlines, and failure to deliver promised results. Technology companies face the highest risk with average claims of $125,000, followed by consulting firms at $89,000 per claim. Coverage includes legal defense costs, settlements, and judgments for alleged professional errors.

Equipment Breakdown Prevents Mechanical Failure Losses

Equipment breakdown coverage pays for spoiled inventory, extra expenses during repairs, and business income losses from mechanical failures. This protection costs 2-4% of your equipment value annually but prevents catastrophic losses from HVAC failures, computer crashes, and production equipment breakdowns that standard property insurance excludes (these mechanical failures can shut down operations for weeks without proper coverage).

Final Thoughts

Business Owners Policy coverages create comprehensive protection that small businesses need to survive unexpected incidents. Property, liability, and business interruption insurance work together to prevent single events from destroying years of hard work. Small businesses save 15-20% on premiums compared to separate policies while they gain streamlined claims and simplified policy management.

Appropriate coverage limits require careful evaluation of your assets, revenue, and industry risks. Property limits should match replacement costs rather than depreciated values. Liability coverage of $1 million per occurrence works for most businesses, but professional services often need $2 million to meet client contract requirements (business interruption limits should cover 12 months of expenses and lost profits based on your financial records).

We at FirstMark Insurance Group help businesses navigate insurance complexities and find ideal coverage at competitive rates. Contact us today to review your current protection and identify gaps that could threaten your business operations. Our team will present options from top insurance providers that fit your specific requirements and budget constraints.