Professional liability insurance protects your reputation and finances when clients claim you failed to deliver the standard of care they expected. Whether you’re an attorney, accountant, consultant, or medical professional in Washington, a single negligence claim can threaten your business.

Getting accurate Washington professional liability quotes requires understanding what insurers evaluate and how your specific situation affects your premium. We at FirstMark Insurance Group help professionals navigate this process with clarity and precision.

What Professional Liability Insurance Actually Covers

Professional liability insurance protects you when clients sue for negligence, errors, or failure to deliver the standard of care expected in your field. In Washington, this coverage pays for legal defense costs and damages awarded by courts or settlements-expenses that can easily exceed $100,000 even for small claims. The Washington Office of the Insurance Commissioner reported 318 new malpractice claims in 2021, with a median indemnity payout of just over $340,000 and the highest verdict exceeding $12 million. For attorneys, accountants, consultants, engineers, healthcare providers, and technology professionals, a single claim without coverage can force closure. Washington’s consulting sector alone contributed $12.4 billion to the state’s GDP in 2023, with about 87,000 people earning income from professional advice-most of them operating as solo practitioners or small firms with limited financial reserves. The median professional liability claim against Washington consultants in 2022 was roughly $112,000, about 18% higher than the national median according to the Insurance Information Institute. A 2023 national survey estimated the average Washington consultant spends about $48,700 on legal fees before indemnity payments are even considered, which underscores why robust coverage matters more than premium cost.

Defense Costs Arrive First and Drain Cash Flow

Your professional liability policy covers both defense costs and indemnity, but defense expenses often arrive first and fastest. A Spokane SaaS claim settled for $425,000 plus $150,000 in defense costs, illustrating how forensic analysis, expert witnesses, and litigation consume significant resources before any settlement. Seattle-area attorney rates average around $367 per hour, meaning a moderately complex claim can accumulate $50,000 to $100,000 in legal fees within months. Without coverage, you pay these costs immediately from operating capital, potentially forcing you to reduce staff, delay client projects, or tap lines of credit. Professional liability policies written on a claims-made basis require continuous coverage; if you stop paying premiums or switch carriers without extended reporting coverage, you lose protection for past work-a critical vulnerability for professionals serving long-term clients where problems surface years later.

Washington’s Regulatory Requirements Vary by Profession

Different professions and clients impose different coverage requirements. Physicians must show financial responsibility under Washington’s RCW 7.70.150, while architects bidding on public contracts must demonstrate errors and omissions coverage. Adult family homes in Washington must carry commercial general liability and professional liability insurance, with average annual per-bed premiums of $424 according to a Washington Office of the Insurance Commissioner study analyzing 14,746 liability policies from 2019 through 2024. The state Department of Enterprise Services requires minimum professional liability of $2 million aggregate for most consulting contracts with state agencies. If you serve international clients, confirm your insurer covers work performed outside the U.S., as some carriers exclude foreign engagements. High-risk industries like aerospace, healthcare IT, and financial advisory often require $2 million to $5 million per occurrence to satisfy client contracts-limits that cost significantly more but protect your ability to win enterprise business.

Understanding what your policy covers and what regulatory minimums apply to your profession sets the foundation for selecting appropriate limits. The next step involves recognizing which specific factors insurers evaluate when calculating your premium, since two professionals in the same field can receive vastly different quotes based on their claims history, revenue, and risk profile.

What Determines Your Professional Liability Premium

Industry Risk Creates the Foundation

Industry risk sits at the center of every quote you receive. Insurers categorize professionals by exposure level, and two consultants earning identical revenue face vastly different premiums based on their specialization. A solo graphic designer typically pays $600 to $1,000 annually for a $1 million per $1 million policy, while a five-attorney law firm with the same revenue structure pays $7,500 to $15,000 for $2 million per $4 million coverage. Technology and software professionals face particularly acute scrutiny because data breaches, missed deadlines, and software errors create measurable financial damages that clients can quantify. Healthcare providers encounter even steeper premiums due to malpractice exposure, with a mid-size clinic serving 20 practitioners paying $55,000 to $120,000 annually. Washington’s aerospace sector, concentrated around Puget Sound, commands premium rates reflecting design-flaw liability, while agribusiness operations face distinct underwriting based on labeling and compliance risks.

Claims History Shapes Your Rate More Than Any Other Factor

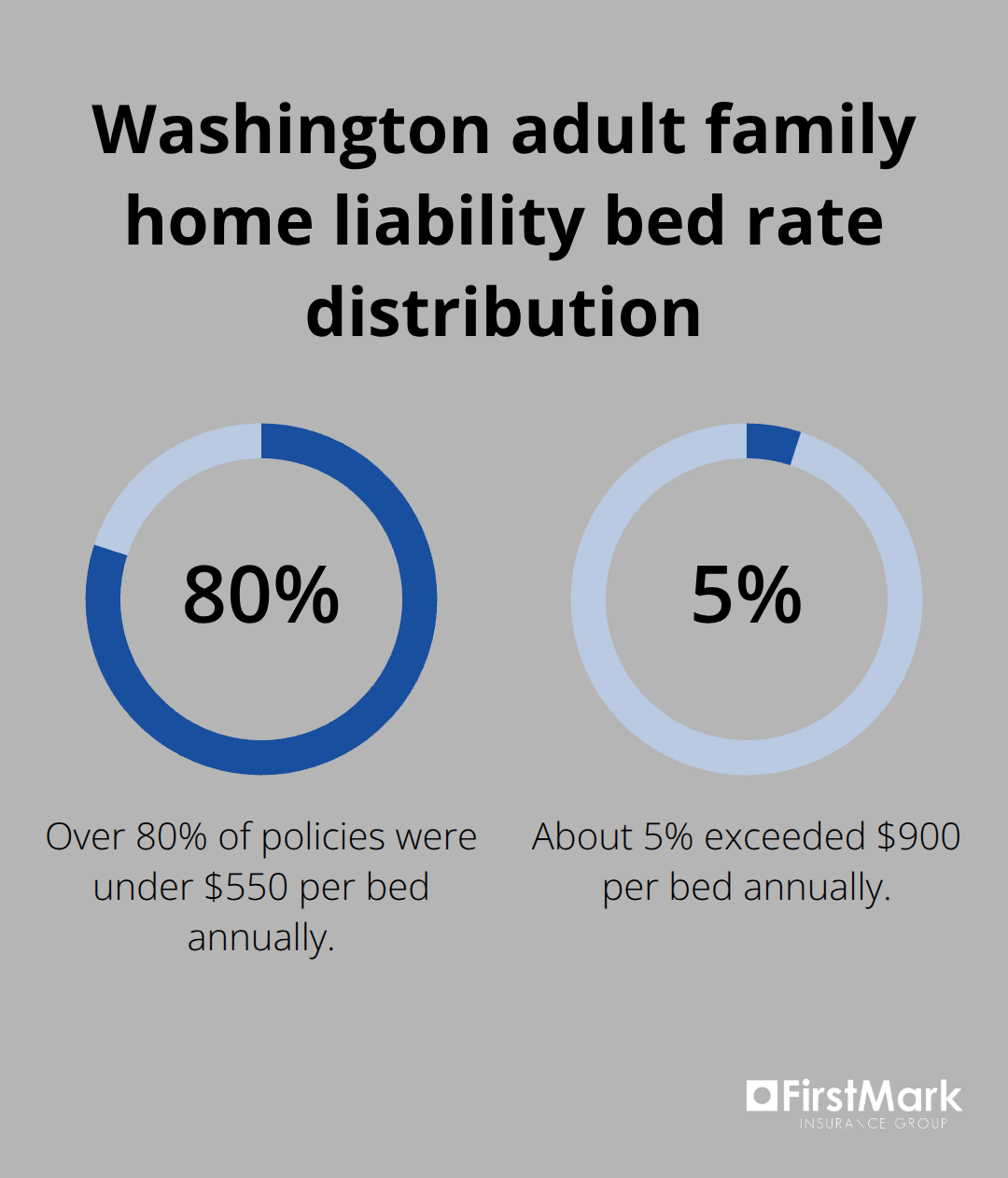

Your actual claims history shapes your quote more decisively than any other factor. A professional with a clean loss record for five years qualifies for preferred rates, whereas even one settled claim triggers surcharges that persist for years. The Washington Office of the Insurance Commissioner data shows that among adult family homes in Washington, over 80 percent of policies carried annual bed rates under $550, yet approximately 5 percent faced charges exceeding $900 per bed annually-more than double the median. This spread reflects underwriting decisions based on prior claims, staffing stability, and facility management practices.

Deductibles and Coverage Limits Require Strategic Decisions

Increasing your deductible from $2,500 to $10,000 reduces premiums by approximately 20 percent, though higher deductibles strain cash flow during defense phases when legal fees accumulate fastest. Solo practitioners and small firms often accept $5,000 deductibles as a middle ground, balancing premium savings against manageable out-of-pocket exposure. Coverage limits demand strategic thinking beyond regulatory minimums. Professional liability coverage must be at least $1 million per occurrence and $3 million annual aggregate, but enterprise clients frequently demand higher limits, and aerospace contractors may require even higher. Bundling professional liability with cyber liability or general liability saves 15 to 20 percent on total premiums compared to purchasing policies separately, though you must verify aggregate limits across all bundled coverages remain sufficient.

Geography and Risk Management Practices Lower Your Cost

Geography influences your quote in subtle but measurable ways. Downtown Seattle offices with superior fire suppression systems and low flood risk receive lower property and liability premiums than converted warehouses in Yakima facing wildfire exposure. Risk-management practices reduce premiums by 5 to 10 percent when you document client intake procedures, maintain written engagement letters, implement peer-review programs, and establish documented workflows. Cybersecurity controls including multi-factor authentication, employee training, and backup systems specifically lower cyber liability costs.

Understanding these premium drivers positions you to make informed decisions about coverage structure. The next step involves learning how to gather the right information and compare quotes effectively, which requires knowing exactly what insurers need from you and how to evaluate their responses.

How to Get Accurate Professional Liability Quotes in Washington

Gather the Information Insurers Actually Need

Insurers cannot quote you accurately without detailed information about your business structure, revenue, and actual service scope. Start by documenting your gross annual revenue for the past three years, your number of employees or contractors, and the specific services you deliver. If you’re a consultant, specify whether you provide strategic advice, implementation support, or both-the distinction matters because implementation claims typically cost more to defend. If you’re a healthcare provider, note whether you work within a network or independently, since network providers face different malpractice exposure.

Collect your claims history, including any prior incidents reported to previous insurers, even if they didn’t result in lawsuits. The Washington Office of the Insurance Commissioner requires insurers to explain premium increases under transparency rules, so your loss-run history directly influences your quote. Document any risk-management practices you’ve implemented: written engagement letters, documented workflows, peer-review programs, or cybersecurity controls like multi-factor authentication. Insurers reduce premiums by 5 to 10 percent when you demonstrate these practices.

If you serve specific industries or client types-such as state agencies, healthcare systems, or technology companies-note those relationships because they often impose minimum coverage requirements that affect your quote structure. Professionals who skip this preparation stage receive inflated quotes based on worst-case assumptions, then face premium reductions later when they supply accurate information, creating frustrating back-and-forth negotiations.

Compare Three Quotes Side by Side

Obtaining three quotes from different carriers reveals how dramatically premiums vary for identical coverage. The Hartford offers some of Washington’s lowest professional liability quotes at approximately $81 per month, while ERGO NEXT averages about $83 per month with stronger customer ratings. Simply Business provides access to 16 or more carriers including CNA, Travelers, and Hiscox, allowing you to compare pricing across substantially different underwriting appetites within a single platform.

When comparing quotes, verify that coverage limits, deductibles, and policy terms match across all three-a $1 million per occurrence limit differs fundamentally from $2 million, and defense-inside-limits language versus defense-outside-limits dramatically affects your actual protection. Take time to review what each carrier excludes and which endorsements they offer at additional cost.

Work with an Agent Who Understands Washington Markets

An experienced insurance agent who understands Washington’s regulatory environment and your specific profession eliminates guesswork. Agents identify which carriers specialize in your industry, negotiate better terms on extended reporting periods, and ensure endorsements like additional insured status or waiver of subrogation match your client contracts. If you work in aerospace, agribusiness, or healthcare IT, a local agent familiar with Puget Sound or Spokane market dynamics knows which carriers accept those risks readily and which impose severe restrictions.

We at FirstMark Insurance Group, with 30 years of experience guiding businesses through insurance complexities, help professionals navigate this entire process. Our approach focuses on presenting you with choices from top insurance providers that fit your specific requirements at the best available pricing, ensuring your quote reflects accurate risk assessment rather than overly conservative assumptions that inflate your premium unnecessarily.

Final Thoughts

Professional liability insurance protects your business from the financial devastation that follows a negligence claim. Washington professional liability quotes reveal that median claims exceed $112,000, and defense costs alone can drain $50,000 to $100,000 before settlement discussions begin. Understanding what your policy covers, recognizing which factors drive your premium, and obtaining accurate estimates positions you to make decisions based on facts rather than assumptions.

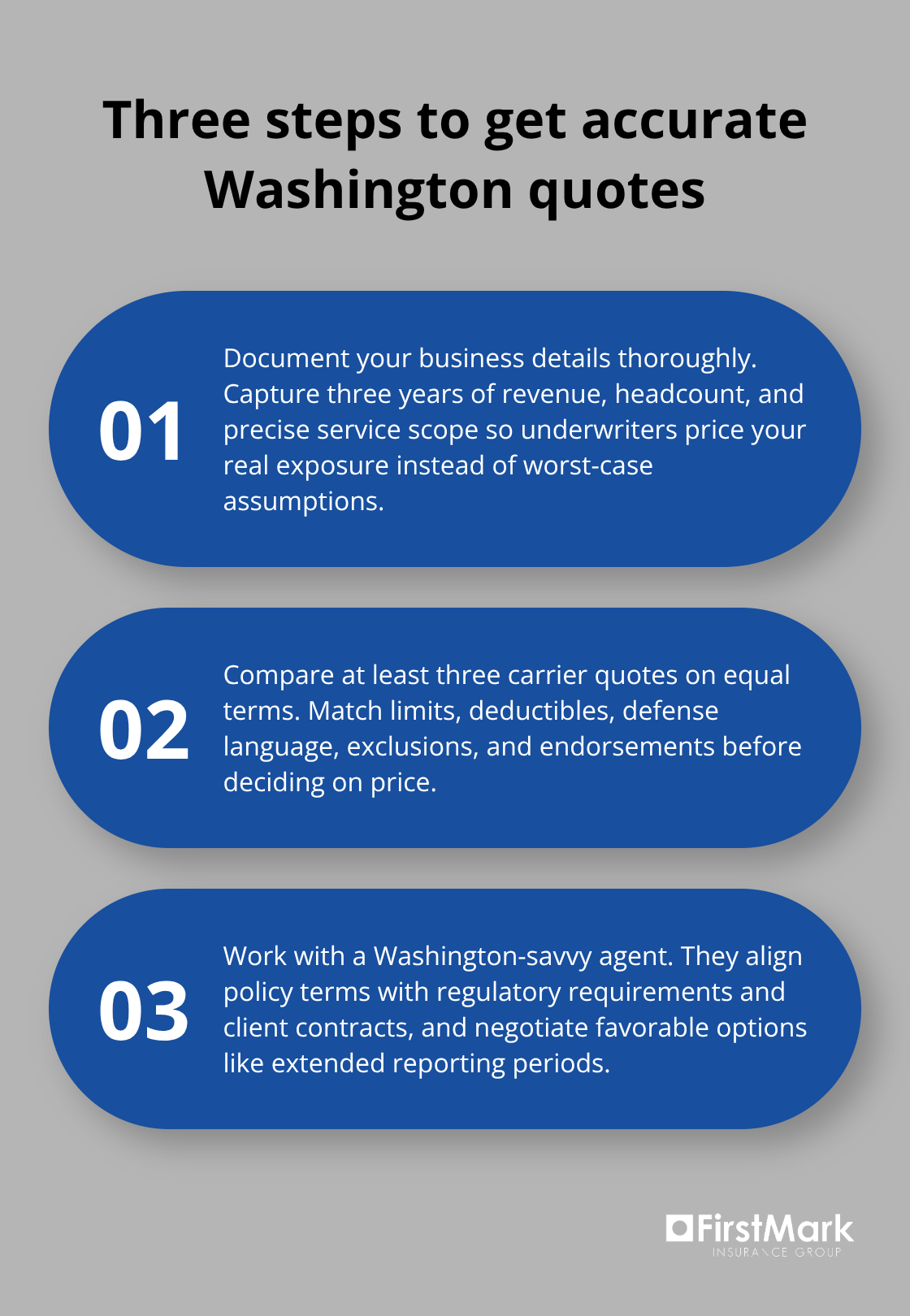

The path forward requires three concrete steps. First, gather detailed information about your business structure, revenue, claims history, and service scope-insurers cannot quote accurately without this foundation. Second, obtain quotes from at least three carriers and compare them side by side, verifying that coverage limits, deductibles, and exclusions match across all proposals. Third, work with an experienced agent who understands your profession and Washington’s regulatory landscape, ensuring your policy includes necessary endorsements and reflects your actual risk profile rather than worst-case assumptions.

Contact FirstMark Insurance Group to discuss your professional liability needs and receive tailored guidance for your situation. We help you understand the relationship between coverage structure and long-term protection, ensuring your policy supports your business growth without leaving gaps that surface during claims.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation