Professional liability claims can devastate a small business. A single lawsuit over a missed deadline, faulty advice, or service failure can drain your reserves and damage your reputation.

At FirstMark Insurance Group, we’ve seen too many business owners operate without adequate protection, thinking general liability is enough. It isn’t. Small business professional liability coverage fills the gap that standard policies leave wide open, and it doesn’t have to break your budget.

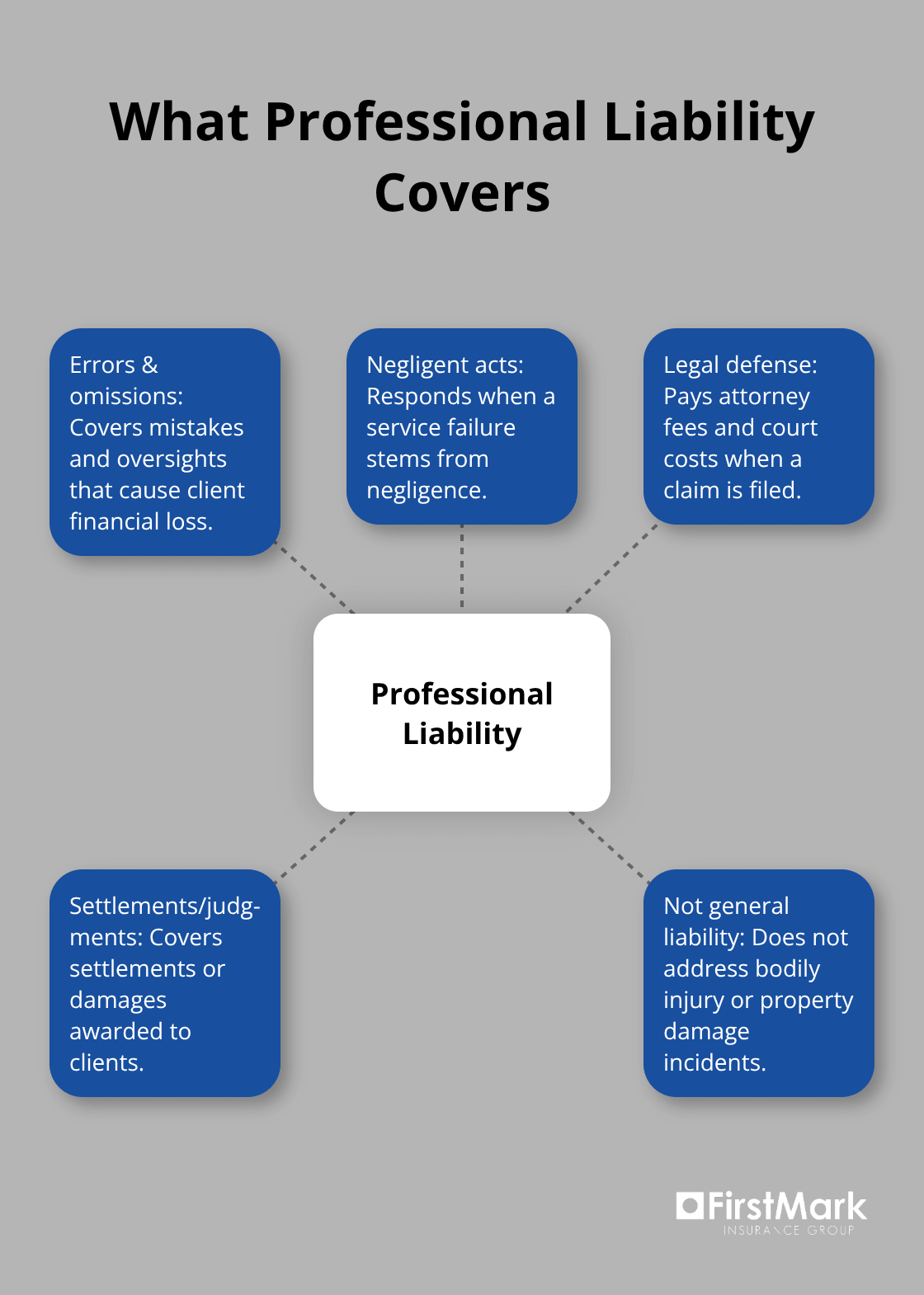

What Professional Liability Really Covers

Professional liability insurance protects your business when a client claims your work caused them financial loss. This isn’t about someone slipping in your office or getting hurt on your property-that’s what general liability handles.

Professional liability covers errors, omissions, and negligent acts. If you’re a consultant and your advice tanks a client’s project, or you’re an accountant and a tax error costs them thousands, professional liability steps in to cover legal defense costs and settlements.

How Professional Liability Claims Actually Work

Professional services claims vary dramatically in cost and scope. A missed deadline for an IT consultant might trigger a $50,000 claim. A design flaw for an engineer could balloon into six figures. General liability won’t touch these situations because they don’t involve physical injury or property damage-they involve the quality or outcome of your service. The Hartford reports that professional services claims average about $61 monthly in premiums across industries, reflecting the real exposure that service providers face daily.

The Gap General Liability Leaves Open

Most small business owners buy general liability and assume they’re protected. They’re wrong. General liability covers third-party bodily injury, property damage, and advertising injury. It protects you if a customer falls in your office or your ad infringes on someone’s trademark. But it completely ignores professional service failures.

A therapist, accountant, consultant, or IT professional operating on general liability alone has zero protection against their core risks. Your client sues. You have no coverage. You pay out of pocket for legal fees, settlements, and any damages awarded.

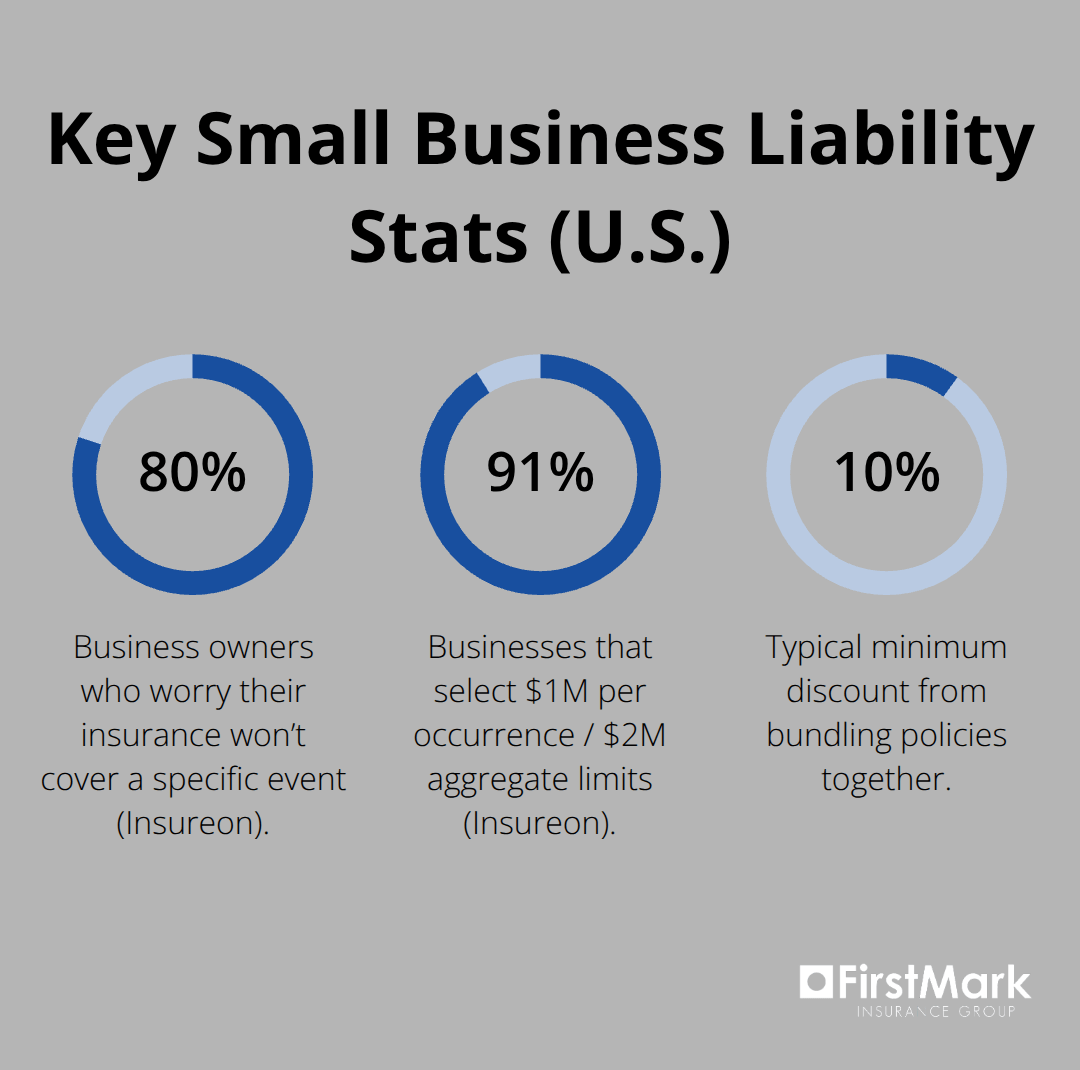

According to Insureon data, about 80% of business owners worry their insurance won’t cover a specific event-and for service-based businesses, that event is almost always a professional mistake.

Affordable Protection Against Catastrophic Exposure

For solo professionals, professional liability premiums run roughly $500 to $1,500 annually. Mid-sized firms typically pay $1,500 to $5,000 per year. That’s affordable protection against catastrophic exposure. Bundling professional liability with general liability often yields discounts, bringing your total cost down further while eliminating the dangerous gap between two separate policies.

The right coverage transforms your risk profile. Instead of facing unlimited personal liability for professional mistakes, you transfer that risk to an insurer. Your business stays protected. Your reputation stays intact. Your finances remain stable. Now that you understand what professional liability actually covers and why general liability falls short, the next step involves assessing your specific risk exposure and finding the coverage options that fit your budget.

Finding Affordable Professional Liability Coverage

Assess Your Actual Risk Exposure

Assessing your actual risk exposure starts with an honest conversation about what could go wrong in your business. A consultant managing client projects faces different exposure than an accountant preparing tax returns, which differs again from an engineer designing systems. The Hartford’s data shows professional services claims average around 62% pay $300 to $600 annually for their professional liability coverage, but your specific premium depends entirely on your industry classification, business size, and revenue. Restaurants pay roughly $413 monthly for general liability due to slip-and-fall risk, while IT consultants pay substantially less because their core risks don’t involve bodily injury. Your professional liability premium reflects your actual exposure.

Document your current revenue, employee count, and the specific services you deliver. This information forms the foundation for accurate quotes. When you request quotes from multiple carriers-not one or two, but at least three to five-you reveal whether you’re looking at competitive pricing or overpaying for coverage. Insureon works with over 40 U.S. providers and has issued more than 1.5 million policies, giving you access to carriers with different pricing models and industry specializations. Solo professionals typically find premiums between $500 and $1,500 annually, while mid-sized firms see $1,500 to $5,000 per year. Getting multiple quotes takes roughly 20 minutes of your time.

Bundle Policies for Meaningful Savings

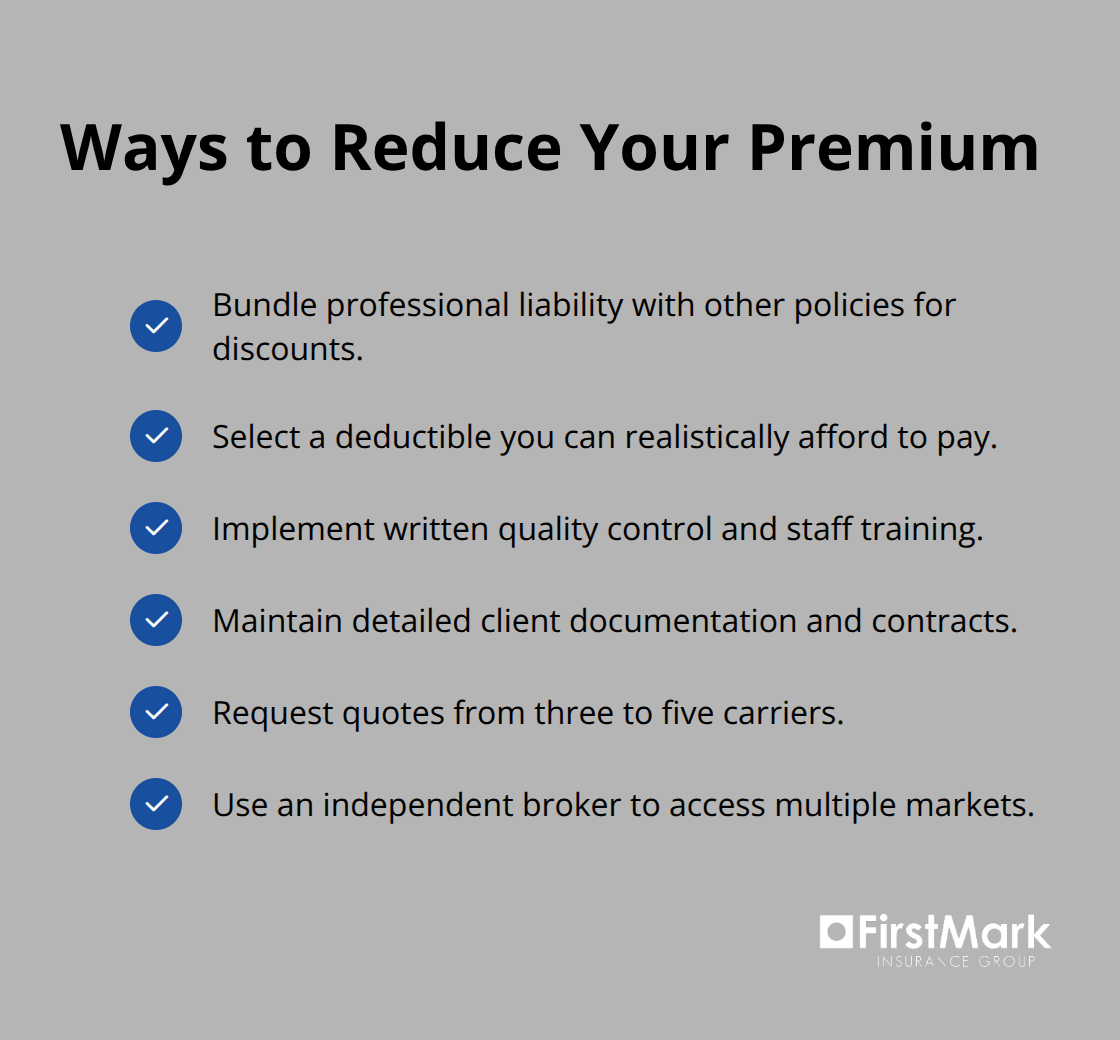

Bundling professional liability with general liability, commercial property, or cyber insurance delivers meaningful savings-typically 10 to 20 percent off combined premiums compared to buying policies separately. A Business Owner’s Policy bundling general liability and property coverage averages around $57 monthly, versus separate policies that cost more. When you add professional liability to that bundle, carriers like The Hartford and PHLY offer additional discounts because they prefer multi-product relationships.

Your deductible choice directly impacts your monthly cost. Increasing your deductible from $500 to $1,000 or $2,500 reduces your premium noticeably, but you’ll pay more out of pocket if a claim occurs. Most small businesses choose the standard $1 million per occurrence and $2 million aggregate limits-91 percent of businesses surveyed by Insureon selected exactly this combination-because it balances solid protection with reasonable premiums.

Strengthen Your Risk Profile

Implementing documented risk management practices strengthens your negotiating position with insurers. If you maintain written quality control processes, provide regular staff training, and keep detailed client documentation, insurers recognize lower risk and offer better rates. An independent insurance broker accessing wholesale markets and multiple carriers often secures 15 to 25 percent better rates than direct quotes because they work with specialty insurers unavailable through standard channels.

These cost-reduction strategies work together. A broker helps you bundle policies, document your risk controls, and present your business in the strongest possible light to underwriters. The combination of smart deductible selection, multi-policy bundling, and demonstrated risk management transforms professional liability from an expensive add-on into affordable, integrated protection.

With your coverage options identified and your budget optimized, the next step involves selecting the specific limits and deductibles that match your industry’s actual exposure.

What Coverage Limits Actually Mean for Your Business

The standard $1 million per occurrence and $2 million aggregate limit has become the default choice for small businesses, and Insureon data confirms that 91 percent of businesses select exactly this combination. This isn’t because it’s universally optimal-it’s because it’s the middle ground that most carriers offer and most brokers recommend. The reality is more nuanced. A solo consultant handling project advisory work faces vastly different exposure than a mid-sized engineering firm designing infrastructure systems. Your coverage limit should reflect what a realistic worst-case claim in your industry actually costs, not what sounds reasonable in the abstract.

Match Your Limits to Your Industry’s Real Exposure

The Hartford’s claims data shows professional services claims average around $61 monthly in premiums, but individual claims can range from $30,000 for a missed deadline to $500,000 for a design error that cascades through a client’s operations. Starting with the $1M/$2M standard makes sense, but you should pressure-test this assumption against your specific work. If you’re a therapist or small consultant, $1M per occurrence might be genuinely excessive and drive your premium higher than necessary. If you’re an engineer or architect advising on major projects, $1M could leave you dangerously underprotected.

The Hartford and PHLY, two of the strongest carriers for professional liability, will adjust your limits during the quoting process. Request quotes at both the standard $1M/$2M and at lower limits like $500K/$1M to see the actual premium difference. That comparison reveals whether you’re overpaying for coverage you’ll never use.

Choose Your Deductible Based on Cash Position

Your deductible choice directly controls your monthly cost, and this is where most small business owners make poor decisions. Increasing your deductible from $500 to $1,000 cuts your premium by roughly 10 to 15 percent, while jumping to $2,500 can reduce it by 20 to 30 percent depending on your industry and claims history. The math seems obvious-higher deductible means lower premium. But the decision requires honest assessment of your cash position.

If a claim occurs and you must pay $2,500 out of pocket before your insurance kicks in, can you absorb that hit without disrupting operations or client service? Most small business owners cannot, which is why the $500 deductible remains standard across the industry. The trap occurs when owners select a $2,500 or $5,000 deductible to save premium dollars, then face a real claim and realize they lack the reserves to pay it. You then negotiate with the carrier, damage the relationship, and potentially lose the policy. A $500 or $1,000 deductible keeps your monthly cost reasonable while ensuring you can actually meet your obligation if a claim materializes.

Understand What Your Policy Excludes

Policy exclusions rarely surprise small business owners because most standard professional liability policies cover the same core risks-errors, omissions, negligence, and breach of contract. What matters is understanding what your policy specifically excludes. Some carriers exclude prior acts, meaning claims arising from work you performed before the policy started date. Others exclude certain service types or client industries.

When you request quotes, ask explicitly what the carrier excludes for your profession. If you’re in IT and cyber liability isn’t bundled, confirm whether your professional liability covers data breach response or only covers claims by clients who suffered financial loss from your coding errors. The carrier’s answer determines whether you need additional cyber coverage. Don’t accept vague language-demand specificity about what is and isn’t covered before you commit to a policy.

Final Thoughts

Professional liability insurance protects your business from the financial devastation of service failures, missed deadlines, and negligent advice. The coverage remains affordable, especially when you bundle it with general liability or commercial property policies. Solo professionals pay $500 to $1,500 annually, while mid-sized firms typically invest $1,500 to $5,000 per year for solid protection that costs far less than defending a single lawsuit or paying a settlement out of pocket.

Three concrete actions move you forward immediately. Document your current revenue, employee count, and the specific services you deliver, then request quotes from at least three to five carriers to reveal whether you’re looking at competitive pricing or overpaying. Ask each carrier about bundling discounts and how their exclusions apply to your profession, since a $500 deductible paired with standard $1 million per occurrence limits represents the choice most small businesses make for good reason-it balances affordability with genuine protection.

At FirstMark Insurance Group, we guide businesses through small business professional liability decisions and work with top insurance providers to present you with choices that fit your requirements at the best available pricing. Reach out to FirstMark Insurance Group or another licensed broker, provide your business details, and request quotes-most carriers deliver certificates of insurance within 24 hours of purchase. After you secure coverage, schedule an annual review to confirm your limits still match your business size and revenue, since your coverage needs change as your business grows.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation