General liability protection in Washington isn’t optional-it’s a business fundamental. Whether you operate a small service company or manage a larger enterprise, the right coverage shields you from costly claims that could otherwise devastate your finances.

At FirstMark Insurance Group, we’ve seen firsthand how the wrong coverage limits leave business owners exposed. This guide walks you through exactly what you need.

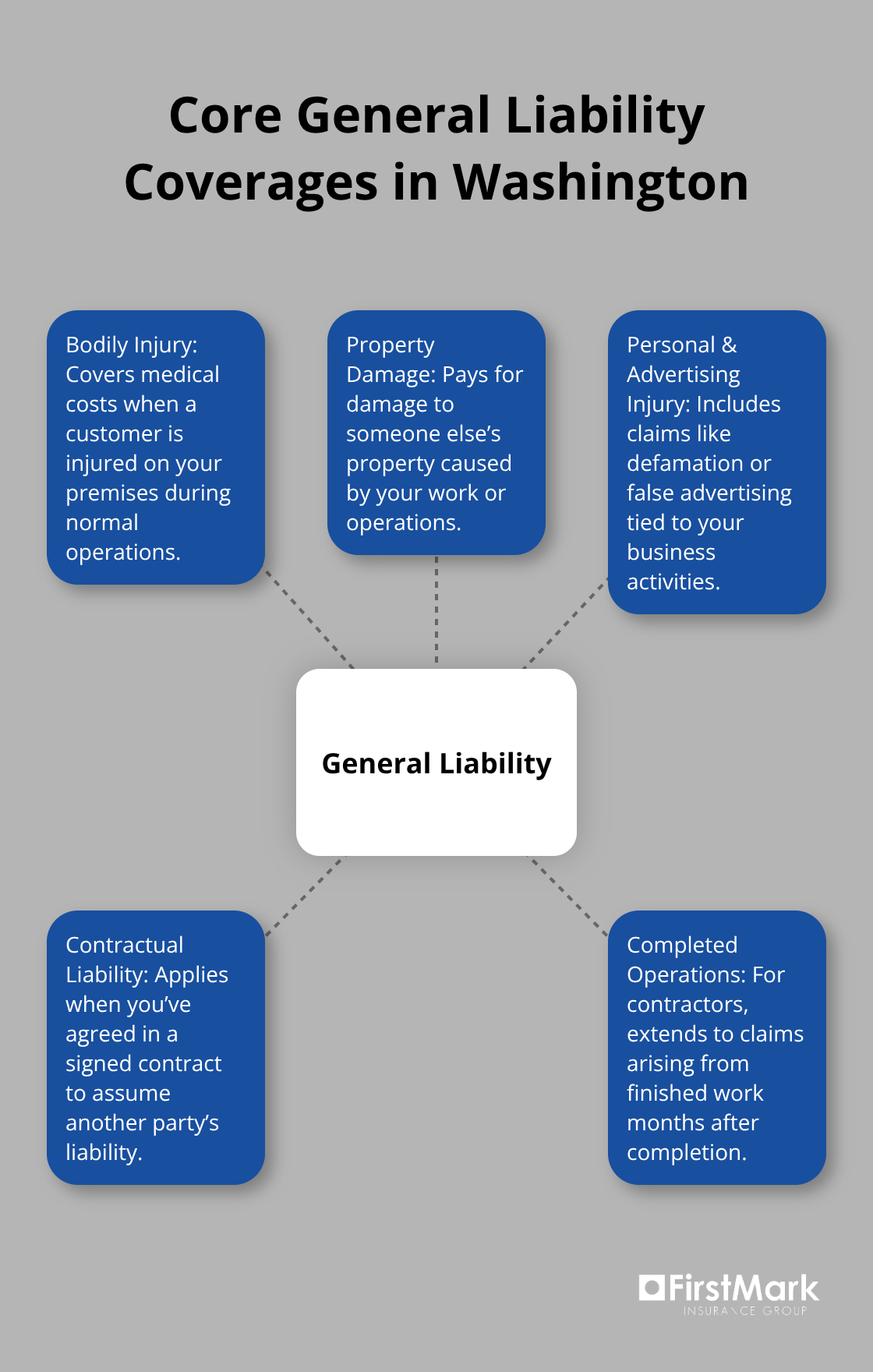

What General Liability Actually Covers in Washington

The Scope of Protection

General liability insurance protects your business against third-party claims for bodily injury and property damage that occur during normal operations. This covers medical bills when a customer slips on your premises, damage to someone else’s property caused by your work, or injuries from your products. Washington law doesn’t mandate general liability for all businesses, but most clients, landlords, and contract opportunities require it-often at $1 million per occurrence with $2 million aggregate. The coverage also includes personal injury claims like defamation or false advertising, and contractual liability if you’ve agreed to cover someone else’s liability in a signed agreement.

Coverage for Contractors and Specialized Operations

For contractors, completed operations liability extends protection to claims from work you finished months ago. Enhanced services facilities in Washington must comply with state regulations under WAC 388-107-1120, which require minimum limits of $1 million per occurrence and $2 million general aggregate, with coverage for employee and volunteer acts, independent contractors, and products liability.

Real Claims and Their Costs

Real claims show why adequate limits matter. A slip-and-fall resulting in a broken hip can cost $50,000 to $150,000 in medical expenses alone, and Washington’s pure comparative negligence system means plaintiffs recover damages even if partially at fault-there’s no cap on non-economic damages. Construction defects, water damage from installation errors, or injury from equipment failure regularly exceed $500,000 in settlement value.

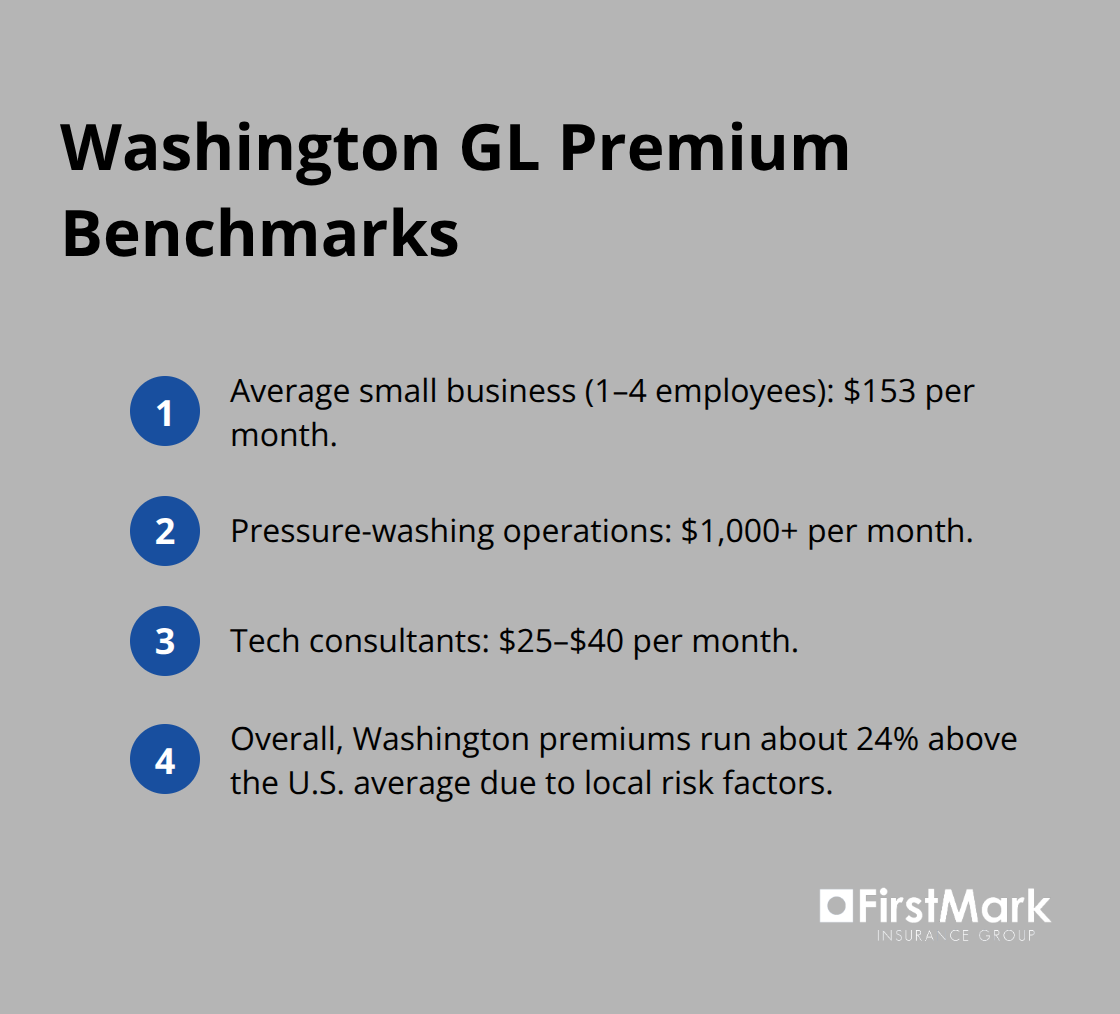

Premium Costs Across Washington Industries

General liability premiums in Washington average $153 per month for small businesses with 1–4 employees, according to MoneyGeek data, though costs vary dramatically by industry: pressure-washing operations run $1,000+ monthly while tech consultants pay $25–$40. High-risk sectors like roofing, hospitality, and healthcare face steeper premiums because their loss histories justify higher underwriting costs. Washington’s factors-high wage levels, plaintiff-friendly courts in the Seattle area, rainfall that increases slip-and-fall exposure, and seismic risk-push premiums 24% above the national average.

Comparing Quotes Across Carriers

Your actual premium depends on location, industry classification, revenue, and loss history. The baseline $1M/$2M policy structure lets you compare quotes apples-to-apples across carriers and understand how your specific risk profile affects pricing. Understanding these cost drivers helps you move forward to the next critical step: determining whether standard limits actually fit your business’s unique exposure.

Finding Your Actual Coverage Limits

How Location, Industry, and Business Size Shape Your Needs

Location, industry, and business size determine what limits make sense for your operation. A tech consultant in Seattle faces entirely different exposure than a roofing contractor in Spokane, yet many business owners simply accept whatever their agent suggests without understanding why. The $1 million per occurrence and $2 million aggregate baseline works for some businesses but leaves others dangerously underprotected or overpaying for unnecessary coverage. Washington’s regulatory environment adds another layer: state licensing requirements set minimums at $200,000 public liability and $50,000 property damage for general contractors, while cannabis businesses require $1 million minimum with the state as additional insured. King County procurement rules push minimums far higher at $1 million per occurrence and $2 million aggregate for vendors seeking county contracts. Most landlords and commercial clients demand these higher limits regardless of state minimums, which means your actual floor is set by market expectations, not law.

Revenue and Employee Count Drive Your Exposure

Your revenue and employee count directly shape your exposure and therefore your limits. A solo consultant generating $150,000 annually faces different claim severity potential than a roofing crew with ten employees handling $2 million in annual contracts. MoneyGeek data shows solo businesses average $76 monthly while companies with 1–4 employees pay $153 monthly and those with 20–49 employees reach $3,059 monthly, reflecting genuine exposure differences. Right-sizing means matching your coverage limits to realistic worst-case scenarios: if your highest-value project is $500,000, a $1 million per occurrence limit provides reasonable cushion without excessive premium waste.

Real Settlement Values in Washington

Construction defect claims, water damage from installation errors, and serious injury settlements regularly hit $500,000 to $1 million in Washington, particularly in the Seattle area where verdicts run higher due to pure comparative negligence rules and no caps on non-economic damages. These figures aren’t theoretical-they reflect actual claim patterns that underwriters use to assess your risk category and price your coverage accordingly.

Comparing Quotes and Timing Your Reviews

Request detailed renewal quote breakdowns from at least two carriers showing rate per exposure unit and available discounts, then compare against the Washington Office of the Insurance Commissioner’s rate-change lookup tools to verify you’re not overpaying. Annual reviews 60–90 days before renewal catch exposure changes like new service lines or expanded employee counts that require limit adjustments. Bundling general liability with property, workers compensation, and commercial auto typically delivers 10–20% aggregate savings versus separate policies, which often makes higher limits more affordable than you’d expect.

Moving Forward With Confidence

Once you’ve matched your limits to your actual exposure and locked in competitive pricing through bundling, you’re positioned to identify and avoid the coverage gaps that trip up most business owners. The next chapter examines the mistakes that leave even well-intentioned operators exposed-and how to sidestep them entirely.

Common Mistakes Business Owners Make

Underinsuring Without Calculating Real Exposure

Most Washington business owners make one critical mistake before they even purchase a policy: they accept whatever limits their agent suggests or simply match what a competitor carries, without calculating their actual worst-case scenario. A $1 million per occurrence limit sounds substantial until a construction defect claim hits $1.2 million or a serious injury at your premises results in $800,000 in medical costs plus another $400,000 in pain and suffering damages. Washington’s pure comparative negligence system means plaintiffs recover even when partially at fault, and courts impose no cap on non-economic damages, which inflates settlement values beyond what many business owners anticipate.

The gap between what you think you’re protected against and what actually happens is where financial disaster lives. Businesses that discover mid-claim their limits are insufficient face a harsh reality: the policy is already in force, and adjusting coverage mid-term means starting over with underwriting delays and potential coverage disputes. Your worst-case scenario should drive your limit selection, not industry averages or competitor benchmarks.

Overlooking Industry-Specific Exposures

The second mistake compounds the first: overlooking industry-specific exposures that require tailored coverage beyond the standard baseline. A contractor handling $2 million in annual work might assume the state minimum of $200,000 public liability suffices, but King County procurement rules demand $1 million per occurrence and $2 million aggregate for any county contract, and most commercial clients simply refuse to work with contractors carrying less.

Enhanced services facilities under Washington law must carry $1 million per occurrence with $2 million aggregate minimum and must explicitly cover employee and volunteer acts, independent contractors, and products liability-gaps that invalidate otherwise adequate policies. A roofing operation that adds a new service line installing solar panels faces entirely different liability exposure than traditional roofing, yet many owners never notify their carrier or request coverage adjustments. Understanding what a Business Owners Policy covers helps you identify whether your current protection aligns with your industry’s actual demands.

Failing to Review Coverage Annually

The third mistake-failing to review coverage annually-lets exposure changes accumulate silently until a claim exposes the gaps. Documented safety programs can reduce premiums by 5–15% when carriers recognize measurable loss prevention, yet most businesses never implement the protocols that qualify for these discounts. Annual reviews 60–90 days before renewal catch exposure shifts like expanded employee counts, new service offerings, or increased contract values that require limit adjustments.

Request a detailed renewal quote breakdown showing rate per exposure unit and available discounts, then compare against at least one competing carrier to verify your renewal is competitive. The cost of an annual review-a single phone call with your agent-is negligible compared to the financial exposure you carry for the next twelve months. This simple discipline prevents the silent accumulation of unaddressed risk that transforms adequate coverage into inadequate protection.

Final Thoughts

General liability protection in Washington requires you to match your coverage limits to your actual business exposure, not industry averages or what competitors carry. The $1 million per occurrence and $2 million aggregate baseline works for many operations, but your specific location, industry classification, revenue, and employee count determine whether this standard structure protects you adequately or leaves gaps that could cost hundreds of thousands of dollars when a claim arrives. The three mistakes we’ve outlined-underinsuring without calculating worst-case scenarios, overlooking industry-specific exposures, and skipping annual coverage reviews-are entirely preventable.

Your next step is straightforward: gather your current policy documents and business details, then request detailed renewal quotes from at least two carriers showing rate breakdowns and available discounts. Compare those quotes against the Washington Office of the Insurance Commissioner’s rate-change lookup tools to verify competitive pricing, and consider bundling general liability with property, workers compensation, and commercial auto to capture the 10–20% aggregate savings that typically make higher limits more affordable than you’d expect. Implement documented safety protocols aligned with your industry’s standards-these can reduce premiums by 5–15% while genuinely lowering your claim risk.

We at FirstMark Insurance Group have spent 30 years helping Washington businesses navigate these decisions with clarity and confidence. Our team works with top insurance providers to present you with coverage choices that fit your requirements at the best available pricing, and we provide regular guidance throughout the year to keep your general liability protection WA aligned with your evolving business needs. Contact us to discuss your specific exposure and lock in the right coverage today.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation