A business owner’s policy cost varies wildly depending on your industry, location, and the coverage you select. Most business owners have no idea what they should actually be paying, which leads to either overpaying or being dangerously underinsured.

We at FirstMark Insurance Group help business owners understand their BOP pricing so they can budget accurately and get the protection they need without wasting money.

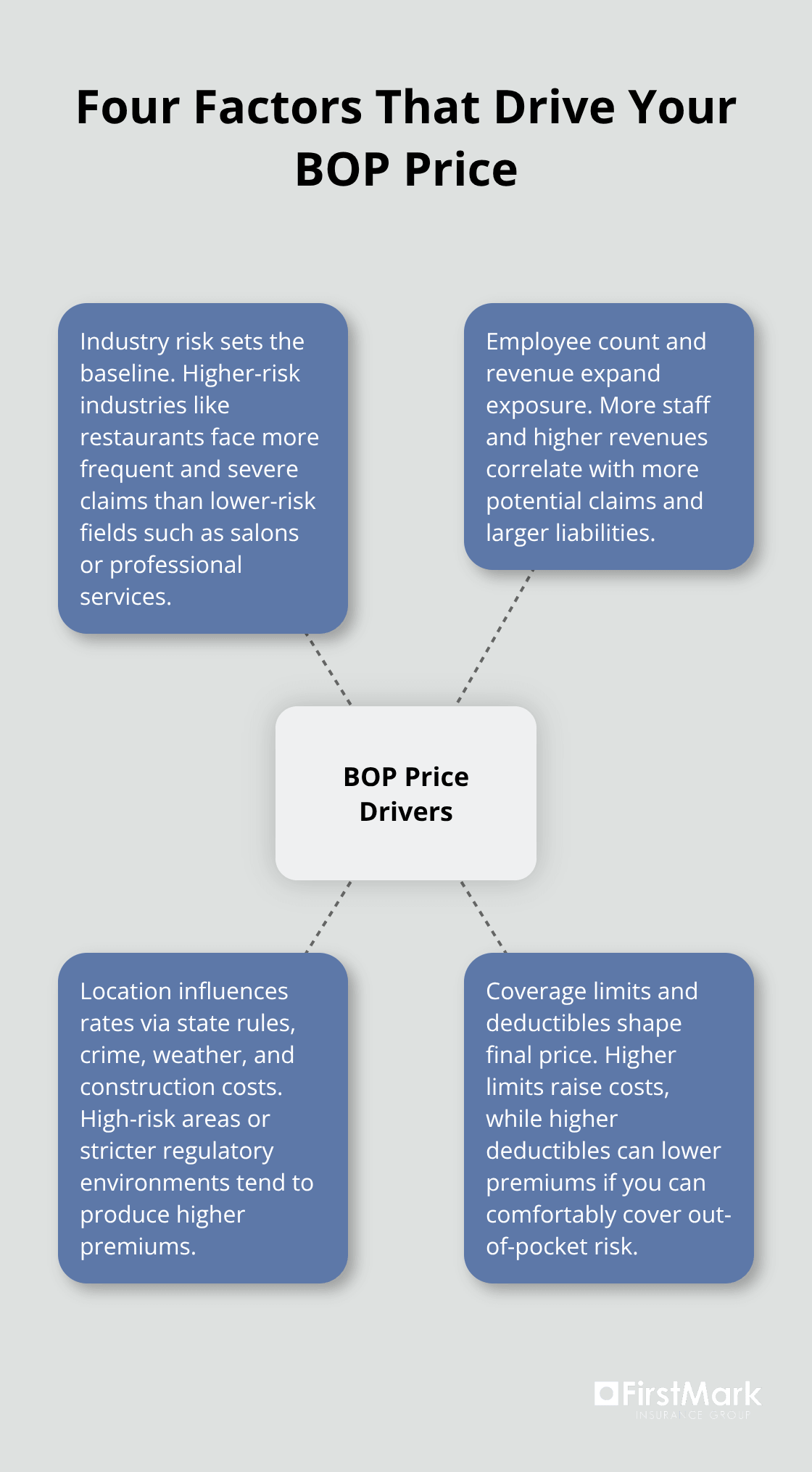

What Drives Your Business Owner’s Policy Price

Industry Risk Sets Your Baseline Cost

Your BOP premium hinges on four concrete factors that insurers scrutinize closely, and understanding each one helps you predict costs and find savings. Industry risk sits at the top of the list-a beauty salon pays far less than a restaurant, and that gap is massive. According to The Hartford’s data, beauty salons average around $113 per month while restaurants climb to $413 per month for similar coverage.

This difference reflects claim frequency and severity in each industry. Retail stores run about $152 monthly, manufacturers $115, and professional services like accounting firms stay low at roughly $85 per month. Your specific business type determines your baseline cost before anything else factors in.

Employee Count and Revenue Expand Your Exposure

Revenue and employee headcount directly impact your exposure. More employees mean more workers’ compensation risk, more payroll to protect, and statistically more claims. A solo consultant with zero staff pays substantially less than a business with five employees in the same industry. Insurers view each additional employee as increased liability exposure, so your staffing plan should influence your BOP budget.

Location Creates Significant Price Variations

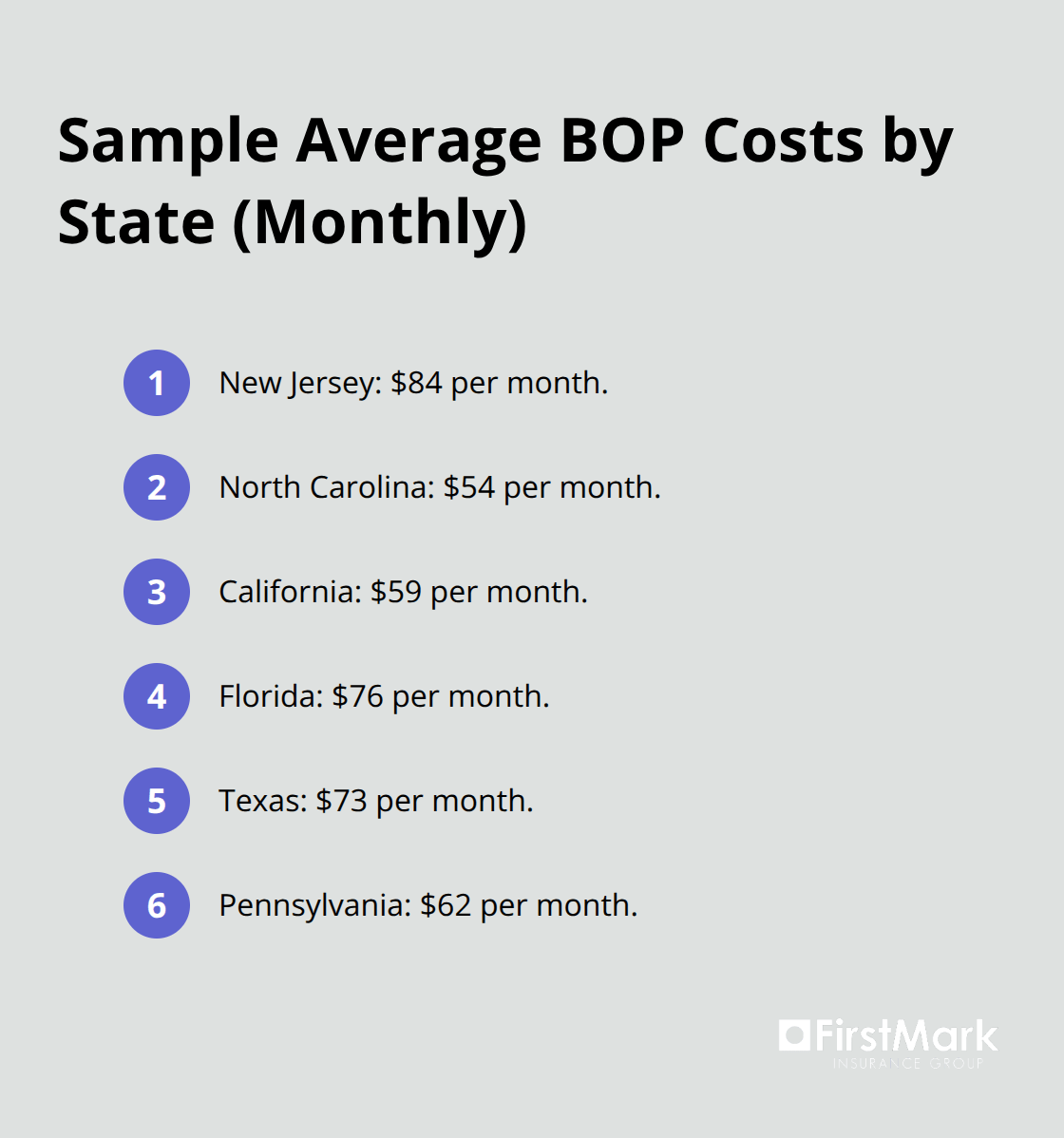

Location matters intensely because state regulations, crime rates, weather patterns, and construction costs vary wildly. New Jersey businesses pay roughly $84 monthly for a BOP while North Carolina averages $54-a 55% difference for the same coverage limits. California runs about $59 monthly, Florida $76, Texas $73, and Pennsylvania $62.

These state-level variations reflect both regulatory requirements and historical claim patterns. A business located in a flood-prone area or high-crime neighborhood will face higher premiums than one in a safer zone.

Coverage Limits and Deductibles Control Your Premium

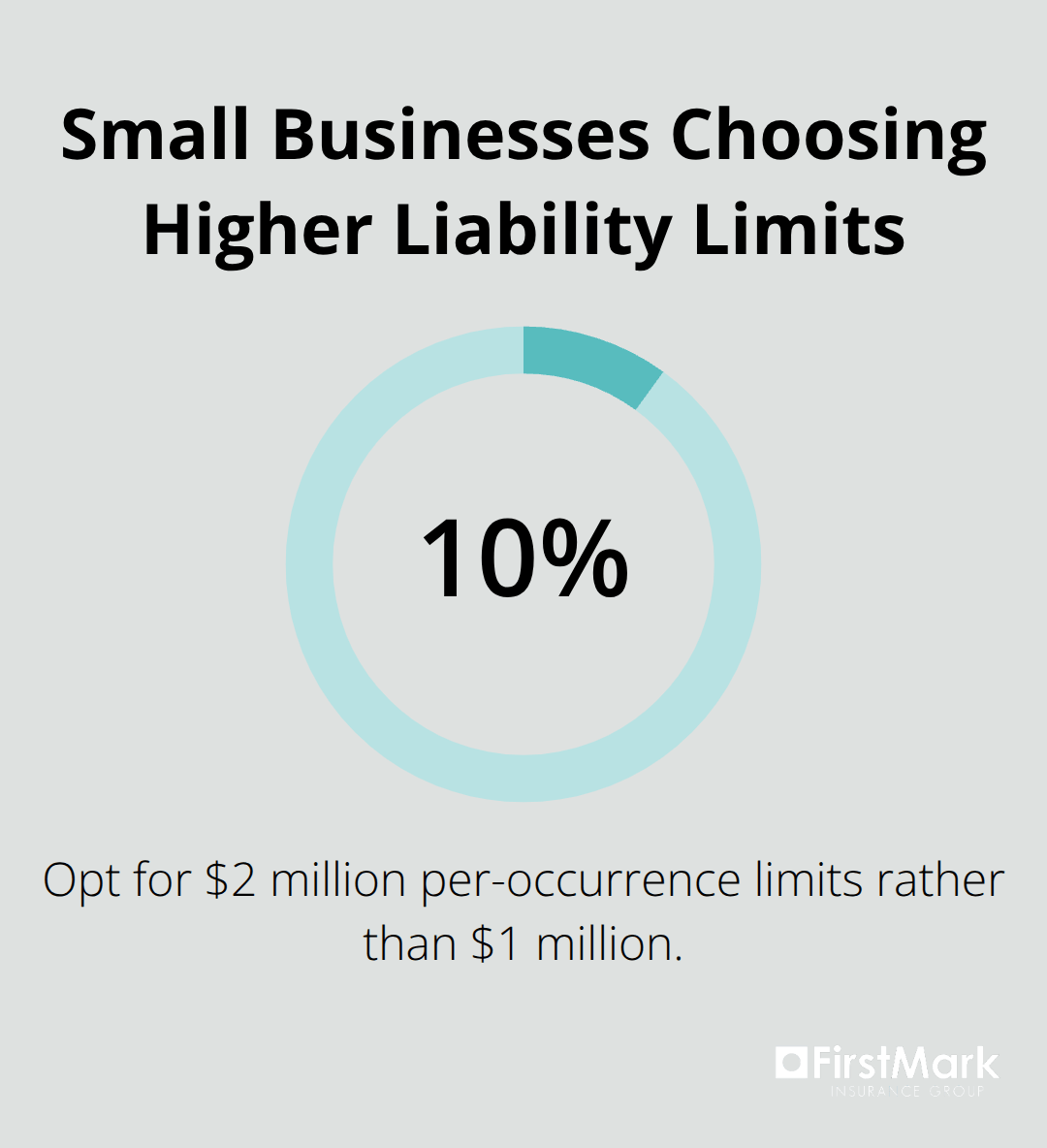

Coverage limits and deductibles represent your final lever. Most businesses choose $1 million per-occurrence with $2 million aggregate limits, which covers typical small business exposures, while about 10% opt for higher $2 million per-occurrence limits. A $500 deductible is standard, but raising it to $1,000 or $2,500 cuts your premium noticeably-though you must have cash reserves to cover that deductible if you file a claim.

Selecting replacement cost coverage instead of actual cash value also raises your premium because you receive more in a claim payout. Once you understand how these four factors shape your price, you can move forward with concrete strategies to reduce what you pay.

Average Business Owner’s Policy Costs by Industry

Retail and E-Commerce Businesses Face Customer-Related Risks

Retail stores run roughly $152 monthly according to The Hartford, while e-commerce operations typically land in the $150 to $180 monthly range depending on whether you maintain a physical storefront or operate online only. Physical retail locations command higher premiums due to customer injuries and property damage risks that online-only businesses avoid entirely. A customer slip-and-fall in your store or damage to merchandise on your premises creates genuine liability exposure that e-commerce operators simply don’t face. Your storefront location, foot traffic volume, and product type all influence where your premium lands within that range.

Professional Services Firms Pay the Lowest Premiums

Consultants, accountants, engineers, and architects consistently pay the least for Business Owner’s Policy coverage-around $85 to $107 monthly depending on your specific discipline. Your primary liability involves advice or service delivery rather than physical products or premises hazards. Engineers average $107 monthly while accountants stay near $85, reflecting slightly different risk profiles within the professional services category. This lower cost structure makes BOP an affordable protection layer for service-based businesses that operate primarily from offices.

Construction and Contracting Companies Handle Equipment and Materials

Construction and contracting operations should budget $115 to $200 monthly depending on whether you work from an office or maintain active job sites with equipment and materials. Manufacturers face similar exposure at roughly $115 monthly because both industries handle equipment, materials, and physical labor that create genuine liability. Job site hazards, equipment damage, and material theft all factor into underwriter assessments. Your specific trade-carpentry, electrical, plumbing, general contracting-influences your exact premium within that range.

Food Service Operations Command Premium Prices

Food service establishments must plan for $400 to $500 monthly minimum, and many pay significantly more if they serve alcohol or operate high-volume establishments. Restaurants average $413 monthly according to The Hartford-nearly five times what a consultant pays. This astronomical difference exists because restaurants combine high customer volume, food safety risks, liquor liability in many cases, and kitchen equipment hazards that generate frequent claims. A small café operates differently than a full-service restaurant with a bar, so your specific operation type matters tremendously.

Individual Risk Profiles Create Pricing Variations Within Industries

These figures assume standard $1 million per-occurrence coverage and $500 deductibles; your actual cost shifts based on your specific revenue, employee count, location, and claims history. Two restaurants in the same city might receive quotes differing by 30 percent or more based on their individual risk profiles and underwriting criteria. Getting quotes from multiple carriers matters tremendously because pricing varies between insurers even within the same industry. Your revenue level, staffing size, and prior claims history all influence where you land within your industry’s typical range, which means the next step involves understanding what specific cost drivers apply to your business.

How to Cut Your Business Owner’s Policy Premium

Bundle Coverage for Substantial Discounts

Lowering your BOP cost requires moving beyond passive acceptance of whatever quote you receive. The most effective strategy involves bundling business insurance coverages with other business insurance. General liability, commercial property, and business interruption all land in one policy, but adding workers’ compensation, commercial auto, or cyber liability to that same carrier typically yields discounts across your entire package. Bundling simplifies policy management by reducing paperwork and helping you keep track of fewer separate bills.

Request itemized quotes showing the bundled price versus purchasing each policy separately; the difference often exceeds several hundred dollars annually. This comparison reveals exactly what you save by consolidating coverage under one carrier rather than spreading policies across multiple insurers.

Implement Safety Programs That Reduce Claims

Your second lever involves implementing measurable safety programs that demonstrably reduce claim frequency. Installing water and moisture detectors, maintaining detailed safety procedures, conducting regular equipment inspections, and documenting employee safety training all signal to underwriters that you take risk management seriously. Carriers respond by holding premiums flat or even reducing them at renewal.

This approach beats hoping for rate cuts; you actively remove the behaviors and conditions that trigger claims. Underwriters want evidence that your business operates differently than it did twelve months prior, and that evidence justifies better pricing.

Raise Your Deductible to Lower Premiums

Your deductible choice represents the most direct control you have over premium costs. Raising your deductible from $500 to $1,000 typically cuts your premium by 10 to 15 percent, while jumping to $2,500 can reduce costs by 20 to 30 percent depending on your industry and location. The catch is mathematical: you must maintain sufficient cash reserves to cover that deductible without disrupting operations if a claim occurs.

A restaurant cannot absorb a $2,500 deductible from weekly cash flow, but a consulting firm with stable monthly revenue can comfortably set aside that amount. Calculate your actual deductible capacity before selecting a higher threshold.

Renegotiate at Renewal Time

Treat your annual policy renewal as a renegotiation event rather than a rubber-stamp exercise. Request a detailed renewal proposal that breaks down each cost component and explains any rate increases. Compare quotes from at least two other carriers; many businesses discover that switching to a new insurer costs less than renewing with their existing provider, though this requires weighing the administrative effort and potential new inspections against actual savings.

Document your risk management investments and present them during renewal conversations. Underwriters want concrete evidence that your business operates differently than it did twelve months prior, and that evidence justifies better pricing.

Final Thoughts

Understanding your business owner’s policy cost transforms how you approach insurance decisions. Industry, location, employee count, and coverage limits drive your premium, and the strategies we’ve covered-bundling policies, implementing safety programs, raising deductibles, and renegotiating at renewal-give you concrete control over what you pay. A 10 to 15 percent reduction from a higher deductible or documented safety program represents real money that stays in your business.

Working with an experienced insurance agent removes the overwhelm from this process. We at FirstMark Insurance Group have spent 30 years helping business owners find coverage that fits their actual needs at the best available pricing, and we explore offerings from top providers to present you with real choices tailored to your situation. Rather than accepting whatever quote arrives in your inbox, contact FirstMark Insurance Group to discuss your coverage needs with an agent who takes time to understand your business.

Regular policy reviews keep your coverage aligned with your actual business as it grows and changes. The coverage limits that protected you three years ago may no longer match your current revenue or property value, and an annual conversation with your agent catches these gaps before they become expensive problems during a claim.