Construction projects face real financial exposure when materials, equipment, and work-in-progress assets sit on-site. Builders risk insurance quotes reveal how much protection costs and what gaps might exist in your coverage.

At FirstMark Insurance Group, we’ve seen too many builders underestimate their exposure or overpay for inadequate policies. Getting accurate quotes from multiple providers isn’t just about price-it’s about understanding what you’re actually protected against as your project moves forward.

What Builders Risk Insurance Actually Covers

Builders risk insurance protects the physical assets on your construction site from the moment materials arrive until the project reaches completion. This coverage applies to buildings and structures under construction, foundations, fixtures, machinery, underground piping, electrical work, temporary structures, and building materials stored on-site. It also extends to materials in transit to your project and covers debris removal costs if damage occurs. The policy activates when construction begins and terminates shortly after completion or when the building becomes operational.

The Coverage Gap Standard Policies Leave Behind

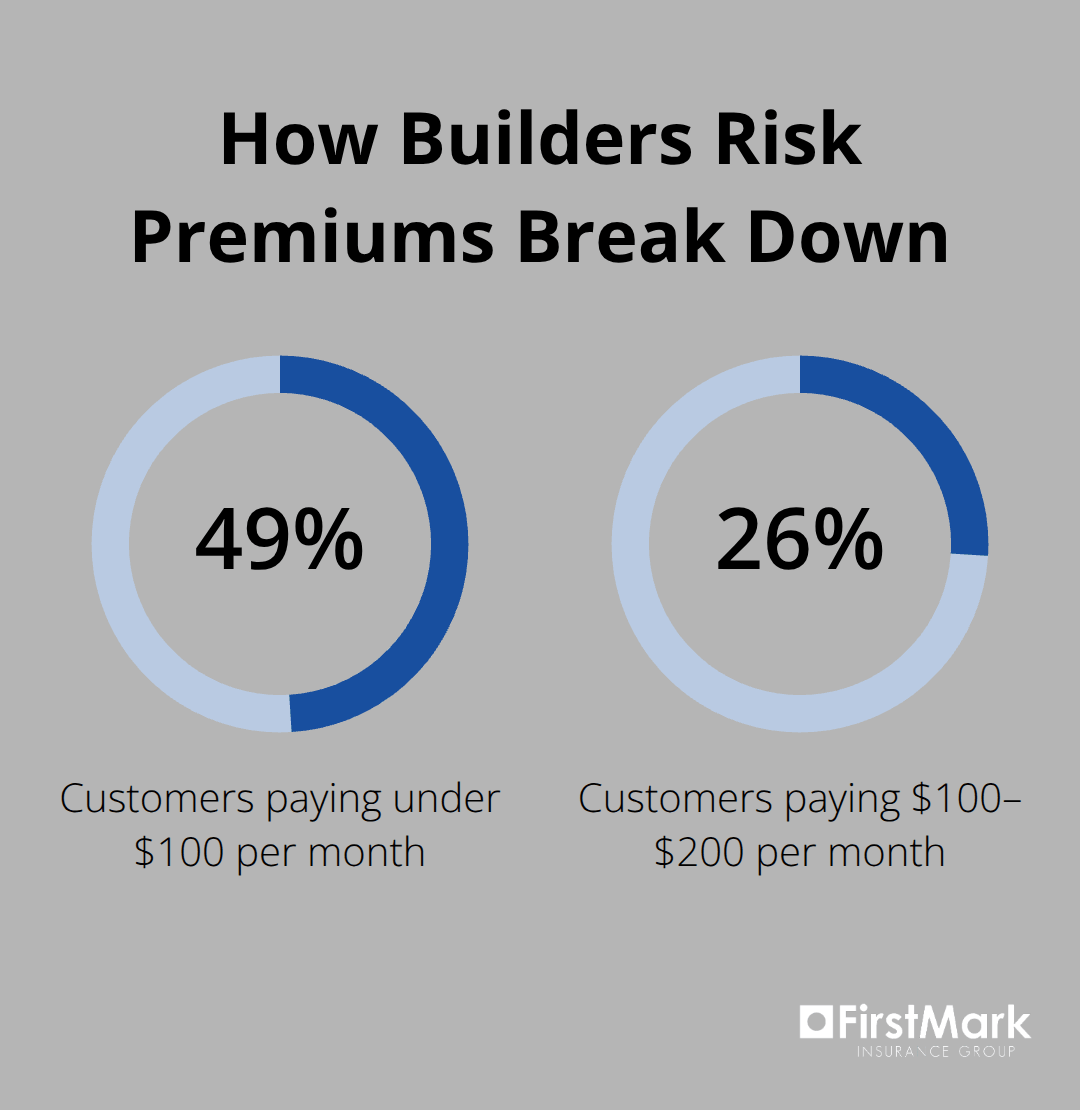

Standard homeowners or commercial property policies explicitly exclude losses during construction, which is why builders risk exists as a separate product. Without this coverage, you carry the full financial burden of fire, lightning, windstorm, hail, explosion, theft, and vandalism-perils that occur regularly on active job sites. According to Insureon’s analysis of their customer base, the average builders risk premium runs about $105 per month, with approximately 49% of customers paying less than $100 monthly and 26% paying between $100 and $200. Premiums typically fall between 1% and 4% of your total completed project value, making the cost relatively modest compared to the exposure you’re protecting.

Why General Liability Falls Short

Contractors frequently assume their general liability policy covers construction-related property damage, but this assumption costs them significantly. General liability insurance protects against bodily injury and property damage claims you cause to third parties-it does not cover damage to construction materials and work-in-progress assets on your own project. If wind damages materials stacked on your site or theft occurs at night, general liability will deny the claim entirely.

The Distinct Role Builders Risk Plays

Builders risk fills this specific gap by focusing exclusively on your own property during the construction phase. The two policies operate independently and serve fundamentally different purposes. You need both: general liability shields you from lawsuits when someone gets hurt or you damage someone else’s property, while builders risk protects your own materials and work. Many contracts now require proof of both policies before work can commence, particularly on government projects or FHA-financed construction (this dual-policy requirement reflects how construction lenders and owners understand real risk exposure on active sites).

Understanding what each policy covers sets the foundation for requesting accurate quotes. The next section walks through the specific information you’ll need to provide when contacting insurers for quotes.

Getting Accurate Quotes for Builders Risk

Provide the Right Project Details

Requesting builders risk quotes requires precision on your end because insurers base pricing on specific project details, and incomplete information leads to inflated estimates or coverage gaps that surface later. You must document your total completed project value-this is the hard cost to rebuild, excluding land value. You’ll also need to specify your construction type, whether the project is new ground-up construction or a renovation, the square footage involved, and your location down to the zip code.

Location matters enormously in builders risk pricing. A $300,000 new home near a fire station can quote under $1,000, while the identical project more than five miles away in a brush area runs 20-30% higher. Include your years of construction experience and any losses in the past five years-this history directly influences underwriting decisions and pricing. If you’ve had no claims, state this explicitly to your underwriter.

Compare Carriers, Not Just Prices

When you request quotes from multiple carriers, you’re not hunting for the lowest price; you’re identifying which insurer understands your specific project risk. Request quotes from at least three carriers to establish a meaningful comparison. Providers quoting significantly lower than others often signal they’ve undervalued your project scope or excluded important coverages like debris removal or materials in transit.

Spot Red Flags in Quote Details

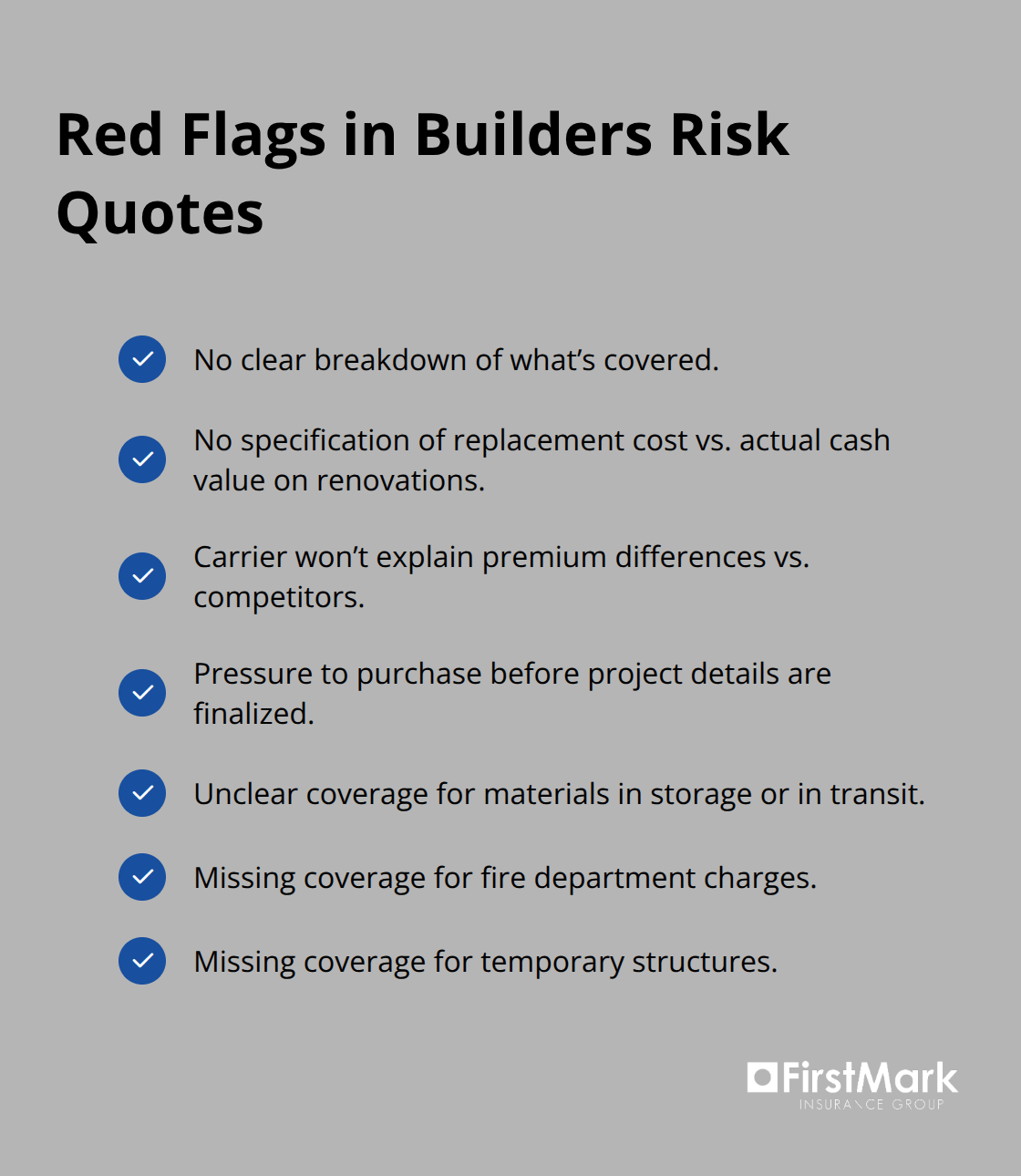

Several warning signs indicate an insurer hasn’t properly evaluated your project. Quotes without a clear breakdown of what’s covered, policies that don’t specify replacement cost versus actual cash value for existing structures on renovation projects, or carriers unwilling to explain why their premium differs from competitors all warrant caution.

Avoid providers who pressure you into purchasing before project details are finalized or who won’t clarify whether your materials in storage or transit are covered. Verify that any quote includes coverage for fire department charges and temporary structures, as these are standard but occasionally omitted by less experienced underwriters.

Evaluate Beyond the Monthly Premium

Once you’ve collected three solid quotes, compare not just the monthly premium but the deductible amount, policy duration (six versus twelve months), and which optional coverages are included versus available as add-ons. This comparison reveals which carrier aligns with your project timeline and risk tolerance. The lowest quote often masks higher deductibles or shorter coverage periods that create exposure gaps. Understanding these details positions you to make an informed decision about which provider offers the protection your project actually needs.

With accurate quotes in hand, you can now examine the specific factors that drive pricing differences across carriers-and why two insurers may quote the same project at substantially different rates.

What Actually Drives Your Builders Risk Premium

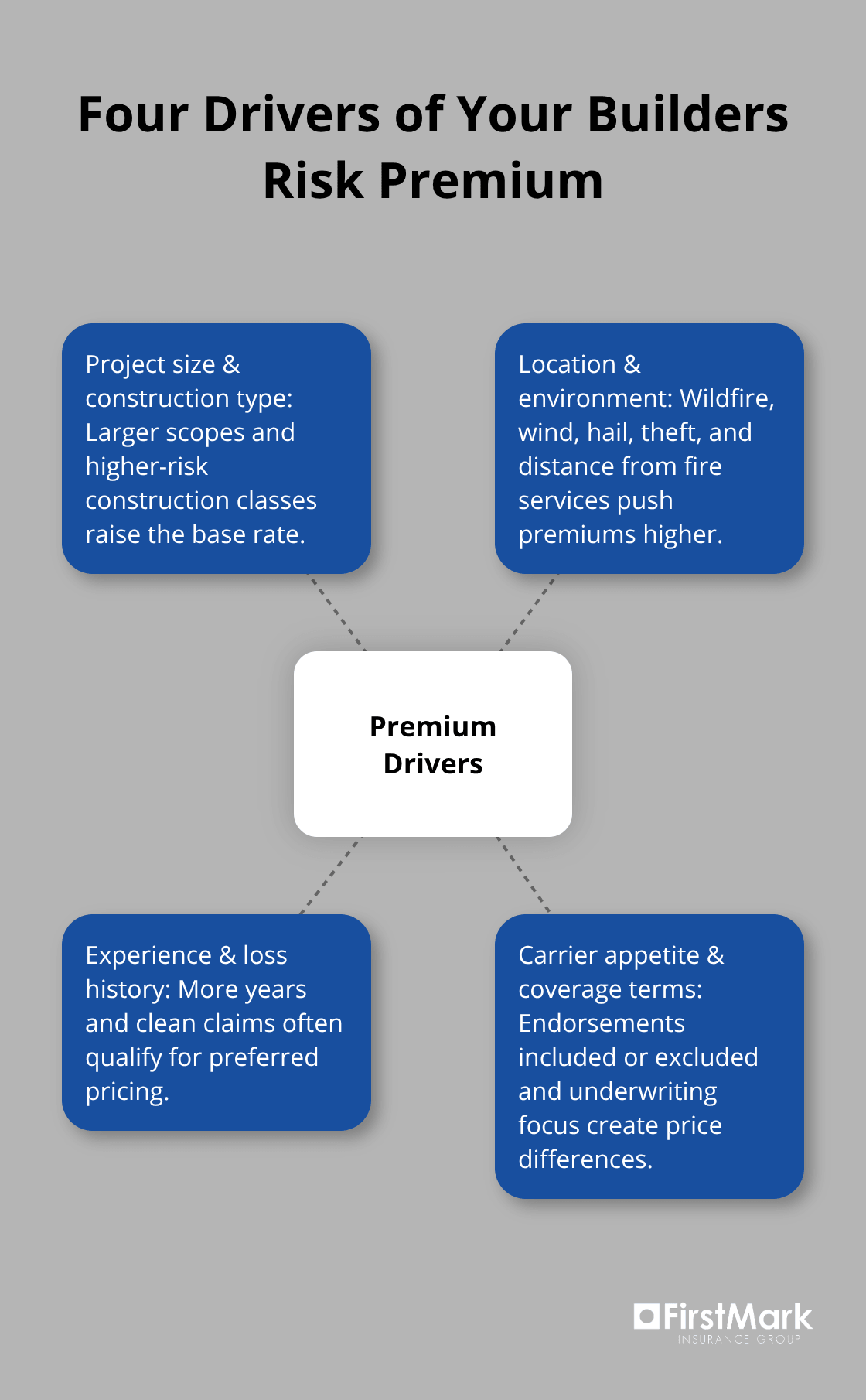

Your builders risk premium reflects four distinct cost drivers that insurers weight differently, and understanding how each one influences your quote prevents you from overpaying or selecting inadequate coverage.

Project Size and Construction Type Set Your Base Rate

Project size and construction type form the foundation of your premium calculation. Insureon’s data shows that premiums typically range from 1% to 4% of your total completed project value, meaning a $500,000 project might carry an annual premium between $5,000 and $20,000 depending on construction specifics.

New ground-up construction quotes lower upfront because early phases carry minimal risk exposure-materials haven’t accumulated on-site yet and structural work hasn’t begun. Renovation projects cost substantially more to insure because you protect both the new work costs and the existing structure’s rebuild value, which underwriters typically value at actual cash value rather than replacement cost.

A cosmetic kitchen remodel quotes far lower than a project involving load-bearing wall removal or adding a second story, since structural changes dramatically increase risk classification. Wood-frame construction consistently commands higher premiums than concrete or masonry fire-resistive buildings because wood presents greater exposure to fire loss. If your project uses fire-resistive materials and superior construction methods, explicitly document these details when requesting quotes-underwriters price these favorably and some carriers offer meaningful discounts for quality construction practices.

Location and Environmental Risk Factors Create Significant Premium Swings

Location determines whether your premium stays reasonable or climbs significantly beyond base rates. A $300,000 new home near a fire station with good hydrant access costs under $1,000 annually according to industry benchmarks, while the identical project more than five miles away in a brush area runs 20–30% higher due to fire response delays and wildfire exposure. Coastal properties, areas prone to hail or tornadoes, and regions with higher theft and vandalism risks all trigger premium increases because loss frequency data supports higher pricing.

Remote locations with limited site access cost more because emergency response times lengthen and material security becomes harder to maintain. Your proximity to fire protection resources directly influences what carriers will charge. Areas with strong fire department infrastructure and accessible hydrants receive favorable rates, while isolated sites face substantial premiums.

Your Experience and Loss History Shape Underwriting Decisions

Your years of construction experience and loss history directly influence underwriting appetite and pricing. Contractors with five or more years of experience and zero claims in the past five years qualify for preferred rates at most carriers. First-time builders or those with prior losses face higher premiums or additional underwriting requirements-some insurers require projects over 30% complete to undergo detailed underwriting review before binding coverage, which can delay your quote process.

When you request quotes, lead with your strongest qualifications: clean loss history, established track record, and proximity to fire protection resources. Carriers weight these factors differently, which explains why shopping three or more providers often reveals 20–40% premium variation on identical projects.

Comparing Quotes Reveals True Value Differences

The carrier that quotes lowest doesn’t necessarily offer the best value if they’ve underestimated your project scope or excluded critical endorsements like expediting costs or materials in transit coverage. Request detailed breakdowns from each provider to understand what accounts for premium differences. One insurer may price aggressively on new construction but charge substantially more for renovations, while another carrier shows the opposite pattern based on their underwriting appetite and claims experience.

Final Thoughts

Selecting builders risk insurance comes down to matching your project’s specific exposure with a carrier that prices fairly and responds when claims arise. The builders risk insurance quotes you’ve gathered reveal not just cost differences but how each insurer evaluates your risk profile. A carrier quoting significantly lower may have underestimated your project scope, while one quoting higher might be pricing in superior claims service or broader coverage terms.

Your next step involves requesting certificates of insurance from your preferred carrier and confirming coverage activates before materials arrive on-site. Timing matters critically here-if your policy isn’t in force when construction begins, pre-existing work typically won’t be covered, leaving you exposed to losses that could have been prevented. Coordinate with your general contractor, subcontractors, and project lender to confirm everyone understands who holds the policy and what it covers.

As your project progresses, your coverage needs may shift. Change orders that expand scope, material substitutions that increase project value, or timeline extensions all warrant reviewing your policy limits and duration. Contact FirstMark Insurance Group to discuss your builders risk needs and receive quotes from carriers experienced in your project type and location.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation