A business umbrella policy fills the gap when your standard liability coverage runs out. One lawsuit or major claim can wipe out years of profits and put your assets at risk.

At FirstMark Insurance Group, we help business owners understand why umbrella protection matters. This guide walks you through what’s covered, when you need it, and how to pick the right limits for your company.

What an Umbrella Policy Actually Covers

An umbrella policy activates only after your underlying liability coverage maxes out. If a customer is injured on your property and sues for $2 million, but your general liability policy caps at $1 million, your umbrella fills that $1 million gap. This is the core function: excess protection across multiple policies at once. Unlike excess liability, which increases the limit on a single policy, umbrella policy covers your general liability, commercial auto, and employer’s liability simultaneously. Hartford reports that average commercial liability claims reach about $54,000, but claims frequently exceed $1 million. That gap between standard coverage and catastrophic claims is exactly where umbrella protection works.

Defense Costs and Legal Expenses

One of the most expensive parts of any lawsuit isn’t the settlement itself-it’s defending against the claim. Attorney fees, expert witness costs, court expenses, and investigation fees pile up fast. A robust umbrella policy covers these defense costs, so you don’t drain your operating budget while fighting a lawsuit. Defense costs can run into hundreds of thousands of dollars before a case even reaches settlement. Your umbrella doesn’t just pay damages; it pays the legal machinery required to resolve the claim. Without this layer, you remain personally responsible for mounting legal bills while waiting for your primary coverage to potentially kick in.

What Actually Stays Excluded

Umbrella policies have hard boundaries. They don’t cover professional liability claims, workers’ compensation injuries, intentional misconduct, or damage to your own business property. They also exclude claims that arise from violations of employment law or contractual disputes unrelated to bodily injury or property damage. Understanding these exclusions prevents the dangerous assumption that umbrella covers everything beyond your primary limits. Some states impose additional exclusions, so your specific policy language matters. This is why you should review actual policy documents rather than rely on general descriptions. If your business operates in California or New York (where liability claims run about 40 percent higher than national averages), exclusions become even more important to understand before a claim arises.

State-Specific Coverage Variations

Coverage terms and exclusions shift across state lines. What your umbrella covers in one state may not apply in another, and some states restrict certain types of claims or impose unique requirements. Your policy documents spell out these state-specific provisions, and they directly affect what protection you actually have. This variation is why a one-size-fits-all approach fails for umbrella planning. You need to know your state’s rules before you face a claim.

Moving to Coverage Limits

The amount of umbrella protection you purchase matters as much as what it covers. Your business size, industry, assets, and contractual obligations all shape how much coverage makes sense for your situation.

When Your Business Really Needs Umbrella Protection

Most business owners wait too long to buy umbrella insurance. They assume their general liability policy is enough until a single lawsuit threatens everything they’ve built. The truth is simpler: if your business has assets worth protecting, you need umbrella coverage now.

Companies with total assets over $1 million should target at least $2 million in umbrella limits according to industry standards. Small businesses often dismiss umbrella as unnecessary overhead, but more than 40 percent of small businesses will experience a claim in the next 10 years. That gap between what your standard policy covers and what catastrophic claims actually cost exposes most business owners. Revenue matters too. A tech firm generating $5 million annually faces different liability exposure than a $500,000 service business, and settlements often scale with company size and revenue.

California and New York businesses face an additional pressure: liability claims run about 40 percent higher in these states than national averages, making umbrella protection there nearly mandatory rather than optional.

Industry determines your real exposure

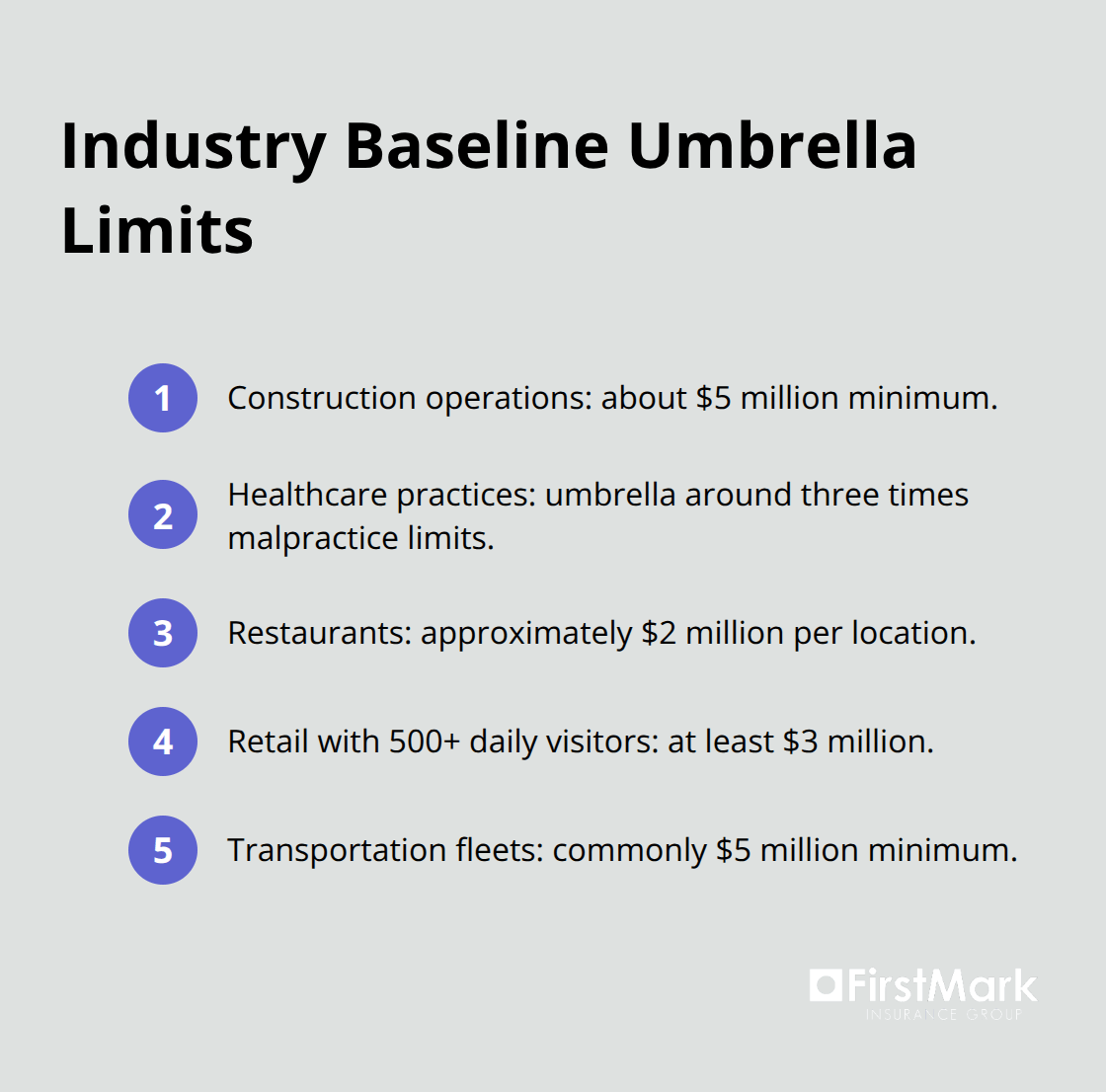

Construction companies, healthcare providers, transportation fleets, and restaurants face fundamentally different liability risks than software consultants or accounting firms. Construction operations require coverage equal to about $5 million minimum due to on-site injury potential and property damage exposure. Healthcare practices typically need umbrella limits around three times their malpractice coverage limits.

Restaurants should carry approximately $2 million in umbrella protection per location because of constant customer interaction and food-handling risks. Retail stores with 500 or more daily visitors need a minimum of $3 million in umbrella limits. Transportation fleets commonly face $5 million minimum requirements from clients and insurance underwriters. Your industry determines baseline protection needs, not guesswork or generic recommendations.

If your business involves frequent customer contact, on-site work at client locations, or handling of other people’s property, your umbrella need increases substantially. Contractual obligations amplify this requirement further.

Contracts and clients often dictate your limits

Vendors and clients frequently demand specific umbrella coverage before they’ll do business with you. Most contract requirements fall in the $2 million to $5 million range, though major corporate clients sometimes require $10 million or more. You cannot negotiate around these requirements if you want the work.

Reviewing every vendor contract, client agreement, and partnership arrangement reveals your true minimum umbrella obligation. If you operate in regulated industries like construction or healthcare, regulatory mandates may also specify umbrella minimums. Asset protection becomes the final consideration. A judgment against your business can seize company assets, personal guarantees, and future revenue streams.

How coverage limits protect your financial future

Umbrella insurance sits between your business and financial ruin when a catastrophic claim arrives. The right limit depends on three factors: your total assets, your annual revenue, and your industry’s typical claim severity. A $2 million umbrella protects a small business with modest assets, but a growing company with $10 million in assets and $8 million in annual revenue needs substantially more protection.

Your next step involves evaluating the specific coverage options available and comparing how different policies handle the gaps in your current protection.

How to Choose the Right Umbrella Policy for Your Business

Start With Your Underlying Coverage

Your umbrella policy depends entirely on underlying coverage that already exists. General liability, commercial auto, and employer’s liability policies must be in place before umbrella activates. Most insurers require underlying coverage of at least $1 million per occurrence to qualify for umbrella protection. If your current limits fall below this threshold, raising them first costs less than you might expect and strengthens your overall protection.

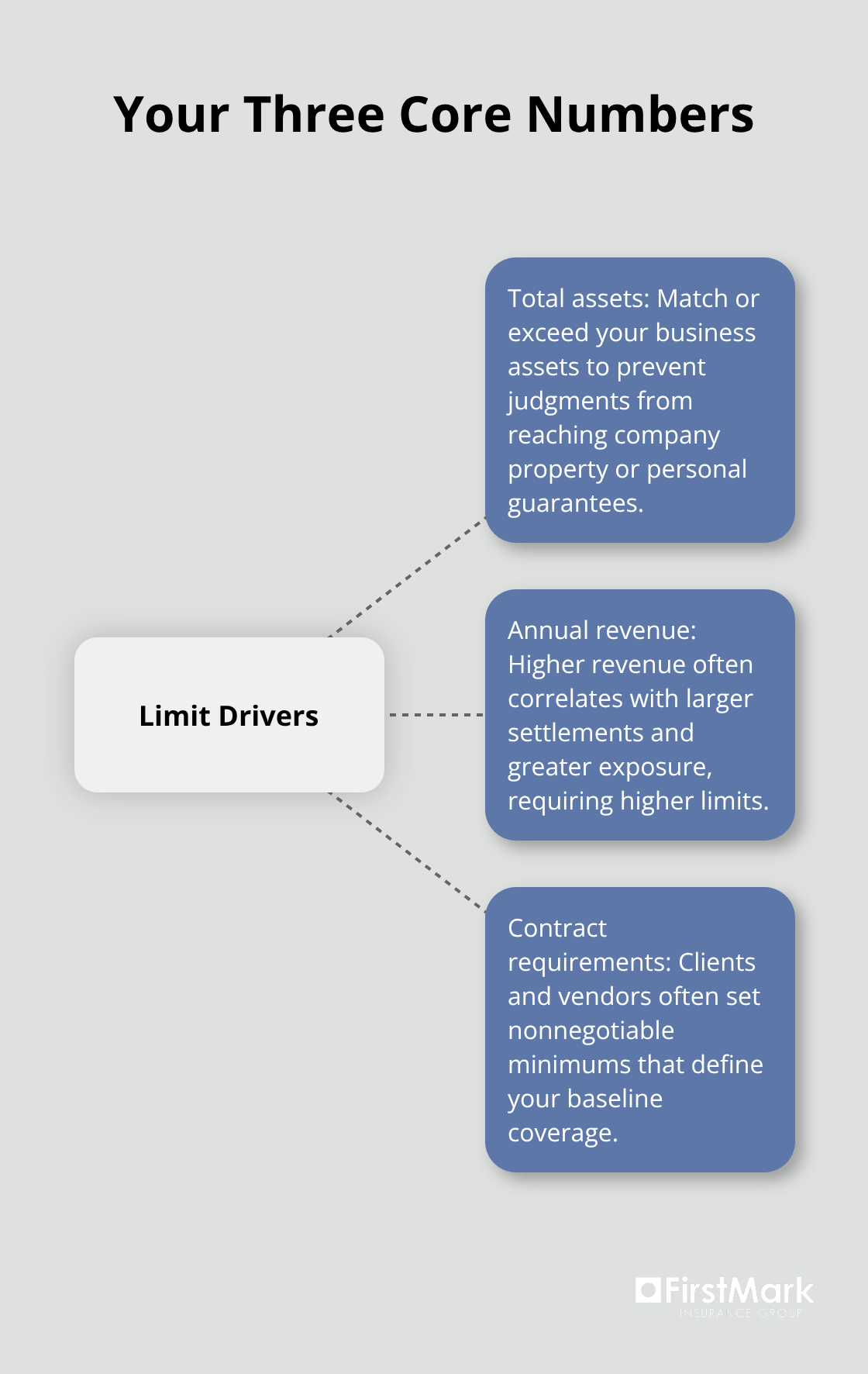

Identify Your Three Core Numbers

Determine your actual umbrella need by listing three concrete items: your total business assets, your annual revenue, and every contractual requirement from clients and vendors. A business with $3 million in assets and $2 million annual revenue faces different exposure than one with $10 million in assets and $5 million revenue. Contract requirements often specify exact umbrella minimums, so these aren’t negotiable-they’re baseline obligations you must meet. Once you know what you need, you can move forward with confidence rather than guessing at appropriate limits.

Compare Quotes From Multiple Carriers

Get quotes from at least three different carriers because pricing varies dramatically based on your industry, location, and loss history. A $1 million umbrella policy typically costs around $75 per month according to industry data, with roughly $40 additional per month for each additional $1 million in coverage. This baseline shifts upward in high-risk states like California and New York, where claims run 40 percent higher than national averages. Geography matters more than most business owners realize when comparing quotes.

Examine Policy Language, Not Just Price

Two policies with identical limits can provide vastly different protection based on what they exclude and how they handle defense costs. Examine whether the policy covers defense costs inside or outside your umbrella limit-this distinction can cost hundreds of thousands of dollars in a major claim. Ask each carrier how they handle claims that touch multiple underlying policies and whether they coordinate seamlessly or create coverage gaps. Some insurers offer shorter response times and more responsive claim handling, which matters enormously when your business faces a lawsuit.

Request sample policies from each carrier so you can compare exclusions directly rather than relying on summaries. Pay particular attention to how each policy defines covered liability, since state-specific variations can exclude claims that matter to your business. Don’t select based on cost alone-the cheapest option often excludes critical coverage your industry requires.

Verify Coverage Meets Your Obligations

Once you’ve narrowed to two or three finalists, verify that each policy meets your contractual obligations and covers the liability exposures specific to your operations. Right protection provides extended coverage beyond the limits of primary liability policies. Each policy should align with both your industry’s standard requirements and the unique demands of your client relationships.

Final Thoughts

Umbrella insurance protects your business when standard liability coverage falls short. A single lawsuit can exceed your primary policy limits by hundreds of thousands of dollars, leaving your personal assets and company finances exposed. The businesses that operate with confidence are the ones that understand their exposure and act before a claim arrives.

Your assessment starts with three concrete numbers: total assets, annual revenue, and contractual coverage requirements from clients and vendors. These numbers determine your baseline umbrella need, not industry averages or generic recommendations. A business with $3 million in assets needs different protection than one with $10 million, and your contracts often dictate exact minimums you must meet to keep working with key clients.

Once you know what you need, compare quotes from multiple carriers because pricing varies dramatically by location, industry, and loss history. A $1 million umbrella typically costs around $75 per month, with roughly $40 additional per month for each additional $1 million (California and New York businesses pay more due to higher claim frequencies). Examine policy language, defense cost provisions, and how each carrier handles claims touching multiple underlying policies rather than selecting based on price alone. Contact us at FirstMark Insurance Group to discuss your business umbrella policy needs and get quotes from carriers that understand your industry.