Construction projects face real financial exposure from the moment work begins. At FirstMark Insurance Group, we understand that builders risk insurance for contractors isn’t optional-it’s the foundation of responsible project management.

Your team, equipment, and materials need protection against weather, theft, and liability claims. This guide walks you through the coverage types that matter, how to select the right policy, and strategies to prevent costly claims.

What Builder Risk Insurance Actually Covers

Property Damage Protection on Construction Projects

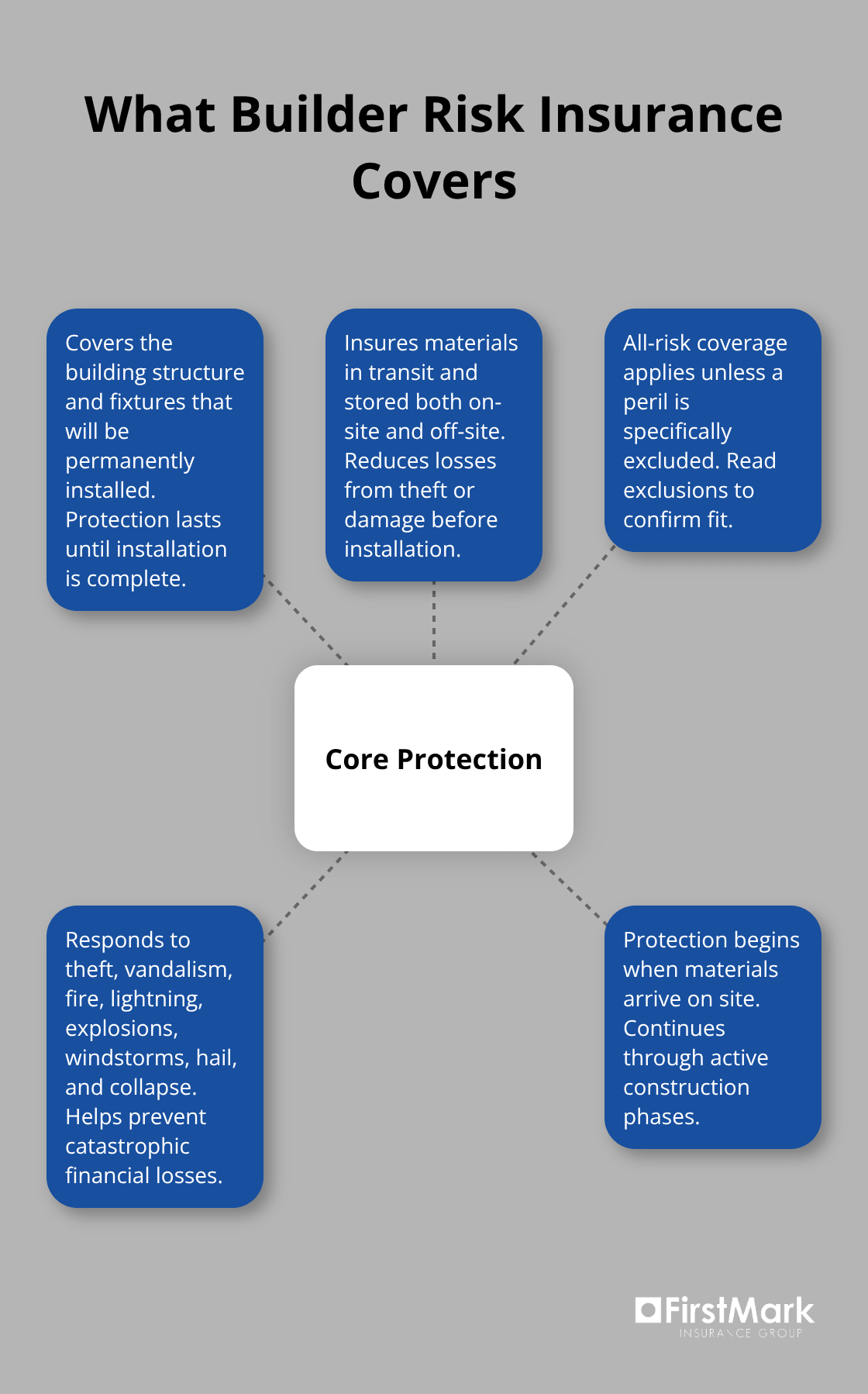

Builder risk insurance protects the physical assets on your construction project from the moment materials arrive until installation is complete. The coverage operates on an all-risk basis, meaning it protects against most perils unless specifically excluded in your policy.

Property damage protection covers the building structure, materials in transit, stored materials both on-site and off-site, and fixtures that will be permanently installed. This extends to theft, vandalism, fire, lightning, explosions, windstorms, hail, and collapse. When the builders risk market reached 5.36 billion dollars last year, it reflected growing recognition among contractors that this coverage prevents catastrophic financial losses.

A 250,000 dollar residential project and a 2.5 million dollar commercial building carry vastly different exposure levels, and your policy limits should match your anticipated total project costs to avoid underinsurance. Weather-related damage represents one of the most frequent claims contractors face. Water intrusion from storms, wind damage during framing, and hail damage to materials cost contractors millions annually. Many standard policies exclude water damage or limit coverage for moisture intrusion, which is why you need to verify whether your policy includes water damage endorsements and what specific perils trigger coverage. Debris removal typically comes with minimal premium increases but covers cleanup costs after a damaging event, protecting your project timeline and budget.

Equipment, Tools, and Liability Boundaries

Equipment and tools on job sites face constant exposure to theft and damage. Your builder risk policy should cover contractor equipment, tools, and machinery stored on-site or in temporary structures, though some carriers impose sublimits on high-value items. Liability coverage operates separately from builder risk insurance and requires its own policy. Builder risk does not cover third-party bodily injury or property damage to neighboring structures, which means you absolutely need a general liability policy alongside your builder risk coverage.

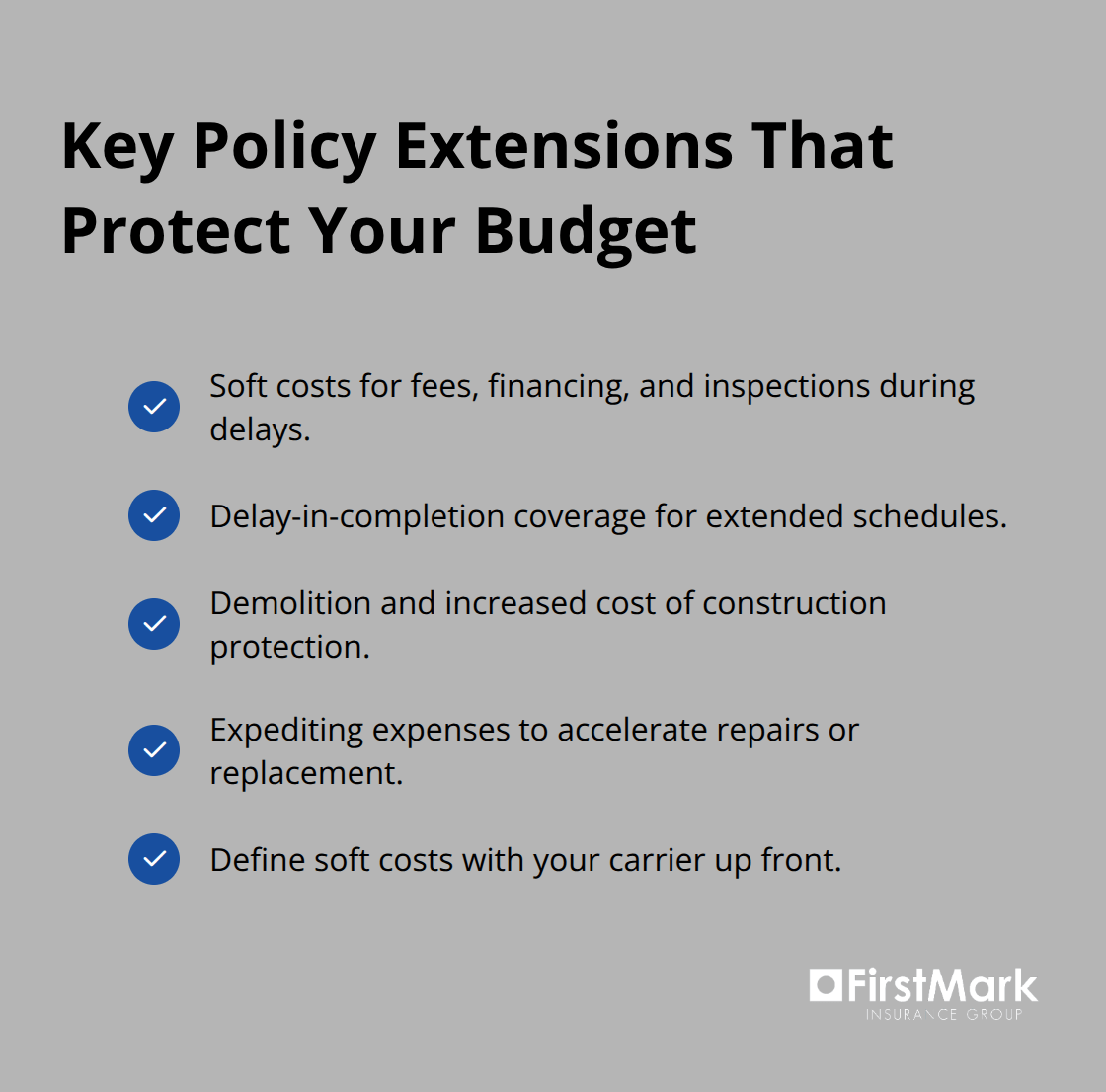

Extensions That Protect Your Project Timeline and Budget

Soft costs extensions address non-material expenses like design fees, financing costs, and inspections that accumulate when construction delays occur, and delay-in-completion extensions can cover costs if substantial completion extends beyond schedule. Demolition and increased cost of construction extensions help when you must demolish damaged work and rebuild under stricter building codes or regulations that increase construction costs.

Expediting expenses extensions cover the costs to accelerate repairs or replacement after a loss, though limits typically cap at a percentage of the hard costs. Your policy should specifically define what constitutes soft costs with your carrier, as definitions vary widely and affect claim outcomes.

Subcontractor Risk and Underwriting Transparency

Subcontractor default insurance remains a critical risk transfer tool, with mechanical, electrical, and plumbing contractors representing the most frequent sources of defaults in 2025. Contractors who implement standardized risk controls and conduct thorough financial evaluations of subcontractors secure more favorable underwriting terms from carriers. Data-driven underwriting now evaluates construction timelines, material sourcing, weather patterns, and subcontractor reliability to price risk accurately. Transparent project information strengthens your negotiating position when securing coverage, and carriers reward contractors who share detailed subcontractor financial data and project schedules with better terms and faster underwriting decisions.

Selecting the Right Policy for Your Project

Match Policy Terms to Your Project Reality

Choosing builder risk insurance requires matching policy terms to your specific project reality, not settling for generic coverage that leaves gaps when claims occur. Project scope determines everything about your policy structure, from coverage limits to endorsement selections. A $250,000 residential remodel needs fundamentally different protection than a $2.5 million commercial build, and carriers structure their underwriting accordingly. Duration matters equally-a three-month renovation carries different weather exposure than an eighteen-month infrastructure project.

Your policy start date should align precisely with when you take possession of materials, not when construction officially breaks ground, since coverage gaps between material delivery and active construction have triggered countless disputes. Document your anticipated project completion date during underwriting because policies renew based on duration, and extensions cost less upfront than purchasing new policies mid-project when circumstances change.

Identify and Address Coverage Gaps

Exclusions and limitations separate adequate coverage from false security, which is why reviewing the actual policy language matters more than carrier marketing materials. Water intrusion exclusions remain the single largest gap in standard builders risk policies, yet water damage from storms and construction defects cost contractors millions annually. Ask your carrier explicitly whether water damage receives coverage during the framing phase, whether moisture intrusion from incomplete roofing or windows triggers coverage, and what sublimits apply to water-related claims.

Settling, cracking, and shrinkage exclusions typically exempt normal building movement, but verify that accidental damage from unexpected events remains covered. Earth movement exclusions can be negotiated downward in many cases, particularly if you work in stable soil conditions. Mold and pollution exclusions are common; consider adding separate Contractor’s Pollution Liability coverage to address these gaps.

Compare Quotes Based on Coverage Scope

Compare quotes from multiple carriers not by price alone, but by coverage scope-a lower premium with excluded water damage costs exponentially more when a storm hits during framing than a higher-premium policy with comprehensive water protection. Request detailed endorsement options from each carrier and confirm that soft costs extensions, demolition coverage, and expediting expenses align with your project timeline and budget constraints.

The carriers you select should demonstrate financial strength and a track record of responsive claims handling. Your broker should help you evaluate each proposal against your specific project exposures rather than simply presenting the lowest bid. This evaluation process directly influences whether your coverage protects your project when damage occurs or leaves you exposed to uninsured losses.

Prepare Accurate Project Information for Underwriting

Transparent project information strengthens your negotiating position when securing coverage. Carriers reward contractors who share detailed subcontractor financial data, material sourcing plans, and realistic project schedules with better terms and faster underwriting decisions. Data-driven underwriting now evaluates construction timelines, material sourcing, weather patterns, and subcontractor reliability to price risk accurately. When you provide complete information upfront, underwriters can structure policies that actually fit your project rather than applying generic terms that may not address your specific exposures.

The underwriting process itself becomes a risk management conversation-one where your transparency about project challenges (weather exposure, complex MEP scopes, aggressive timelines) allows carriers to recommend appropriate endorsements and coverage limits. This collaborative approach prevents the costly scenario where you discover coverage gaps only after a loss occurs.

Common Claims and How to Prevent Them

Weather Damage Requires Active Mitigation, Not Hope

Weather inflicts the highest damage costs on construction projects, with water intrusion accounting for millions in annual claims across the industry. Wind damage during framing phases, hail striking materials before installation, and storm-driven water penetration through incomplete building envelopes represent the most frequent weather-related losses contractors face. The solution isn’t hoping for good weather-it’s institutionalizing water-mitigation protocols across every project.

Install backup power solutions to maintain temporary drainage systems during storms, establish clearance zones around the structure to prevent water pooling, and require subcontractors to seal openings with weather-resistant barriers before any precipitation event. Data from mitigation practices directly informs your enterprise-level strategy around subcontractor selection and capital allocation, meaning contractors who track which subs execute water protection consistently secure better underwriting terms and lower premiums on future projects.

Catastrophe modeling technology now allows carriers to quantify your specific site’s wildfire, hurricane, flood, and earthquake exposure with precision. Request these risk assessments during underwriting and use the results to guide your site-hardening investments. Most policies impose higher deductibles for water-related or catastrophic losses, which means the cost of prevention through proper drainage and temporary protection systems pays for itself through lower claims frequency and maintained coverage terms.

Theft and Security Lapses Drain Profitability

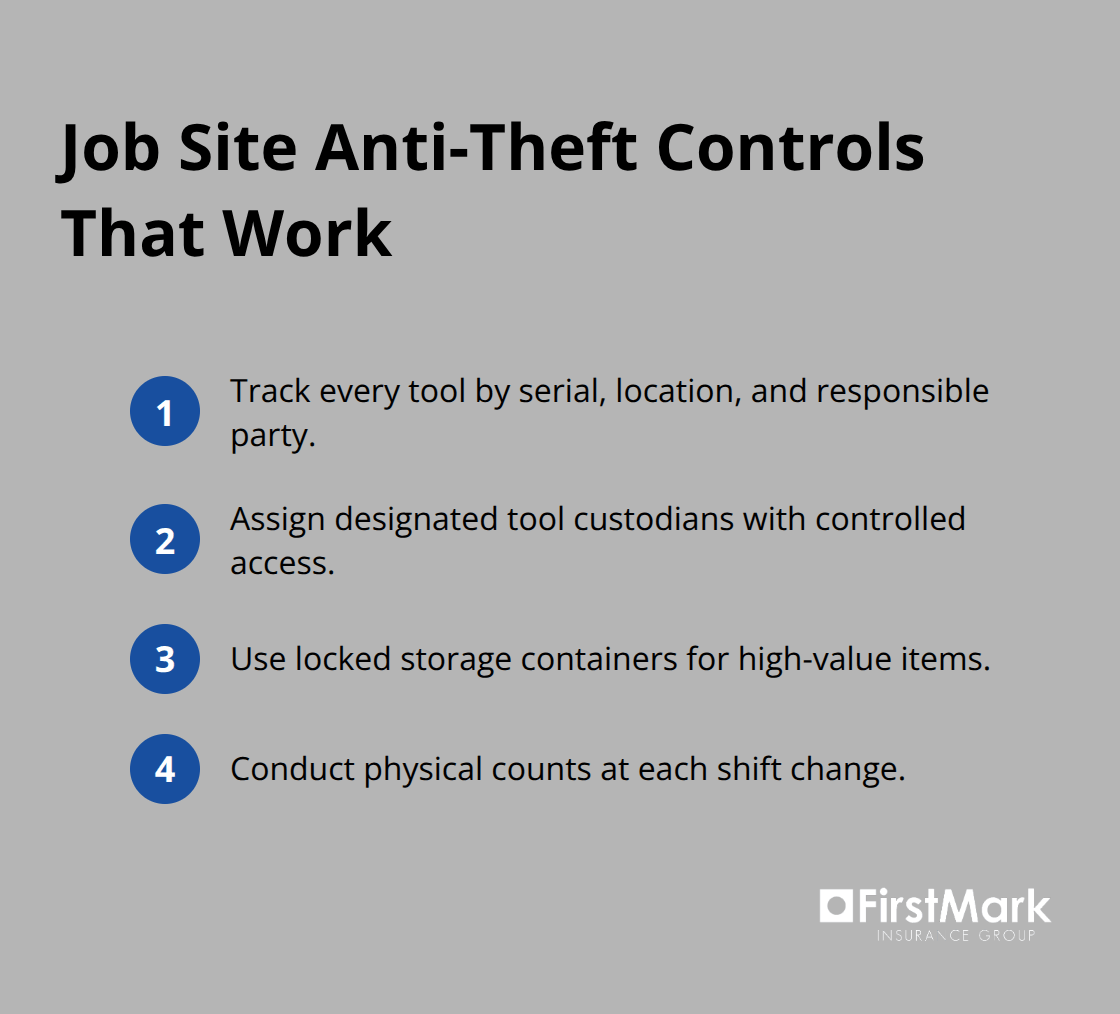

Theft and security lapses drain contractor profitability in ways that weather damage alone cannot explain. Job site theft typically targets high-value equipment, copper wiring, and tool caches left unattended overnight, with average losses ranging from thousands to hundreds of thousands depending on project scale and location.

Establish a single equipment inventory system that tracks every tool and piece of equipment by serial number, location, and responsible party-this eliminates the confusion that allows theft to occur undetected for days. Assign designated tool custodians rather than allowing open access, implement locked storage containers for high-value items, and conduct physical counts at shift changes rather than relying on memory.

Worker Safety Demands Rigorous Protocols

Worker-related incidents demand rigorous safety protocols because builder risk insurance does not cover third-party bodily injury or workplace accidents; general liability and workers compensation policies handle those exposures separately. Mechanical, electrical, and plumbing subcontractors represent the most frequent sources of job site incidents according to 2025 industry data, so require these trades to maintain current safety certifications, provide copies of their insurance declarations before mobilizing to site, and conduct pre-work safety briefings that cover site-specific hazards.

Document all safety training and incident reports in a centralized system that your carrier can review during underwriting, because contractors who demonstrate rigorous safety discipline secure more favorable coverage terms and faster claim resolution when incidents occur.

Final Thoughts

Builder risk insurance for contractors protects far more than your immediate project-it establishes a foundation for sustainable growth across your entire business. Contractors who treat underwriting as a collaborative conversation rather than a paperwork exercise receive policies that address their specific exposures instead of generic terms that leave gaps when claims occur. Transparent project information, detailed subcontractor data, and realistic timelines allow underwriters to structure coverage that actually fits your operations and secures favorable terms.

The strongest builders risk insurance contractors maintain consistent risk management practices across multiple projects, tracking weather mitigation, equipment security, and safety protocols to build a track record that carriers reward with better terms on future work. This data becomes your competitive advantage when bidding on larger or more complex projects where underwriting scrutiny increases and lenders demand proof of responsible risk management. Your investment in proper coverage and loss prevention directly influences your ability to win contracts and maintain profitability.

We at FirstMark Insurance Group work with top insurance providers to present you with builders risk coverage that fits your requirements at the best available pricing. Our role is simplifying your insurance journey so you can focus on what you do best-building quality projects on schedule and within budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation