General liability premiums in Washington vary significantly based on your business profile, industry, and local regulations. Understanding what influences your costs helps you make informed decisions about coverage.

At FirstMark Insurance Group, we’ve guided countless Washington business owners through this process. This guide breaks down the factors that shape your premiums and shows you practical ways to reduce them.

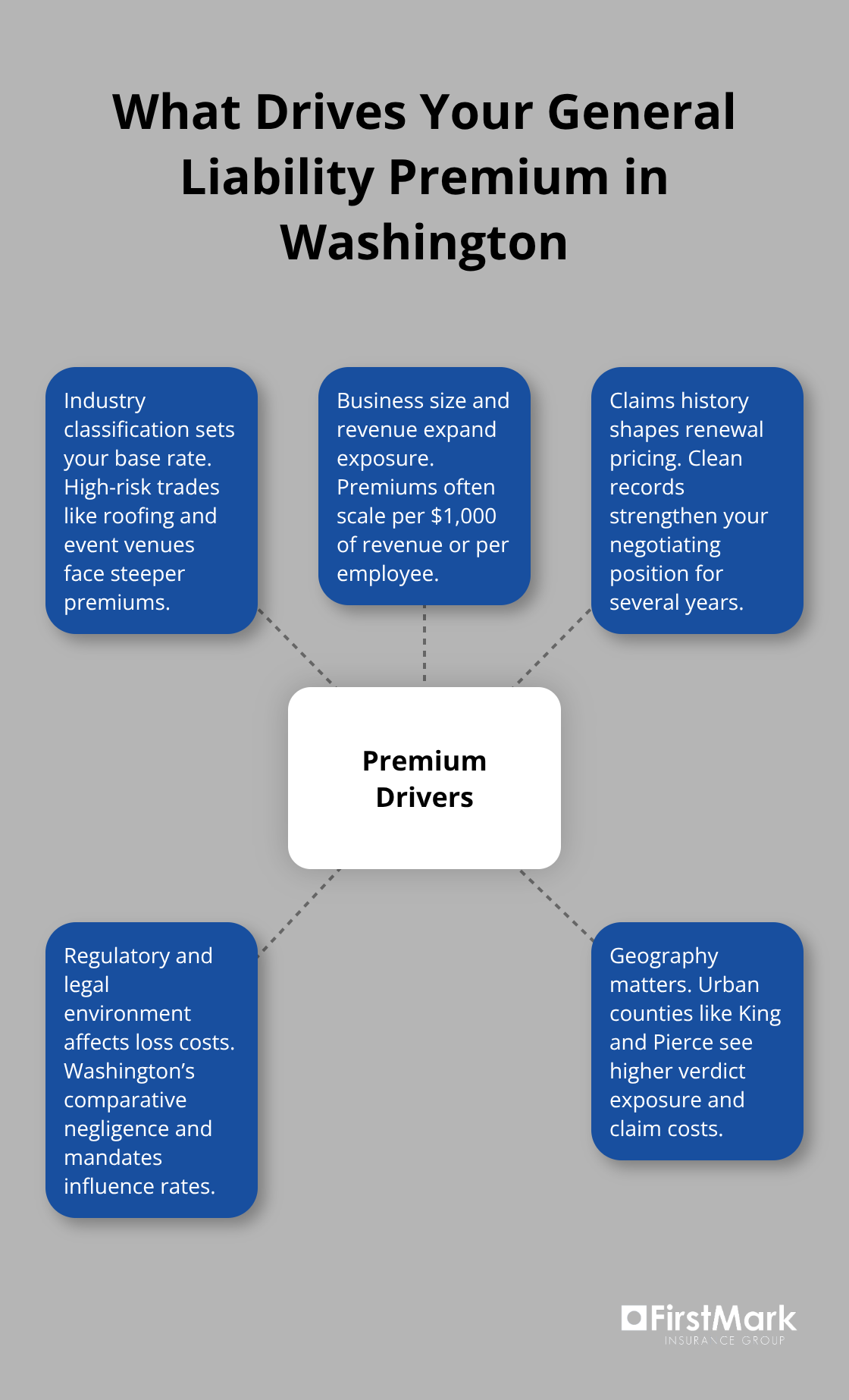

What Drives Your General Liability Premium in Washington

Industry Classification Sets Your Base Rate

Your industry classification sits at the foundation of your premium calculation. A software consultant in Seattle pays roughly $25 to $40 per month for general liability coverage, while a pressure washing operation in the same city faces $1,000 or more monthly. This gap reflects genuine risk differences that insurers measure through detailed loss data. Roofing contractors, construction firms, and venues hosting public events carry higher injury exposure and property damage potential, which translates directly to steeper premiums. Washington’s seismic risk and wet climate add complexity for certain operations, especially those involving equipment or outdoor work.

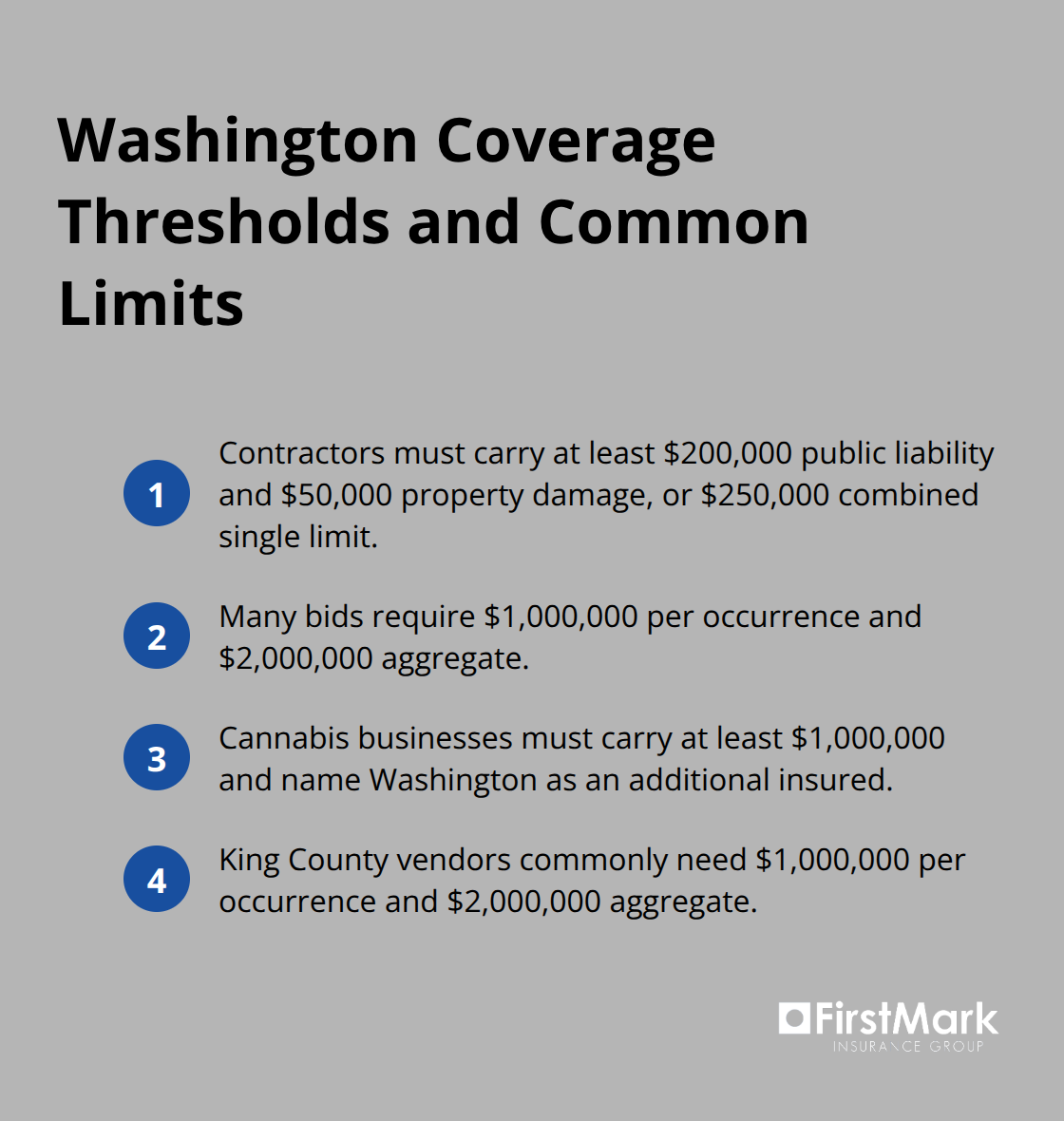

Contractors must maintain at least $200,000 in public liability coverage under state licensing rules, but many clients and landlords demand $1,000,000 per occurrence as standard. Cannabis businesses face the strictest requirements at $1,000,000 minimum, with the state named as an additional insured. The Washington Department of Labor & Industries enforces these thresholds, and failure to meet them can suspend your license. Your specific industry risk profile cannot be negotiated away-insurers determine it through historical claim patterns and severity data.

Business Size and Revenue Shape Your Exposure

Business size and revenue directly influence your exposure calculation and premium structure. A two-person accounting firm with $150,000 annual revenue will pay substantially less than a 50-person construction company with $5 million in revenue, because payroll, square footage, and project scope all correlate with claim frequency and severity. Insurers often calculate premiums per thousand dollars of revenue or per employee, so scaling your business typically increases your total premium even if your per-unit rate stays constant.

Claims History Determines Your Renewal Cost

Claims history matters more than almost any other factor in your renewal quote. A single serious claim-say, a $250,000 bodily injury settlement-can increase your renewal premium by 20 to 40 percent for three to five years, depending on the carrier and your loss pattern. Washington’s pure comparative negligence rule means injured parties can recover even if they bear partial fault, which raises settlement values and claim frequency compared to other states.

If you have maintained a clean loss history over the past three to five years, you hold a genuine competitive advantage in renewal negotiations. Conversely, multiple small claims signal elevated risk to underwriters and trigger aggressive premium increases. Proactive documentation of safety measures, employee training records, and risk reduction investments can help offset a prior claim during renewal discussions, though the claim itself will remain visible on your record. Understanding how Washington’s regulatory environment compounds these premium drivers will help you anticipate costs and plan your coverage strategy accordingly.

Washington’s Regulatory Requirements Shape Your Costs

State Licensing Mandates Set Your Baseline Coverage

Washington’s licensing framework directly influences what you pay for general liability coverage. The Washington Department of Labor & Industries requires contractors to maintain minimum coverage of $200,000 in public liability and $50,000 in property damage, or a combined single limit of $250,000. These thresholds serve as the baseline, but most clients and project bids demand substantially higher limits-typically $1,000,000 per occurrence with $2,000,000 aggregate. Cannabis businesses face the strictest mandate at $1,000,000 minimum coverage with Washington named as an additional insured. King County procurement rules push limits even higher, requiring $1,000,000 per occurrence and $2,000,000 aggregate for any vendor seeking county work.

This regulatory complexity means your premium calculation starts not with what you think you need, but with what state law and contract requirements actually demand. Insurers price policies to match these mandated thresholds, so a contractor bidding on state-regulated work automatically qualifies for higher premium tiers than one serving only private residential clients.

Comparative Negligence Rules Raise Settlement Values

Washington’s pure comparative negligence standard amplifies your liability exposure compared to other states. Under this rule, injured parties recover damages even if they bear partial fault for an accident, which means settlements and jury awards trend higher than in states with different negligence frameworks. This legal environment directly affects how insurers calculate your premium-they price policies based on historical claim costs in Washington, and those costs reflect the state’s generous recovery standards.

The Washington Office of the Insurance Commissioner reviews all proposed rate changes to verify they are actuarially justified, which creates transparency but also means carriers can justify larger premium increases when loss data shows rising claim costs. General liability renewal rates in Washington rose 3.28 percentage points in 2025 according to the Ivans Index, the sharpest increase among tracked commercial lines.

Geographic Location Determines Your Rate Tier

Urban counties like King and Pierce typically see premiums 30 to 50 percent higher than rural areas due to larger verdict pools and elevated claim costs. When you renew your policy, the carrier’s underwriter will examine your specific county location, industry classification within that county, and prior claims to calculate your rate. This means a roofing contractor in Seattle faces materially different pricing than one in a rural Washington county, even with identical business size and claims history.

Your location interacts with your industry risk profile to produce your final premium. A pressure washing operation in King County will pay substantially more than the same operation in a sparsely populated county, because both the verdict pool and the frequency of claims differ. These geographic variations reflect real differences in claim costs, not arbitrary pricing decisions. Understanding how location compounds your other risk factors helps you anticipate what your renewal quote will reflect and prepares you to discuss rate management strategies with your insurance professional.

How to Reduce Your General Liability Premiums

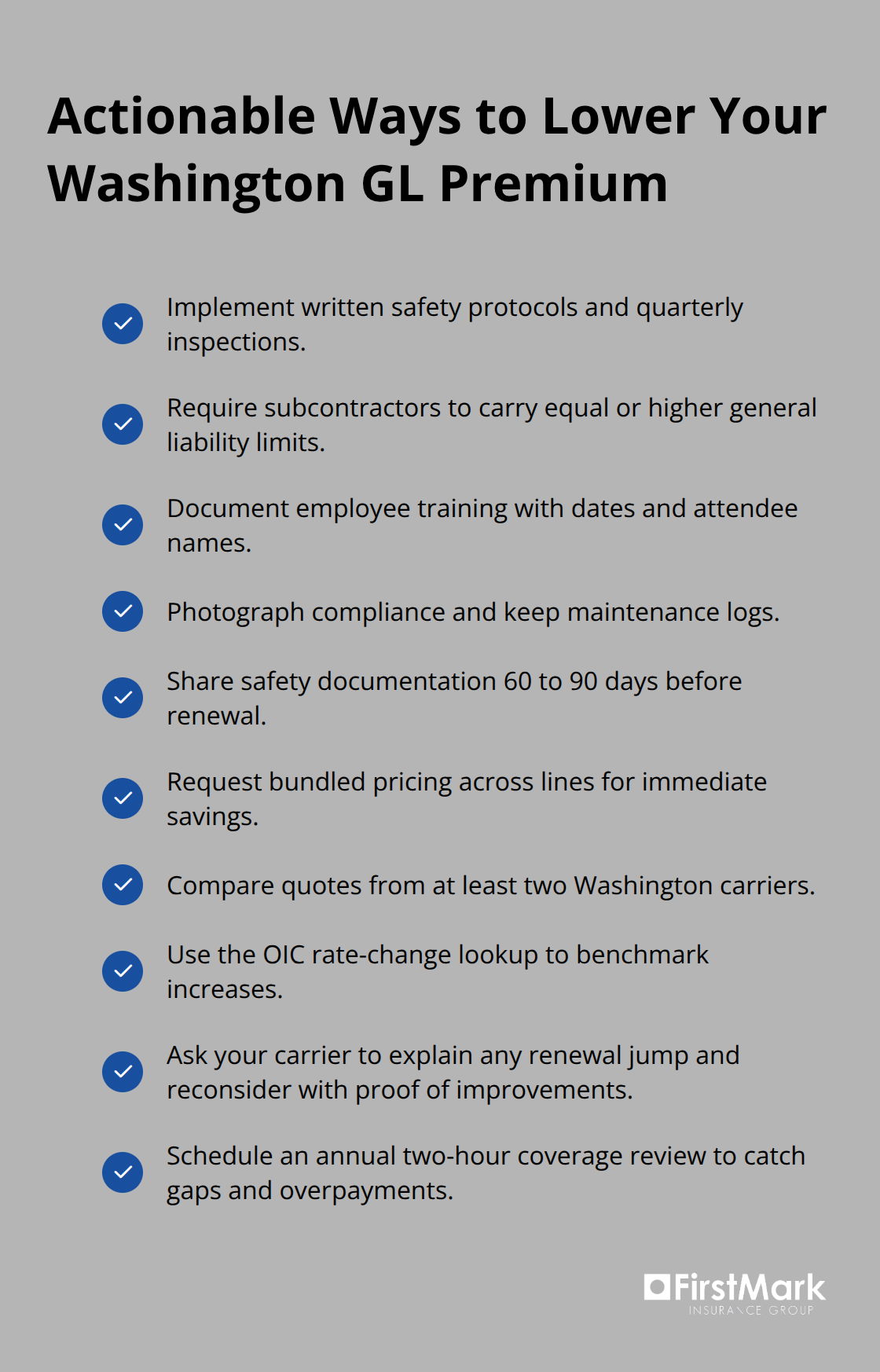

The regulatory environment and claims history you cannot change, but your premium calculation includes several levers you control directly. Documented safety programs, bundled coverage types, and timely policy reviews can reduce your costs by 10 to 25 percent depending on your current profile and carrier. Washington business owners have cut their renewal premiums by thousands of dollars annually through these specific strategies, and the investments required are modest compared to the savings.

Safety Programs Lower Your Underwriting Risk

Insurers reward measurable risk reduction with lower premiums. A contractor who maintains written safety protocols, conducts quarterly jobsite inspections, requires subcontractors to carry equal or higher general liability limits, and documents employee training receives better renewal pricing than one without these programs. The investment is straightforward: create a simple safety checklist specific to your operations, photograph compliance, keep training records with dates and attendee names, and share this documentation with your carrier 60 to 90 days before renewal.

Carriers like The Hartford and ERGO NEXT explicitly factor safety program documentation into their underwriting decisions, often granting 5 to 15 percent premium reductions for businesses that demonstrate sustained risk management. Non-slip flooring in retail spaces, clear signage on hazards, regular equipment maintenance logs, and incident reporting systems all signal to underwriters that you take loss prevention seriously. This approach works because it reduces both claim frequency and severity, which directly impacts the carrier’s expected losses and justifies lower pricing.

Multi-Policy Bundling Delivers Immediate Savings

Bundling general liability with commercial property, workers compensation, and commercial auto into a single package or through the same carrier typically yields 10 to 20 percent aggregate savings compared to purchasing policies separately. A small construction firm paying $2,500 annually for standalone general liability, $1,800 for property, and $3,200 for commercial auto can reduce that combined $7,500 to roughly $6,000 to $6,500 through bundling. Carriers incentivize this consolidation because it reduces their administrative costs and increases customer retention.

When you shop for quotes, request bundled pricing explicitly and compare the total package cost, not just the general liability line item. Some carriers waive or reduce certificate of insurance fees for bundled customers, which adds hidden value if your business frequently needs to issue certificates to clients or landlords. The Hartford offers bundled packages across Washington that include optional cyber liability and professional liability endorsements, which expands your protection while maintaining the discount advantage. This strategy works best when you review your entire insurance portfolio with a licensed agent who can identify overlapping coverage, eliminate redundancies, and structure policies to maximize savings.

Annual Coverage Reviews Prevent Overpayment and Gaps

You should review your coverage 60 to 90 days before renewal to prevent renewing outdated or inadequate limits and to catch premium creep before it compounds. If you hired ten new employees, expanded into a second location, or added a new service line since your last renewal, your exposure has increased and your current limits may no longer match your actual risk. Conversely, if you downsized operations or shifted away from high-risk work, your premium may not reflect that improvement.

Request a detailed renewal quote breakdown from your carrier that shows the rate per thousand of revenue or exposure unit, your claims history surcharge or credit, and any applicable discounts. Compare this to quotes from at least two other carriers in Washington to identify whether your renewal rate is competitive. The Washington Office of the Insurance Commissioner publishes rate-change lookup tools by county and insurer, allowing you to see what other carriers approved for similar businesses in your area. If your renewal premium jumps significantly, ask your carrier specifically what changed (was it a rate increase across the board, a surcharge from a prior claim, or a change in your exposure calculation). Many carriers will reconsider pricing if you present documented risk improvements or competitive quotes from other insurers. This annual discipline takes roughly two hours but can identify $500 to $2,000 in unnecessary costs and prevent coverage lapses that could expose you to uninsured claims.

Final Thoughts

General liability premiums in Washington reflect your industry, business size, claims history, and the state’s regulatory framework. You cannot eliminate these factors, but you control how you respond to them through documented safety programs, bundled coverage, and annual policy reviews that typically reduce your total cost by 10 to 25 percent. The effort required is modest compared to the savings and the protection that comes from knowing your coverage matches your actual exposure.

Finding competitive rates requires comparing quotes from at least two carriers and understanding what drives the differences in their pricing. Request detailed breakdowns that show your rate per exposure unit, any claims surcharges, and available discounts, then use the Washington Office of the Insurance Commissioner’s rate-change lookup tool to see what other insurers approved for similar businesses in your county. This transparency helps you identify whether your renewal quote is competitive and gives you concrete information to discuss with your carrier if you believe the increase is unjustified.

Working with an insurance professional who understands Washington’s regulatory environment and has access to multiple carriers saves you time and money. At FirstMark Insurance Group, we help you understand what changed in your renewal, identify cost-reduction opportunities, and structure your coverage to protect your business without overpaying (rather than accepting your renewal quote at face value). Contact FirstMark Insurance Group to discuss your general liability premiums in Washington and discover how much you might save through a comprehensive policy review.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation