One mistake we see Washington professionals make is underestimating their exposure to client claims. A single lawsuit can drain resources and damage your reputation, which is why professional liability insurance in WA isn’t optional-it’s foundational.

At FirstMark Insurance Group, we work with practitioners across industries who understand that the right coverage protects both their business and their clients’ interests. This guide walks you through what you need to know to make an informed decision.

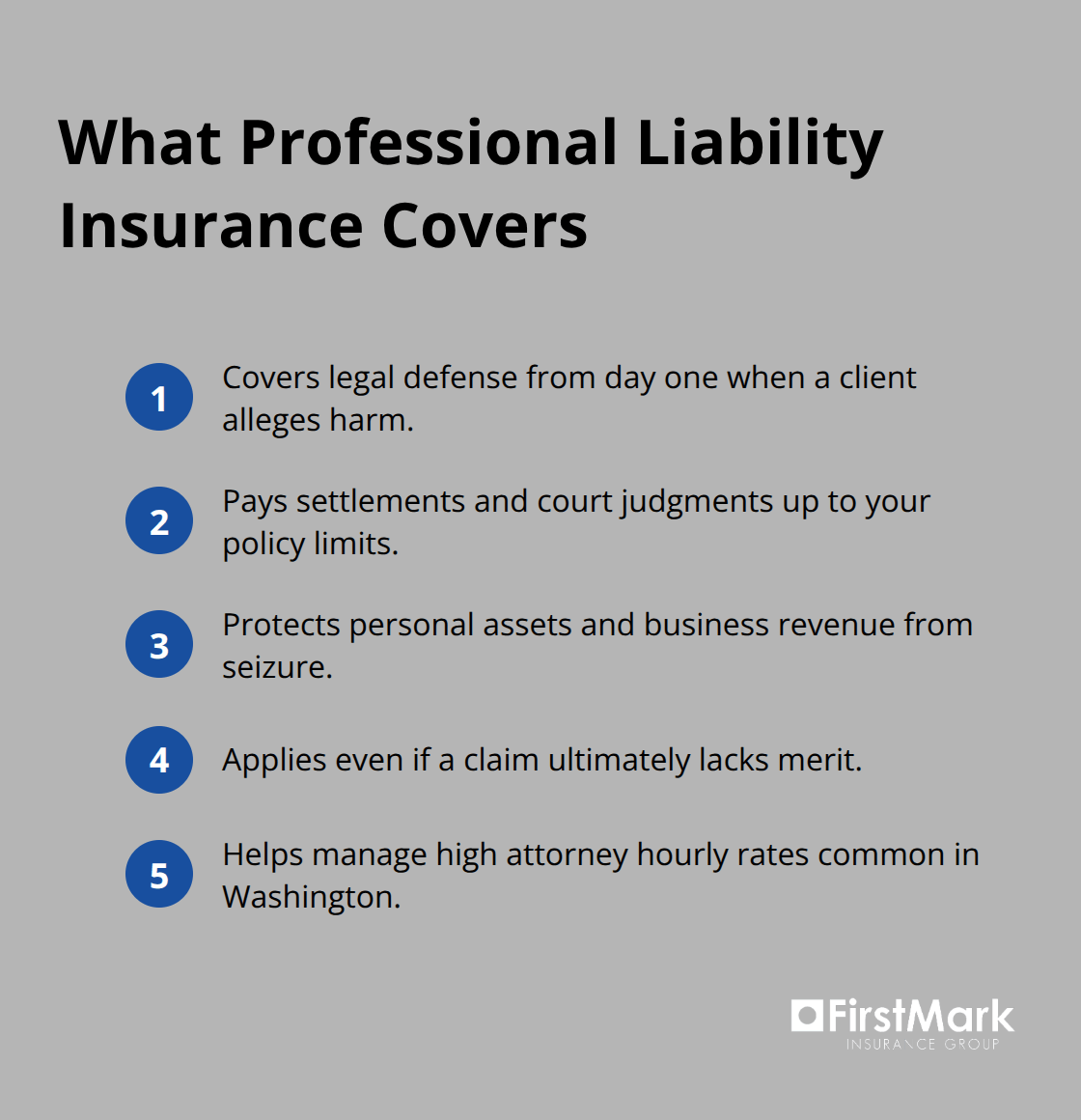

What Professional Liability Insurance Actually Covers

Professional liability insurance in Washington covers two critical areas: the cost of defending yourself against client claims and the financial settlement or judgment if a claim succeeds. When a client alleges you provided faulty advice, made a professional error, or failed to deliver promised services, this coverage pays for your legal defense from day one, regardless of whether the claim has merit.

Defense costs alone can reach thousands of dollars monthly in Washington, where Seattle-area attorneys charge between $162 and $392 per hour on average. Without this protection, you absorb those expenses immediately while the claim is still being investigated. The policy also covers settlements and court judgments up to your chosen limits, protecting your personal assets and business revenue from being seized to pay damages.

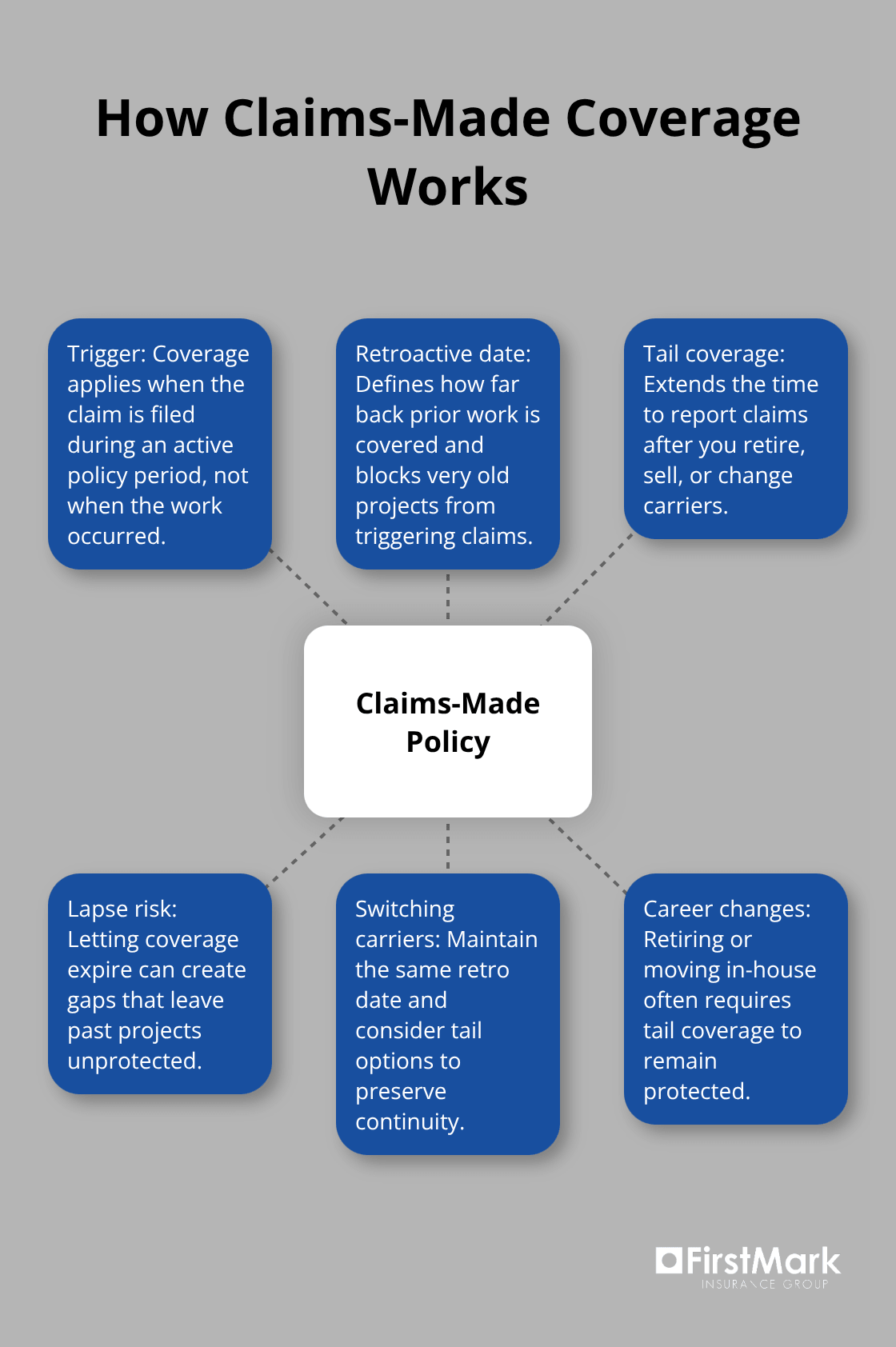

How Claims-Made Policies Work in Washington

Most Washington professionals structure their coverage with per-occurrence limits and aggregate limits for the policy period-for example, $1 million per claim with $2 million total annual coverage. Nearly all malpractice policies operate on a claims-made basis, meaning coverage applies when the claim is filed during your active policy period, not necessarily when the work was performed. This structure matters significantly because it creates gaps if you switch insurers or let coverage lapse.

If you worked on a project in 2024 but a client files a claim in 2026 after your policy has ended, that claim may fall outside coverage unless you purchased tail coverage-an extended reporting period that protects you for claims filed after you stop working or change carriers.

This protection proves particularly important for professionals who retire, sell their practice, or transition to in-house roles. The policy also references a retroactive date, which specifies when coverage begins for past work and prevents clients from filing claims on ancient projects. Washington’s Office of the Insurance Commissioner reported that in 2021, the median indemnity payout for medical malpractice claims was just over $340,000, with the highest verdict exceeding $12 million, illustrating why adequate limits matter and why retroactive date clarity prevents costly surprises.

Coverage Limits Vary by Industry and Risk

Coverage limits in Washington vary significantly by profession and risk profile. Seattle-area public bids frequently require $1 million per occurrence and $2 million aggregate, establishing a practical floor for many service providers. A five-attorney law firm typically pays $7,500 to $15,000 annually for $2 million per $4 million aggregate coverage, while a solo graphic designer might pay $600 to $1,000 for $1 million per $1 million coverage. Higher-risk industries like tax services, engineering, and healthcare often require substantially higher limits; a mid-size medical clinic might carry $55,000 to $120,000 in annual premiums for adequate protection.

Deductibles and Premium Reduction Strategies

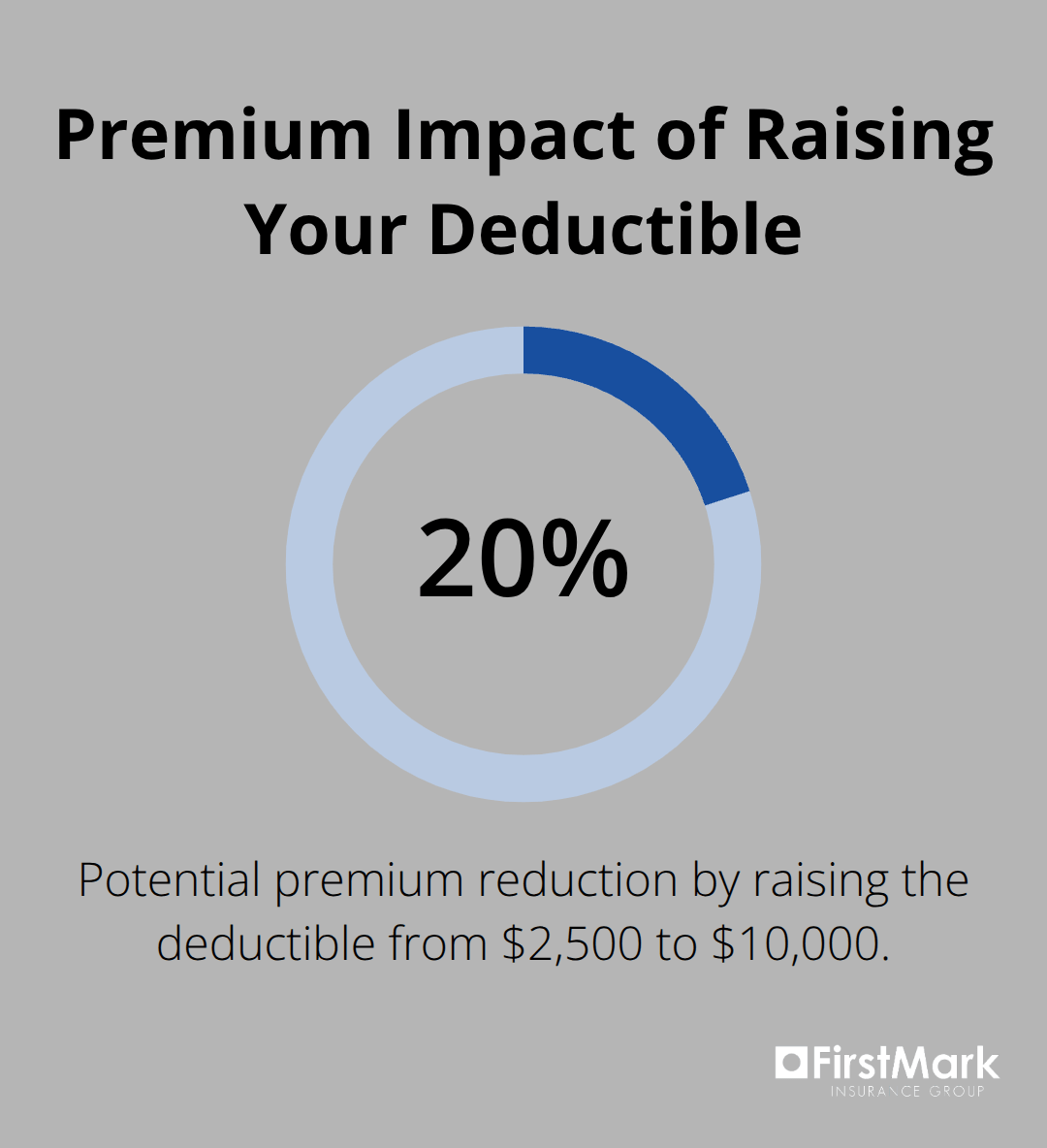

Increasing your deductible from $2,500 to $10,000 can reduce premiums by up to 20 percent, though this shifts more defense costs onto your shoulders during claims. Washington’s comparative negligence standard and the Consumer Protection Act create exposure for treble damages in deceptive-practice cases, making robust limits a practical investment rather than an optional expense.

When you evaluate policies, confirm what exclusions apply-professional liability typically excludes employment-related claims, criminal conduct, bodily injury, property damage, and cyber incidents, all of which require separate coverage.

Selecting the Right Coverage for Your Practice

The right coverage limits align with your industry standards and claims exposure, ensuring you neither overpay for unnecessary protection nor expose yourself to unmanageable risk. Your specific profession, revenue, claims history, and staff size all influence what limits make sense for your situation. Understanding these variables helps you move forward with confidence into the next critical step: identifying which Washington providers offer the coverage structure and terms that match your professional needs.

Why Washington Professionals Face Real Liability Exposure

Washington’s Liability Landscape Demands Protection

Washington’s business environment creates specific liability pressures that professionals in other states don’t encounter. The state hosts more than 650,000 small businesses with roughly 1.4 million employees concentrated in knowledge-based sectors where a single error-a missed deadline, incorrect advice, or faulty analysis-triggers substantial damages. Washington’s comparative negligence standard allows courts to assign liability proportionally, and the Consumer Protection Act permits treble damages for deceptive practices, meaning a $100,000 mistake could result in a $300,000 judgment. In 2021 alone, Washington recorded 318 new medical malpractice claims with a median indemnity payout of just over $340,000, though verdicts occasionally exceeded $12 million according to the Washington Office of the Insurance Commissioner. These aren’t theoretical scenarios-they’re documented claims filed against practitioners who believed their expertise alone would protect them.

Your professional competence matters tremendously, but it doesn’t shield you from the legal and financial machinery that activates the moment a client alleges harm. Without professional liability insurance, you personally absorb defense costs that typically range from $50,000 to $250,000 even for claims that ultimately prove baseless, plus any settlements or judgments the court orders.

Client Expectations Now Include Insurance Verification

Your clients expect financial accountability, and many now require proof of coverage before engaging your services. Public sector clients in the Seattle area routinely demand $1 million per occurrence and $2 million aggregate limits as a condition of contract, making insurance not just prudent but mandatory for competitive bidding. Private clients increasingly ask about your coverage status during initial consultations-they understand that a professional without insurance signals either overconfidence or financial instability, neither of which inspires confidence. This expectation reflects market reality: when clients hire professionals in Washington, they’re implicitly betting their own outcomes on your judgment and execution. Insurance demonstrates you’ve taken that responsibility seriously enough to back it with financial protection.

Operational Stability Depends on Adequate Coverage

Beyond client requirements, your own operational stability depends on maintaining coverage that matches your actual exposure. A five-attorney law firm operating with outdated $500,000 limits faces catastrophic personal liability if a single client claim exceeds that threshold, forcing partners to cover the gap from personal assets. Similarly, a mid-size accounting firm handling tax and audit work for growing companies faces compounding exposure as client complexity increases, yet many firms fail to adjust limits upward as their practice evolves. The professionals who maintain adequate, current coverage eliminate the scenario where a single claim dismantles years of business building.

This reality underscores why selecting the right coverage limits and policy structure matters so profoundly. The next step involves understanding how to evaluate your specific industry’s risk profile and match it with coverage that actually protects your practice.

Selecting Coverage That Matches Your Real Risk Profile

Assess Your Actual Exposure, Not Industry Defaults

Start by identifying what your specific profession actually exposes you to, then match that exposure to concrete coverage limits rather than accepting industry defaults. A solo tax accountant preparing returns for small businesses faces materially different claims than a tax consultant advising on complex corporate restructurings, yet both often quote identical $1 million per $2 million limits without analyzing whether those numbers reflect their actual work. Your revenue, client complexity, and the types of decisions you make daily should drive your limit selection. If you bill $500,000 annually advising on high-stakes transactions, carrying $500,000 in coverage leaves you dangerously exposed if a single claim approaches your annual revenue. Conversely, a consultant billing $250,000 yearly to small clients may find $2 million limits excessive and wasteful.

Understand Baseline Requirements for Washington Work

Seattle-area public sector contracts typically require $1 million per occurrence and $2 million aggregate as a baseline, so if you pursue government work, that becomes your minimum threshold regardless of your firm size. Washington’s Office of the Insurance Commissioner reported that five-attorney law firms typically pay $7,500 to $15,000 annually for $2 million per $4 million coverage, while mid-size medical clinics pay $55,000 to $120,000 for substantially higher limits reflecting the stakes of healthcare decisions. Your claims history also shapes available pricing; a firm with zero claims over five years qualifies for better rates than one with multiple defense costs, so documenting your risk management practices during the quoting process demonstrates stability to insurers.

Evaluate Policy Exclusions and Structure Carefully

Once you’ve determined appropriate limits, examine the specific exclusions and policy structure before committing. Professional liability policies universally exclude employment disputes, cyber incidents, criminal conduct, and bodily injury claims, meaning those exposures require separate coverage you must purchase independently. The claims-made trigger means a policy covers only claims filed during active coverage, creating a critical gap if you retire, sell your practice, or change carriers without extended reporting period tail coverage. Washington medical malpractice claims in 2021 reached a median settlement of $340,000 with verdicts occasionally exceeding $12 million according to state records, underscoring why your deductible choice matters operationally.

Calculate Deductible Impact on Cash Flow

Raising your deductible from $2,500 to $10,000 can reduce premiums by approximately 20 percent, but that shift means you personally pay the first $10,000 in defense costs during a claim, which affects your monthly cash flow immediately. This trade-off works well for established firms with strong reserves but creates hardship for younger practices operating with tighter margins. Request comparative quotes from multiple insurers, not just pricing but actual policy documents, and confirm whether each policy covers your retroactive date adequately if you’ve carried prior insurance.

Verify Coverage for Your Entire Team

Verify that independent contractors you engage are either named on your policy or covered through blanket endorsement language, preventing coverage gaps when subcontractors face claims related to your client relationships. The right policy structure eliminates surprises when claims actually arise, protecting both your immediate financial position and your long-term business continuity.

Final Thoughts

Professional liability insurance in Washington protects your practice from the financial and reputational damage that follows client claims, but only when you’ve selected coverage that actually matches your exposure. Your coverage limits should reflect your revenue, client complexity, and industry standards rather than generic defaults, and your deductible choice should balance premium savings against your firm’s cash-flow capacity. Your policy exclusions demand complete understanding so you know what separate coverage you need for employment disputes, cyber incidents, or other exposures your professional liability insurance WA policy doesn’t address.

The next step is straightforward: gather quotes from multiple insurers, request actual policy documents rather than summaries, and verify that each option covers your retroactive date and includes tail coverage provisions if you anticipate future transitions. Ask about endorsements that extend coverage to your team members and confirm whether independent contractors are named or covered through blanket language. Request comparative quotes that show per-occurrence limits, aggregate limits, deductible options, and annual premiums side by side so you can evaluate trade-offs clearly.

At FirstMark Insurance Group, we work with Washington professionals to match them with coverage that protects their practice without unnecessary expense. We explore offerings from top providers and present you with choices at the best available pricing. Contact FirstMark Insurance Group to discuss your professional liability insurance needs and secure the protection your practice deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation