One mistake in your professional work can trigger a lawsuit that threatens your practice and personal assets. E&O insurance for professionals protects you when clients claim you failed to deliver the standard of care they expected.

At FirstMark Insurance Group, we’ve seen how quickly a single claim can escalate into legal battles that drain time and money. The right coverage transforms a potential catastrophe into a manageable business risk.

What E&O Insurance Actually Covers

E&O insurance protects you against three distinct financial exposures that can devastate a professional practice. First, it covers damages awarded in court or agreed upon in settlements when a client successfully claims you failed to meet professional standards. Second, it pays your legal defense costs, including attorney fees and court expenses, even if a claim proves groundless. Third, it covers regulatory defense costs if licensing boards or government agencies investigate complaints stemming from your work. The Hartford reports that E&O covers judgments, settlements, court costs, and defense against regulatory actions, which means you’re protected whether a case settles quickly or drags through litigation. Without this coverage, you’re personally liable for every dollar, which can wipe out years of business profits. According to BizInsure data from over 5,000 small-business customers, the average annual E&O cost is $767.24, with more than half of buyers paying less than $600 per year. This modest investment shields you from exposure that could reach hundreds of thousands of dollars in a serious claim.

What E&O Won’t Cover

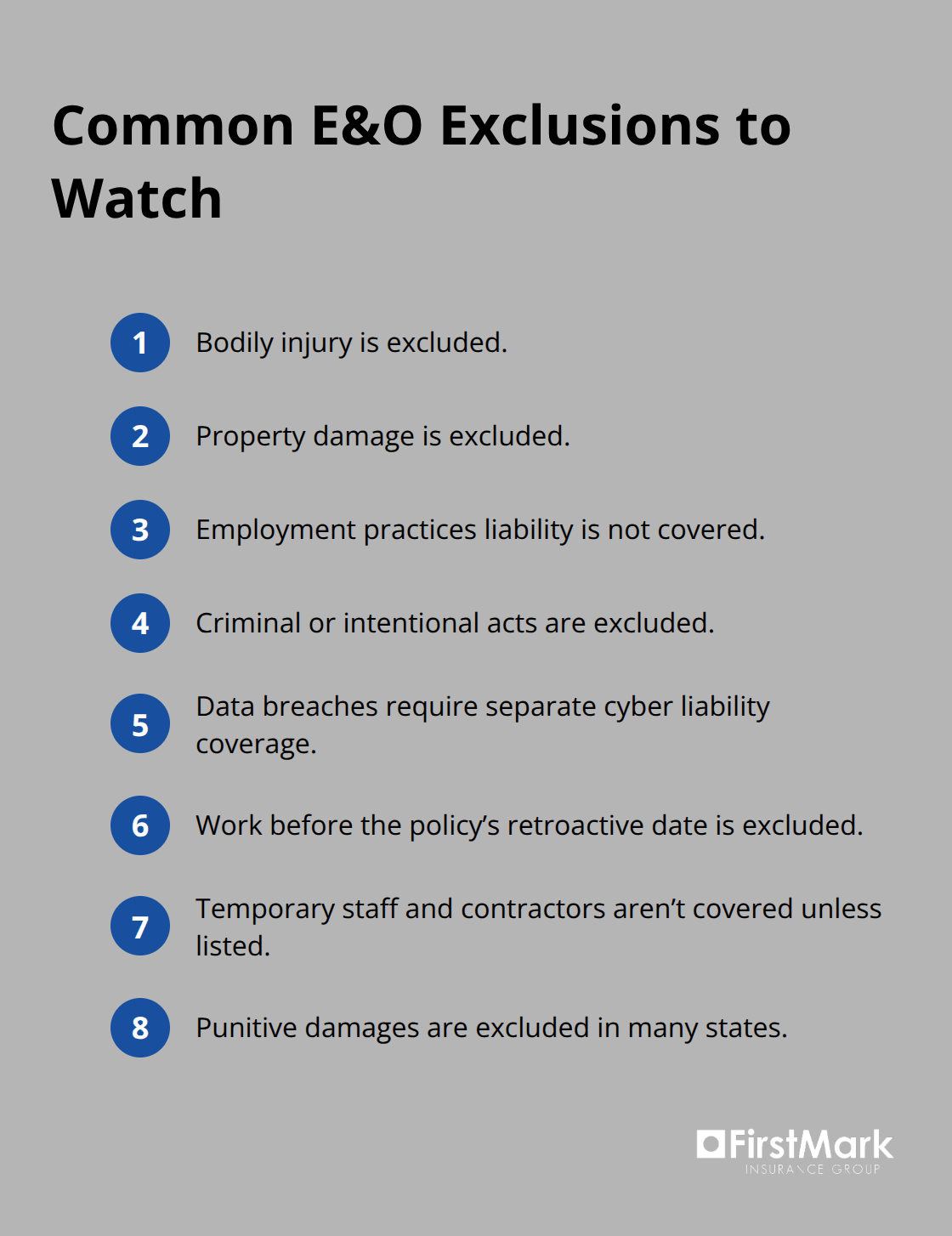

E&O has hard boundaries you must understand before relying on it. The policy excludes bodily injury, property damage, employment practices liability, criminal acts, data breaches, and work performed before your policy’s retroactive date. If a client sues you for a mistake made three years ago but you didn’t purchase E&O until last month, that claim falls outside coverage. This is why establishing retroactive coverage when you first obtain a policy matters tremendously.

Additionally, E&O does not cover temporary employees or contractors unless they’re explicitly listed on your policy, creating a dangerous gap if you hire freelancers without confirming coverage. Cyber liability, covering data breaches and ransomware attacks, requires separate insurance entirely. E&O also excludes punitive damages in many states, meaning if a court awards extra damages to punish intentional misconduct, you absorb that cost yourself. Understanding these exclusions prevents the false security of thinking you’re fully protected when significant gaps exist.

Defense Costs That E&O Covers

One of E&O’s most valuable features is that it pays defense costs regardless of claim outcome. Your insurer funds your attorney throughout depositions, discovery, trial preparation, and trial itself. This means you can mount a vigorous defense without draining business cash or personal savings to cover legal bills. Many professionals face financial pressure to settle meritless claims simply because they can’t afford legal fees, but E&O eliminates that pressure. The policy also covers time spent away from your practice at depositions and trials, and some policies provide subpoena assistance to locate necessary witnesses. This coverage applies even if the claim ultimately fails, protecting you from the crushing cost of defending yourself against unfounded allegations. These protections form the foundation of your risk management strategy, but they only work if you understand which industries face the highest exposure to claims.

Who Needs E&O Insurance Most

Design Professionals Face Immediate Exposure

Architects and engineers face immediate exposure the moment they submit plans or specifications to clients. E&O coverage covers contractors against financial loss resulting from mistakes, errors, or claims of negligence. Design and architecture firms specifically face risk from errors in plans or specifications that lead to delays or costly revisions, making E&O a baseline business requirement rather than optional protection. Design professionals routinely encounter clients who demand E&O coverage as a contract requirement before awarding projects, which means lacking this protection eliminates entire market segments. One miscalculation can cost you access to future work and expose you to substantial liability.

Consultants and Advisors Operate in Treacherous Territory

Consultants and financial advisors operate in equally treacherous territory because their advice directly influences client financial outcomes. When a management consultant’s strategy recommendation leads to failed initiatives, or a financial advisor’s guidance causes investment losses, clients sue for damages that reflect months or years of lost profits. These claims often reach settlement amounts in the six figures because the financial impact is quantifiable and substantial. Your recommendations carry financial weight that clients can measure, making litigation an attractive option when outcomes disappoint them.

Medical and Legal Professionals Carry the Highest Risk

Medical and legal professionals carry the highest litigation risk across all professions, which explains why E&O premiums for these fields command premium pricing. A physician’s diagnostic error, a surgeon’s operative mistake, or an attorney’s missed filing deadline can alter a client’s life trajectory, creating powerful motivation to litigate and substantial damages when negligence is proven. The stakes in these professions are personal and profound, not merely financial.

E&O as a Contractual Requirement

What distinguishes these professions is that E&O isn’t merely prudent insurance-it’s often contractually mandatory. Clients in construction, corporate consulting, and healthcare frequently insert coverage requirements directly into engagement agreements, specifying minimum limits and requiring proof of active policies before work begins. This means E&O coverage determines your ability to compete for lucrative projects, not just your financial protection if something goes wrong. The cost structure reflects actual risk: according to BizInsure data, E&O premiums vary significantly by profession because underwriters price based on claims frequency and severity within each field. Riskier professions pay more, but the alternative is losing access to clients who won’t work without proof of coverage.

Timing and Coverage Gaps Matter

For architects and engineers, establishing E&O early in your career prevents retroactive date gaps that could leave past projects unprotected. For consultants and advisors, you must ensure your policy covers all service lines you offer-whether strategy, financial planning, or implementation support-to prevent the dangerous scenario where a claim falls outside coverage because you failed to disclose a service offering during application. For medical and legal professionals, tail coverage becomes critical when you transition roles or retire, extending protection for claims that arise after you’ve stopped practicing but relate to services you provided while the policy was active. These aren’t theoretical concerns; they’re standard underwriting issues that determine whether claims get paid or denied. Understanding your specific exposure and matching it to the right coverage structure separates professionals who stay protected from those who discover gaps only when a claim arrives.

How E&O Claims Actually Happen

Advisory Mistakes Create Quantifiable Losses

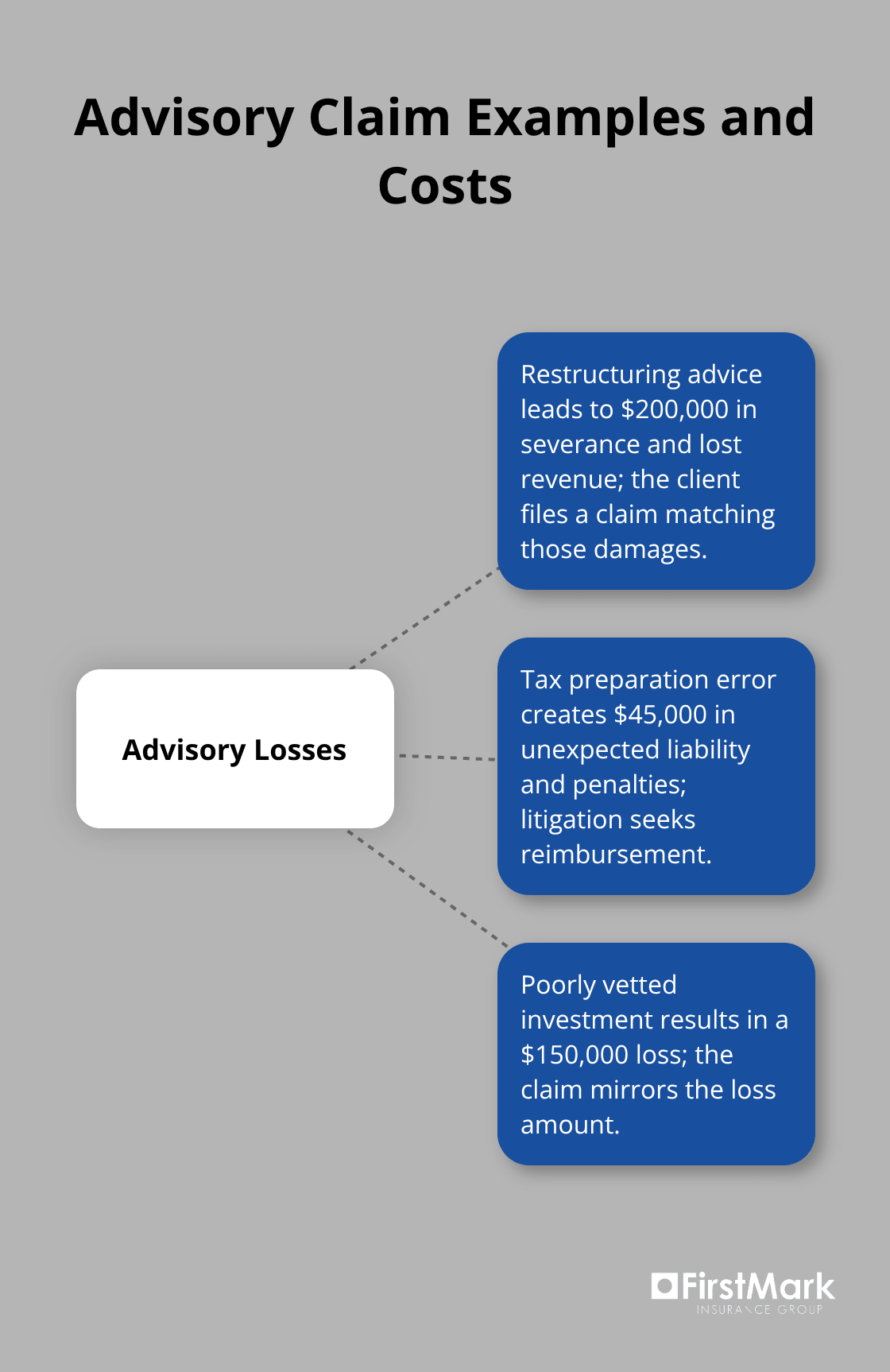

When a project deadline slips and a client’s business suffers financial damage, they don’t blame themselves-they blame you. A management consultant recommends a restructuring that costs a company $200,000 in severance and lost revenue, then the executive team decides the advice was flawed and files a claim. A tax preparer miscalculates deductions, costing a business owner $45,000 in unexpected tax liability plus penalties, and litigation follows immediately. These aren’t hypothetical scenarios; they’re the standard E&O claims that arrive without warning.

Clients measure financial impact precisely, which makes damages calculations straightforward during settlement negotiations. When a consultant’s recommendation fails or an advisor’s strategy underperforms, the client has concrete numbers showing what they lost. This quantifiable harm makes litigation economically rational from the client’s perspective, which means professionals in advisory roles face relentless exposure. The financial advisor whose client loses $150,000 on a poorly vetted investment faces a claim that mirrors that exact loss. The professional whose decision carries measurable financial consequences operates in constant litigation risk.

Design Errors Trigger Cascading Costs

Design errors create a different but equally serious exposure because they trigger cascading costs that multiply beyond the original mistake. A structural engineer’s load calculation error discovered during construction forces contractors to reinforce foundations at exponential cost. An interior designer specifies materials that prove incompatible, requiring complete replacement of finishes mid-project. An architect’s dimensional error forces rework that extends timelines and inflates labor costs across multiple trades. What distinguishes design claims is that clients cannot simply reverse the decision-they must absorb the correction costs as sunk expenses. Unlike advisory claims where a client might have ignored advice, design claims create undeniable proof of error through physical reality. The building won’t stand, the space doesn’t function, or the system fails inspection. This clarity makes defense difficult and settlement amounts substantial because the error is objectively verifiable.

Project Scope and Correction Costs Determine Exposure

Design professionals must carry E&O coverage at limits matching potential project values because a single error on a $5 million construction project can generate claims exceeding $1 million when correction costs and delay damages accumulate. An engineer’s design miscalculation requires expensive remediation work, and the lawsuit mirrors the full cost of correction. Coverage for these scenarios includes both the direct cost of correction and the indirect costs of project delays, which often exceed the correction expense itself. Without adequate limits, a design professional faces personal liability that can exceed business assets, making proper coverage selection not optional but existential to practice survival.

Final Thoughts

E&O insurance for professionals forms the foundation of sustainable practice, not an optional expense you add later. Every professional faces genuine exposure to claims that destroy years of reputation and financial security, and a single claim without protection costs more than a decade of premiums. The math favors coverage for any rational business owner who wants to protect what they’ve built.

Assess your coverage needs by examining three critical factors: what your clients demand contractually, your maximum exposure per project, and whether your policy covers all service lines you offer. A consultant managing a $2 million initiative faces different risk than one handling $50,000 projects, and your limits should reflect realistic worst-case scenarios. If your engagement agreements specify E&O coverage with minimum limits, that requirement becomes your baseline, and failing to disclose a service offering during application creates dangerous gaps where claims fall outside coverage.

We at FirstMark Insurance Group help professionals navigate this assessment process, working with top insurance providers to present tailored coverage that matches your actual exposure. Contact FirstMark Insurance Group to discuss your practice, your client base, and your contractual requirements so we can determine appropriate limits and establish retroactive coverage that protects your past work.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation