Washington general liability rates vary significantly based on your business profile and risk factors. At FirstMark Insurance Group, we’ve helped countless Washington business owners understand what drives their premiums and how to optimize their coverage costs.

Your industry, revenue, claims history, and location all play measurable roles in determining what you’ll pay. The good news is that understanding these factors puts you in control of your insurance strategy.

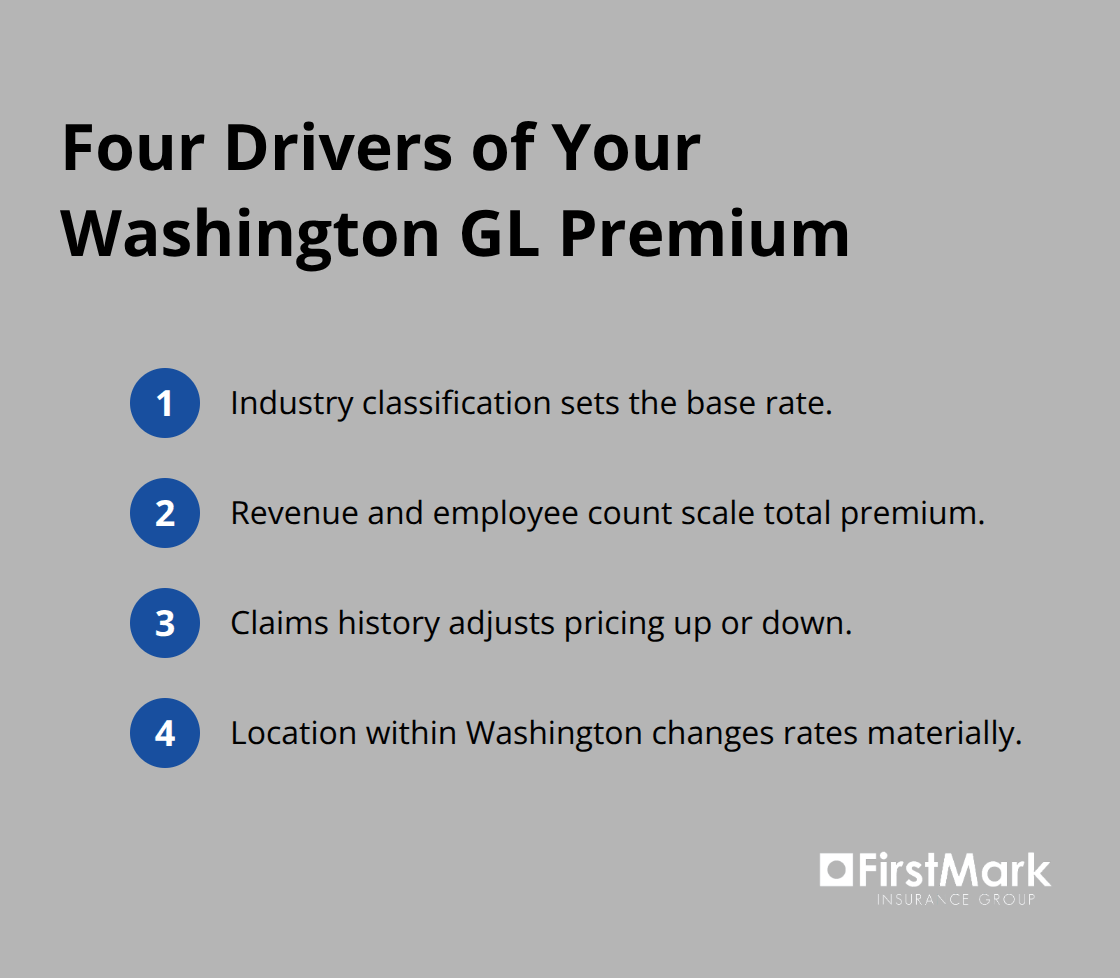

What Really Drives Your General Liability Premium

Industry Classification Sets Your Rate Foundation

Your industry classification is the single biggest lever that insurers pull when pricing your policy, and it’s non-negotiable. Washington uses more than 300 risk classifications to reflect hazard levels across different occupations, so a software consultant in Seattle and a pressure washing business pay vastly different rates. A drone business might pay around $19 per month in general liability premiums, while a pressure washing operation can exceed $1,000 monthly. This isn’t arbitrary-it’s based on historical claim patterns and injury severity data specific to your industry.

Contractors face particularly steep premiums, averaging around $291 per month because construction work carries genuine exposure to property damage and bodily injury claims. The Hartford remains the cheapest overall option at roughly $93 per month for small two-employee businesses, but your actual quote depends entirely on what you do and where you operate.

Revenue and Employee Count Affect Your Total Premium

Revenue and employee count matter because insurers calculate premiums per thousand dollars of revenue or per employee, meaning a growing business naturally faces higher total costs even if the per-unit rate stays flat. A business doubling its revenue doesn’t double its risk in every category, but your insurer will adjust exposure calculations accordingly. Transparency about your actual revenue figures during underwriting prevents surprises at renewal and helps carriers price your policy accurately.

Claims History Creates Long-Term Consequences

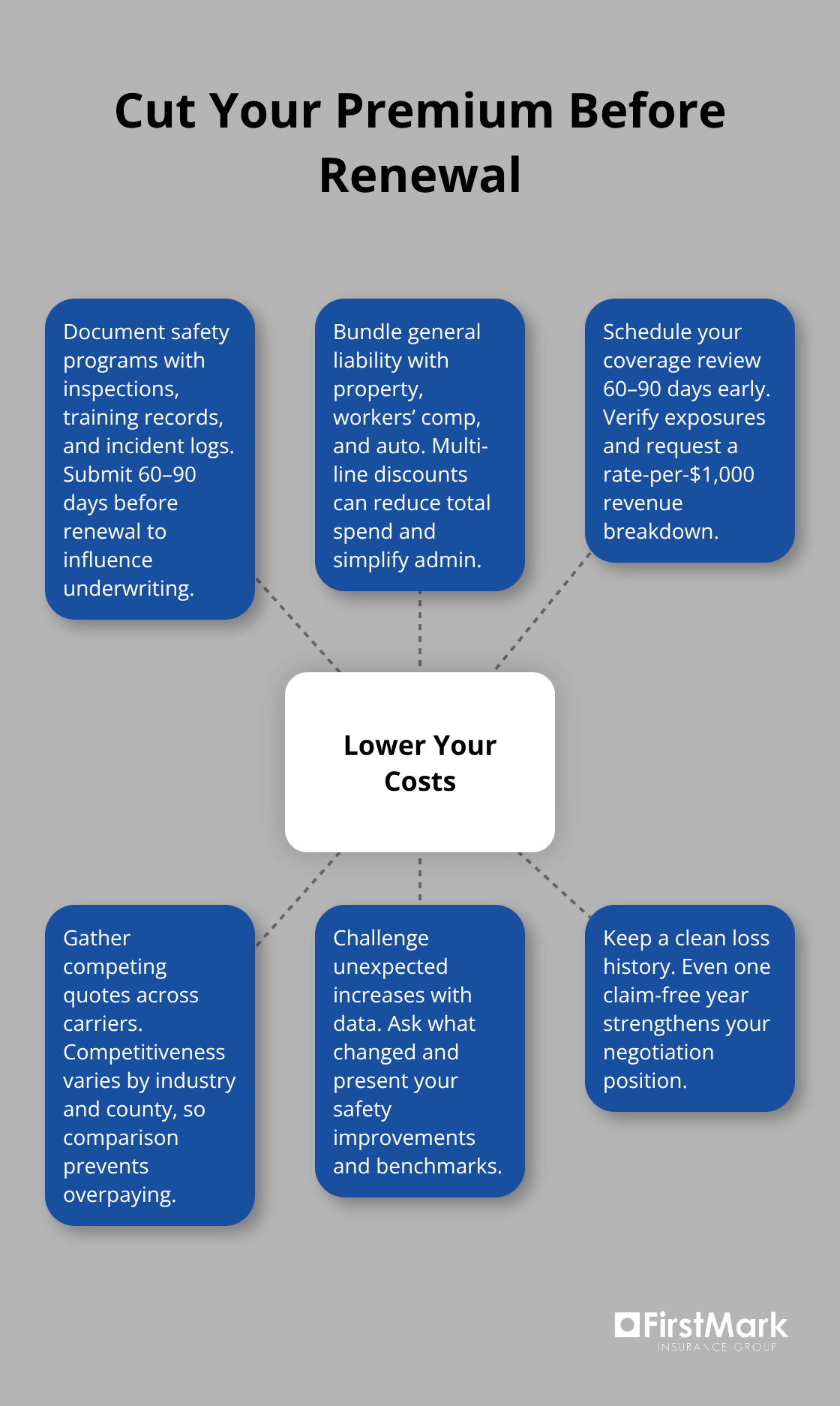

Your claims history operates like a permanent record that follows you through renewal cycles. A clean loss history provides genuine competitive advantage in negotiations and can support favorable pricing, while even one prior claim can trigger surcharges that persist for years. What many business owners miss is that documented risk improvements-written safety protocols, quarterly jobsite inspections, subcontractor liability requirements, training records submitted 60 to 90 days before renewal-can offset the impact of a prior claim during negotiations.

Safety programs can reduce underwriting risk and lower premiums by roughly 5 to 15 percent, so the work you do to prevent losses directly influences what carriers charge.

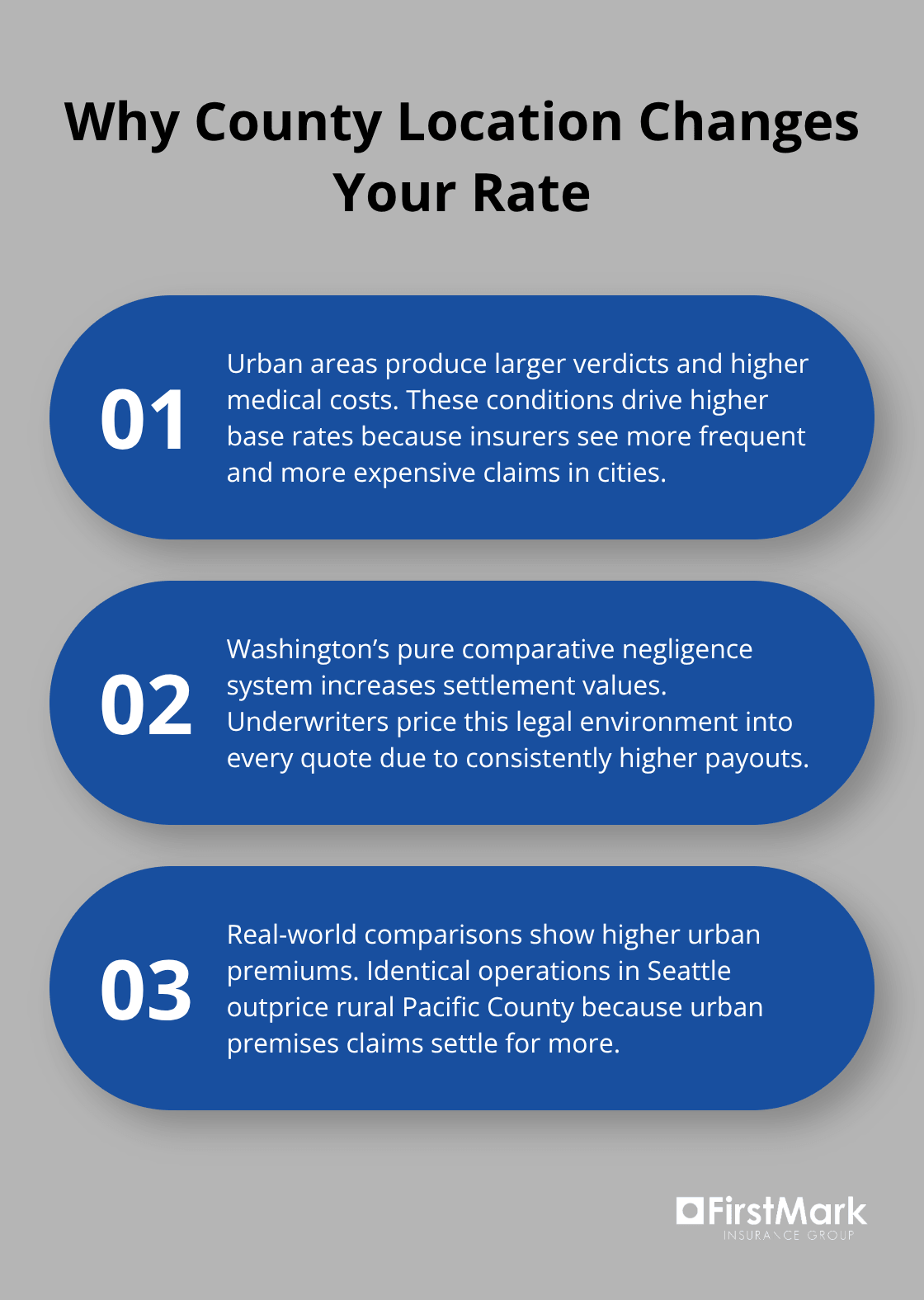

Location Within Washington Creates Dramatic Price Variation

King County and Pierce County premiums run 30 to 50 percent higher than rural counties because urban areas have larger verdict pools, higher medical costs, and more litigation history. Washington’s pure comparative negligence framework and the Insurance Fair Conduct Act tend to raise settlement values and claim frequency, which insurers factor into every quote. An identical business operating in rural Wahkiakum County pays substantially less than the same operation in downtown Seattle, regardless of other factors.

Understanding how insurers assess these location-based risks helps you anticipate what your renewal quote will reflect and prepares you to discuss rate increases with your carrier.

How Insurers Price Your Coverage

Underwriting Departments Assess Your Risk Profile

Underwriting departments at major carriers like The Hartford and ERGO NEXT apply structured risk assessment processes that compare your business against historical claim data. When you submit your quote request, the underwriter evaluates your industry classification, annual revenue, employee headcount, location, and prior claims to assign a baseline rate. That rate gets adjusted based on your experience factor, which reflects whether your loss history is better or worse than the average business in your classification. Your actual quote depends on how the underwriter interprets your specific exposure-a contractor with one prior claim and documented safety protocols receives different underwriting treatment than a contractor with multiple recent losses and no safety documentation. This is why identical businesses in the same industry can receive dramatically different quotes from the same carrier.

County Location Reshapes Your Premium Fundamentally

County location fundamentally reshapes what you’ll pay because King County and Pierce County premiums run 30 to 50 percent higher than rural Washington counties. An insurer quotes higher rates in urban areas because verdict pools are larger, medical costs run higher, and claim frequency historically exceeds rural patterns. Washington’s pure comparative negligence system means juries award larger settlements than states using contributory negligence rules, and underwriters price this legal environment into every quote. A pressure washing business in Seattle pays substantially more than the identical operation in rural Pacific County because the claims data tells underwriters that urban premises liability claims settle for more money.

This isn’t negotiable with your carrier-it reflects real cost differences in your market.

Carrier Competition Varies by Industry and Location

The solution isn’t to argue your county’s verdict history; it’s to gather competing quotes from multiple carriers because carrier competitiveness varies significantly by industry and location. Your industry and location combination determines which carrier prices you most competitively. When renewal quotes arrive, request a detailed breakdown showing the rate per thousand dollars of revenue and identify what changed from the prior year (whether it’s a carrier rate increase, a surcharge tied to your prior claim, or a revised exposure calculation based on updated revenue figures). This transparency lets you bring documented risk improvements to renewal negotiations and prevents you from overpaying for coverage that doesn’t reflect your actual risk profile.

Understanding how carriers price your specific combination of industry, location, and claims history positions you to negotiate effectively at renewal and identify which insurers offer the best value for your operation. The next section explores concrete steps you can take to lower your costs before renewal arrives.

Concrete Steps to Cut Your Premium Before Renewal

Document Your Safety Practices to Reduce Rates

Documented safety programs reduce your premium directly because insurers price risk based on what they observe in your operations. The Hartford and ERGO NEXT explicitly factor safety documentation into underwriting decisions, supporting reductions of roughly 5 to 15 percent when you submit evidence of genuine risk management. Written protocols alone won’t move the needle-you need quarterly jobsite inspections, subcontractor liability requirements, training records, and incident logs submitted 60 to 90 days before your renewal date.

Contractors especially benefit from this approach because your industry already carries high baseline premiums; a documented safety program can yield meaningful savings and signals to underwriters that you operate differently than contractors with poor loss histories. Start by photographing your current safety practices, documenting near-misses, and recording employee training completion dates. When renewal arrives, submit this documentation with a cover letter explaining your risk reduction efforts. Underwriters review this material during the renewal evaluation and often approve lower rates than they would without it.

Bundle Policies to Unlock Multi-Line Discounts

Bundling general liability with property, workers’ compensation, and auto coverage yields 10 to 20 percent total savings across your policies while reducing certificate of insurance fees and administrative overhead. Request a bundled quote from at least two carriers-The Hartford typically offers competitive bundled pricing, and ERGO NEXT provides strong digital tools for managing multiple policies together.

Schedule Your Coverage Review at the Right Time

Schedule your annual coverage review 60 to 90 days before renewal, not on renewal day itself. During this window, verify that your exposure figures match your actual business (revenue, employee count, square footage), request a renewal quote breakdown showing the rate per thousand dollars of revenue, and compare quotes from multiple carriers side by side. Use the Washington Office of the Insurance Commissioner rate-change lookup tools to see what similar businesses in your county received approval for in recent renewals-this benchmarking prevents you from accepting inflated increases.

Challenge Unexpected Rate Increases With Data

If your renewal premium jumps unexpectedly, ask your carrier specifically what changed: whether it’s a carrier-wide rate increase, a surcharge tied to a prior claim, or a revised exposure calculation. Bring your documented safety improvements and competitive quotes to these conversations. A clean loss history provides genuine competitive advantage during negotiations, so even one year without claims strengthens your position for the next renewal cycle.

Final Thoughts

Washington general liability rates reflect measurable business realities: your industry classification, revenue, claims history, and location determine what you pay. Understanding these factors transforms your insurance from a line item on your budget into a strategic decision you can actively manage. A pressure washing business paying $1,000 monthly and a drone operator paying $19 experience different rates because their work carries genuinely different injury exposure, claim severity, and historical loss patterns.

What you control is how you respond to these realities. Documented safety programs reduce your premium by 5 to 15 percent because underwriters price risk based on observable evidence of your practices. Bundling policies yields 10 to 20 percent savings across your coverage, while reviewing your policy 60 to 90 days before renewal and gathering competing quotes prevents you from accepting inflated increases.

At FirstMark Insurance Group, we help Washington business owners navigate these complexities and find coverage that aligns with their actual risk profile and budget. Contact us to discuss your washington general liability rates and explore how we can optimize your coverage strategy.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation