Running a successful business in Seattle while managing substantial personal wealth demands more than standard insurance. You face unique risks that typical policies simply don’t address.

At FirstMark Insurance Group, we’ve built concierge client insurance specifically for leaders like you-those who need comprehensive protection without the administrative burden.

What Concierge Client Insurance Actually Is

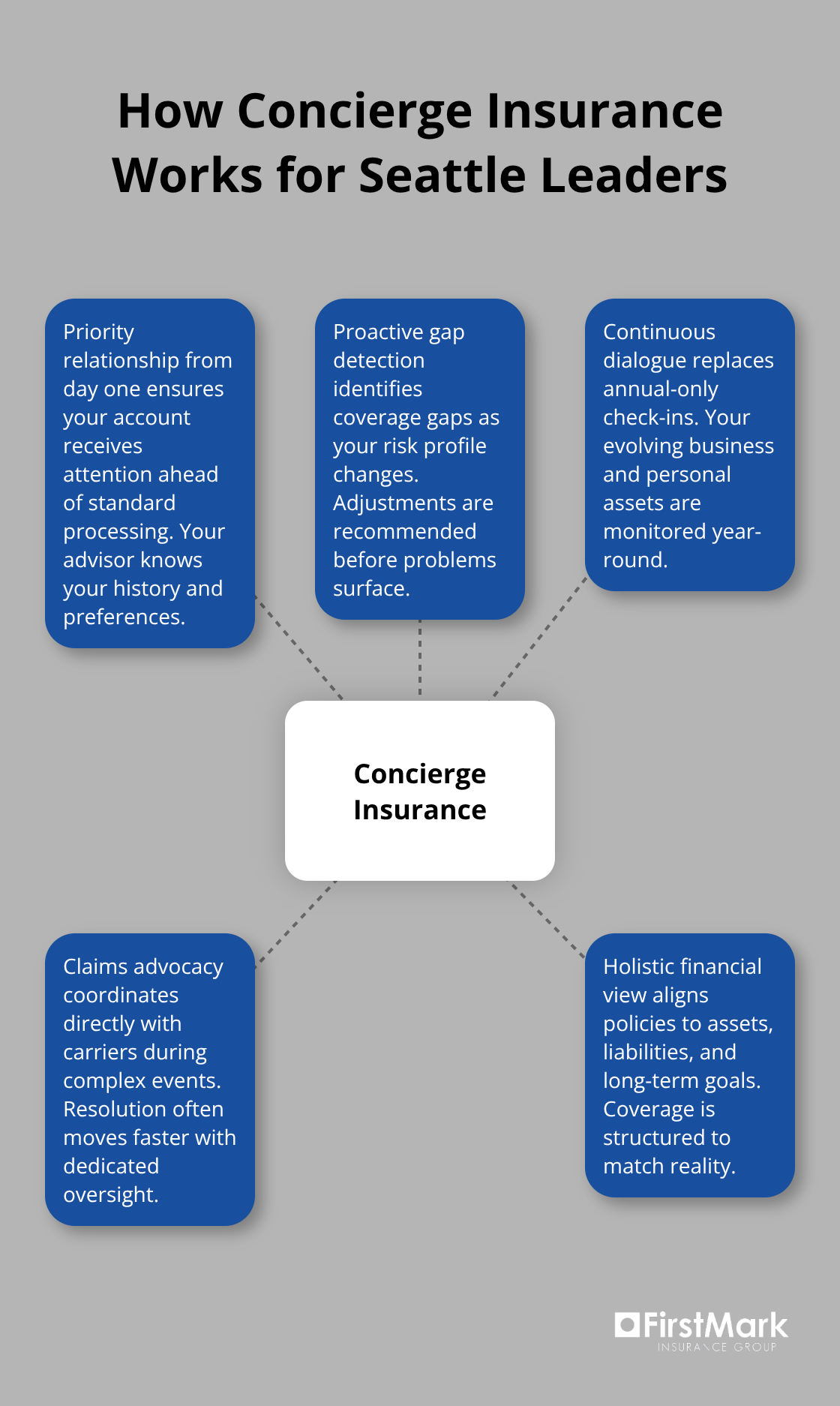

Concierge client insurance operates on a fundamentally different principle than standard coverage. Rather than a transactional relationship where you purchase a policy and contact your agent only when filing a claim, concierge insurance positions your account as a priority relationship from day one. This means your insurance advisor understands your full financial picture-your business structure, personal assets, liability exposures, and long-term wealth goals-and structures your coverage accordingly.

Busy leaders in Seattle need more than a policy document. They need someone who proactively identifies gaps, communicates changes in their risk profile, and adjusts coverage before problems surface. Standard insurance rarely works this way; most carriers treat clients identically regardless of their circumstances or sophistication. Concierge insurance rejects that model entirely.

The Real Difference in Risk Assessment

Standard policies rely on applications and annual renewals. Concierge insurance involves continuous dialogue. When you operate multiple businesses, hold real estate across Washington state, or manage significant personal wealth, your risks shift constantly-a new acquisition, a major hire, a property renovation, or a market downturn all affect your insurance needs.

Your existing policy likely contains blind spots if you’ve hired new employees, added a rental property, or changed your business operations. Concierge insurance catches those gaps before they become expensive problems. Rather than waiting for your annual renewal to discuss changes, your advisor stays informed about your evolving situation throughout the year and recommends adjustments that protect your interests.

Dedicated Support That Responds

Busy leaders don’t have time to chase down claims adjusters or decode policy language. Concierge service means your account receives priority attention, consistent communication, and a single point of contact who knows your history and preferences.

When you need a claim processed, you’re not one of thousands in a queue; your advisor handles coordination with carriers and ensures nothing falls through the cracks. This matters significantly when claims involve complex business interruption, professional liability, or substantial personal property losses. Claims that might take months to settle under standard policies often move much faster when your carrier knows you’re a priority account with dedicated oversight.

How Coverage Adapts to Your Life

Your insurance needs don’t remain static. A successful leader’s circumstances change-sometimes dramatically and sometimes subtly. Concierge insurance accounts for this reality by treating your coverage as a living document rather than a static contract.

When major life events occur (a business expansion, a significant acquisition, or a substantial change in personal assets), your advisor proactively reviews your protection and recommends updates. This approach prevents the common scenario where business owners discover coverage gaps only after a loss occurs. Your advisor stays ahead of your risks rather than reacting to them after the fact.

Priority Access When It Matters Most

Standard insurance relationships become transactional during claims. You contact a claims department, wait on hold, and navigate bureaucratic processes designed to handle high volume rather than individual circumstances.

Concierge service operates differently. Your dedicated advisor coordinates directly with carriers on your behalf, advocates for your interests, and ensures your claim receives appropriate attention. When substantial losses occur-whether business interruption, professional liability disputes, or major property damage-this level of support can significantly affect both resolution speed and outcome quality. The difference between standard and concierge claims handling becomes most apparent when complexity increases and time pressure mounts. As your business and personal wealth grow more sophisticated, your insurance relationship should grow more sophisticated as well.

Why Seattle Leaders Face Unique Insurance Complexity

Seattle’s business landscape creates a distinct set of insurance challenges that standard policies simply cannot address. High-net-worth individuals in the region typically operate across multiple income streams-a primary business, real estate holdings, investment portfolios, board positions, or advisory roles-each carrying separate liability exposures and coverage requirements. A tech executive who also owns rental properties across Washington state while serving on a nonprofit board faces risks that no single standard policy was designed to cover comprehensively. Insurance companies build their standard products around average risk profiles, which means they underestimate the exposures that sophisticated business owners actually carry. The result is coverage that looks adequate on paper but leaves dangerous gaps in practice.

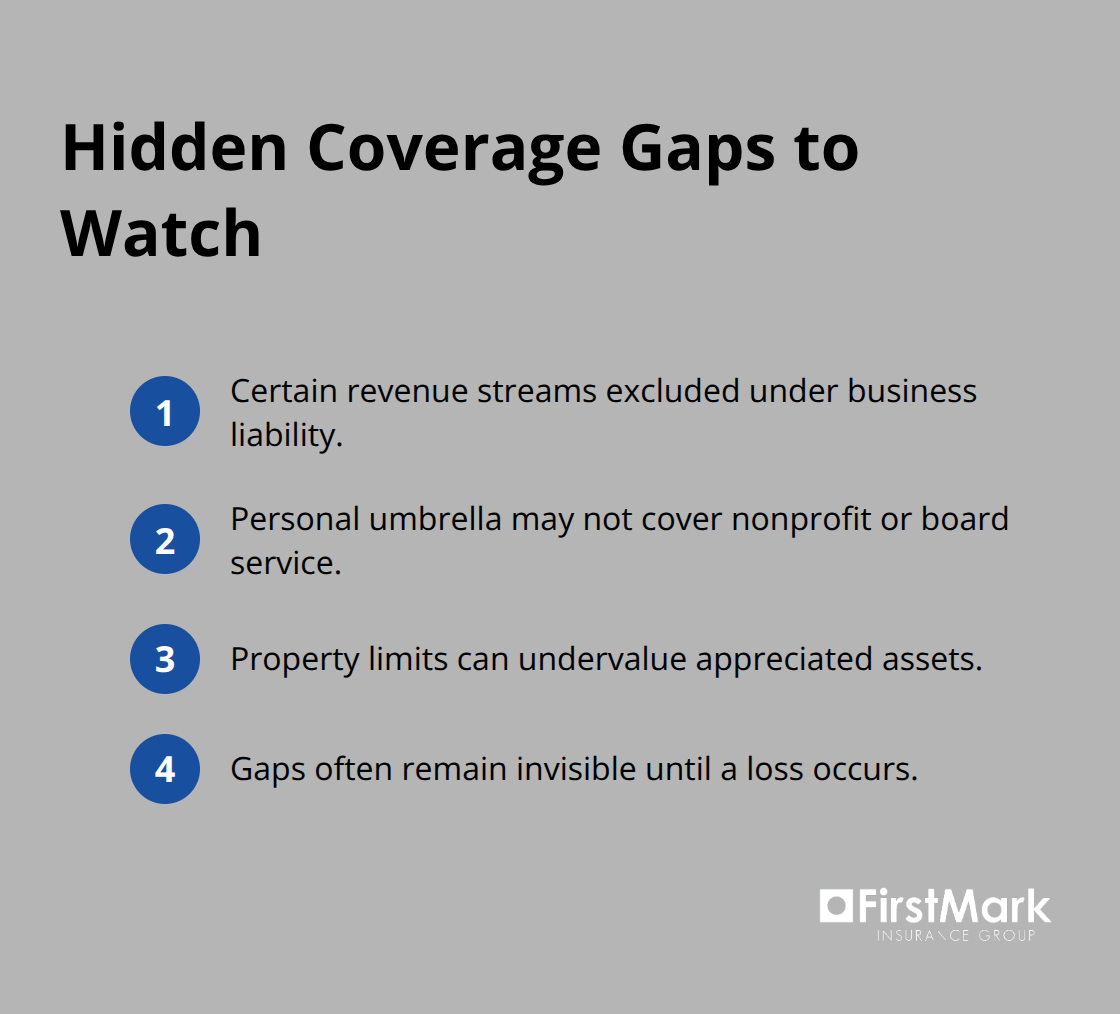

Coverage Gaps Hide Until Loss Strikes

Your business liability policy might exclude certain revenue streams. Your personal umbrella might not cover your board service. Your property coverage might undervalue assets that have appreciated significantly since your last renewal. These gaps don’t announce themselves until a loss occurs, which is far too late.

Standard insurance relationships demand that you stay organized enough to remember policy details, track coverage changes, and initiate conversations about your evolving risks. Most carriers treat clients identically regardless of their circumstances or sophistication, which means they miss the nuances that matter most to accomplished leaders.

Time Pressure Compounds Coverage Problems

The time cost of managing insurance properly compounds these coverage problems. A busy leader cannot reasonably spend hours researching carriers, comparing policy language, tracking regulatory changes, or monitoring whether coverage still matches current risk profile. When you manage business operations, family responsibilities, and financial complexity, insurance becomes one more administrative burden that consumes mental energy without generating revenue or meaningful personal satisfaction.

Rapid Changes Outpace Annual Renewals

A business acquisition, a major hire, or a property purchase changes your risk profile immediately, but standard policies don’t adapt until your next annual renewal. A tech executive who acquires a subsidiary operates for months with inadequate protection before the policy adjusts. A real estate investor who purchases a commercial building faces coverage gaps during the critical period between closing and renewal. Standard insurance relationships force your life to fit a static policy document rather than adapting the document to match your actual circumstances. This lag time creates exposure windows that can prove costly if losses occur during the interim period.

What Sophisticated Leaders Actually Need

Seattle’s most accomplished leaders need insurance that works as hard as they do, adjusting proactively to match their actual lives rather than forcing their circumstances into predetermined categories. Your advisor should track policy details and initiate conversations with you, not the reverse. This distinction matters most when your circumstances shift rapidly, and it separates concierge insurance from the transactional relationships that dominate the standard market. As your business and personal wealth grow more sophisticated, your insurance relationship should evolve accordingly-which is precisely why understanding how concierge service actually delivers that protection becomes essential.

How FirstMark Delivers Comprehensive Protection

Complete coverage audits Reveal Hidden Gaps

We at FirstMark Insurance Group approach each client relationship by starting with a complete audit of your existing coverage-not to rubber-stamp what you already own, but to identify what you’re actually missing. Most Seattle business leaders discover their first significant gap only after a loss occurs, which means they’ve been exposed for months or years without realizing it. Our process begins differently.

We map your full financial picture: business structure, real estate holdings across Washington state, board positions, investment portfolios, and personal assets. We then cross-reference this against your current policies line by line, testing for exclusions, coverage limits that haven’t kept pace with asset appreciation, and liability gaps between policies. A tech executive with a rental property and nonprofit board service typically carries three to five separate policies from different carriers, each with conflicting definitions of what they cover and what they exclude.

Consolidating Fragmented Coverage Into Strategy

We consolidate that fragmentation into a coordinated strategy where each policy supports the others rather than creating overlapping blind spots. This comprehensive review often reveals that standard policies undervalue appreciated assets, exclude revenue streams entirely, or carry liability limits designed for businesses half your size. Once we identify these gaps, we don’t simply recommend higher limits; we structure coverage that actually matches your risk profile rather than forcing your circumstances into predetermined categories.

Proactive Account Management Throughout the Year

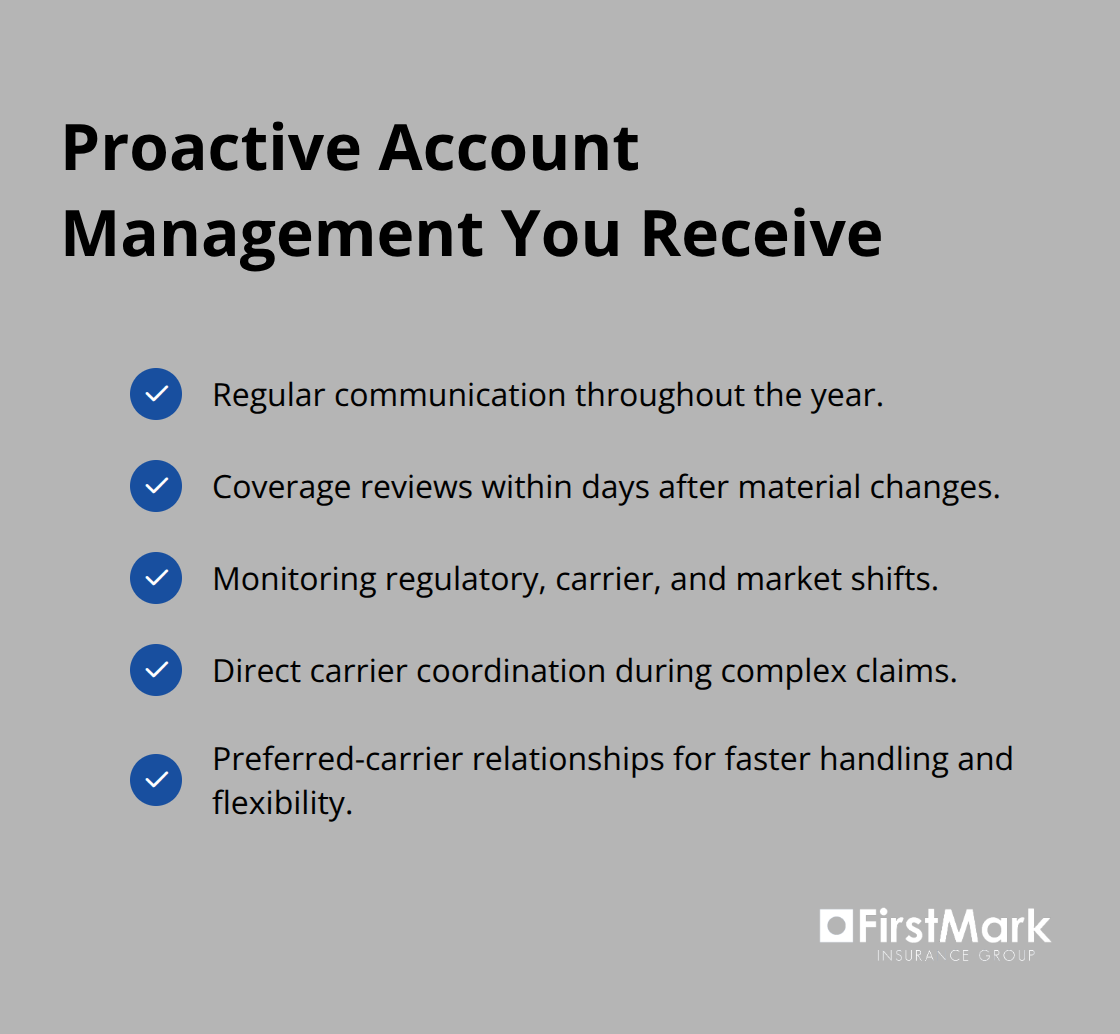

Proactive account management separates concierge service from transactional insurance relationships, and it’s where most agencies fail Seattle’s accomplished leaders. We maintain regular communication throughout the year-not waiting for your annual renewal to discuss changes. When you acquire a subsidiary, hire key employees, purchase commercial real estate, or experience other material changes to your risk profile, your account receives a coverage review within days, not months.

This approach prevents the exposure windows that plague standard policies, where you operate unprotected between a significant life change and your next renewal date. We also monitor regulatory changes, carrier updates, and market shifts that affect your protection, notifying you when adjustments make sense.

Direct Carrier Coordination During Claims

During claims, we coordinate directly with carriers on your behalf, ensuring complex situations receive appropriate attention rather than standard processing. A business interruption claim or professional liability dispute involving substantial exposure demands advocacy that standard claims departments simply cannot provide, and our involvement accelerates resolution while protecting your interests. We also leverage relationships with preferred carriers who recognize the value of sophisticated accounts and respond accordingly with faster claims handling, coverage flexibility, and competitive pricing that reflects your profile.

Final Thoughts

Concierge client insurance in Seattle addresses a real problem that standard policies ignore: busy leaders who operate across multiple business interests, real estate holdings, and investment portfolios need protection that adapts to their actual circumstances rather than forcing their lives into predetermined categories. Standard insurance relationships treat you like every other client, leaving dangerous gaps until losses occur, while concierge service means your advisor tracks your evolving risks throughout the year and recommends adjustments before exposure windows open. This distinction compounds significantly as your business and personal wealth grow more sophisticated, and it separates the relationships that protect accomplished professionals from the transactional arrangements that dominate the market.

We at FirstMark Insurance Group have spent 30 years guiding families and businesses through insurance complexity, and we’ve learned that the most successful leaders share a common need: they want someone who understands their full financial picture and protects it proactively rather than reacting after problems surface. Your coverage should adapt as your life changes, your advisor should stay informed about your evolving risks, and claims should receive priority attention when they matter most. This approach prevents the scenario where business owners discover coverage gaps only after a loss occurs.

If you manage a successful business in Seattle while juggling real estate holdings, board positions, or investment portfolios, your insurance relationship should reflect that complexity. FirstMark Insurance Group offers the personalized guidance and comprehensive coverage review that busy leaders need to protect what they’ve built, and we maintain regular communication throughout the year to keep your coverage aligned with your actual circumstances. Reach out to discuss your current coverage and identify gaps that standard policies have missed.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation