General liability insurance protects your Washington small business from costly lawsuits and property damage claims. Without proper coverage, a single incident could threaten your company’s financial stability and reputation.

Getting Washington general liability quotes from multiple providers helps you understand your options and find coverage that fits your business needs. At FirstMark Insurance Group, we guide small business owners through this process with clarity and expertise.

What General Liability Actually Covers

General liability insurance protects your Washington business against third-party claims for bodily injury and property damage. If a customer trips on your premises and breaks their arm, or your equipment damages a client’s property, this coverage pays for medical bills, legal defense, and settlement costs. The policy also covers personal and advertising injury claims-accusations that your marketing harmed someone’s reputation or violated their privacy rights. Most Washington small businesses carry limits of around one million dollars per occurrence, which handles typical incidents without exhausting your protection. However, contractors and cannabis businesses face higher mandates: contractors must meet minimum thresholds under RCW 18.27.050 with at least fifty thousand dollars in property damage and one hundred thousand dollars per person liability, while cannabis licensees under WAC 314-55-082 require one million dollars minimum with an A-minus rated insurer and the state named as additional insured.

Why Your Business Needs This Coverage Now

Washington does not legally mandate general liability for most small businesses, but this absence creates a dangerous misconception. Your landlord, clients, and contract partners will absolutely require proof of coverage before you occupy space or start work. A single lawsuit without insurance can bankrupt a small operation-legal defense costs alone can reach tens of thousands of dollars before any settlement. Washington’s pure comparative negligence framework means even partial fault on your part triggers liability, and the Insurance Fair Conduct Act encourages aggressive settlement negotiations that drive costs higher. Location matters significantly: King County and Pierce County premiums run thirty to fifty percent higher than rural areas due to higher verdict pools and medical costs, so a Seattle-based service business pays substantially more than an identical operation in rural Wahkiakum County. Your claims history follows you for years; a single prior claim can trigger surcharges that persist across multiple renewal periods, making early prevention far more economical than managing aftermath.

How Washington Regulations Shape Your Quote

Washington’s insurance environment reflects specific state risks that underwriters price into your quote. The state sits atop the Cascadia and Puget Sound fault lines, creating earthquake exposure that insurers account for in coastal and urban policies. Frequent rainfall and flood risk in many regions push underwriters to require additional endorsements or separate flood coverage through the National Flood Insurance Program, which caps structure coverage at five hundred thousand dollars and contents at five hundred thousand dollars. Licensed contractors cannot legally operate without minimum coverage, and the state suspends contractor registrations automatically if coverage lapses.

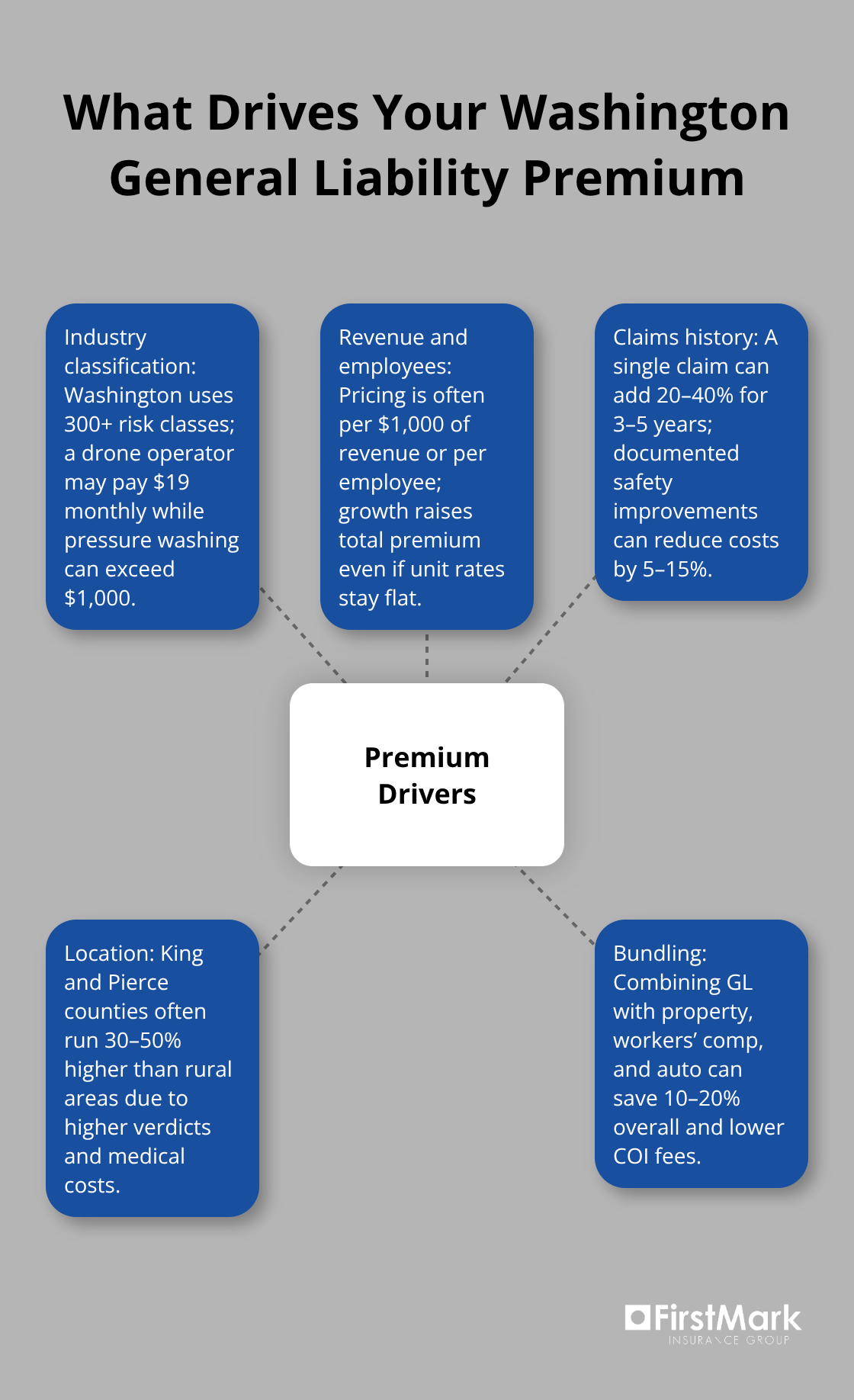

If you hire employees, Washington mandates workers’ compensation through the state fund or self-insurance; private insurers do not provide this coverage in Washington, which shapes how you bundle and price your total business insurance package. The state uses over three hundred risk classifications, meaning a drone operator might pay nineteen dollars monthly while a pressure washing business pays over one thousand dollars monthly-your specific industry classification drives your baseline rate far more than general size or location alone.

What Comes Next in Your Quote Process

Understanding what general liability covers and why Washington regulations matter sets the foundation for your next step: evaluating the specific factors that insurers examine when they calculate your individual quote. Your industry type, revenue, employee count, and claims history all influence the final premium you receive, and knowing how each factor works helps you prepare accurate information for quotes and identify opportunities to reduce costs before you apply.

Factors That Affect Your General Liability Quote

Industry Classification Drives Your Baseline Rate

Your Washington general liability premium lands on a specific number because underwriters assess your business against measurable risk factors, not guesswork. Industry classification dominates the calculation-Washington uses over three hundred distinct risk categories, and two businesses of identical size in different industries receive vastly different quotes. A drone operator pays nineteen dollars monthly while a pressure washing business pays over one thousand dollars monthly because pressure washing involves direct contact with client property, higher injury exposure, and historical loss patterns that underwriters price accordingly. Contractors average around two hundred ninety-one dollars monthly due to genuine exposure to property damage and bodily injury claims on job sites. The Hartford, the top general liability insurer in Washington, charges an average of ninety-three dollars monthly for a two-employee operation across many service industries, while ERGO NEXT runs about one hundred seventeen dollars monthly-but these figures shift dramatically based on your specific trade.

Revenue Growth and Employee Count Increase Your Premium

Your annual revenue and employee count matter because insurers often price per one thousand dollars of revenue or per employee, meaning revenue growth increases your total premium even if the per-unit rate stays flat. A business that grows from fifty thousand to one hundred thousand in annual revenue typically sees premium increases of twenty to thirty percent without any change in underwriting risk factors. This structure rewards early planning: when you anticipate revenue growth, you can adjust your coverage limits proactively rather than facing surprise increases at renewal.

Claims History Creates Long-Lasting Premium Impact

A clean loss history gives you negotiating leverage at renewal, while a single prior claim triggers surcharges that can persist for three to five years across multiple renewal periods, sometimes adding twenty to forty percent to your base premium depending on claim severity. Documentation of risk improvements submitted during your annual coverage review can reduce premiums by five to fifteen percent, which means investing in safety now directly lowers your costs later. The Hartford and ERGO NEXT explicitly factor safety documentation into underwriting decisions, so quarterly jobsite inspections, subcontractor liability requirements, training records, and incident logs create measurable value.

Location Within Washington Introduces Substantial Rate Variation

King County and Pierce County premiums run thirty to fifty percent higher than rural counties due to higher verdict pools, elevated medical costs, and more litigation activity under Washington’s pure comparative negligence framework. An identical business operating in Seattle versus rural Wahkiakum County receives dramatically different quotes from the same carrier because underwriters assess local market risk differently, and this variance is not primarily negotiable. Bundling general liability with property, workers’ compensation, and commercial auto yields ten to twenty percent overall savings and reduces certificate of insurance fees, making it the single most effective cost-reduction strategy for small businesses.

Getting Transparency in Your Quote Breakdown

When you obtain quotes, ask carriers for a detailed breakdown showing the rate per one thousand dollars of revenue and what changed from your prior year-this transparency reveals whether your increase stems from carrier-wide adjustments, prior-claim surcharges, or revised exposure figures, giving you concrete ground for negotiation or shopping alternative carriers. Understanding these specific factors positions you to take action before your next renewal and to evaluate which providers offer the best fit for your operation. The next step involves learning how to compare quotes effectively and work with an agent who understands Washington’s unique insurance landscape.

How to Secure Quotes That Match Your Business Reality

Request Multiple Quotes and Compare Systematically

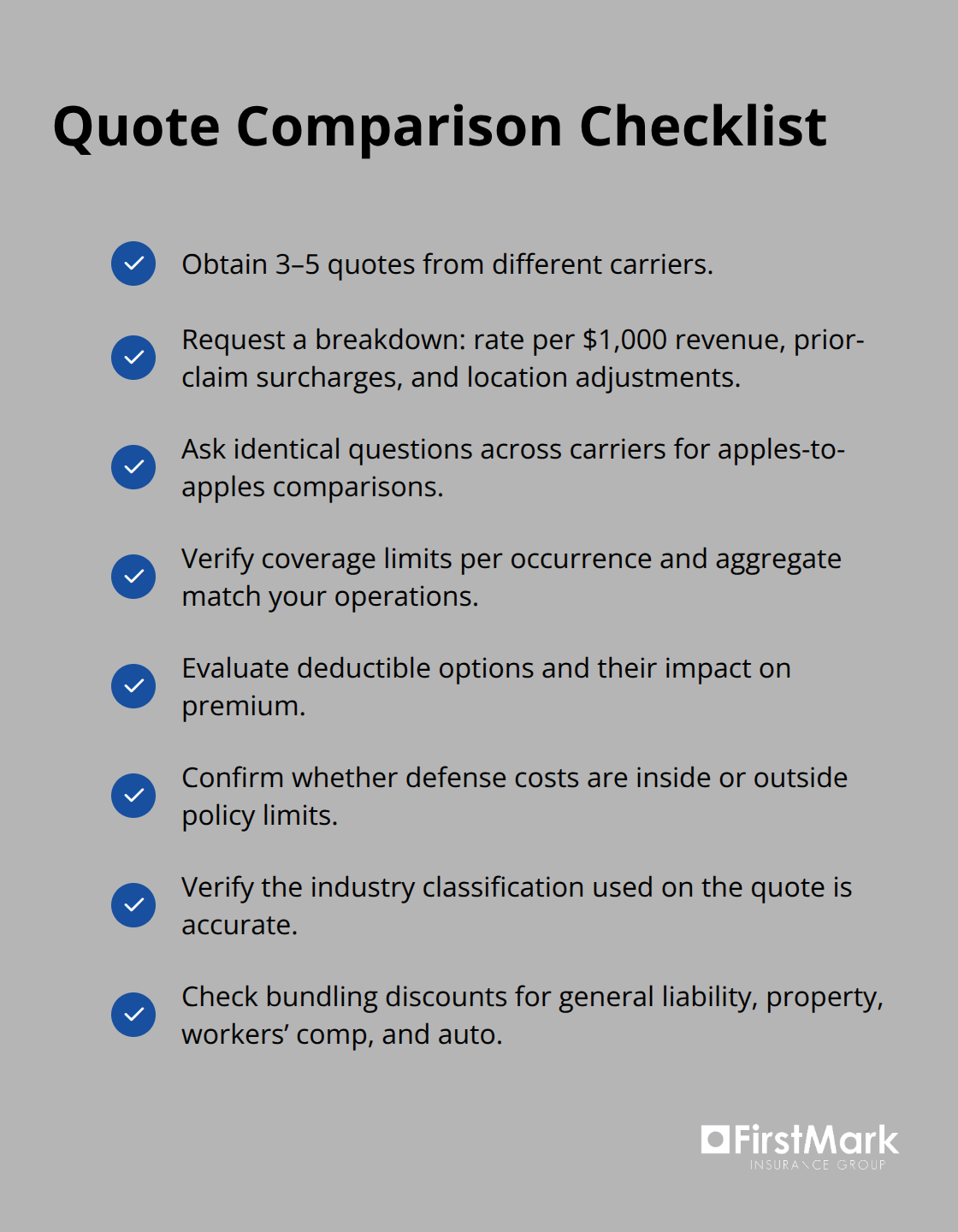

Obtaining three to five quotes from different carriers is non-negotiable if you want pricing that matches your business reality rather than a carrier’s generic assumptions. The Hartford averages ninety-three dollars monthly for small Washington operations, while Simply Business runs around one hundred nine dollars and Nationwide approximately one hundred eleven dollars, but these figures mean nothing until you see your own quotes side by side. When you request quotes, demand a detailed breakdown showing the rate per one thousand dollars of revenue, any prior-claim surcharges, location-based adjustments, and what changed from your previous policy year. This transparency exposes whether your increase stems from carrier-wide rate hikes affecting all customers or from underwriter decisions specific to your business. Many small business owners accept the first quote they receive and never discover they could pay thirty to forty percent less elsewhere, particularly if their claims history is clean or their industry carries lower risk than the initial carrier assumed.

Schedule your quote requests for sixty to ninety days before renewal so you have time to compare, negotiate, and switch carriers if necessary without coverage gaps. Ask each carrier the same questions in identical order so comparisons become straightforward: What are your coverage limits per occurrence and aggregate? What deductible options exist and how much do they reduce the premium? Are defense costs paid inside or outside your policy limits? Does the quote include the industry classification you disclosed? What discounts apply if you bundle general liability with commercial property, workers compensation, or commercial auto?

Understand Coverage Limits and Deductible Trade-Offs

Coverage limits and deductibles directly determine whether a cheap quote actually protects your business or leaves you exposed. Most Washington small businesses operate with one million dollars per occurrence and one million aggregate, which handles typical incidents without exhausting protection, but contractors and cannabis operations face mandatory higher limits under state law that you cannot negotiate downward. Your deductible choice creates a permanent trade-off: raising it from five hundred to two thousand five hundred dollars typically cuts your annual premium by ten to twenty percent, but only select this if you can genuinely absorb that deductible from operating cash without disrupting payroll or operations.

King County and Pierce County businesses often discover that bundling general liability with property, workers compensation, and auto yields ten to twenty percent overall savings compared to purchasing each policy separately, making bundling the single most effective cost-reduction strategy available to you.

Identify Coverage Gaps Before You Commit

When you work with an agent, insist on clarity about what your policy excludes because a cheap quote sometimes reflects exclusions that leave critical gaps. Ask whether professional liability, pollution coverage, or cyber insurance should supplement your general liability, particularly if you handle customer data or work near water sources where Washington’s hazardous materials regulations apply. An experienced agent understands which coverage combinations actually reduce your total risk and cost rather than creating a patchwork of inadequate policies that fails during a claim.

The agent should also document your current coverage limits and review them annually as your revenue grows or your service scope expands, because coverage that protected you at fifty thousand dollars in annual revenue may prove insufficient at one hundred fifty thousand dollars.

Final Thoughts

Washington general liability quotes reveal a straightforward truth: the cheapest option rarely matches your actual business needs. Industry classification, revenue, employee count, claims history, and location drive your premium far more than shopping for the lowest price, and a drone operator and a pressure washing business receive vastly different quotes because underwriters assess genuine risk exposure. Your claims history follows you for years, making prevention and documentation today directly lower your costs at renewal, while bundling general liability with property and workers compensation yields ten to twenty percent overall savings.

Schedule your quote requests sixty to ninety days before renewal so you have time to compare, negotiate, and switch carriers without coverage gaps. Ask each carrier identical questions about coverage limits, deductible options, whether defense costs sit inside or outside your limits, and what discounts apply for bundling, then verify that your coverage limits match your actual business size and service scope. Request clarity on exclusions and whether professional liability or cyber insurance should supplement your general liability, particularly if you handle customer data or operate near water sources.

We at FirstMark Insurance Group guide Washington small business owners through this process with expertise that simplifies insurance complexity and explores offerings from top providers. Contact FirstMark Insurance Group to begin your quote process with an agency that understands Washington’s unique insurance landscape and your business reality.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation