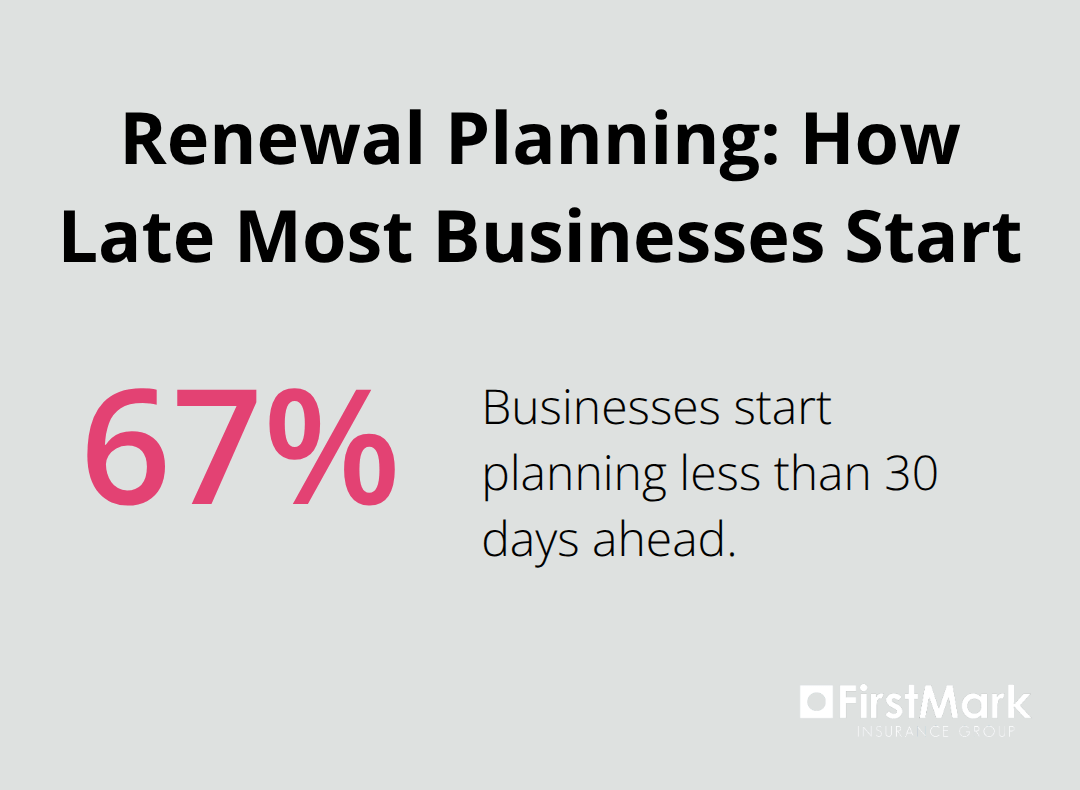

Business insurance renewals happen faster than most business owners expect. The average commercial policy renewal process begins 90 days before expiration, yet 67% of businesses start planning less than 30 days ahead.

We at FirstMark Insurance Group see companies miss significant savings opportunities because they treat renewals as routine paperwork. Smart preparation during the business insurance renewal process can reduce premiums by 15-25% while improving coverage quality.

When Do Insurance Renewal Deadlines Really Matter

Most insurance carriers send renewal notifications just 14-21 days before policy expiration, which creates artificial urgency that costs businesses money. This standard practice forces rushed decisions when premium negotiations require 60-90 days for optimal results. Insurance companies know that late-starting businesses accept higher rates because they fear coverage gaps, with new business having higher loss ratios and lower retention rates than renewal business.

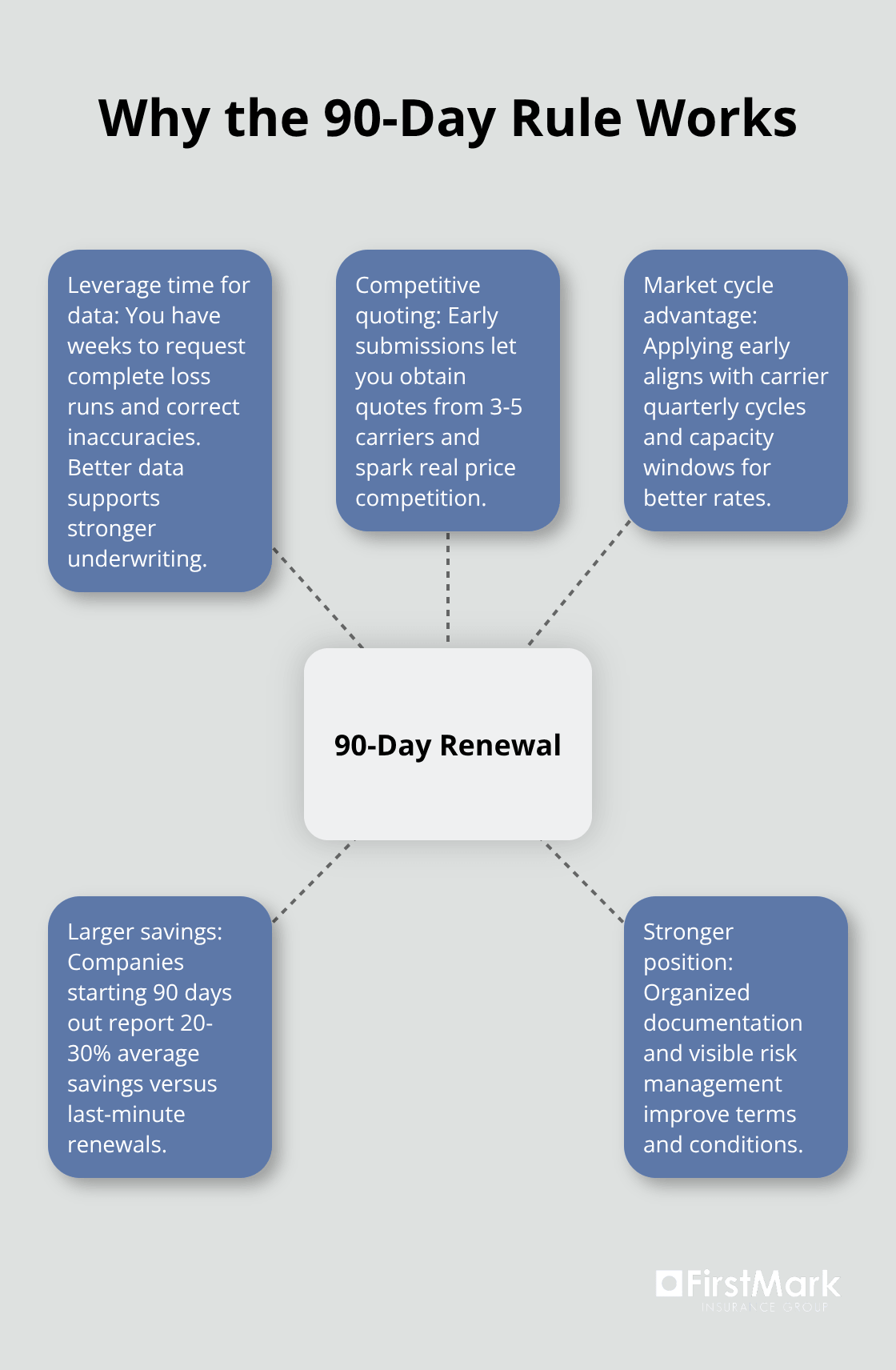

The 90-Day Rule Changes Everything

You transform your position completely when you start your renewal process 90 days before expiration. At this timeline, you can request detailed loss runs, gather comprehensive business updates, and secure competitive quotes from 3-5 carriers. Companies who follow the 90-day rule report average savings of 20-30% compared to last-minute renewals. The insurance market operates on quarterly cycles, and carriers allocate their best rates to early applicants who demonstrate serious risk management practices.

Market Conditions Drive Premium Changes More Than Claims

Insurance markets follow predictable seasonal patterns that directly impact your renewal rates. January renewals typically cost 8-12% more than July renewals due to increased demand and tighter carrier capacity. The P/C insurance industry experiences peaks and troughs in premium growth cycles that can significantly impact rates regardless of your claims history. Strategic businesses understand these market cycles and time policy changes to secure multi-year agreements during soft market periods, which locks in favorable rates before market conditions deteriorate.

Documentation Requirements Create Hidden Deadlines

Carriers require extensive documentation that takes weeks to compile properly. Financial statements, loss runs, employee records, and updated business descriptions all need current information that may not exist in your files. The process becomes more complex when you add new locations, services, or equipment during the policy term. Smart business owners maintain updated insurance files year-round rather than scramble to gather documents at renewal time.

Once you understand these timeline realities, the next step involves taking specific actions to review your current coverage and identify potential gaps.

How Do You Execute a Thorough Coverage Review

Your current insurance policies contain specific details that most business owners never examine closely. Coverage limits, deductibles, and exclusions change between policy periods, yet many businesses never thoroughly review their renewal documents. Start with your declarations pages and compare each coverage line against your actual business operations today versus when you first purchased the policy. Professional liability limits that seemed adequate at $1 million may now require $2-5 million based on new client contracts or expanded service offerings.

Coverage Gaps Appear When Business Operations Evolve

Equipment purchases, new locations, additional employees, and expanded services create immediate coverage gaps that many businesses miss until claims occur. Workers compensation requirements kick in after you hire your first employee in most states, while cyber liability becomes necessary once you store customer payment information. Commercial auto coverage needs updates when employees use personal vehicles for business purposes (which requires hired and non-owned auto endorsements). Review your business description section carefully because outdated language can void claims for new revenue streams or service categories.

Documentation Updates Require Systematic Preparation

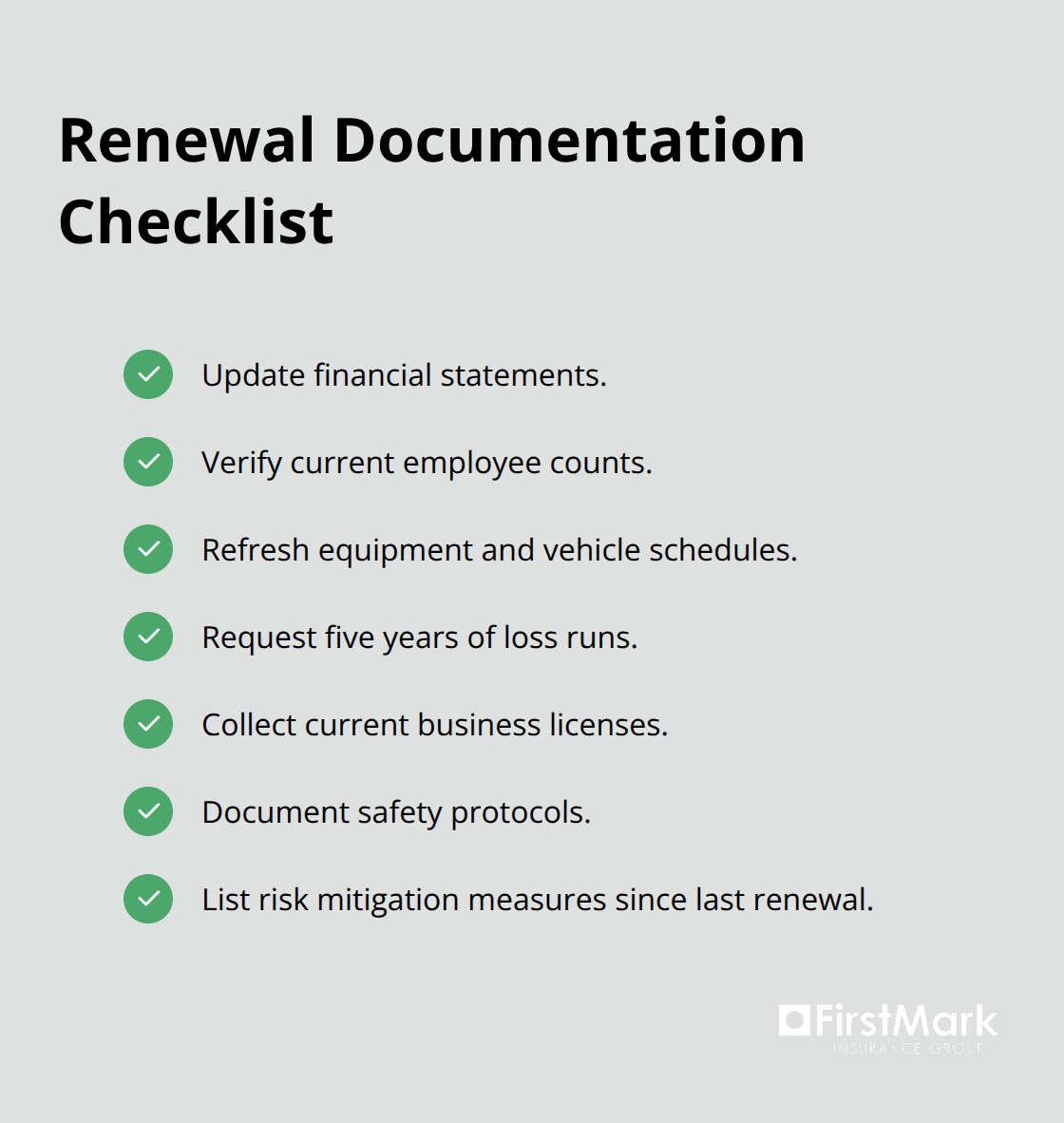

Financial statements from your accountant, updated employee counts, equipment schedules, and vehicle information must reflect current business reality. Carriers use this information to calculate accurate premiums and coverage limits, so outdated data costs money through incorrect pricing. Compile loss runs for the past five years, which show your claims history and help demonstrate improved risk management practices. Create a master file with current business licenses, safety protocols, and risk mitigation measures you have implemented since your last renewal.

Quote Comparison Demands Accurate Business Information

Carriers base their proposals on the data you provide rather than assumptions about your operations. Quote comparison becomes meaningless without accurate business information, as each insurer evaluates risk differently based on your current operations. Submit identical information to all carriers to receive comparable quotes that reflect true market pricing. Inconsistent data submissions (such as different revenue figures or employee counts) produce quotes that cannot be properly evaluated against each other.

These preparation steps set the foundation for the next phase: identifying common mistakes that derail even well-planned renewal processes.

What Renewal Mistakes Cost Your Business Money

Automatic policy renewals create the most expensive insurance mistakes businesses make today. Your insurance carrier assumes you accept their proposed rates when you ignore renewal communications, which eliminates any negotiation leverage you might have. Insurance companies deliberately price automatic renewals higher because they know passive customers rarely switch carriers. The process works against you from day one when carriers send renewal notices with inflated rates and expect pushback that never comes.

Business Changes Without Coverage Updates Void Claims

Revenue increases, new equipment purchases, and additional employees automatically change your risk profile in ways that standard policies cannot cover. Companies that grow from $500,000 to $2 million in annual revenue need higher liability limits, yet many businesses never update their coverage amounts. Professional liability insurance becomes inadequate when you add services to product sales, while cyber coverage requirements change completely when you start to process credit card payments. Equipment schedules must reflect current replacement costs rather than original purchase prices (as inflation affects claim settlements significantly).

Rate Shopping Timing Determines Available Options

Insurance markets operate on quarterly cycles that directly impact available rates and carrier appetite for new business. Fourth quarter renewals face the highest rates because carriers restrict capacity as they head into year-end, while second quarter renewals typically offer the most competitive prices. The time when you shop for rates determines which carriers will even provide quotes for your business type. Hard market conditions reduce carrier options by 30-40%, which makes early preparation the only way to secure competitive alternatives.

Businesses that wait until 30 days before expiration often find only one or two carriers who will provide coverage (this eliminates price competition entirely and forces acceptance of whatever terms get offered).

Documentation Delays Create Last-Minute Problems

Incomplete or outdated documentation forces carriers to make assumptions about your business that typically result in higher premiums. Financial statements, employee records, and equipment schedules require current information that may take weeks to compile properly. Carriers cannot provide accurate quotes without complete business information, which means rushed documentation leads to inflated pricing estimates. The process becomes more complex when you add new locations, services, or equipment during the policy term without proper documentation updates.

Final Thoughts

The business insurance renewal process demands strategic preparation that starts months before your policy expires. Companies that begin renewal preparation 90 days early secure 20-30% better rates while obtaining comprehensive coverage that matches their current operations. Market timing, thorough documentation, and systematic coverage reviews separate successful renewals from costly mistakes.

Professional insurance guidance transforms renewals from reactive paperwork into proactive risk management. We at FirstMark Insurance Group help businesses navigate market cycles and secure optimal coverage at competitive rates. Professional support becomes particularly valuable during hard market conditions when carrier options become limited and rates increase across all coverage lines.

Start preparation for your next renewal today by collecting current financial statements, updating equipment schedules, and documenting business changes since your last policy period (this foundation work prevents last-minute scrambles). Contact FirstMark Insurance Group to begin your renewal preparation process and secure the coverage your business needs at rates that fit your budget.