A single liability claim can devastate a Seattle business that lacks proper protection. Commercial general liability in Seattle isn’t optional-it’s the foundation of responsible risk management.

We at FirstMark Insurance Group help businesses understand what coverage actually protects them and what gaps could cost them everything. This guide walks you through the essentials.

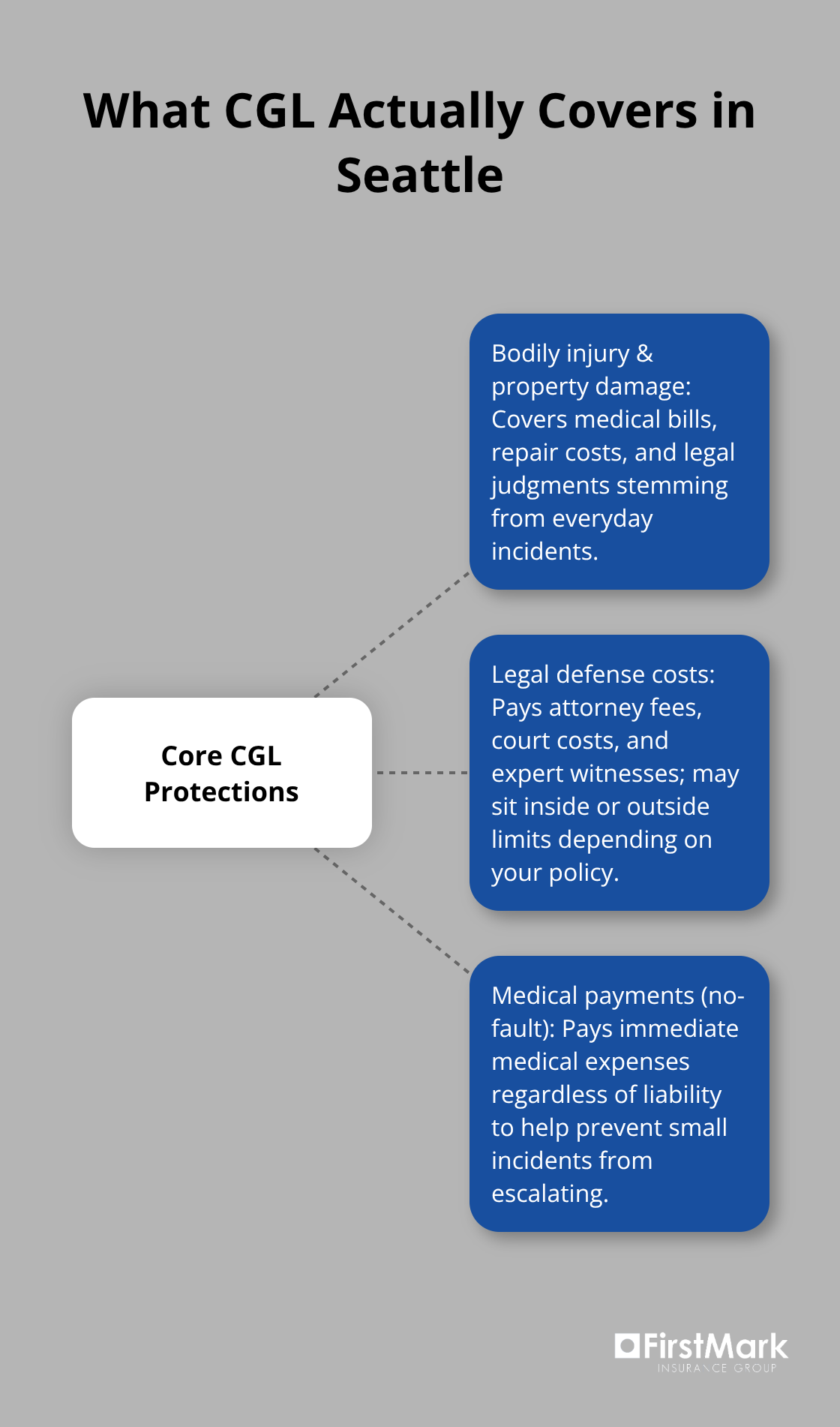

What Your Commercial General Liability Policy Actually Covers

Commercial general liability insurance protects your Seattle business from three primary financial exposures that arise from everyday operations. The first is bodily injury and property damage claims-when a customer slips on your premises, a delivery truck damages a client’s storefront, or an employee accidentally injures someone during work. Your policy covers medical expenses, repair costs, and legal judgments up to your chosen limits. The second protection addresses legal defense costs and court settlements. According to the Insurance Information Institute, CGL policies typically pay defense expenses separately from indemnity payments, meaning your insurer covers attorney fees, court costs, and expert witness fees even if a claim is ultimately dismissed. This distinction matters enormously in Seattle, where King County’s plaintiff-friendly litigation environment can drive defense costs significantly higher. The third component covers medical payments on a no-fault basis-if someone gets hurt at your business location, your policy pays their immediate medical bills regardless of liability, which often prevents smaller incidents from escalating into formal claims.

Understanding Your Coverage Limits in Practice

Most Seattle businesses start with $1 million per occurrence and $2 million aggregate limits, which covers typical slip-and-fall and property damage scenarios. However, your actual exposure depends entirely on your industry and customer interaction level. Construction contractors regularly need $2 million per occurrence because a serious injury on-site can easily exceed $1 million in medical costs and pain-and-suffering damages. Conversely, a marketing firm with minimal physical premises exposure might operate safely at lower limits. The critical error we see repeatedly is businesses that carry limits designed for higher-risk industries simply because they haven’t reassessed their actual exposure. A retail shop with $1 million coverage and annual revenue of $500,000 is likely overinsured, while a healthcare practice with the same limits is likely underinsured given the severity of potential medical malpractice crossover. Your policy’s aggregate limit-the total your insurer pays across all claims in one year-matters more than most business owners realize; once you hit that number, you remain uninsured for the remainder of the policy period.

Defense Costs and Real Financial Impact

The way your policy handles defense costs significantly affects your out-of-pocket exposure. Some policies include defense costs within your per-occurrence limit, meaning a $100,000 legal defense reduces your available settlement money to $900,000. Other policies pay defense costs outside the limits, protecting your full indemnity amount. In high-stakes Seattle litigation, this difference can mean $500,000 or more in additional protection.

You should specifically ask your insurer whether defense costs are inside or outside limits when you compare quotes. Additionally, your policy’s occurrence form versus claims-made structure matters; occurrence policies cover incidents that happen during your policy period regardless of when you report them, which is standard and preferable for most businesses. This protects you from coverage gaps if you switch insurers or let a policy lapse.

What Happens When Your Limits Fall Short

Your chosen limits determine your maximum protection, but they don’t tell the whole story about your actual financial exposure. A single catastrophic injury claim in Seattle can easily exceed $2 million when you factor in medical costs, lost wages, pain and suffering, and punitive damages in a plaintiff-friendly jurisdiction. Many business owners discover too late that their standard limits leave them personally liable for amounts above their policy ceiling. An umbrella policy extends your protection beyond your base CGL limits and typically costs far less than you’d expect-often $300 to $500 annually for an additional $1 million in coverage. This additional layer becomes especially important if your business involves customer interaction, employees working off-site, or any activity with significant injury potential. Your industry classification and loss history directly influence both your base premium and your umbrella policy cost, so the investment in higher limits often reflects your actual risk profile more accurately than standard limits alone.

Why Seattle Businesses Need This Coverage

Seattle’s geography and legal environment create liability exposures that most business owners underestimate until a claim arrives. Western Washington’s heavy rainfall drives slip-and-fall incidents across retail, hospitality, and service businesses at rates significantly higher than drier regions. The Pacific Northwest’s seismic activity adds earthquake-related liability exposure that standard commercial general liability policies typically exclude, forcing many Seattle businesses to purchase separate endorsements or standalone earthquake coverage. King County’s litigation environment compounds these physical risks; the area ranks among the nation’s most plaintiff-friendly jurisdictions, meaning medical awards and settlement amounts trend substantially higher than national averages. A bodily injury claim that might settle for $150,000 in a conservative market can easily reach $400,000 or more in King County, making your chosen policy limits directly connected to your actual financial exposure rather than theoretical scenarios.

Washington State Requirements and Contract Demands

Washington State does not mandate commercial general liability insurance the way it requires workers’ compensation for businesses with employees, but that absence of legal requirement masks a critical business reality. Your landlord, major clients, and contractors will demand proof of coverage through certificates of insurance before allowing you on their premises or engaging your services. Contracts worth tens of thousands of dollars routinely fail to execute because a business lacks adequate CGL documentation. More importantly, a single lawsuit can eliminate years of profit and force personal asset liquidation if you operate as a sole proprietor or LLC without sufficient insurance.

Industry-Specific Exposure and Claim Severity

Construction contractors face the highest exposure; a serious injury on-site can generate medical costs exceeding $500,000 before accounting for lost wages and pain-and-suffering damages that Seattle juries award generously. Healthcare providers, childcare facilities, and any business with regular customer or visitor traffic face similar severity exposure. The financial devastation from an uninsured claim extends beyond the immediate settlement amount to include legal fees that can reach six figures even in cases that ultimately succeed.

Matching Coverage to Your Actual Risk

Your industry classification and loss history directly influence both your base premium and your overall protection strategy. Construction work demands higher limits than office-based professional services, yet many business owners carry identical coverage across different risk profiles. The gap between standard limits and realistic claim scenarios in Seattle’s legal environment often leaves businesses dangerously underinsured. Understanding your specific exposure allows you to select limits that actually protect your assets rather than defaulting to industry templates that may not fit your operations.

As you assess your coverage needs, the next critical step involves determining the right limits for your business size, industry, and revenue level.

Sizing Coverage to Match Your Business Reality

The gap between standard coverage limits and your actual financial exposure in Seattle often determines whether a liability claim depletes your reserves or devastates your business entirely. Construction contractors operating in the region should carry minimum $2 million per occurrence limits because a single serious injury claim routinely exceeds $1 million when medical costs, lost wages, and Seattle jury awards combine. Healthcare practices, childcare facilities, and any business with regular customer traffic face similar severity exposure that demands limits well above the $1 million baseline most small businesses default to.

How Industry Classification Shapes Your Limits

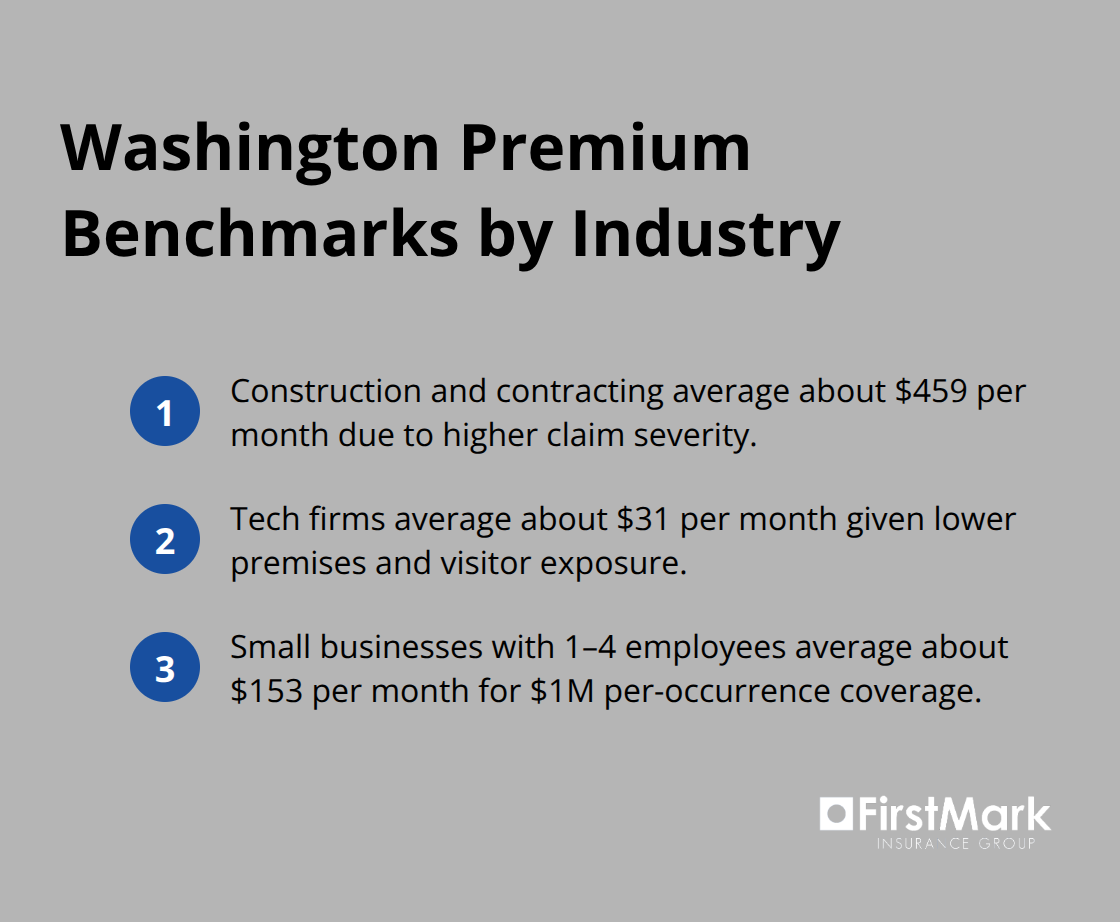

Your industry classification drives this calculation more than any other factor. According to pricing data across Washington State, construction and contracting businesses average $459 monthly premiums precisely because claim severity is exponentially higher than tech firms averaging $31 monthly. A tech startup with minimal physical premises and no customer traffic can operate safely at $1 million per occurrence limits; a contractor cannot.

The critical error occurs when business owners assume industry templates apply to their specific operation without examining actual exposure.

A retail shop with $500,000 in annual revenue and minimal employee count may be overinsured at $1 million limits, while that same limit leaves a healthcare provider dangerously exposed. Your policy’s aggregate limit-the total your insurer pays across all claims during one policy year-matters equally; once exhausted, you remain completely uninsured for the remainder of your policy period regardless of new claims. Selecting limits requires honest assessment of your worst-case scenario, not comfortable assumptions about what probably won’t happen.

Revenue, Assets, and Defense Cost Realities

Revenue and asset value provide the second critical measurement for your coverage limits. A business with $2 million in annual revenue and $500,000 in equipment and inventory cannot afford limits that leave personal assets exposed above the policy ceiling. Defense costs in serious Seattle litigation frequently reach substantial amounts before any settlement occurs, meaning your chosen limits must accommodate both legal defense and actual indemnity payments.

Small businesses with 1 to 4 employees in Washington average $153 monthly premiums for $1 million per occurrence coverage, while adding a first employee more than doubles that premium to reflect increased exposure. Your actual comparison must evaluate identical policy terms across multiple providers because quote variance outside major metro areas can be pronounced. Request quotes specifying whether defense costs sit inside or outside your per-occurrence limit, since this distinction can represent significant real financial protection.

Bundling Strategies and Quote Comparison

Many Seattle businesses discover that bundling general liability with property coverage through a Business Owner’s Policy produces substantially lower combined costs than purchasing standalone policies, sometimes reducing total annual premiums by 15 to 25 percent. Your actual comparison must evaluate identical policy terms across multiple providers because quote variance outside major metro areas can be pronounced. When you request quotes, specify whether defense costs sit inside or outside your per-occurrence limit-this distinction can represent significant real financial protection.

We at FirstMark Insurance Group work with top insurance providers to present you with choices that fit your requirements at the best available pricing, helping you navigate these comparisons and ensure your limits genuinely reflect your exposure rather than defaulting to industry templates that may leave you underinsured or unnecessarily overprotected.

Final Thoughts

Commercial general liability in Seattle protects your business from financial devastation when claims arrive, but only if your coverage limits match your actual exposure. The gap between standard limits and realistic claim scenarios in King County’s plaintiff-friendly environment often determines whether a serious incident depletes your reserves or forces personal asset liquidation. Your industry classification, revenue level, and customer interaction frequency should drive your limit selection far more than industry templates or comfortable assumptions about what probably won’t happen.

Honest assessment of your worst-case scenario matters far more than defaulting to $1 million per occurrence limits that may leave you dangerously exposed or unnecessarily overprotected. Request quotes from multiple providers specifying identical policy terms, including whether defense costs sit inside or outside your per-occurrence limit. Evaluate whether bundling general liability with property coverage through a Business Owner’s Policy produces lower combined costs than standalone policies, and consider an umbrella policy if your business involves customer interaction, employee work off-site, or significant injury potential.

We at FirstMark Insurance Group bring extensive experience guiding businesses through these exact decisions, working with top insurance providers to present you with choices that fit your requirements at the best available pricing. Rather than pushing you toward unnecessary overprotection or leaving you underinsured, we help you select limits that genuinely reflect your exposure and your financial capacity. Contact us today to discuss your specific situation and secure the commercial general liability Seattle coverage your business actually requires.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation