Owning a vacation home in Washington brings freedom and flexibility, but it also exposes you to liability risks that standard homeowners policies often miss.

At FirstMark Insurance Group, we’ve seen too many seasonal property owners discover coverage gaps only after a guest is injured or damage occurs. Vacation home liability in WA requires specialized protection that goes beyond what a typical policy provides.

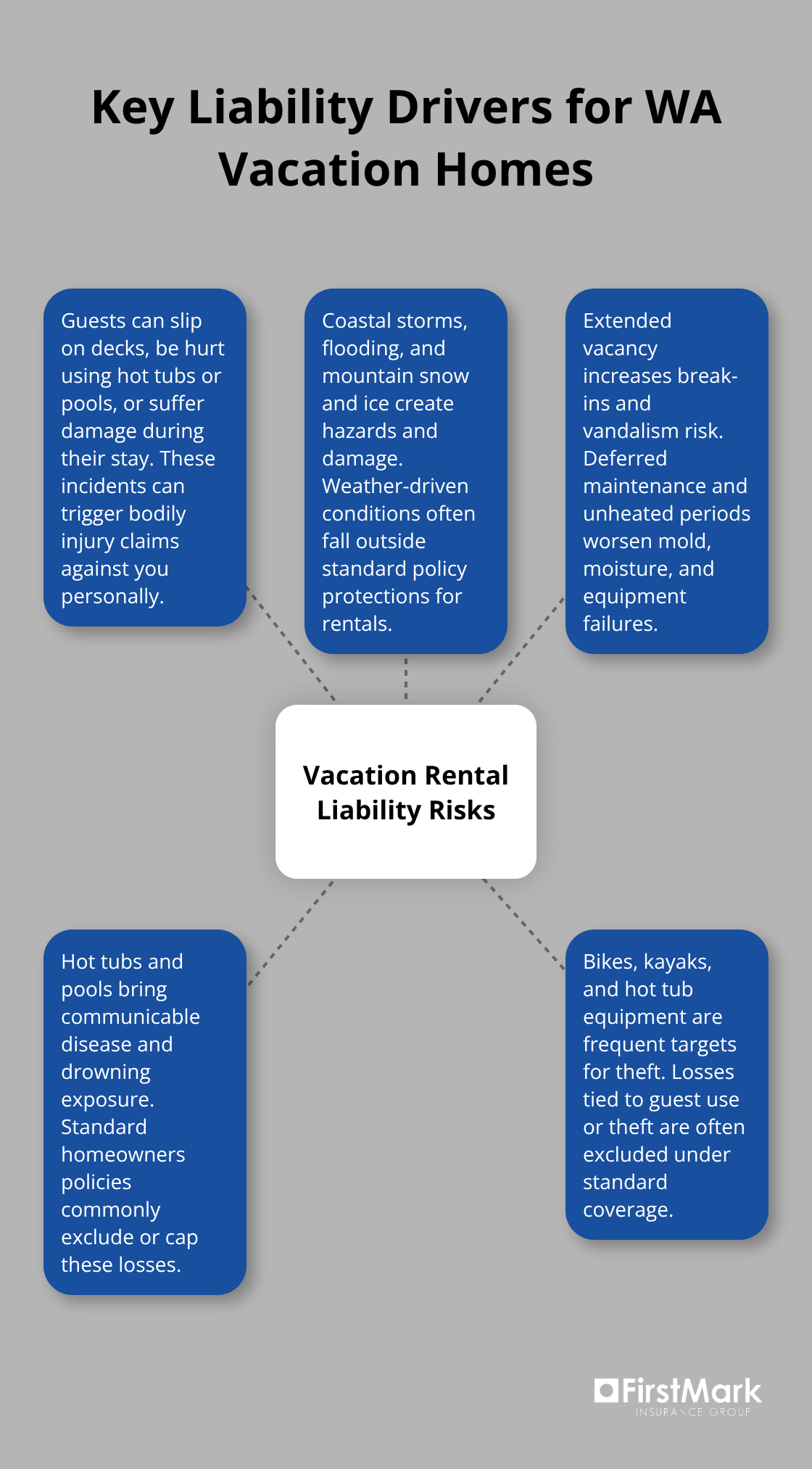

What Liability Risks Come With Seasonal Property Ownership

Guest Activity Creates Exposure Beyond Standard Policies

Seasonal properties in Washington face distinct liability exposures that differ significantly from primary residences. The core issue is that guests-whether paying renters, friends, or family-create injury and damage scenarios that standard homeowners policies exclude or severely limit. When someone slips on your deck in Leavenworth, injures themselves on amenities like hot tubs or pools, or suffers property damage during their stay, your standard policy may deny the claim outright because it treats the property as a rental business rather than a personal residence. The distinction matters legally and financially. A guest injured at your vacation home can pursue a bodily injury claim against you personally, and courts in Washington hold property owners to a premises liability standard that requires you to maintain reasonably safe conditions or warn guests of known hazards. This means you’re liable not just for negligence on your part, but for conditions on the property itself that cause injury.

Washington’s Weather Amplifies Seasonal Risks

Weather and environmental conditions specific to Washington amplify these risks considerably. Properties in coastal areas like Ocean Shores face storm surge, flooding, and water damage that can destroy guest belongings and create liability when water intrusion damages a guest’s possessions or causes injury. Mountain properties around Chelan and Leavenworth experience heavy snow load, ice dam formation, and avalanche risk that standard policies often exclude or cap at minimal limits. Seasonal properties also sit vacant for extended periods, which increases exposure to break-ins, vandalism, and theft of guest amenities like bikes, kayaks, or hot tub equipment-exposures that fall outside typical homeowners coverage.

The Compounding Effect of Vacancy and Maintenance

Property damage from weather isn’t the only concern; when a guest is injured due to inadequate snow removal, a collapsed deck from snow load, or a hot tub malfunction tied to freezing temperatures, you face both property repair costs and personal injury liability. Washington’s rainy climate also creates mold and moisture damage risks that accelerate when properties remain unheated or poorly maintained during off-season months. The combination of guest activity, extended vacancy, and harsh seasonal conditions creates a liability environment that requires coverage specifically designed for vacation properties. Standard homeowners protection leaves you exposed to claims that specialized vacation home policies address directly, which is why understanding your actual coverage needs matters before a loss occurs.

Where Standard Homeowners Policies Fall Short

Rental Activity Triggers Coverage Exclusions

Your standard homeowners policy was designed for a primary residence where you live year-round and control who enters the property. The moment you introduce guest activity-whether through short-term rentals, extended family visits, or seasonal use-that policy becomes inadequate. Most homeowners policies explicitly exclude or severely restrict coverage for rental operations, which means a paying guest transforms your property from a covered dwelling into an uninsured business operation in the eyes of your insurer. When a guest slips on your deck in Port Angeles or suffers a burn from an unattended hot tub, your standard policy will likely deny the claim because the injury occurred during rental activity. Courts in Washington recognize this distinction sharply; a guest injured on a rental property can pursue bodily injury claims that standard policies treat as business liability rather than personal premises liability.

Coverage Limits Fall Far Short of Real Claims

The coverage limits also fail to match vacation home exposure. Most homeowners policies cap liability at $100,000 to $300,000, while a serious guest injury claim easily exceeds $500,000 when medical expenses, lost wages, and pain and suffering are included. Property damage coverage gaps are equally problematic; theft of guest amenities like kayaks or bikes, damage to guest belongings during their stay, and liability for damage guests cause to neighboring properties fall outside standard coverage or are excluded entirely when the property is rented.

Specialized Vacation Rental Policies Address What Standard Policies Miss

Vacation home liability requires commercial general liability coverage specifically designed for short-term rental operations. This coverage addresses guest bodily injury, property damage, personal injury claims from invasion of privacy, and off-property liability when guests use amenities like community pools or bikes tied to your rental experience. Additional protections for bed bug infestations, liquor liability, and property entrustment (theft and vandalism by guests) are standard in vacation rental policies but completely absent from homeowners coverage.

Hot Tubs and Pools Create Uninsured Exposure

Washington vacation properties face particular exposure from hot tubs and pools, which generate communicable disease claims and drowning liability that standard policies exclude or cap severely. If you rent your property through Airbnb or Vrbo, platform protection like AirCover provides some coverage but leaves significant gaps-these protections typically cap at $1 million and exclude many business-related exposures that a dedicated vacation home policy covers.

The Real Cost of Operating Without Proper Coverage

The practical reality is that attempting to operate a seasonal rental under a standard homeowners policy exposes you to claims that your insurer will deny, leaving you personally liable for guest injuries and property damage that specialized coverage would address. Understanding what your current policy actually covers-and what it excludes-is the first step toward identifying the protection gaps that could affect your financial security. The next section examines the specific liability limits and additional protections you actually need to operate a vacation property safely in Washington.

What Coverage Limits Actually Protect Your Vacation Home

Why $100,000 Falls Short for Vacation Properties

A $100,000 liability limit offers false security until a guest suffers a serious injury on your property. In Washington, a slip-and-fall claim with hospitalization, surgery, and ongoing physical therapy routinely exceeds $500,000 when you factor in medical expenses, lost wages, and pain and suffering damages. A drowning incident at a vacation rental property can trigger claims exceeding $2 million when a child is involved, and Washington courts consistently award substantial damages for preventable injuries on rental properties. Your standard homeowners policy maxes out far below this threshold, leaving you personally responsible for the difference. If a guest suffers a $750,000 injury claim and your policy caps at $300,000, you face $450,000 in personal liability that could attach to your home, savings, and future income.

Recommended Liability Limits for Vacation Rentals

A minimum of $1 million in commercial general liability coverage protects vacation properties adequately, with $2 million if your property includes high-risk amenities like hot tubs, pools, or waterfront access. This reflects the actual cost of defending and settling real claims rather than theoretical estimates. Properties with multiple high-risk features warrant the higher limit because a single serious incident can exhaust $1 million in coverage quickly. An insurance professional who understands Washington’s vacation rental market helps you select limits matched to your actual exposure, not generic coverage that leaves gaps when claims arrive.

Property Entrustment and Guest-Related Theft

Property entrustment coverage protects against theft and vandalism by guests-kayaks, bikes, and hot tub equipment routinely disappear during guest stays. Standard policies treat these losses as your negligence rather than guest criminal activity, leaving you uncompensated. Vacation rental policies address this exposure directly, covering the financial loss when guests steal or damage your amenities.

Specialized Protections for Rental Operations

Bed bug and flea infestations generate six-figure claims when guests suffer bites and subsequent infestations spread to their homes, yet most homeowners policies exclude pest liability entirely. Liquor liability coverage proves essential because leftover alcohol creates liability if a guest becomes intoxicated and injures themselves or others-platform protections like AirCover exclude alcohol-related claims. Business revenue protection covers your lost rental income when a covered claim forces you to close the property for cleaning, repairs, or legal proceedings, typically paying actual income loss with no time limit. Communicable disease liability tied to hot tubs addresses Legionnaires’ disease and similar claims that escalate in cost when multiple guests become ill.

Final Thoughts

Vacation home liability in Washington exposes you to financial risks that standard homeowners policies simply do not address. Guest injuries, property damage, theft of amenities, and specialized claims like bed bug infestations or liquor-related incidents create a liability environment that requires coverage specifically designed for seasonal properties. A $100,000 policy limit offers no real protection when a serious guest injury claim reaches $500,000 or more, and platform protections like AirCover leave significant gaps that leave you personally liable for the difference.

The path forward requires honest assessment of your actual exposure. If your property includes a hot tub, pool, or waterfront access, your liability risk increases substantially. If you rent through Airbnb or Vrbo, your standard homeowners policy actively excludes the rental activity that creates your greatest exposure. If your property sits vacant for months, weather damage and theft of guest amenities fall outside typical coverage limits.

Securing adequate protection means moving beyond standard homeowners coverage to a commercial general liability policy with minimum $1 million in limits, property entrustment coverage for guest theft, and specialized protections for bed bugs, liquor liability, and business revenue loss. An insurance professional who understands vacation rental operations helps you select limits and coverages matched to your specific property and rental model rather than generic protection that fails when claims arrive. Contact FirstMark Insurance Group to review your current coverage, identify gaps, and secure the protection your vacation home liability in WA actually requires.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation