Running a horse farm means managing significant liability exposure. Whether you breed, board, or train horses, accidents happen-and they can be costly.

At FirstMark Insurance Group, we’ve seen firsthand how the right equine farm liability coverage protects your operation when injuries or property damage occur. This guide walks you through what you need to know.

What Your Equine Liability Policy Actually Covers

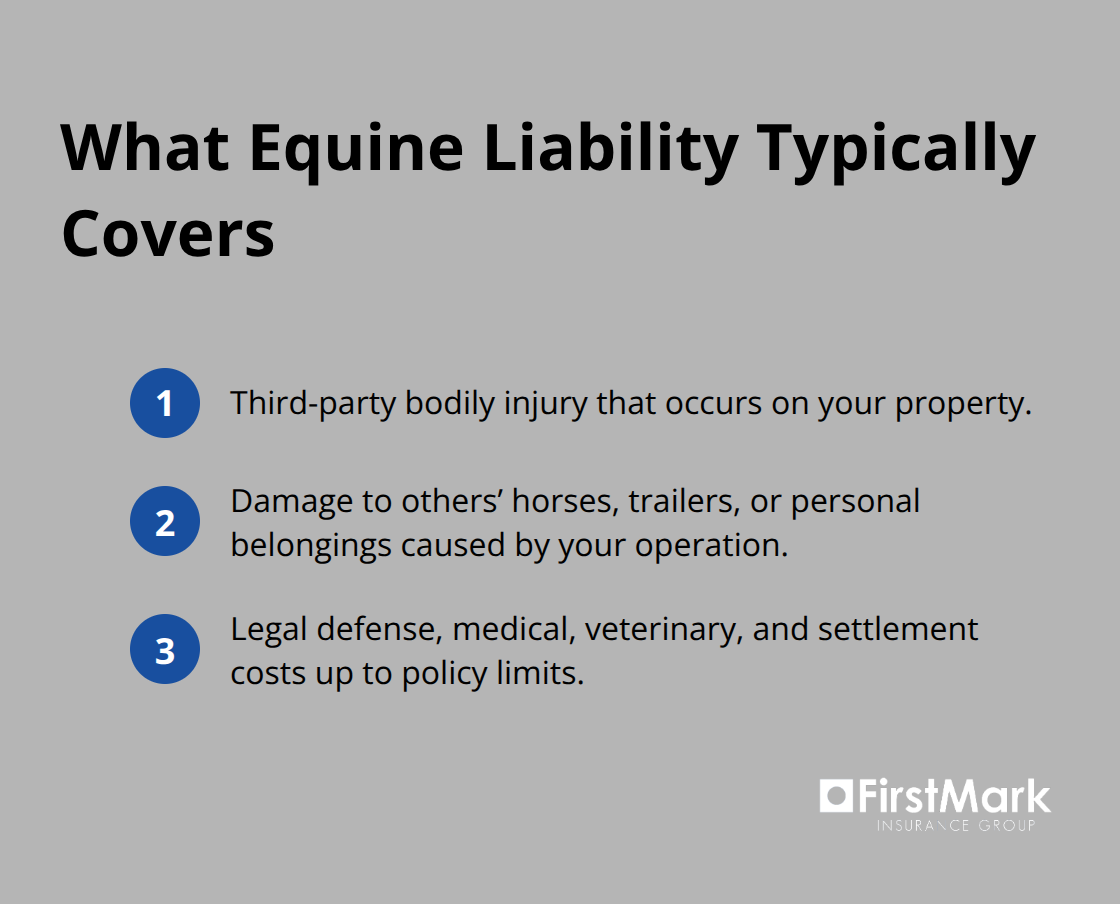

Equine farm liability insurance protects you when someone is injured on your property or when your operation causes damage to someone else’s horse or belongings. This differs fundamentally from property insurance, which covers your own buildings and equipment. Liability coverage pays for third-party claims-injuries or damage involving people or animals not owned by you. If a client’s horse suffers injury during boarding, if a visitor receives a kick while touring your facility, or if your trainer damages equipment belonging to a horse owner, liability coverage steps in to cover medical expenses, veterinary bills, legal defense, and settlement costs.

Understanding Policy Limits and Coverage Amounts

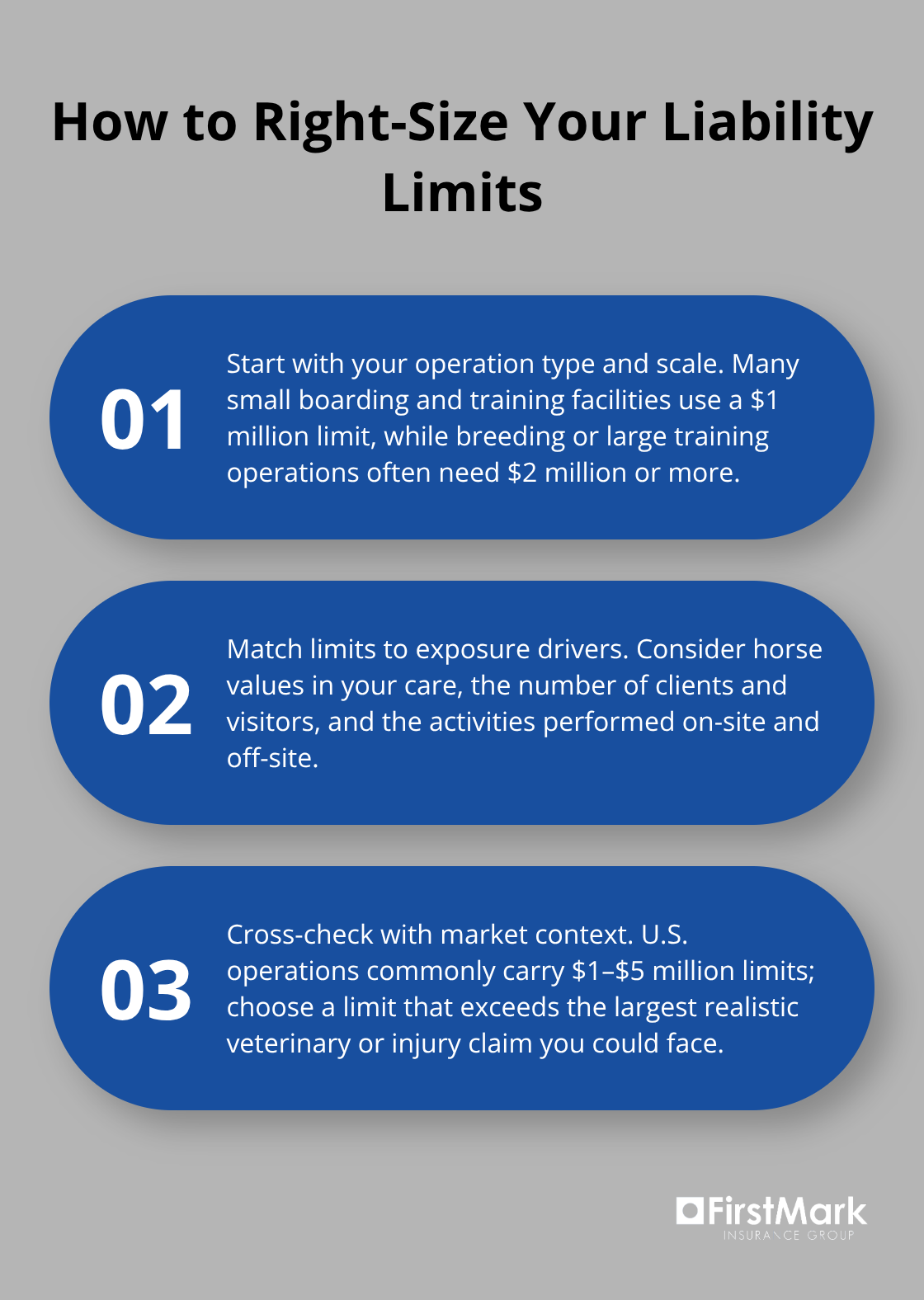

The policy limits you select directly determine how much the insurer will pay. A $1 million liability limit is standard for most boarding and training operations, though breeding facilities with higher-value stock often carry $2 million or higher. The global horse insurance market reached USD 1 billion in 2025 and is projected to grow to USD 2.05 billion by 2035, reflecting rising demand for comprehensive liability protection as operations expand and legal exposure increases. Your chosen limit should reflect the value of horses in your care and the number of third parties who interact with your facility regularly.

Third-Party Injury and Medical Coverage

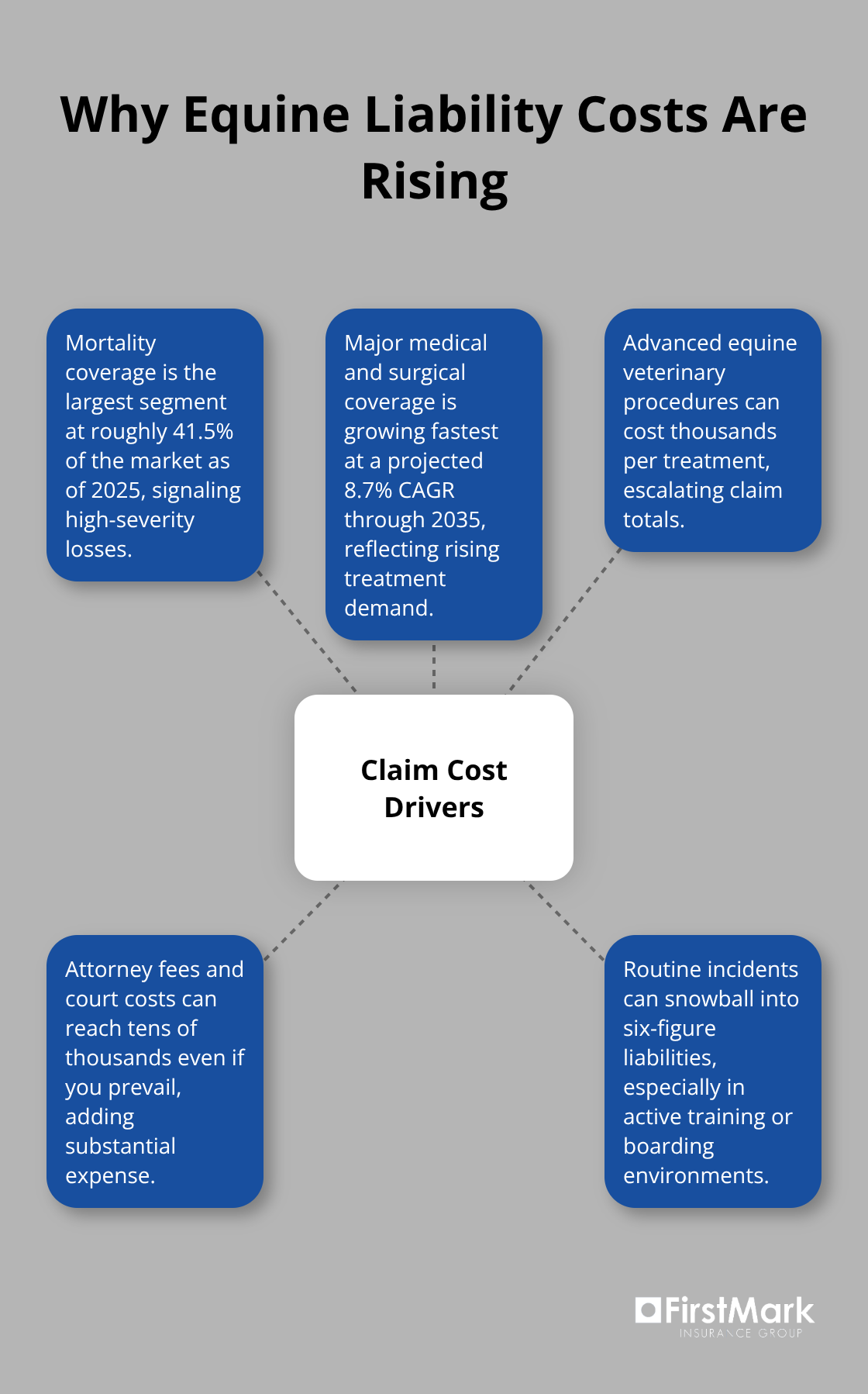

When someone is injured at your farm, liability coverage pays their medical expenses and related costs up to your policy limit. This includes veterinary bills if a client’s horse is hurt in your care. Care, Custody, and Control coverage (commonly called CCC) specifically fills gaps in standard liability by protecting you from liability for horses you don’t own but have responsibility for during boarding, training, or breeding arrangements. Without CCC, your standard general liability policy may not cover a client’s horse that dies or suffers severe injury while in your care. CCC coverage typically covers medical treatment, euthanasia costs, and replacement value, though limits are often modest and may not match the value of valuable horses. If you board or train high-value animals, obtaining mortality insurance for clients’ horses becomes critical because CCC alone may leave significant gaps. Legal defense costs remain separate from settlement amounts, meaning the insurer pays your attorney fees and court costs regardless of whether you lose the case-costs that can easily reach tens of thousands of dollars if litigation proceeds to trial.

Facility Damage and Property Liability

Your liability coverage also protects you if your operation damages someone else’s property. If a client’s trailer sustains damage in your facility, if your farm causes environmental contamination, or if your equipment injures someone’s vehicle, liability coverage responds. However, this does not cover damage to your own buildings, fences, or equipment. For that protection, you need farm property insurance, which covers structures like barns and sheds against fire, windstorm, and theft. The U.S. horse insurance market accounted for roughly USD 372.4 million in 2025, with liability and multi-line coverage representing a growing share as farms recognize that property and liability work together to create comprehensive protection.

Named Additional Insured Endorsements

Named additional insured endorsements are increasingly required by facility owners and boarding operations. This means adding another party (such as your boarding facility) to your policy so they also receive liability protection from your coverage. This protects the facility from claims arising from your training or boarding activities on their premises. Verify with your facility or clients that you meet their insurance requirements, as many require proof of coverage and specific endorsement language before allowing you to operate on their property. Understanding these requirements upfront prevents coverage gaps and ensures all parties have the protection they expect.

What Actually Happens When Things Go Wrong on Your Farm

Horse operations expose you to risks that extend far beyond what most farm owners anticipate. Injuries occur regularly in boarding facilities, training yards, and breeding operations-and they carry substantial financial consequences. A rider thrown during a lesson, a client’s horse that colics while in your care, a barn fire that damages neighboring property, or a visitor kicked by a horse can trigger liability claims that reach into six figures. The data supports this reality: mortality coverage remains the largest segment of equine insurance at roughly 41.5 percent of the market as of 2025, but major medical and surgical coverage is growing fastest at a projected 8.7 percent compound annual growth rate through 2035, indicating that veterinary costs for horses in your care have become a primary concern for facility operators.

This growth reflects the rising cost of equine veterinary care, which includes advanced treatments that can cost thousands of dollars per procedure.

Third-Party Injuries in Breeding Operations

The most common liability exposure in breeding operations stems from injuries to visiting owners or prospective buyers touring your facility. A prospective buyer sustains a bite from a stallion, an owner’s child receives a kick in a paddock, or a veterinarian suffers injury during a breeding procedure-each represents a direct third-party claim against your operation. These incidents happen quickly and often without warning, leaving you exposed to medical bills, legal defense costs, and potential settlements that can reach tens of thousands of dollars.

Boarding and Training Exposures

Boarding facilities face different but equally serious exposures. A client’s horse dies from colic or injury while in your care, a boarder’s family member sustains a serious fall, or a rider’s equipment suffers damage during a lesson. Training operations carry layered exposure because you control both the activity and the horse simultaneously-if a client’s horse suffers a career-ending injury during training, the owner may pursue damages for loss of use or replacement value, which for performance horses can exceed $50,000. Standard general liability policies often exclude or severely limit coverage for horses in your care, which is precisely why Care, Custody, and Control coverage exists. Without CCC coverage explicitly added to your policy, a dead or injured client’s horse may fall outside your liability protection entirely, leaving you personally responsible for replacement costs or veterinary bills that can reach $30,000 to $100,000 for valuable animals.

Environmental and Property Damage Claims

Environmental hazards create additional liability exposure. Manure runoff contaminates a neighbor’s property, your facility causes water pollution, or a hay storage fire spreads to adjacent land-each scenario triggers third-party property damage claims. Facility damage liability also includes situations where your operation injures someone else’s vehicle or equipment: a client’s expensive trailer sustains damage in your facility parking area, or a veterinarian’s equipment suffers harm during care procedures. These claims accumulate quickly and often involve multiple parties seeking compensation.

Multi-Location Operations and Coverage Gaps

Multi-location operations face compounded exposure because coverage gaps can emerge across different premises. A horse transported to a show or clinic may not be covered under your facility’s property coverage, and third-party liability may not extend to off-site activities unless your policy explicitly includes transit and off-premises training coverage. This fragmentation of protection creates blind spots that leave you vulnerable. Understanding where your coverage ends and where exposures remain unprotected becomes essential as your operation expands across multiple locations or involves activities beyond your primary facility.

Building Coverage That Matches Your Operation

Selecting the right equine liability coverage requires moving beyond standard policy templates and matching protection directly to how your farm operates. The differences between a boarding facility, a training operation, and a breeding farm create distinct exposures that demand different coverage structures. A boarding facility primarily faces liability when clients’ horses suffer injury in your care or when visitors sustain injuries on your premises. A training operation carries additional exposure because you control both the activity and the horse, meaning a client’s horse injured during a lesson creates liability for loss of use or replacement value. A breeding operation confronts different risks entirely: prospective buyers touring your facility, visiting owners, and veterinarians performing breeding procedures all represent third-party exposures that standard general liability policies may not adequately address.

Assess Your Operation’s Specific Activities and Exposures

Your first step is honest assessment of which activities dominate your operation and which third parties interact with your farm regularly. Count the number of boarders, clients, and visitors monthly. Document the types of activities occurring: lessons, breeding procedures, show preparation, or veterinary work. Identify the value of horses typically in your care. This information becomes your foundation for selecting appropriate policy limits. A $1 million limit works for most small boarding and training operations, but breeding facilities with high-value stock or large training operations should carry $2 million or higher. The U.S. horse insurance market reached USD 372.4 million in 2025 according to Global Market Insights, with most of that revenue flowing to operations carrying limits between $1 million and $5 million. Your limit should exceed the maximum veterinary bill or injury claim you could realistically face at your facility.

Identify Coverage Gaps and Exclusions

Beyond selecting a limit, you must understand what your policy excludes and where gaps emerge. Care, Custody, and Control coverage must be explicitly added to your general liability policy-it does not exist as standalone coverage. Without CCC, a client’s horse that dies or suffers severe injury while boarding at your facility may fall entirely outside your liability protection. Similarly, if you train at another facility, verify that the facility’s insurance covers your training activities or that your own policy extends to off-premises training. Multi-location operations require explicit coverage for each location and for transit between locations.

Ask your insurer whether your policy covers horses transported to shows or clinics. Verify whether event-day coverage applies if you host clinics or shows, including setup and takedown periods when injuries frequently occur. Review whether your policy covers leasing arrangements if you lease horses to clients. These exclusions matter because they represent real exposures that remain unprotected.

Work with Specialized Equine Insurance Advisors

Specialized equine risk advisors recognize that breeding, boarding, and training operations carry exposures that generic farm policies miss entirely. Request quotes from insurers experienced in equine operations rather than general agricultural providers. Ask potential insurers whether they offer infertility protection for breeding stock, mortality coverage for clients’ horses, and transit insurance for movement of your stock. These endorsements transform basic liability coverage into comprehensive protection aligned with how your operation actually functions. Experienced advisors map your specific activities against policy language and identify where standard coverage falls short. This consultative approach prevents the costly surprise of discovering after a claim that your policy did not cover the activity that caused the injury.

Final Thoughts

Equine farm liability coverage protects what matters most to your operation. Whether you breed, board, or train horses, the right policy structure addresses your specific exposures and prevents financial devastation when injuries or property damage occur. Standard general liability policies leave critical gaps for horse operations, which is why Care, Custody, and Control coverage, appropriate policy limits, and specialized endorsements become non-negotiable components of comprehensive protection.

The foundation of sound equine farm liability rests on honest assessment of your activities and the third parties who interact with your facility. A boarding operation faces different exposures than a training facility or breeding farm, and your coverage must reflect those distinctions. Policy limits should exceed the maximum veterinary bill or injury claim you could realistically face, while named additional insured endorsements protect facility owners and clients who require proof of coverage before allowing you to operate on their premises.

The cost of inadequate coverage extends far beyond insurance premiums-a client’s horse valued at $50,000 that dies in your care, a visitor’s serious injury, or environmental damage claims can reach six figures when legal defense costs accumulate. At FirstMark Insurance Group, we understand that equine farm liability requires more than a generic farm policy, and we work with top insurance providers to match your coverage to your actual operation. Contact FirstMark Insurance Group to discuss your equine operation’s specific exposures and build protection that reflects how your farm actually functions.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation