One mistake we see professionals make is underestimating their exposure to liability claims. A single lawsuit can threaten your business, your reputation, and your financial stability.

Professional liability coverage in Washington protects you against claims of negligence, errors, or inadequate work. At FirstMark Insurance Group, we help businesses understand what protection they actually need and how to get it right.

What Professional Liability Insurance Actually Protects

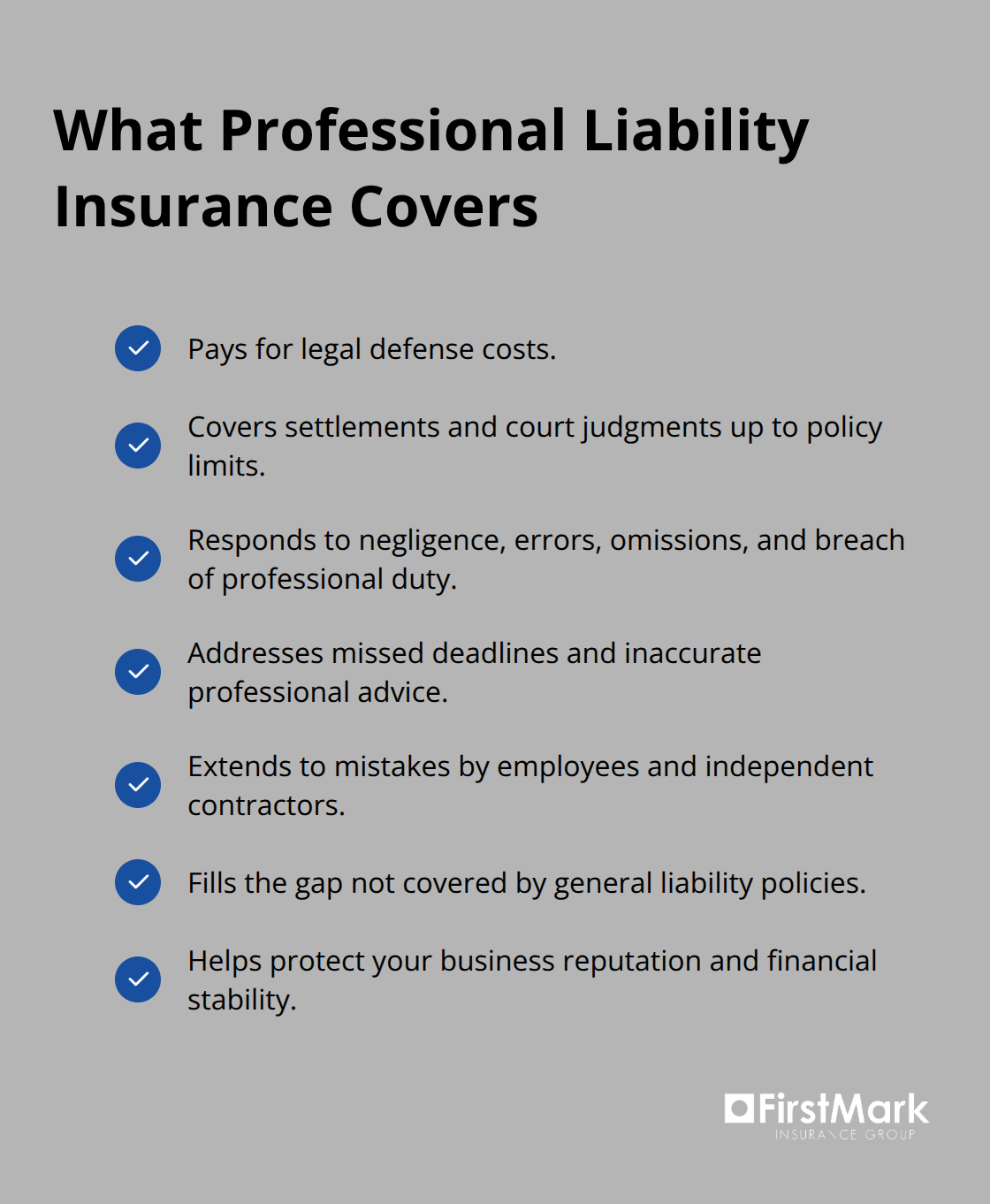

Professional liability insurance covers claims alleging that you failed to perform your work competently or that your advice caused financial harm to a client. This includes negligence, errors, omissions, and breach of professional duty. The coverage pays for legal defense costs, settlements, and judgments up to your policy limits. When a client sues claiming you missed a deadline, gave incorrect advice, or made a mistake in your work product, this policy steps in to cover those costs. It also covers mistakes made by your employees and independent contractors, which means your exposure extends beyond just your own actions. According to Insureon, common claims covered include negligence, work mistakes, missed deadlines, and inaccurate professional advice. What makes this protection essential is that general liability insurance does not cover professional liability. Your commercial general liability policy explicitly excludes claims arising from the quality of your professional work, leaving a dangerous gap if you rely on it alone.

Who Actually Needs This Coverage

Professional liability claims affect far more than attorneys and doctors. IT consultants and software developers face significant exposure when systems fail or data is mishandled. Architects and engineers encounter claims over design flaws or structural problems. Real estate agents deal with claims about mislisting properties or failing to disclose issues. Accountants face allegations of tax preparation errors. Financial advisors are sued over investment advice. Technology professionals, consultants, insurance professionals, and even graphic designers and interior decorators encounter professional liability exposure. Washington state does not legally require professional liability insurance for most professions, but your contracts, clients, or professional licenses may demand it. Many banks, franchises, and institutional clients require proof of coverage before engaging your services. If you sign client agreements, those contracts often include minimum coverage requirements. The reality is that one claim can cost more to defend than years of premiums, making the decision to skip coverage a financial gamble.

Claims Take Years and Cost More Than You Think

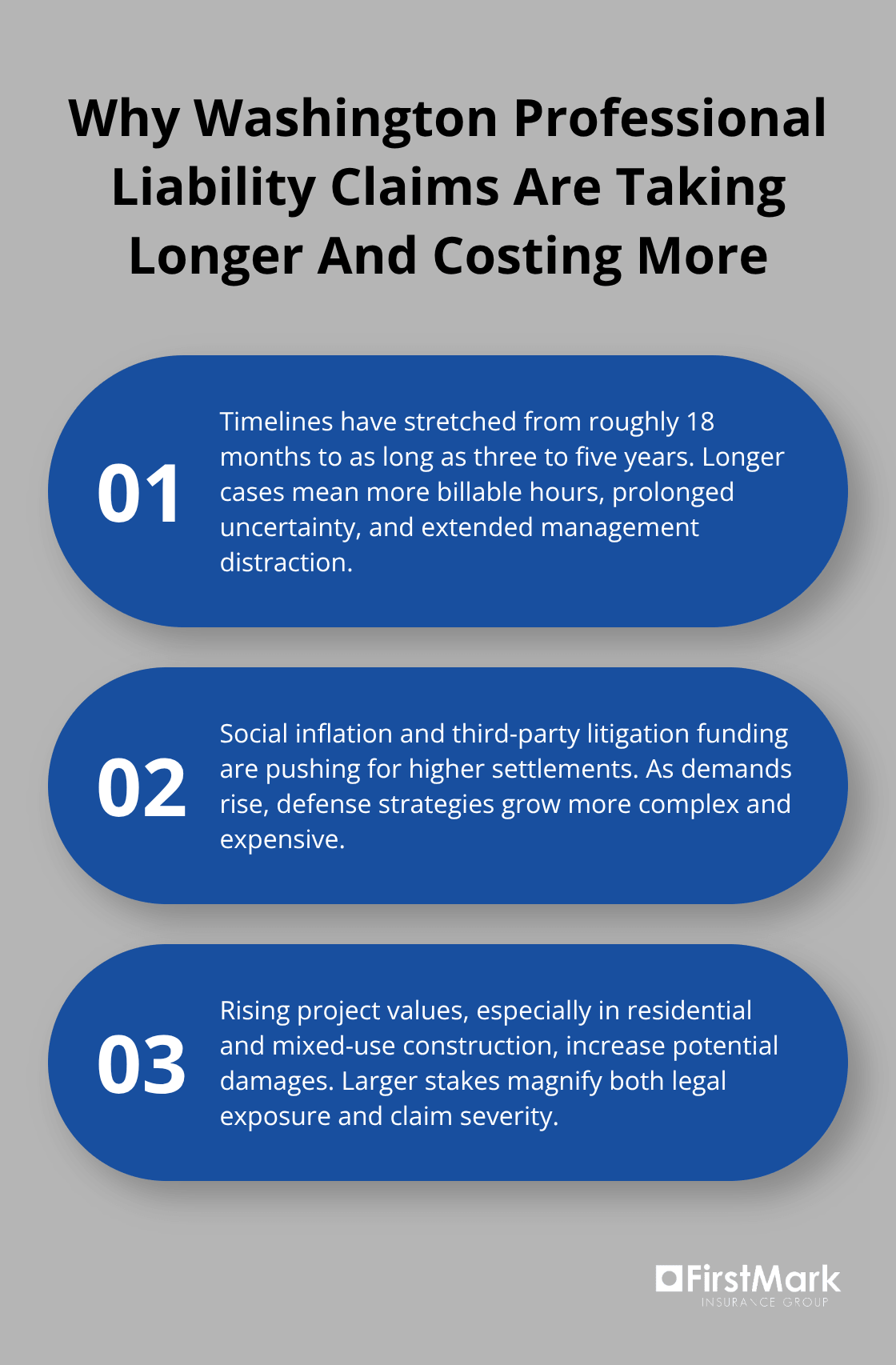

Professional liability claims in Washington are taking longer to resolve than they used to. Claims that once resolved in about 18 months now frequently extend three to five years. This extended timeline means higher legal fees, longer uncertainty, and more management distraction. Social inflation and litigation funding have made disputes costlier, with plaintiffs’ attorneys pursuing higher settlements.

Rising project values, especially in residential and mixed-use construction, magnify financial exposure. If you work on larger projects or handle significant client assets, your potential liability exposure grows substantially. The average cost for professional liability insurance in Washington is about 89 dollars per month, according to Insureon. That modest monthly investment covers defense costs, attorney fees, expert witnesses, and settlements up to your policy limits. Without coverage, a single three-year claim could cost tens of thousands in legal fees alone, even if you ultimately prevail.

What Comes Next in Your Coverage Decision

Understanding what professional liability covers and why you need it sets the foundation for the next critical step: determining exactly how much coverage your business requires and what policy structure fits your situation best.

Washington State Requirements and Regulations

State Law Permits Choice, But Market Forces Demand Coverage

Washington state takes a hands-off approach to professional liability insurance for most professions. Unlike workers’ compensation, which is mandatory for employers, professional liability coverage is not legally mandated for attorneys, accountants, consultants, engineers, architects, real estate agents, or most other service providers. However, this legal freedom masks a practical reality: the absence of a state mandate does not mean the absence of a requirement.

Your clients, your contracts, and your professional standing will demand coverage regardless of what state law says. Banks and institutional lenders routinely require proof of professional liability insurance before financing projects. Real estate clients and franchises demand certificates of insurance as a condition of engagement. If you sign client agreements, those contracts frequently include minimum coverage thresholds that you must meet.

Attorneys and Regulated Practitioners Face Stricter Accountability

The Washington Supreme Court requires attorneys to report annually whether they carry coverage, though it does not mandate a specific amount. For limited licensed legal technicians and limited practice officers in Washington, the rules are far stricter. LLLTs must demonstrate financial responsibility of at least $100,000 per claim and $300,000 in annual aggregate coverage, either through a professional liability policy or employer-provided coverage.

LPOs face similar requirements of $100,000 per claim through an individual errors and omissions policy, employer coverage, or documented net worth. These practitioners must certify annually that coverage remains in force and notify the Washington State Bar if coverage lapses or is cancelled. The bar then notifies employers of any status changes that could affect licensure. This accountability structure shows that Washington recognizes professional liability exposure as serious enough to track and verify for certain regulated practitioners.

Industry-Specific Exposure Shapes Real Coverage Demands

Different industries face distinct exposure patterns that shape coverage requirements. Healthcare providers working with state programs must carry minimum limits of $1,000,000 per occurrence and $3,000,000 in annual aggregate, or face exclusion from provider networks. Architects and engineers handling larger projects now face requests for $5 to $10 million or higher in coverage limits as project values escalate.

Technology professionals frequently bundle professional liability with cyber insurance to address both service quality and data breach exposure. Real estate agents, though not legally required to carry coverage, find that banks, brokers, and clients increasingly demand proof before closing transactions. The practical effect is that Washington professionals operate in an environment where state law permits choice but market forces and contract requirements remove that choice.

The Gap Between Legal Permission and Practical Necessity

Your competitive position, your ability to sign contracts, and your access to institutional clients all depend on carrying adequate coverage. The solution is not to ask whether Washington requires coverage, but to ask what your actual clients and contracts demand and to ensure your policy matches those real-world requirements. This distinction between legal mandates and contractual realities shapes how you should approach your coverage decision-a decision that requires understanding not just what the state allows, but what your specific business situation actually demands.

How Much Coverage Do You Actually Need

Review Your Contracts First

Start with your client agreements and proposals. Most contracts contain insurance requirements buried in the terms and conditions, and these contractual minimums set your baseline coverage need. If a client demands $1,000,000 per occurrence and $3,000,000 aggregate, that becomes your floor regardless of industry standards. Next, examine what your lenders, landlords, and institutional partners require. Banks financing your projects, property owners leasing you space, and franchise operators all impose coverage thresholds as conditions of doing business. These contractual demands override what Washington state law permits.

Calculate Your True Defense Costs

The real question is not what the state requires but what happens if you get sued. Legal defense costs can reach significant amounts before any settlement occurs. Your policy limit must cover both defense costs and potential damages. Professional liability coverage in Washington typically requires at least $1 million per occurrence, making it economical to carry limits that exceed your bare minimum requirements. For architects and engineers handling larger projects, the market now demands $5,000,000 to $10,000,000 in limits as project values escalate. If you work on residential construction, commercial development, or handle significant client assets, conservative underestimation of your exposure creates genuine financial risk.

Understand Claims-Made Policies and Tail Coverage

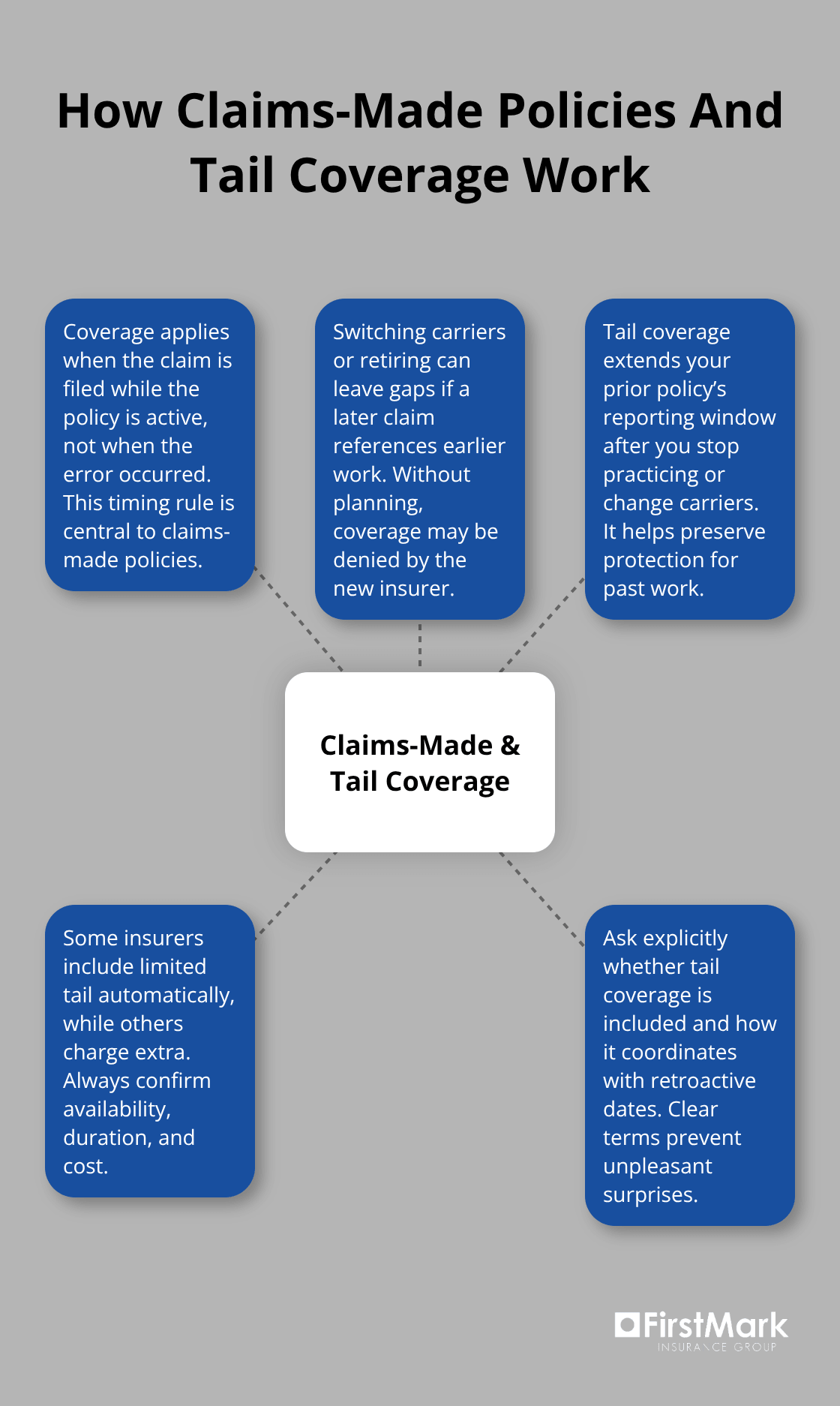

Most professional liability policies operate on a claims-made basis, meaning the policy must be in force when a claim is filed, not when the error occurred. This distinction creates a critical vulnerability if you switch insurers or retire. If you change carriers next year and a client files a claim in three years based on work you performed this year, your new insurer may deny coverage because the claim was not made during their policy period.

Tail coverage, also called extended reporting period coverage, protects you by extending your old policy’s coverage period after you stop practicing or switch carriers. Some insurers include limited tail coverage automatically; others charge extra. When evaluating policies, ask explicitly whether tail coverage is included or available and at what cost.

Review Policy Exclusions and Business Structure

Policy exclusions present another practical concern that most professionals overlook. Many policies exclude claims arising from illegal conduct, intentional misrepresentation, or services performed under an unlisted business entity. If you operate as a sole proprietor but your policy covers you as an LLC, claims may be denied. Review exclusions carefully with your agent to confirm the policy covers your actual business structure and operations. The cost difference between an inadequate policy and appropriate coverage is negligible when measured against the cost of an uninsured claim.

Final Thoughts

Professional liability coverage in Washington protects your business from the financial devastation of a single claim. Review your contracts to identify minimum coverage requirements, calculate realistic defense costs, and understand how claims-made policies work. Confirm that your policy covers your actual business structure and that exclusions do not create gaps in your protection.

Gather your client agreements and contact an insurance partner who understands your specific industry and exposure. Describe your typical projects or engagements, discuss what limits make sense for your business activities, and ask about tail coverage options before you need them. Request a certificate of insurance so you can provide proof to clients and lenders immediately.

We at FirstMark Insurance Group work with top insurance providers to present you with real choices at competitive pricing. We understand that professional liability coverage Washington varies dramatically across industries and project types, and we take time to understand your specific situation before recommending coverage. Contact FirstMark Insurance Group to discuss your professional liability coverage needs and get an accurate assessment of what your business requires.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation