Owning a seaside vacation home represents a significant investment that demands more than standard homeowners insurance. Luxury vacation home insurance requires specialized protection tailored to the unique risks your property faces-from coastal storms to high-value furnishings and guest liability.

At FirstMark Insurance Group, we understand that generic policies leave gaps that can expose you to substantial financial loss. This guide walks you through the coverage layers your seaside retreat actually needs.

Why Standard Homeowners Policies Fail Coastal Properties

Standard homeowners policies treat all residential properties as if they face identical risks, which is fundamentally wrong for seaside vacation homes. A policy written for an inland suburban house does not account for salt spray corrosion and nor’easters affecting coastal properties, tidal surge, or the extended vacancy periods that characterize seasonal properties. When you own a luxury coastal retreat, that disconnect between standard coverage and actual exposure creates dangerous gaps.

High-Value Coastal Homes Face Unique Vulnerabilities

High-value coastal homes commonly feature finished basements, walkout lower levels, and mechanical systems positioned near water-exactly the areas most vulnerable to damage from storm surge and wind-driven rain. A standard policy’s coverage limits and exclusions rarely reflect the true reconstruction cost of a luxury seaside property, which can run substantially higher than inland equivalents due to specialized trades, imported materials, and extended rebuild timelines after a coastal loss.

More critically, standard homeowners policies explicitly exclude flood damage, yet flood risk exists far outside FEMA-designated zones. Tidal surges, drainage constraints, and seasonal storms routinely deliver water to properties that map-based assessments classify as low-risk. For a property worth $1.5 million or more, the gap between standard coverage and actual exposure can easily exceed $200,000 to $400,000 in unprotected losses.

Replacement Costs Exceed Original Purchase Price

Rebuilding a luxury coastal home after a loss costs significantly more than the original purchase price because labor shortages and material inflation compound during reconstruction. Skilled tradespeople specializing in high-end finishes command premium rates, and custom materials often require extended lead times. A standard policy’s dwelling limit may appear adequate until you face actual repair quotes from contractors familiar with coastal restoration.

Specialized high-value carriers like Chubb and Cincinnati Insurance handle longer rebuilds and complex losses, with coverage structures that account for elevation, foundation type, construction methods, and property use. The key distinction is that luxury coastal policies separate wind and flood coverage strategically, addressing sublimits and exclusions that affect real-world damage outcomes. Finished basements, detached structures, service lines vulnerable to old coastal infrastructure, and liability exposures near the water represent significant financial exposure that standard policies routinely overlook.

A practical step involves requesting a Coastal Coverage Stress Test-a focused assessment of how your current policy would respond to an actual wind or flood loss-so you understand not what appears on paper, but how your policy performs when damage occurs.

Seasonal Vacancy Creates Elevated Risk

Vacation homes occupied only part of the year face different underwriting standards than primary residences. Extended vacancy periods create elevated risk for theft, burst pipes, mold, and weather damage, which standard policies either exclude or severely restrict. If your property sits unoccupied for more than 30 consecutive days, your standard homeowners coverage may not respond to water damage from frozen pipes or storm damage, leaving you entirely exposed during off-season months.

Lenders financing second homes typically require proof of insurance even for properties owned free and clear, but that requirement does not guarantee the policy actually covers the risks your seasonal property faces. Active maintenance and monitoring become part of your coverage obligation-periodic inspections, heating system verification, and timely repairs are not optional details but conditions of coverage.

The practical reality is that a policy designed for continuous occupancy leaves seasonal owners exposed during the months when the property is most vulnerable to damage and least likely to have someone present to address problems quickly. This exposure pattern demands a fundamentally different approach to coverage structure and risk management than what standard homeowners policies provide.

Core Protections Every Seaside Home Needs

Water Damage and Storm Coverage Form Your Foundation

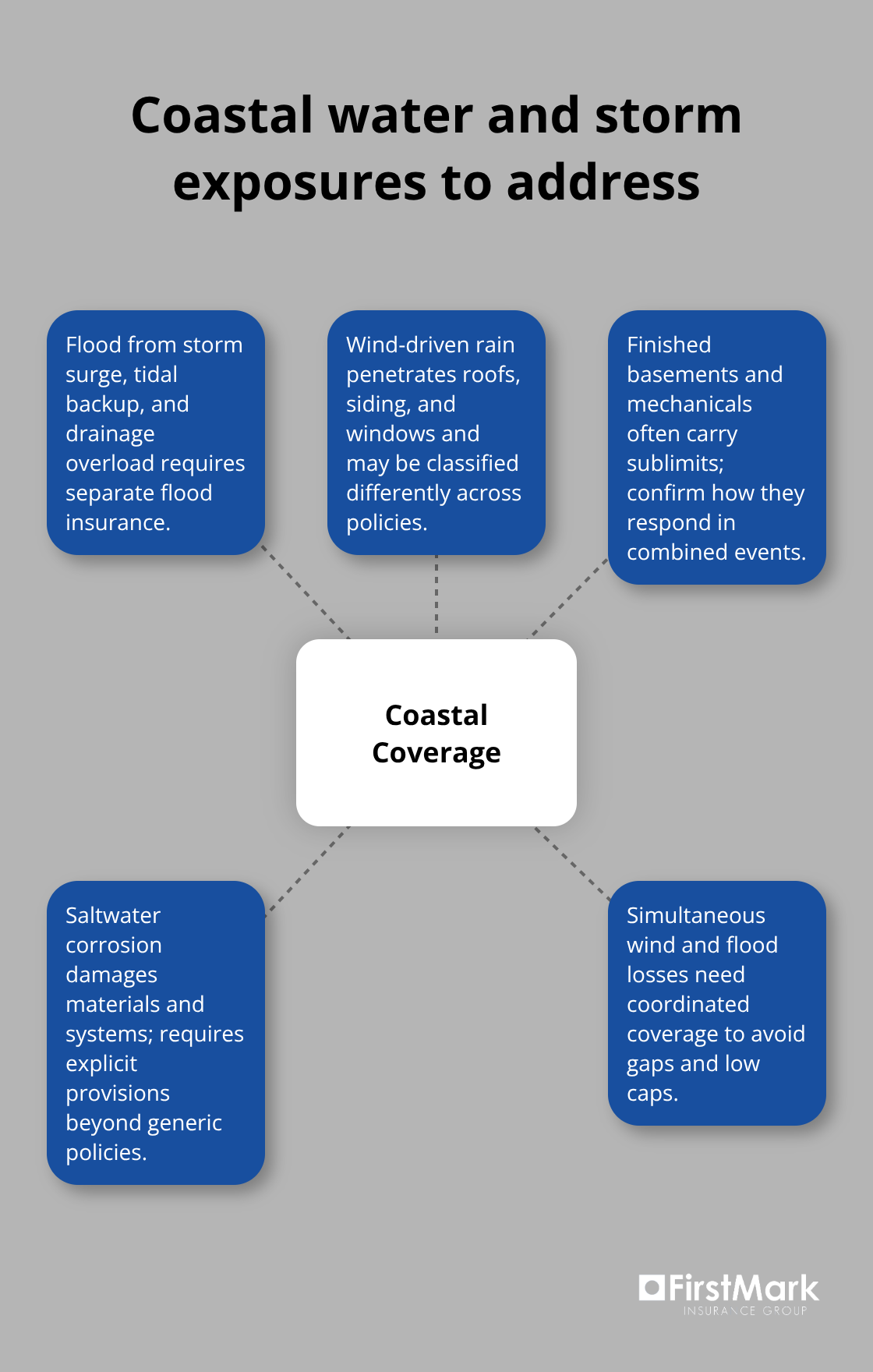

Water damage and storm coverage form the foundation of any viable seaside insurance strategy, yet most vacation home owners misunderstand what their policies actually cover. Standard policies exclude flood damage entirely, which means water arriving via storm surge, tidal backup, or overwhelming drainage systems leaves you unprotected regardless of your dwelling limit. Coastal properties require separate flood insurance coordinated with wind coverage to address the overlapping damage patterns that occur during nor’easters and hurricane-force storms.

Wind-driven rain penetrates roofs, siding, and windows, creating interior moisture problems that extend far beyond visible structural damage. These conditions affect mechanical systems, finished basements, and custom finishes in ways that standard coverage simply does not address. For a $1.5 million seaside home, wind and flood sublimits in a standard policy often cap combined water damage recovery at $50,000 to $75,000-far below actual reconstruction costs when you factor in labor shortages, material inflation, and extended rebuild timelines.

Specialized coastal carriers structure coverage to separate these exposures strategically, accounting for elevation, foundation type, and proximity to water. You should request explicit confirmation from your insurer about how wind-driven rain is classified, whether finished basements carry separate sublimits, and what happens when wind and flood damage occur simultaneously. Saltwater exposure adds another layer of complexity: corrosion affects building materials, HVAC systems, and metal fixtures, requiring explicit coverage provisions that generic policies do not address.

Liability Protection Protects Against Guest-Related Claims

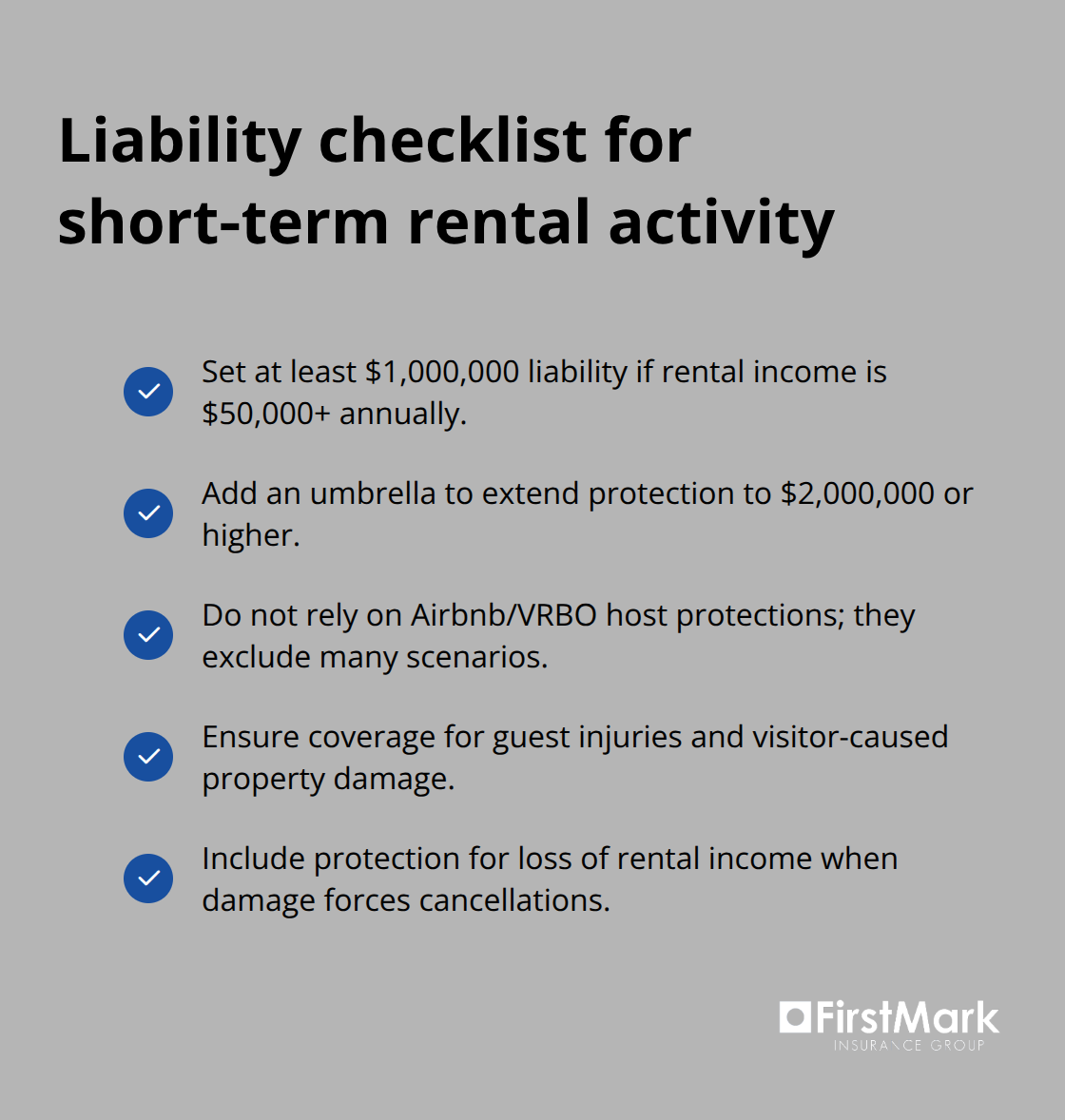

Liability protection becomes critical the moment guests occupy your property, since a visitor injured on your seaside deck or in your pool creates exposure that extends well beyond standard homeowners limits. Coastal properties attract liability claims at higher frequency due to uneven terrain, weathered decking, slippery surfaces from salt spray and moisture, and proximity to water hazards. A standard homeowners policy typically caps liability at $300,000 to $500,000, which proves wholly inadequate when a guest requires hospitalization or permanent disability.

Luxury vacation homes rented through Airbnb or VRBO introduce additional complexity: platform host protections provide minimal backup and exclude numerous scenarios, leaving you exposed for guest injuries, property damage caused by visitors, and loss of rental income if damage forces cancellation. Your liability limit should reflect your property value and rental activity-properties that generate $50,000 or more annually in rental income warrant minimum liability coverage of $1 million, with umbrella policies extending protection to $2 million or higher.

Detached Structures and Equipment Require Separate Attention

Detached structures including pools, hot tubs, gazebos, and elevated decks multiply your exposure because guests often use these amenities without supervision. Equipment breakdown coverage protects against failure of your heating system, electrical panel, or water treatment equipment during extended off-season periods when problems go undetected. Fixture protection becomes essential for high-value outdoor amenities: built-in grills, outdoor kitchens, fire pits, and landscape lighting represent $30,000 to $100,000 in exposure that standard policies treat as personal property with severe sublimits.

You should coordinate all these exposures with a single advisor who understands coastal construction realities rather than relying on generic quotes that treat your luxury seaside property as interchangeable with suburban homes. This coordinated approach prevents gaps and redundancies across your entire protection strategy. The next section examines how to identify the right insurance partner who can translate coastal risk into a comprehensive coverage plan tailored to your specific property and use patterns.

Finding an Insurance Partner Who Understands Coastal Risk

Selecting the right insurance partner for a luxury seaside property requires moving beyond online quote comparisons and generic agent relationships. Most agents lack specialized knowledge of coastal construction, seasonal occupancy patterns, and the specific exposures that separate a $1.5 million seaside home from a standard residential property. Your agent must understand how elevation, foundation type, and proximity to water affect both your risk profile and your coverage needs.

Ask Direct Questions About Coastal Experience

Start conversations with potential agents by asking direct questions about their experience with finished basements in coastal properties, how they structure wind and flood coverage together, and whether they have handled claims involving saltwater corrosion damage. An agent unfamiliar with these specifics will default to standard policies that leave you exposed. At FirstMark Insurance Group, we have spent 30 years guiding families through insurance complexities, and our experience with coastal properties means we understand the gap between what standard policies cover and what your seaside retreat actually needs.

Conduct a Thorough Property Assessment

Your property assessment should start with documentation of what makes your specific location different from inland homes. Gather your property deed, current appraisal, flood zone determination letter from FEMA, and recent inspection reports that highlight water intrusion history or foundation concerns. Request that your agent conduct a site visit rather than relying on satellite imagery and public records. During this visit, discuss your property’s elevation relative to storm surge projections, whether your basement has experienced water entry during past storms, and which mechanical systems sit closest to water.

Specialized carriers like Chubb and Cincinnati Insurance require this level of detail before underwriting high-value coastal properties, and their underwriting standards force a rigorous examination that reveals actual exposure. Your agent should also clarify how rental activity affects your coverage if you generate income from short-term rentals, since platform host protections provide virtually no backup for property damage or loss of rental income.

Compare Coverage, Not Price

When comparing quotes, ignore premium price entirely until you understand what each policy actually covers. Request explicit confirmation of your dwelling limit, flood sublimit, wind sublimit, and how these interact when simultaneous damage occurs. A policy quoting $800 annually with a $50,000 flood sublimit provides false economy compared to a $1,200 policy with adequate flood and wind separation.

Ask each agent to walk you through a hypothetical nor’easter scenario: your roof sustains wind damage, storm surge floods your basement, and wind-driven rain damages finished spaces. Which coverages respond? What are your out-of-pocket costs? Where are the gaps? An agent who cannot articulate this clearly does not understand your exposure.

Final Thoughts

Protecting a luxury vacation home requires moving beyond the assumption that standard homeowners insurance provides adequate coverage. The gaps we outlined-from flood exclusions to seasonal vacancy restrictions to inadequate liability limits-represent real financial exposure that materializes the moment damage occurs. Your seaside property demands a coverage strategy built specifically for coastal risk, not a generic policy adapted from inland standards.

Taking action means scheduling a conversation with an insurance partner who understands coastal construction and has handled claims involving saltwater corrosion, wind-driven rain damage, and seasonal vacancy exposures. Request a site visit rather than accepting quotes based on satellite imagery, and conduct a Coastal Coverage Stress Test to understand how your policy actually performs during a real loss. Compare coverage structures, not premium prices, and demand explicit confirmation of how your dwelling limit, flood sublimit, and wind sublimit interact when simultaneous damage occurs.

We at FirstMark Insurance Group have spent 30 years guiding families through these complexities, and we understand that luxury vacation home insurance represents a partnership, not a transaction. Contact us to discuss how we can help you protect your seaside investment with confidence and ensure your coverage aligns with your property’s actual needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation