Building substantial wealth across multiple properties and investments creates protection challenges that standard insurance simply cannot address. High net worth estate coverage requires a fundamentally different approach-one that accounts for the complexity of your assets and the sophistication of your financial position.

At FirstMark Insurance Group, we work with clients who understand that generic policies leave significant gaps. The strategies in this guide reflect what we’ve learned helping discerning individuals structure comprehensive protection for their legacies.

Why Standard Coverage Misses the Mark

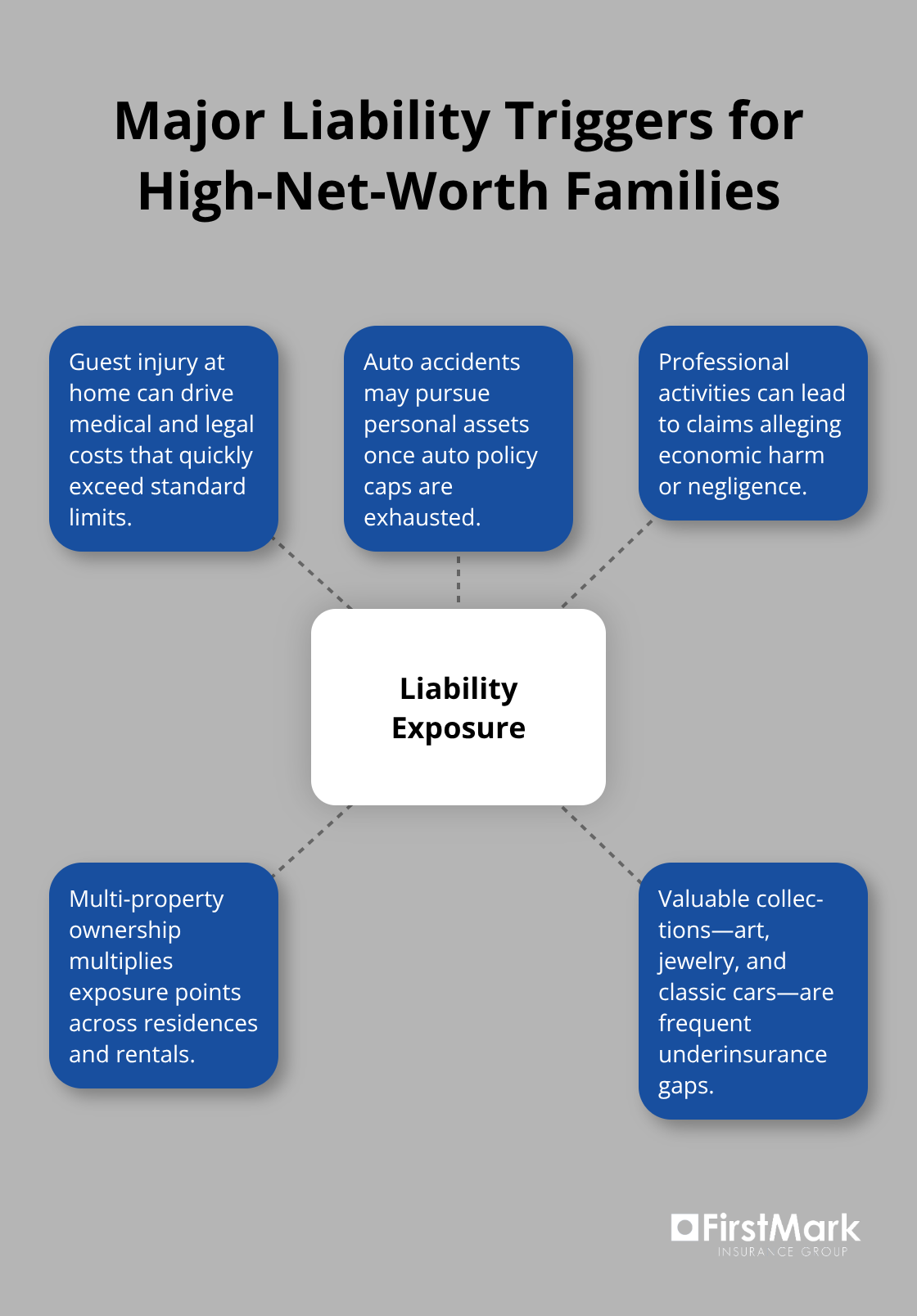

High net worth individuals face a coverage paradox. Standard homeowners policies cap liability protection at $300,000 to $500,000, yet a single lawsuit from a guest injured on your property or a car accident you cause could expose assets worth millions. The gap widens when you own multiple properties, operate investment vehicles, or hold valuable collections. Traditional insurers design policies for average households, not for clients with diversified real estate portfolios, business interests, or significant liquid assets that courts will pursue in litigation.

The Real Cost of Underinsurance

Your net worth becomes a liability magnet. If you own a $3 million primary residence, a $2 million vacation home, and rental properties generating six-figure annual income, a standard homeowners policy protects only the structure itself, leaving your personal assets vulnerable. Liability exposure extends beyond your properties too. A visitor injured at your home, a business associate harmed through your professional activities, or even an accident in your vehicle can trigger claims that exhaust standard umbrella limits within months.

Adequate coverage for high net worth estates requires coordinated homeowners policies on each property, umbrella policies starting at $2 million to $5 million in coverage, and specialty policies for business interests or valuable assets. The cost of this layered approach, while meaningful, pales against the risk of defending a $10 million judgment with insufficient insurance. State-specific liability trends also matter, making comprehensive coverage non-negotiable for high net worth households.

Protecting Assets Beyond Your Primary Home

Your assets require more than generic protection. If you hold fine art, classic vehicles, jewelry, or alternative investments, standard homeowners policies exclude these items entirely or limit coverage to amounts far below their actual value. A single piece of art worth $500,000 receives perhaps $5,000 in coverage under a typical policy. Investment real estate operates under different rules than primary residences, often requiring landlord liability policies that address tenant-related claims.

Business interests introduce additional exposure if you own an LLC, operate as a partnership, or hold equity stakes that courts can attach during litigation. Each layer of complexity demands deliberate structuring. Your insurance portfolio should reflect the actual composition of your wealth, not the assumptions of a standard underwriter. Coordinating this protection across multiple carriers, properties, and asset classes requires expertise that goes beyond what local agents typically provide.

Moving Forward With Specialized Guidance

The gap between what you own and what standard policies cover grows wider with each property you acquire and each asset class you add to your portfolio. Addressing this gap requires a strategic approach that accounts for your specific holdings and exposure profile. The next section examines how to structure comprehensive protection that coordinates across your entire estate, ensuring no significant exposure falls through the cracks.

Building Your Estate Protection Framework

Establish Proper Coverage on Your Primary Residence

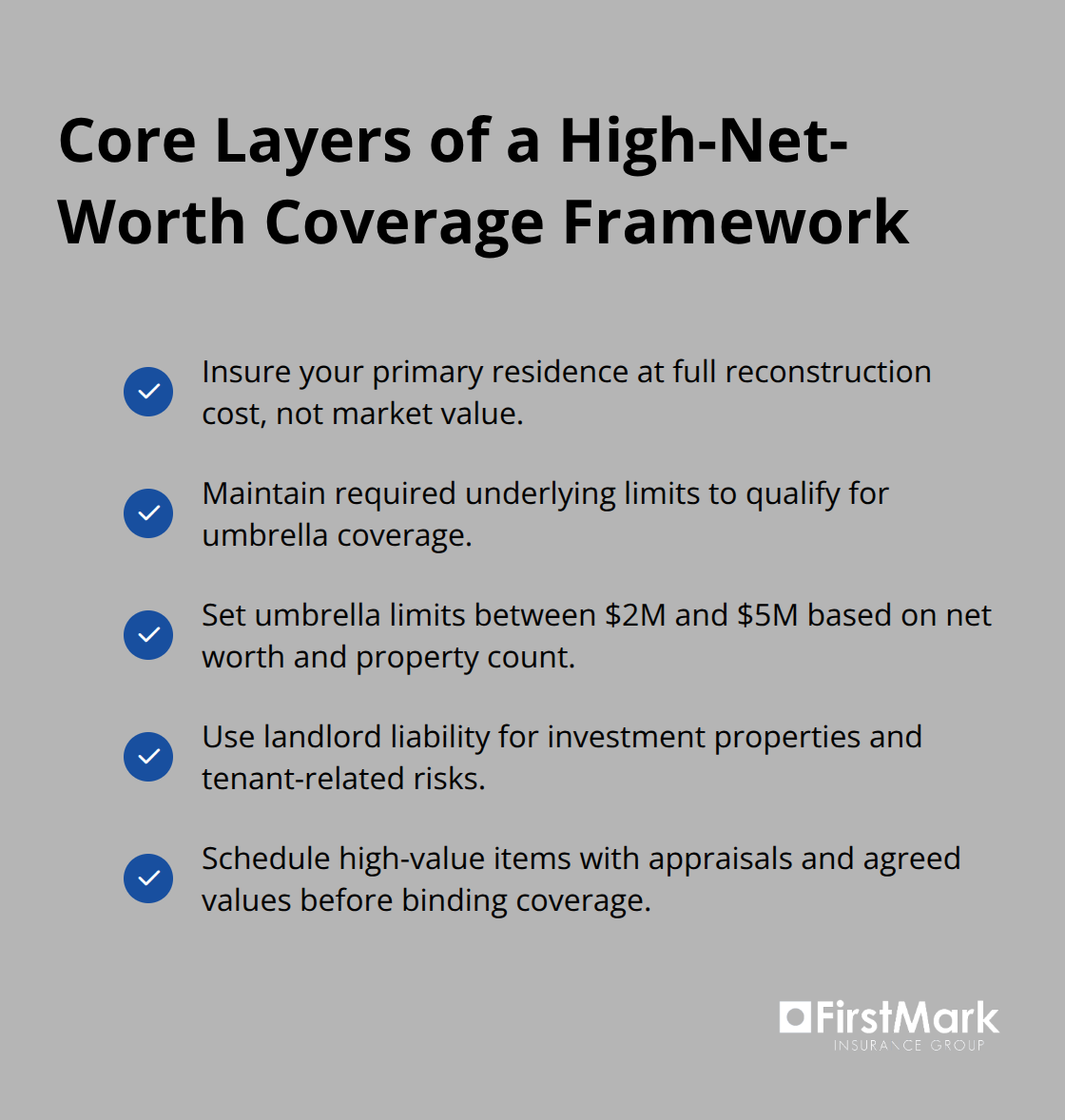

Start with your primary residence and establish a homeowners policy that reflects its actual replacement cost, not just the mortgage amount. Many high net worth individuals underestimate replacement costs because they focus on land value rather than construction expenses. If your primary home cost $3 million to build but sits on land worth $1.5 million, your policy should cover the full $3 million reconstruction expense, not the combined value. Construction costs in your area determine this figure more accurately than market price, so request a professional replacement cost analysis from your insurer before finalizing coverage limits.

Layer Umbrella Coverage Strategically

Next, add an umbrella policy on top of your homeowners and auto coverage. Most carriers require $300,000 to $500,000 in underlying liability limits before they’ll issue umbrella coverage, so coordinate these policies with the same insurer when possible to avoid coverage gaps. Umbrella policies starting at $2 million provide meaningful protection for high net worth households, though $5 million offers more appropriate coverage if your net worth exceeds $10 million or you own multiple investment properties.

Each additional property requires its own homeowners or landlord policy tailored to its use, then backed by the same umbrella carrier for seamless coordination.

Address Specialty Assets and Collections

Specialty coverage fills the gaps that standard policies ignore entirely. Fine art, classic vehicles, jewelry, and collectibles need scheduled personal property coverage that lists items individually with agreed-upon values, bypassing the typical $5,000 limits in standard homeowners policies. Request appraisals from qualified professionals for any item exceeding $10,000 in value, then provide these to your insurer before coverage takes effect. Investment real estate demands landlord liability policies that address tenant-related claims, lost rent coverage, and landlord’s protective liability, which differ substantially from owner-occupied homeowners policies.

Coordinate Business and Partnership Interests

If you operate a business or hold partnership interests, business liability coverage must exist separately from your personal umbrella, with limits that match your exposure level. For example, if your LLC generates $500,000 in annual revenue, minimum business liability coverage should start at $1 million. Document all asset ownership structures with your insurance agent so they understand whether properties sit in trusts, LLCs, or personal names, as this affects coverage placement and claims handling.

Maintain Alignment With Changing Circumstances

Your protection portfolio requires regular attention because asset values rise, new properties enter your holdings, and liability exposures shift with business changes or family circumstances. Annual reviews catch these shifts before coverage gaps emerge. As your estate grows more complex-particularly when business interests or alternative investments enter the picture-the coordination between your insurance structure and your overall wealth strategy becomes increasingly important.

Insurance’s Role in Estate Preservation

Your insurance structure directly impacts how much wealth actually reaches your beneficiaries. Most high net worth individuals focus exclusively on trust documents and tax strategies while treating insurance as a separate line item, missing the critical intersection where proper coverage placement reduces both taxes and administrative costs. When structured correctly, insurance becomes a wealth preservation tool that works alongside your estate plan rather than against it.

How Insurance Protects Your Estate From Forced Liquidation

The federal lifetime gift and estate tax exemption sits at $15 million per individual in 2026 according to the IRS, creating a narrow window for strategic planning before these limits reset. If your net worth exceeds this threshold, every dollar of unnecessary insurance costs or poorly coordinated coverage represents wealth that flows to tax authorities instead of your heirs.

A $10 million estate with gaps in liability coverage faces potential lawsuits that force asset liquidation, triggering capital gains taxes and disrupting the orderly transfer you’ve planned. Adequate umbrella and specialty coverage prevents forced asset sales, allowing your estate to transfer according to your documented wishes rather than creditor demands. The coordination between coverage limits and asset values matters more than the premium amount you pay.

Matching Coverage Limits to Your Actual Exposure

If you own $5 million in real estate across three states, your umbrella policy should reflect this exposure level, not the arbitrary $2 million minimum that generic advisors recommend. Investment real estate generates different liability profiles than primary residences, requiring landlord liability policies with limits that match your rental income and tenant exposure.

A property generating $100,000 annually in rental income needs minimum business liability coverage of $1 million, not the $300,000 that works for a modest primary home. This specificity prevents the scenario where a tenant injury claim exhausts your coverage within days, exposing personal assets to attachment.

Coordinating Ownership Structure With Policy Placement

Your beneficiaries also benefit from clear ownership documentation that coordinates with your insurance structure. Properties held in trusts or LLCs require different policy placements than individually owned assets, and misalignment creates claims complications that delay settlements and increase legal costs during probate.

The IRS allows annual exclusion gifts up to $19,000 per recipient per year, enabling systematic wealth transfer without touching your lifetime exemption. Strategic use of life insurance within an irrevocable life insurance trust removes policy proceeds from your taxable estate entirely, creating liquidity for your heirs to pay any estate taxes without forced asset sales.

Using Life Insurance to Fund Tax Obligations

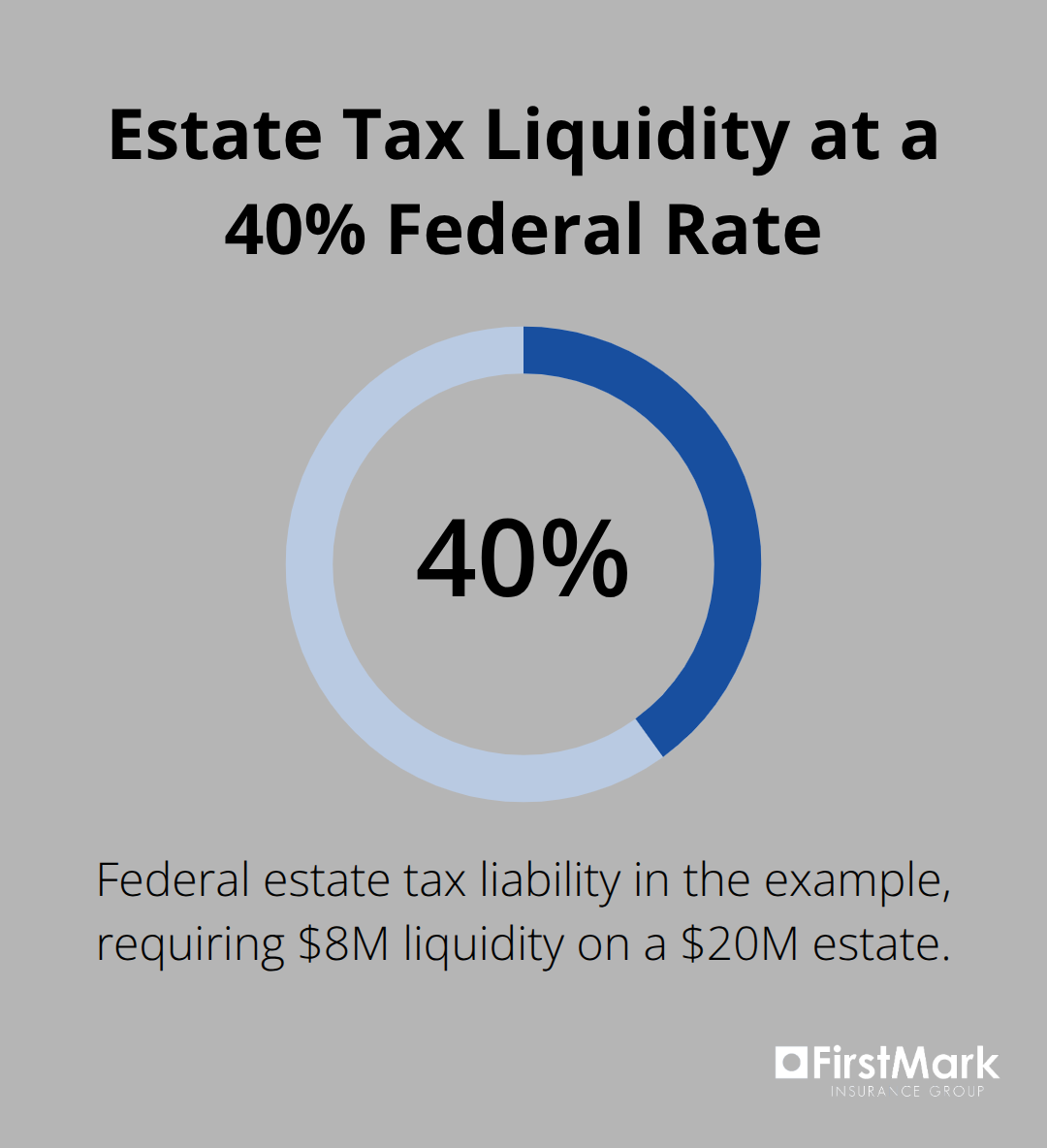

This approach works particularly well for high net worth individuals whose estates will owe significant federal taxes. A $20 million estate facing 40 percent federal tax liability needs $8 million in liquid funds to settle obligations, and life insurance provides this without disrupting your investment portfolio or real estate holdings. The policy proceeds sit outside your taxable estate when held in a properly structured trust, meaning the full benefit reaches your heirs tax-free.

State-level taxes compound this planning need, with twelve states plus Washington, D.C. imposing estate taxes according to the IRS, and five states imposing inheritance taxes. If you maintain residences in multiple states or conduct business across state lines, your exposure multiplies beyond federal calculations alone.

Integrating Insurance With Your Complete Wealth Strategy

Professional coordination between your insurance agent, estate planning attorney, and tax advisor prevents the common mistake where policies are placed in ways that accidentally trigger unnecessary taxes or create gaps in your coverage strategy. This integrated approach recognizes that insurance is not overhead to minimize but rather a foundational component of wealth preservation that reduces both risk and tax burden when structured properly.

Final Thoughts

High net worth estate coverage requires coordination across multiple layers of protection, and this coordination must align with your estate plan, trust documents, and overall wealth strategy to function effectively. Life insurance structured within an irrevocable trust removes policy proceeds from your taxable estate while providing liquidity for tax obligations, preventing forced asset sales that would disrupt your wealth transfer plan. State-specific tax exposure compounds federal considerations, making comprehensive coordination essential rather than optional for families with significant holdings across multiple jurisdictions.

Your protection plan needs regular review because asset values rise, new properties enter your holdings, and liability exposures shift with business changes or family circumstances. Annual reviews catch these shifts before coverage gaps emerge and create vulnerability. As your estate grows more complex, the coordination between your insurance structure and your overall wealth strategy becomes increasingly important to your long-term financial security.

Connect with FirstMark Insurance Group to build a comprehensive high net worth estate coverage strategy tailored to your specific holdings and exposure profile.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation