Luxury homes worth $1 million or more require specialized insurance protection that standard homeowners policies simply cannot provide. High value home insurance addresses the unique risks and replacement costs associated with premium properties.

We at FirstMark Insurance Group understand that affluent homeowners face distinct coverage challenges. Your custom finishes, art collections, and high-end materials demand tailored protection strategies.

What Qualifies as a High-Value Home

Property value determines high-value home classification, with most insurers setting thresholds between $750,000 and $1 million. Market value alone doesn’t tell the complete story though. Homes that exceed 4,500 square feet automatically qualify for specialized coverage, regardless of their market price.

The Insurance Information Institute reports that standard homeowners policies typically cap coverage at $500,000 for dwelling protection. This makes them inadequate for luxury properties where replacement costs often soar well above market values.

Property Value Thresholds and Market Standards

Insurance carriers evaluate multiple factors beyond simple market value when they classify high-value homes. Square footage plays a major role in this assessment process. Properties with extensive custom features may qualify for specialized coverage even when their market value falls below the typical $1 million threshold.

Construction quality and materials significantly influence these classifications. A 3,000-square-foot home built with premium materials often requires the same specialized coverage as a larger standard home. Insurers recognize that replacement costs don’t always correlate directly with market prices (especially in areas with unique architectural styles).

Custom Features and Premium Materials

High-end construction materials drive replacement costs far beyond market value expectations. Imported marble countertops cost $200 to $500 per square foot to replace, while hand-carved woodwork and custom millwork add substantial complexity to reconstruction projects.

Smart home technology, wine cellars, and chef-grade kitchens create coverage challenges that standard policies simply ignore. Insurance carriers examine these features during property inspections because replacement costs often exceed 150% of the home’s market value. Custom pools, outdoor kitchens, and guest houses require separate coverage calculations that standard policies cannot accommodate.

Geographic Location and Risk Factors

Location significantly impacts high-value home insurance requirements and premium calculations. Coastal properties face hurricane and flood risks that demand specialized coverage options beyond standard homeowners protection.

Wildfire-prone areas present significant insurance challenges with specialized coverage requirements and higher premium costs. Rural luxury properties present unique challenges with limited fire department access and longer emergency response times that insurers must factor into their risk assessments.

Urban high-value homes face different risk profiles including higher liability exposure from increased foot traffic and proximity to neighbors. These location-specific factors directly influence the type of coverage options you’ll need to consider when selecting your high-end insurance policy.

Key Coverage Areas for High-Value Home Insurance

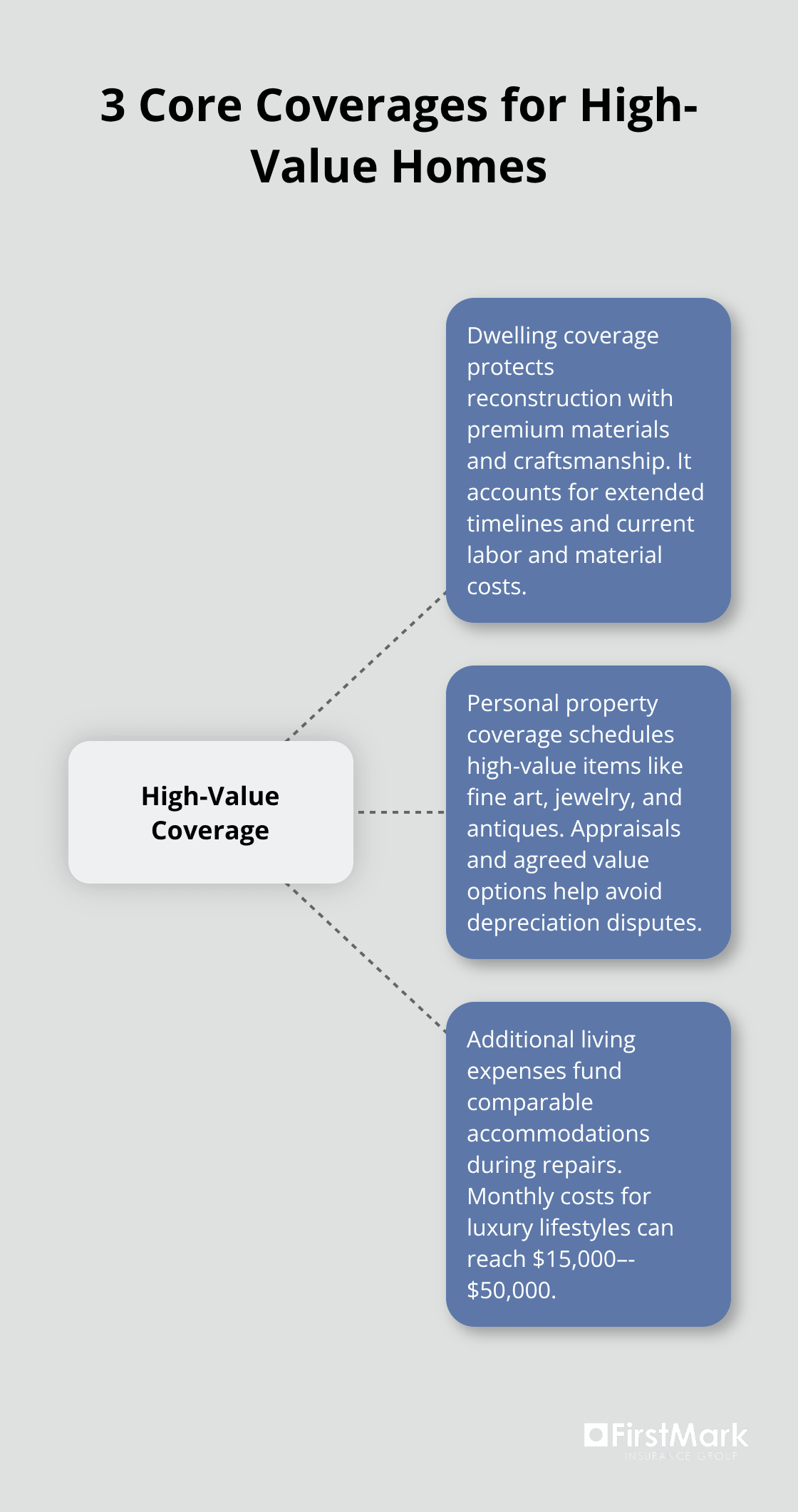

High-value home insurance requires three fundamental coverage areas that standard policies inadequately address. Dwelling coverage must account for premium construction materials where replacement costs often exceed 200% of market value. Personal property protection needs specialized scheduling for art collections, jewelry, and antiques that can total millions in value. Additional living expenses become critical when luxury homeowners face temporary displacement costs of $15,000 to $50,000 monthly for comparable accommodations.

Dwelling Coverage for Premium Materials and Construction

Standard homeowners policies cap dwelling coverage at $500,000, but luxury home reconstruction averages $400 to $800 per square foot according to the National Association of Home Builders. Custom millwork alone costs $150 to $300 per linear foot to replace, while imported stone and tile can reach $50 to $200 per square foot.

High-value policies provide extended replacement cost coverage that pays 125% to 150% above policy limits when reconstruction exceeds estimates. This protection proves essential when specialized craftsmen require professional-grade estimates using current construction costs, materials, and labor rates for custom work that can take 18 to 36 months to complete.

Personal Property Protection for Valuable Collections

Standard policies limit jewelry coverage to $1,500 and fine art to $2,500 (amounts that prove useless for affluent homeowners). High-value policies typically include $50,000 to $100,000 automatic jewelry coverage with options for unlimited scheduled items.

Fine art and collectibles require professional appraisals every three to five years, with some insurers offering agreed value coverage that eliminates depreciation disputes during claims. Wine collections averaging $100,000 to $500,000 need specialized temperature-controlled storage protection that standard policies exclude entirely.

Additional Living Expenses and Loss of Use Coverage

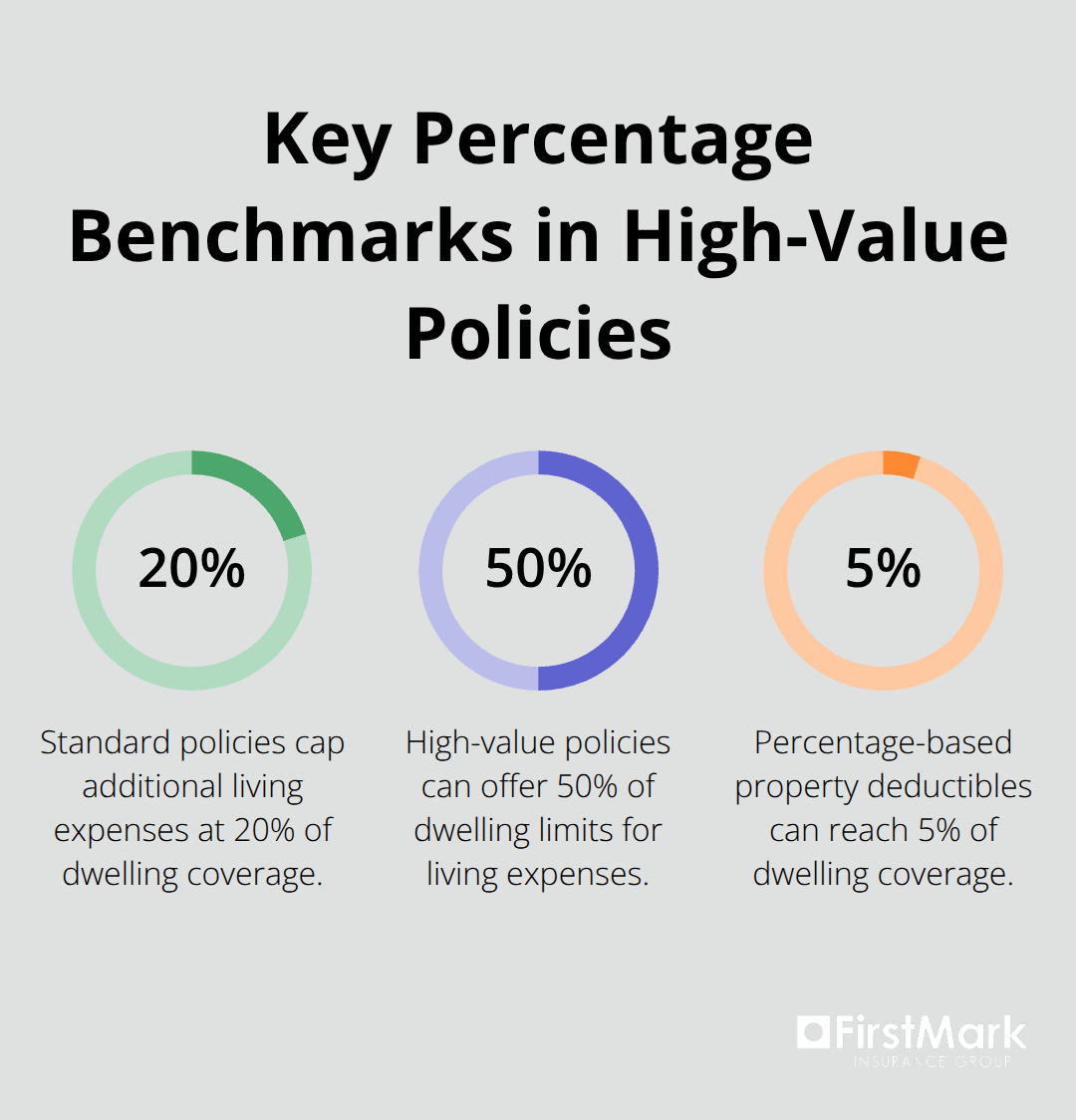

Luxury homeowners face monthly temporary housing costs of $15,000 to $50,000 when their primary residence becomes uninhabitable. Standard policies limit additional living expenses to 20% of dwelling coverage, providing inadequate protection for affluent lifestyles.

High-value policies offer 50% to 100% of dwelling limits for living expenses, covering luxury hotel suites, furnished rentals, and private chef services. Claims processing for these expenses typically takes 30 to 60 days, making immediate cash flow protection through your insurer absolutely necessary for maintaining your standard of living during reconstruction periods.

The complexity of these coverage areas makes selecting the right insurance carrier and policy structure absolutely critical for proper protection.

How to Select the Right High-Value Home Insurance Policy

Affluent homeowners must target carriers that specialize exclusively in luxury properties rather than traditional insurers that offer basic high-value add-ons. PURE, AIG Private Client Group, and Chubb dominate this market with dedicated underwriting teams that understand million-dollar reconstruction projects and custom craftsmanship timelines.

These specialized insurers maintain claims departments staffed with adjusters experienced in appraising fine art, antique furniture, and imported materials that standard carriers struggle to evaluate properly. Traditional insurers like State Farm or Allstate lack the expertise and vendor networks necessary for luxury home claims, often causing months of delays and inadequate settlements that can cost homeowners hundreds of thousands in out-of-pocket expenses.

Evaluating Specialized Insurance Carriers

Luxury home insurers differentiate themselves through their underwriting approach and claims handling capabilities. PURE focuses exclusively on high-net-worth clients and maintains a network of preferred contractors who specialize in luxury home restoration. Chubb offers masterpiece coverage for fine art collections and provides risk management consultations that help prevent losses before they occur.

AIG Private Client Group provides worldwide coverage for personal property and maintains relationships with international restoration experts. These carriers typically require minimum annual premiums of $15,000 to $25,000, which reflects their specialized service levels and expertise in handling complex luxury property claims.

Policy Limits and Deductible Strategies

High-value policies should include dwelling coverage of at least 150% of estimated replacement costs, with many affluent homeowners opting for unlimited rebuilding coverage that eliminates disputes over final reconstruction expenses. Personal property limits need careful calculation based on professional appraisals, with jewelry coverage ranging from $100,000 to $500,000 and fine art protection often exceeding $1 million for serious collectors.

Deductible structures vary dramatically between carriers, with percentage-based options ranging from 1% to 5% of dwelling coverage. A $2 million home could carry deductibles between $20,000 and $100,000. Smart homeowners choose higher deductibles on property damage while maintaining low or zero deductibles on theft and liability claims where smaller losses prove more frequent.

Working with Specialized Insurance Professionals

Professional appraisers certified by the American Society of Appraisers charge $500 to $1,500 for comprehensive home valuations that determine proper coverage limits. Insurance agents who specialize in high-net-worth clients typically require minimum premiums of $25,000 annually before accepting new accounts.

These specialists maintain relationships with restoration contractors, security consultants, and risk management experts who provide services unavailable through standard insurance channels. The specialized underwriting process often extends timelines by 30-45 days for comprehensive coverage approval due to regulatory complexity and detailed requirements.

Final Thoughts

High-value home insurance protects luxury properties worth $1 million or more through specialized coverage that standard policies cannot match. Affluent homeowners need dwelling protection of 150% replacement costs, personal property coverage exceeding $100,000, and additional living expenses that reach $50,000 monthly. Carriers like PURE, Chubb, or AIG Private Client Group provide access to expert adjusters and luxury restoration networks that traditional insurers lack.

Professional appraisals every three to five years maintain accurate coverage limits as property values and collections grow. Regular policy reviews become essential when home renovations, art acquisitions, or market changes affect coverage needs. Annual premium investments of $15,000 to $25,000 reflect the specialized expertise required for million-dollar reconstruction projects (which standard carriers cannot handle effectively).

We at FirstMark Insurance Group guide families through insurance complexities with our commitment to simplify your insurance journey. Our team explores offerings from top providers to find ideal coverage that fits your specific requirements at competitive pricing. Contact us to secure appropriate protection for your luxury property investment.