Wealthy individuals face unique insurance challenges that standard policies simply cannot address. Private client group insurance offers specialized protection for high-net-worth families and their complex assets.

At FirstMark Insurance Group, we see clients struggle with coverage gaps that leave millions of dollars in assets vulnerable. This comprehensive guide breaks down everything you need to know about private client insurance and how it protects your wealth.

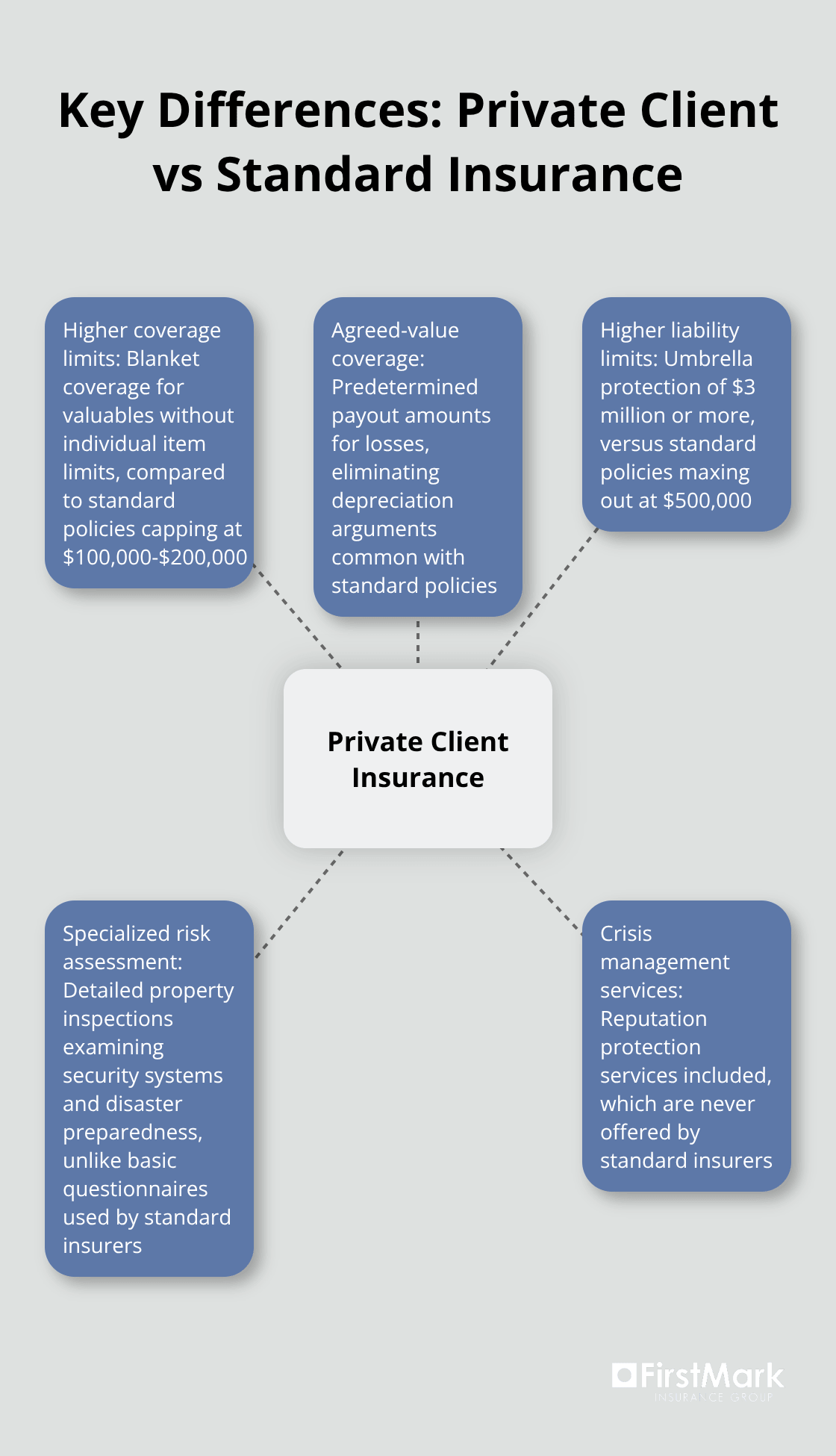

What Makes Private Client Insurance Different

Private client group insurance targets families with liquid assets that exceed $1 million, though most insurers prefer clients with higher investable wealth. This specialized coverage addresses risks that standard homeowners and auto policies completely ignore. Standard insurance assumes you live in a typical home with average possessions, while private client insurance recognizes your art collection, wine cellar, and multiple luxury vehicles require different protection levels.

Coverage Built for Complex Assets

Standard homeowners insurance caps personal property at roughly $100,000 to $200,000, but private client policies provide blanket coverage for valuables without individual item limits. Your Rolex collection, rare books, and antique furniture receive automatic coverage at full replacement value. Private client insurers also offer agreed-value coverage, which means they pay the predetermined amount rather than argue about depreciation after a loss. Standard carriers require separate riders for jewelry over $2,500, while private client policies automatically cover items worth $50,000 or more.

Higher Liability Limits Match Your Wealth

Liability coverage represents the biggest difference between standard and private client insurance. Standard policies typically max out at $500,000 in liability coverage, but wealthy families need umbrella protection of $3 million or more. Private client insurers understand that your net worth makes you a lawsuit target, so they build comprehensive liability defense into every policy. They also provide crisis management services when incidents threaten your reputation (something standard insurers never offer).

Specialized Risk Assessment

Private client insurers conduct detailed property inspections that examine security systems, fire suppression equipment, and natural disaster preparedness. Standard insurers rely on basic questionnaires and drive-by assessments. These thorough evaluations help identify vulnerabilities before they become expensive claims, and insurers often require specific security measures for high-value homes.

The complexity of your assets demands equally sophisticated coverage options that address every aspect of your wealth protection strategy.

Key Coverage Areas for High Net Worth Individuals

Property Protection Beyond Standard Limits

High-net-worth families require property coverage that reflects their actual asset values rather than arbitrary policy caps. Standard homeowners policies limit dwelling coverage to $2 million maximum, but luxury homes in markets like Manhattan or Beverly Hills regularly exceed $10 million in replacement costs. Private client insurers provide dwelling coverage up to $50 million or more without multiple policies. These policies also include automatic inflation protection that adjusts coverage annually based on construction cost increases in your specific market.

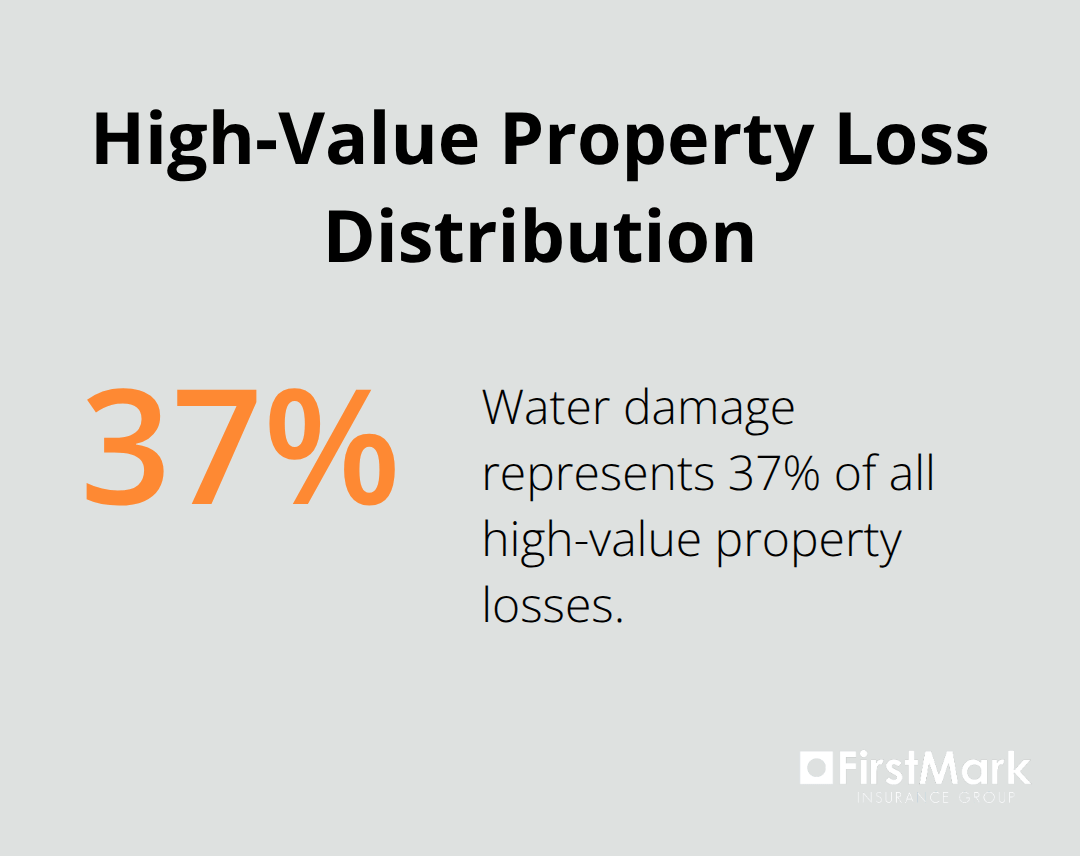

Water damage represents the most expensive claim category for wealthy homeowners (accounting for 37% of all high-value property losses according to industry data). Private client policies mandate water leak detection systems and offer premium discounts up to 15% for homes equipped with monitored systems. Smart home technology integration has become standard, with insurers now requiring interlinked smoke detection and security systems for properties over $3 million in value.

Personal Liability and Reputation Management

Wealthy individuals face lawsuit exposure that extends far beyond standard liability limits. Class-action settlements reached over $4 billion in 2020, with average settlement amounts of $55 million according to recent legal industry analysis, which makes standard umbrella policies insufficient. Private client insurers provide personal liability coverage that starts at $5 million and extends to $100 million for ultra-high-net-worth clients. This coverage includes legal defense costs that fall outside the policy limits and protects your assets from depletion through attorney fees during lengthy litigation.

Crisis management services have become essential components of private client coverage. When wealthy families face public relations disasters, insurers provide immediate access to reputation management specialists and media consultants. These services cost $25,000 to $75,000 monthly when hired independently, but private client policies include them automatically.

Art and Collectibles Coverage Strategies

Fine art insurance requires specialized valuation methods that standard carriers cannot provide. Private client insurers work with certified appraisers who understand market fluctuations in specific collection categories. Art values have increased 87% over the past decade according to Artprice data, which makes regular revaluations essential every three years rather than the previous five-year standard. Policies now provide automatic coverage increases of 10% annually to account for appreciation without new appraisals.

Transportation coverage has become critical as wealthy collectors frequently loan pieces to museums or move collections between residences. Private client policies include worldwide transit coverage and temporary exhibition protection that standard fine arts riders exclude. Storage facility coverage extends to specialized locations like Geneva Freeport, where value accumulation creates unique exposure risks.

The right coverage foundation protects your assets, but success depends heavily on which insurance provider you choose to partner with for these specialized needs.

Which Private Client Insurer Should You Choose

You must evaluate financial stability ratings from AM Best, with A+ or A++ ratings being non-negotiable for wealth protection. Companies rated below A- lack the financial reserves to handle catastrophic claims that could reach $50 million or more for ultra-high-net-worth clients. PURE Insurance maintains an A rating and has paid over $2 billion in claims since 2007, which demonstrates consistent financial performance. Chubb holds an AA- rating and manages $40 billion in net premiums written annually, which provides the capital strength needed for complex high-value claims.

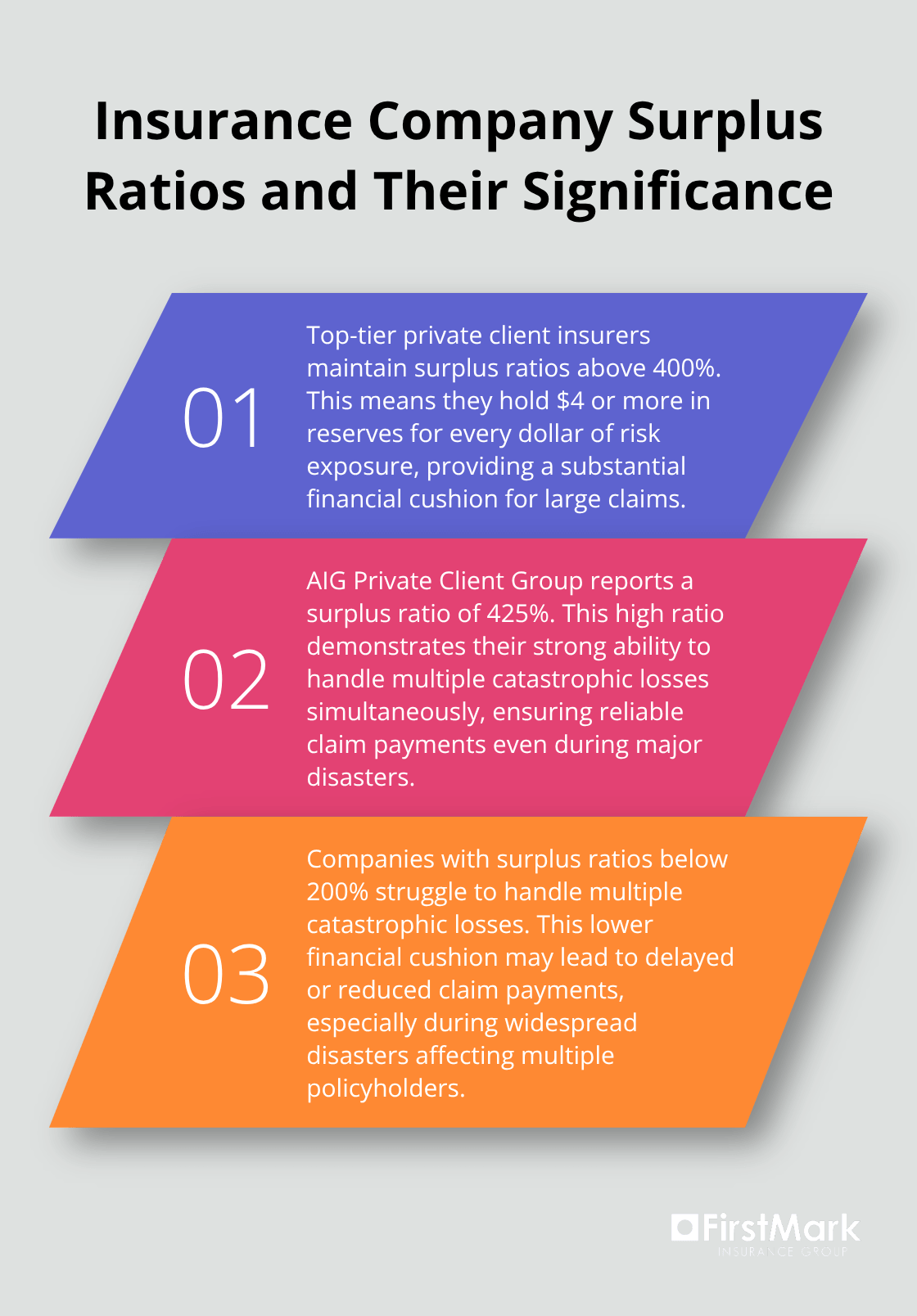

Financial Strength Determines Claim Payment Ability

Insurance company surplus ratios reveal their ability to pay large claims without financial strain. Companies with surplus ratios below 200% struggle to handle multiple catastrophic losses simultaneously, while top-tier private client insurers maintain ratios above 400%. AIG Private Client Group reports a surplus ratio of 425%, which means they hold $4.25 in reserves for every dollar of risk exposure. This financial cushion becomes critical when natural disasters cause significant industry losses within a single event.

Policy Terms That Actually Matter

Private client policies differ dramatically in coverage triggers and exclusion language that standard insurance buyers never encounter. Mysterious disappearance coverage applies when valuable items vanish without evidence of theft, but some insurers limit this coverage to 10% of total policy limits while others provide full replacement value. Newly acquired property coverage varies from 30 days to 365 days, with automatic coverage amounts that range from $100,000 to $2 million. These differences cost clients hundreds of thousands when losses occur during coverage gaps. War and terrorism exclusions have evolved since 2001, with top insurers now including terrorism coverage up to $25 million while others exclude it entirely.

Specialized Agent Expertise Makes the Difference

Private client insurance requires agents who understand complex risk exposures that general insurance agents never encounter. Certified advisors who hold Chartered Property Casualty Underwriter designations possess the technical knowledge needed for proper coverage structure. These specialists conduct comprehensive risk assessments that identify vulnerabilities like art storage conditions, security system adequacy, and natural disaster preparedness. They also coordinate with estate planning attorneys and wealth managers to align insurance strategies with broader financial objectives. Quality insurers provide personal care to ensure each client receives coverage that fits their unique needs rather than standardized policies.

Final Thoughts

Private client group insurance delivers wealth protection that standard policies cannot match. These specialized policies address complex asset structures, higher liability exposures, and unique risks that wealthy families face daily. Comprehensive protection scales with your net worth and includes automatic coverage for valuable collections plus crisis management services.

Regular policy reviews become essential as your wealth grows and asset composition changes. Market fluctuations affect art valuations, property values increase with renovations, and new acquisitions require coverage updates. Annual reviews with qualified specialists identify coverage gaps before they become expensive problems (insurance needs evolve with life changes like property purchases, business ventures, or family growth).

We at FirstMark Insurance Group have guided families through insurance complexities, helping clients find ideal coverage that fits their specific requirements. Our experience with top insurance providers means you receive choices that align with your needs at competitive rates. Contact FirstMark Insurance Group to begin securing comprehensive coverage that protects your wealth and provides peace of mind for your family’s financial future.