Luxury yacht ownership brings incredible freedom on the water, but it also requires specialized protection that standard boat insurance simply cannot provide.

We at FirstMark Insurance Group understand that your yacht represents a significant investment requiring comprehensive coverage tailored to high-value vessels. The right yacht insurance policy protects against unique risks while giving you peace of mind during every voyage.

What Coverage Types Do You Need for Your Yacht

Hull and Machinery Protection

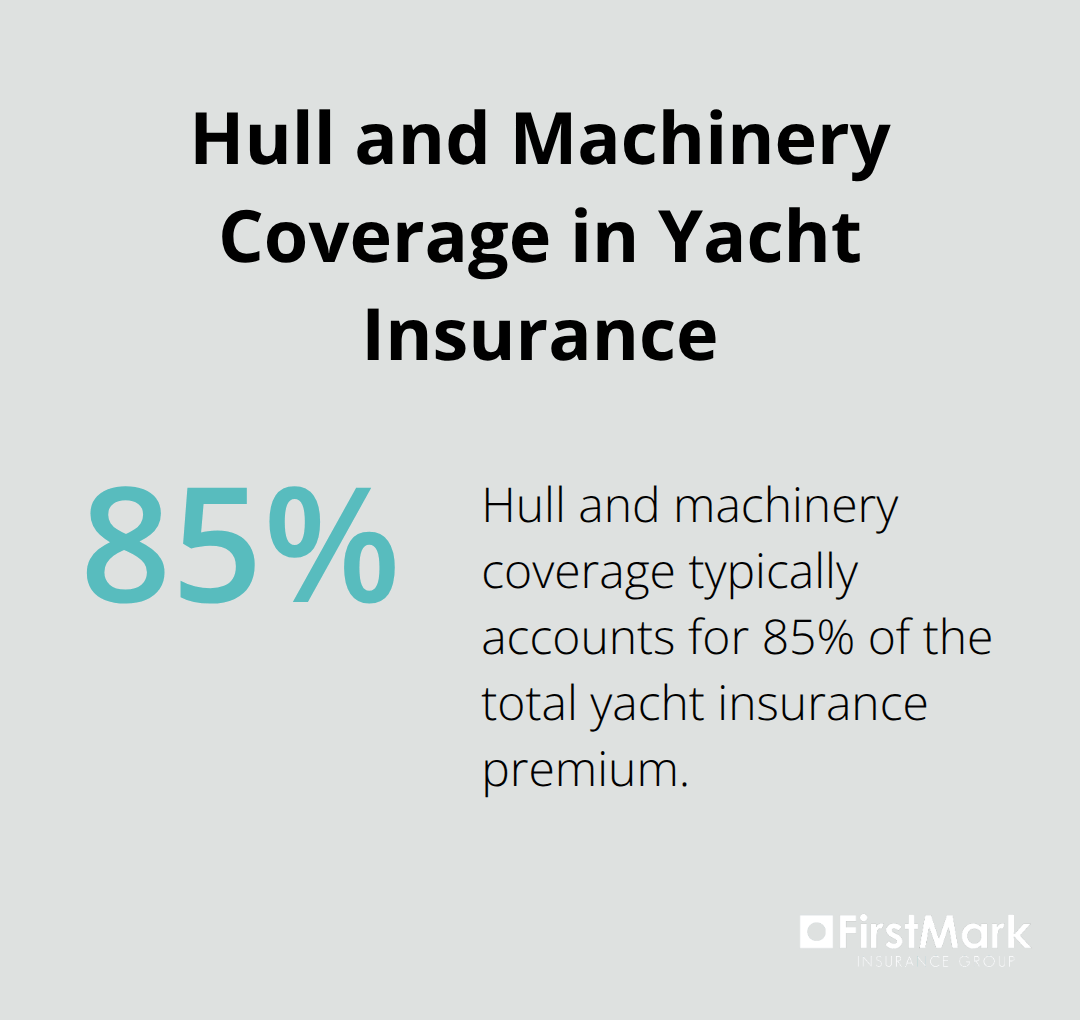

Yacht insurance protection falls into three primary categories that work together to shield you from financial catastrophe. Hull and machinery coverage forms the foundation of your policy and protects the physical vessel itself from damage caused by collisions, grounding, fire, theft, and weather events. This coverage typically accounts for 80-90% of your total premium cost and should reflect your yacht’s current market value.

Most insurers require a marine survey for vessels over $100,000 to establish accurate replacement costs. This appraisal directly impacts your coverage limits and premium calculations, making professional assessment essential for proper protection.

Personal Property and Equipment Coverage

Personal property and equipment protection covers everything aboard your yacht that isn’t permanently attached to the vessel. This includes navigation electronics, fishing gear, personal belongings, and custom modifications like upgraded sound systems or specialized equipment.

Standard policies typically limit personal property coverage to 10% of the hull value (often insufficient for luxury vessels). Luxury yacht owners often need additional coverage for high-end electronics and custom installations that can easily exceed $50,000 in value.

Liability and Medical Payments Protection

Liability and medical payments protection represents your most critical financial safeguard and covers bodily injury and property damage claims against you. The Jones Act protects maritime workers and requires specific crew liability coverage for professional crew members, and marine insurance experts strongly recommend minimum liability limits of $1 million for yachts over 40 feet.

Medical payments coverage handles immediate medical expenses for guests and crew regardless of fault, typically ranging from $5,000 to $25,000 per incident. This coverage proves invaluable when accidents occur far from shore where emergency medical transport costs can reach tens of thousands of dollars.

Understanding these coverage types helps you evaluate how different factors affect your premium costs and policy structure. Professional boat insurance providers can help you find the right coverage whether you’re a lifelong boater or just purchased your first yacht.

What Drives Your Yacht Insurance Costs

Vessel Value and Age Determine Base Premiums

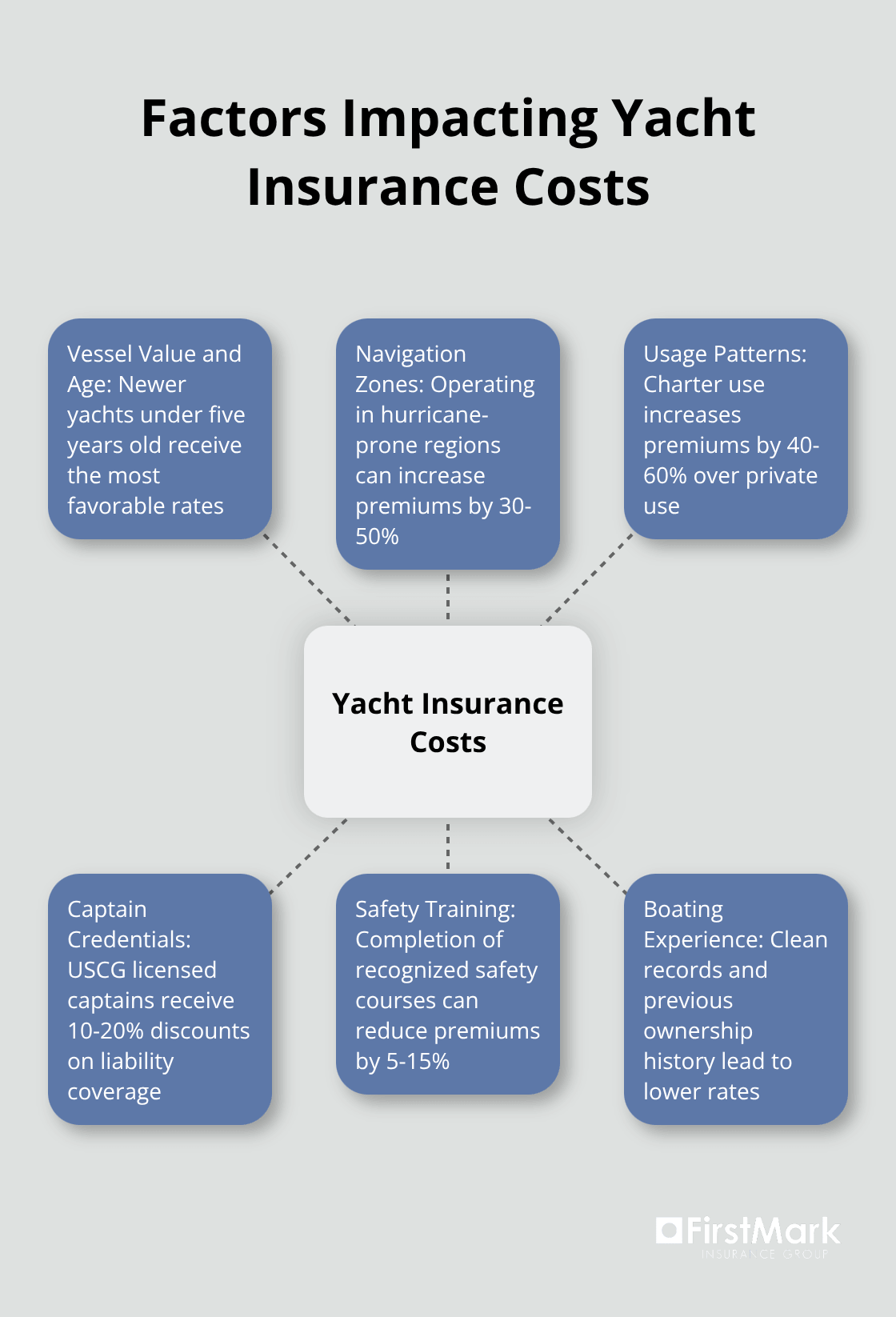

Your yacht’s value and age directly control your insurance costs, with premiums typically ranging from 1% to 5% of the vessel’s insured value annually. A $2 million yacht costs between $20,000 and $100,000 per year to insure, depending on multiple risk factors. Newer yachts under five years old receive the most favorable rates because they feature modern safety equipment and construction standards that reduce claim frequency.

Older vessels face premium increases of 15-25% annually after age 15, as insurers view mechanical systems and outdated safety features as higher risks. Yachts over 25 years old often require specialized underwriters and may face coverage restrictions or higher deductibles to offset increased mechanical failure risks.

Navigation Zones and Usage Patterns Impact Rates

Your cruising area significantly affects premium calculations, with insurers charging 30-50% more for vessels that operate in hurricane-prone regions like the Caribbean during storm season. Yachts restricted to protected waters like the Great Lakes or Puget Sound receive substantial discounts compared to those with worldwide navigation coverage.

Charter use increases premiums by 40-60% over private use policies because commercial operations expose vessels to higher passenger loads and inexperienced operators. Full-time liveaboard status also raises rates by 20-30% due to increased exposure and potential fire hazards from constant electrical usage.

Captain Credentials Reduce Premium Costs

Professional captain certifications and safety training directly lower your insurance costs, with USCG licensed captains receiving discounts of 10-20% on liability coverage. Completion of recognized safety courses like those offered by the US Power Squadrons can reduce premiums by 5-15%, while vessels with professionally trained crew members qualify for additional rate reductions.

Insurers reward experience and offer lower rates to owners with clean boating records and previous yacht ownership history. New yacht owners without marine experience face surcharges of 25-35% during their first policy year, making professional training investments financially beneficial beyond safety considerations.

These cost factors directly influence the type of policy structure that works best for your specific situation and budget requirements. While yacht insurance may seem expensive, quality coverage is affordable when you consider the protection it provides for your valuable investment.

Which Policy Structure Protects Your Investment Best

Agreed Value Provides Superior Protection for Luxury Yachts

Agreed value policies guarantee full replacement cost for total losses without depreciation calculations, which makes them the only sensible choice for luxury yacht owners. These policies lock in your yacht’s value at policy inception based on professional appraisal and protect you from market fluctuations and depreciation disputes during claims. With some agreed value policies, you won’t have to worry about depreciation on partial losses, at least for a certain period or up to a certain age of the vessel.

Actual cash value policies subtract depreciation from claim payouts and leave luxury yacht owners severely underprotected. A five-year-old $2 million yacht might receive only $1.4 million under actual cash value coverage after a total loss, which creates a devastating $600,000 shortfall that destroys your financial position.

Strategic Deductible Selection Balances Cost and Risk

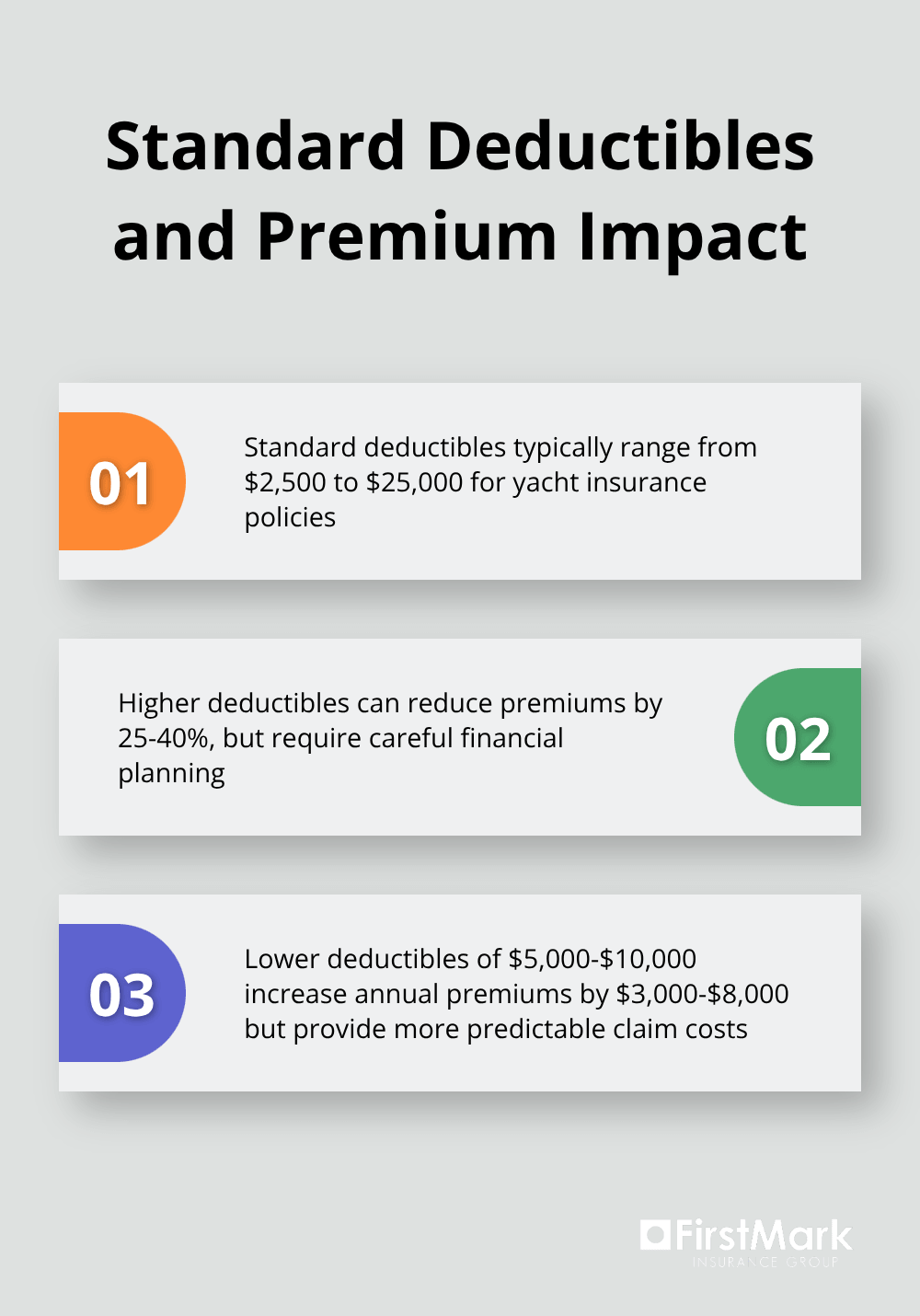

Higher deductibles reduce premiums by 25-40% but require careful cash flow planning for luxury yacht owners. Standard deductibles range from $2,500 to $25,000, with many insurers offering percentage-based options of 1-3% of hull value for vessels over $500,000. A $2 million yacht with a 2% deductible faces $40,000 out-of-pocket costs per claim (making this approach suitable only for owners with substantial liquid assets).

Lower deductibles of $5,000-$10,000 increase annual premiums by $3,000-$8,000 but provide predictable claim costs. This strategy works best for owners who prefer stable budgets over premium savings, especially considering that luxury yacht repairs often exceed $50,000 even for minor incidents.

High-End Equipment Requires Specialized Coverage

Standard yacht policies severely limit coverage for custom electronics, modifications, and specialized equipment that luxury owners routinely install. Navigation systems, custom audio equipment, and performance modifications often exceed $100,000 but receive minimal protection under basic personal property limits. Specialized equipment endorsements protect items not permanently attached to the boat like fishing gear, marine electronics, navigation tools, and safety equipment.

Professional installation documentation and equipment receipts become essential for claims processing (detailed record-keeping becomes a requirement rather than suggestion for luxury yacht owners). Without proper documentation, insurers routinely deny or severely limit payouts for high-value equipment claims.

Final Thoughts

The right yacht insurance balances comprehensive protection with cost-effective coverage that matches your specific vessel and usage patterns. The most expensive policy isn’t always the best choice, but you create devastating financial exposure when you cut corners on essential coverage like agreed value protection or adequate liability limits. Generic insurance agents lack the specialized knowledge needed to properly evaluate yacht-specific exposures that can make or break your financial protection.

Marine insurance specialists understand the unique risks and complex coverage requirements that high-value vessels face. They evaluate crew liability, navigation restrictions, and equipment valuations with the expertise that protects your investment. Professional guidance becomes essential when you need coverage that addresses your yacht’s specific exposures rather than generic solutions that leave dangerous gaps.

We at FirstMark Insurance Group guide families through insurance complexities and help you find ideal yacht insurance coverage at competitive pricing. Our commitment to clear guidance means you receive solutions tailored to your specific needs rather than one-size-fits-all approaches. Your luxury yacht represents a significant investment that deserves protection from professionals who understand marine risks (and the coverage options that address them effectively).