Contractor workers compensation in Washington isn’t optional-it’s a legal requirement that protects your workforce and your business. The rules are specific, the costs vary widely, and getting it wrong can result in serious penalties.

We at FirstMark Insurance Group help contractors navigate these requirements with clarity. This guide walks you through what Washington mandates, how premiums are calculated, and what happens when claims arise.

What Washington Actually Requires for Contractor Coverage

Washington’s workers compensation system operates under a presumption that nearly everyone working is covered unless they meet narrow exemptions. The Department of Labor & Industries applies a six-part test to determine if a worker qualifies as an independent contractor exempt from coverage requirements. To pass this test, the worker must satisfy all six criteria: they operate free from your control or direction, the service falls outside your usual business operations, they maintain a principal place of business separate from yours, they hold their own business license or UBI, they maintain separate business records showing income and expenses, and they are independently established in their trade or occupation. Construction work adds a seventh requirement-the contractor must hold valid contractor registration under RCW 18.27 or possess an electrical license under RCW 18.106 or 19.28. Most contractors fail one or more of these tests, which means they become your responsibility for coverage. A 1099 form does not determine coverage status; L&I uses its own classification criteria regardless of how you label the relationship. This matters because Washington’s 2026 average workers compensation premium increase of 4.9% means the financial consequences of misclassification are rising sharply.

Who Actually Needs Coverage

If you hire workers who don’t pass all six parts of the test, you must obtain a Washington workers compensation account and report their hours quarterly to L&I. You pay premiums based on their classification-construction, electrical, roofing, and similar trades carry higher risk ratings than office work. The state calculates your experience modification rate based on your claims history, which directly affects what you pay; a contractor with multiple claims in the past three years pays substantially more than one with a clean record. You must verify that any subcontractors you hire maintain active L&I accounts within 12 months before awarding work and annually thereafter using L&I’s Verify a Contractor tool. If a subcontractor’s account lapses mid-project, you become liable for unpaid premiums from the lapse date forward. Non-compliance carries real teeth-unpaid premiums trigger penalties and interest, license suspension, debarment from public projects, and potential legal action. The Washington DOSH enforcement framework operates with substantial resources dedicated to audits and verification, making avoidance unrealistic.

Registration and Documentation That Actually Matters

You must document precisely how each worker meets or fails each test component. Keep copies of their business licenses, UBI registrations, proof of separate business addresses, and evidence of independent business operations like separate tax returns or business insurance. Your contract should clearly outline the worker’s independent status and responsibilities, but the actual working relationship-not the contract language-determines L&I’s classification decision. If you previously omitted reportable hours from quarterly filings, you must amend those reports; L&I discovers these gaps through audits and penalties compound over time. The Independent Contractor Guide available on app.leg.wa.gov provides the official framework; using this as your reference protects you far better than relying on assumptions or industry practice. Contact L&I at 360-902-4817 if you need clarification on specific workers, or use their eLearning class on coverage determination to build internal expertise.

What Happens When You Get It Wrong

Misclassification exposes you to unpaid premiums plus penalties and interest calculated from the date the worker should have been covered. L&I audits rely on Washington criteria, not IRS forms-a 1099 or UBI alone does not satisfy L&I’s requirements. Your business license application must indicate that you have workers on your payroll, and you must report their hours accurately on quarterly filings. If you fail to report workers who should be covered, the debt accumulates quickly, and the enforcement resources behind Washington’s system mean L&I will find these gaps. The financial risk intensifies as premium rates climb, making proper classification a matter of significant cost control. Understanding these requirements now prevents far costlier corrections later.

What Drives Your Workers Compensation Premiums in Washington

Your workers compensation premium in Washington is not a fixed number handed down from on high. L&I calculates it based on three concrete factors that shift annually, and understanding how each one works gives you real leverage to control costs.

The Three Factors That Shape Your Premium

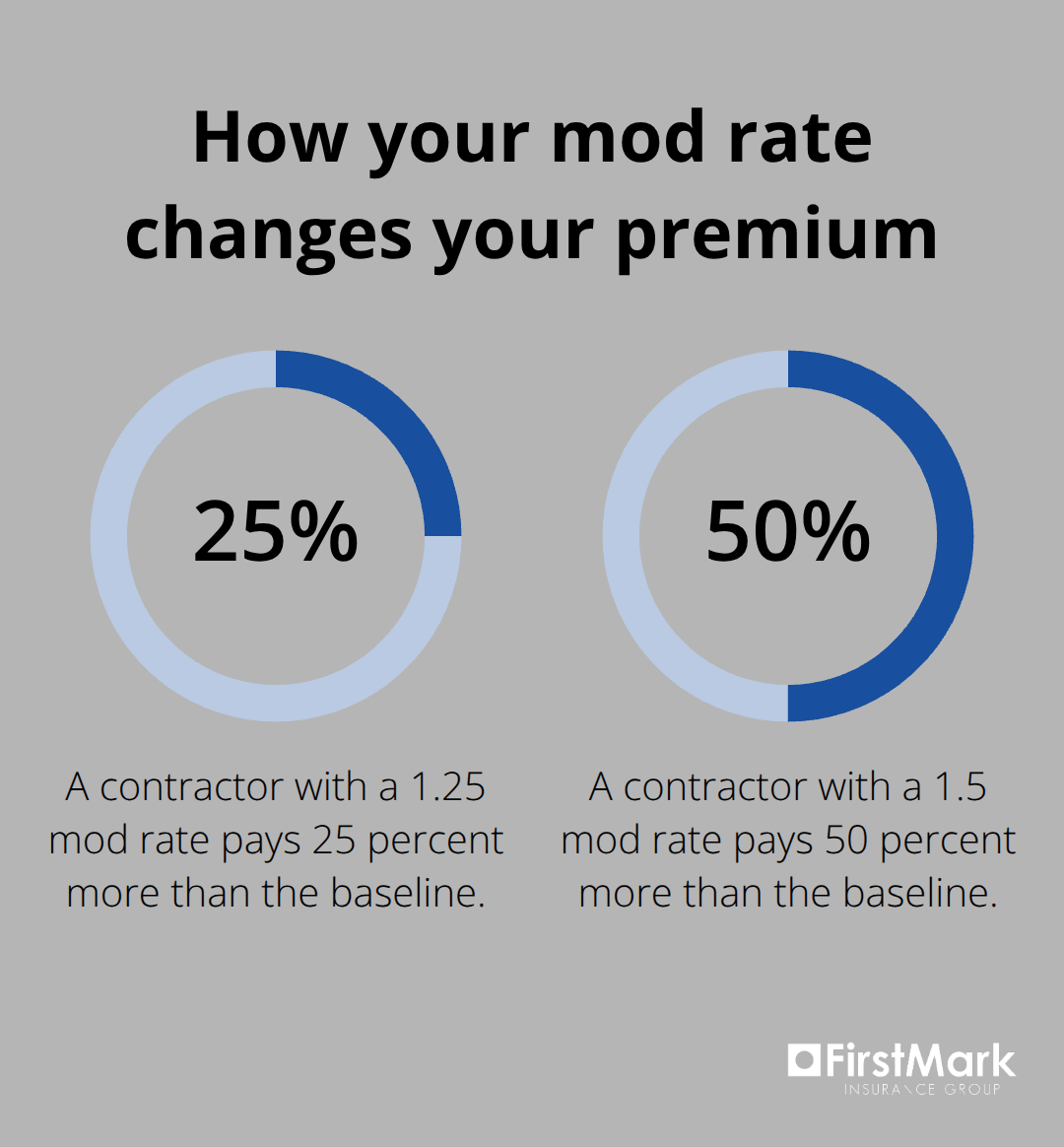

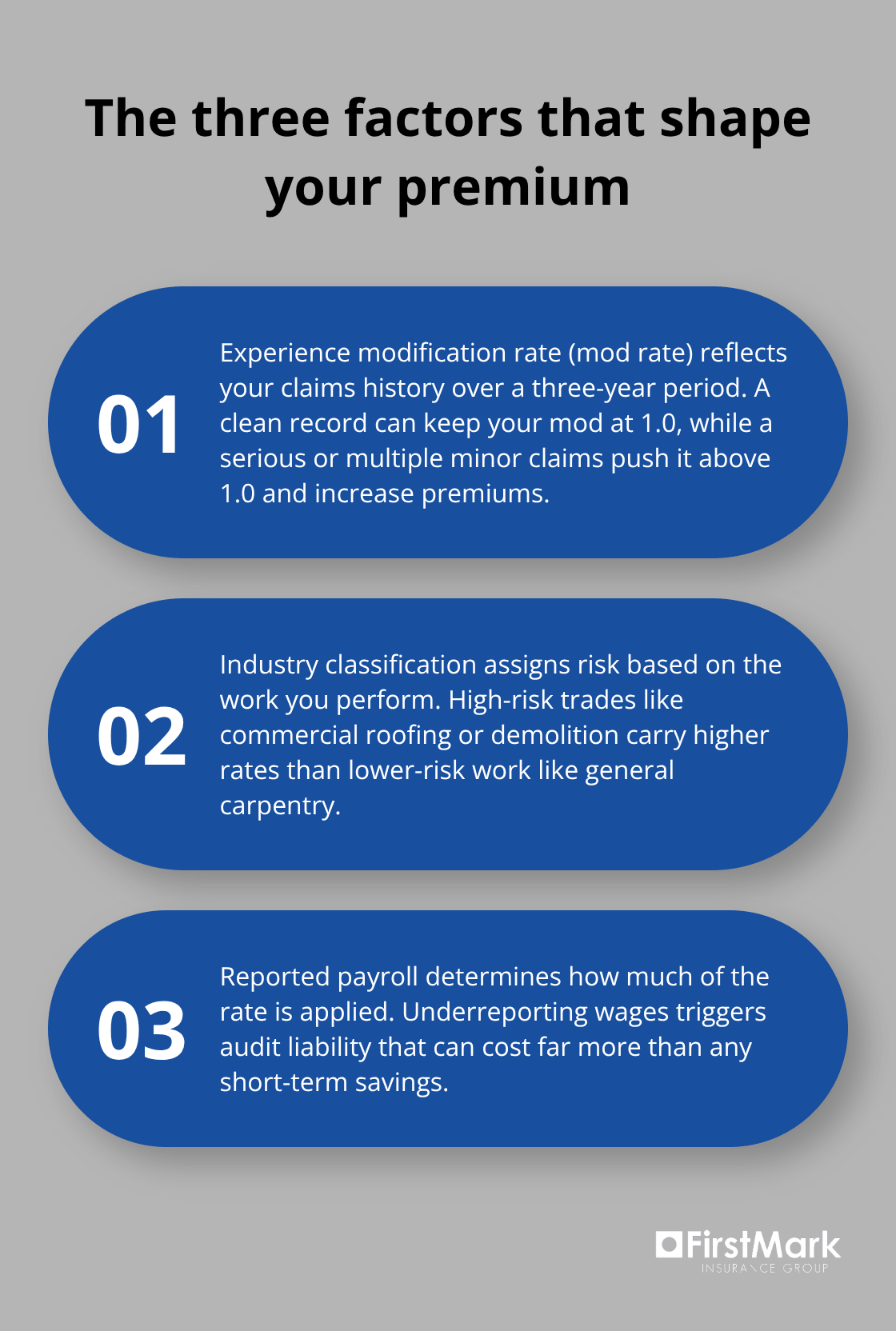

The first factor is your experience modification rate, commonly called your mod rate, which reflects your claims history over a three-year period. If your business filed zero claims in that period, your mod rate sits at 1.0, meaning you pay the standard premium for your industry classification. A single serious claim or multiple minor ones pushes your mod rate above 1.0, multiplying your base premium upward. A contractor with a mod rate of 1.25 pays 25 percent more than the baseline; one at 1.5 pays 50 percent more.

The second factor is your industry classification, which L&I assigns based on the type of work you perform. Construction trades carry risk ratings that vary dramatically-general carpentry sits lower than electrical work, which sits lower than commercial roofing or demolition. Your premium per $100 of payroll might be $2.50 for light carpentry but $8.00 for electrical work, a threefold difference that compounds across your entire payroll.

The third factor is your actual reported payroll. L&I multiplies your classification rate by your total employee hours and wages, so underreporting wages to reduce premiums creates audit liability that costs far more than the savings ever could. The 2026 premium increase of 4.9% across Washington means these calculations hit harder than they did last year, making cost control strategies essential rather than optional.

How Your Claims History Affects Future Costs

Your experience mod rate is the one factor you can actively influence going forward, which is why injury prevention and claims management deserve real attention and budget. Contractors who implement formal safety programs, provide proper PPE at no cost to workers, and conduct regular safety training see fewer claims and lower mod rates over time. Detailed incident documentation strengthens your position during L&I audits and protects your workers simultaneously.

If you experience a workplace injury, report it to L&I within 24 hours for non-hospitalized cases and within 8 hours for hospitalizations or fatalities; prompt reporting protects both your workers and your claims record. Some contractors mistakenly believe that discouraging workers from filing claims keeps their mod rate low, but L&I’s audit process catches unreported injuries through medical records and worker interviews. The penalties for hiding claims far exceed any premium savings you might achieve.

Strategies to Lower Your Premiums Without Cutting Corners

Classify workers accurately in the correct risk category-misclassifying a roofer as a carpenter artificially lowers premiums until an audit discovers the error and retroactively charges you for years of underpayment. Review your quarterly L&I reports before submitting them to confirm that hours and wage data match your payroll records; errors in reporting create audit flags that trigger detailed investigations.

If you operate multiple locations or divisions, ask L&I whether you qualify for separate accounts by trade, since a general contractor with both office staff and field crews might lower overall premiums by segregating classifications. Consider whether subcontracting specific high-risk work to licensed specialists makes financial sense compared to bringing that work in-house; a roofing contractor who subcontracts electrical work to a licensed electrician avoids the higher electrical classification rate on payroll while maintaining project control.

Classification errors often persist for years until someone questions them, which means a thorough review of your current codes can uncover savings you did not know existed. Your quarterly filings and classification assignments warrant the same attention you give to payroll accuracy, since both directly affect your bottom line and your compliance standing with L&I.

What Happens When a Contractor Gets Injured on the Job

Filing the Injury Report Correctly

When a worker on your crew sustains an injury, the filing process begins immediately and the details matter far more than most contractors realize. Your worker must report the injury to the Washington Department of Labor & Industries within one year per RCW 51.28.050, though filing sooner substantially improves the odds of approval and faster benefit processing. The worker can file by phone at 877-561-3453, online through L&I’s portal, or at their doctor’s office. The report must include the injury location, names and contact information for any witnesses, your company’s details, wage information, the worker’s dependents’ names and dates of birth, the treating doctor’s name, and the hospital or clinic where treatment occurred. Your documentation team should compile detailed incident records, witness statements, and medical reports during those first hours, since this foundation shapes the entire claim trajectory and either enables smooth resolution or prolongs disputes.

Selecting Medical Providers and Meeting Notification Deadlines

The worker can choose any physician who holds L&I approval as an examiner. If the first doctor isn’t approved, a care transfer form allows switching to another provider without penalty. L&I categorizes injuries into hospitalized cases (requiring notification within 8 hours) and non-hospitalized cases (requiring notification within 24 hours). Failures to report trigger penalties that stack quickly, making prompt communication with L&I essential. Self-insured employers file using the Self-Insured Accident Report form, which they can submit online or by mail, and should verify their filing status with L&I to avoid processing delays.

Understanding What Coverage Includes and Excludes

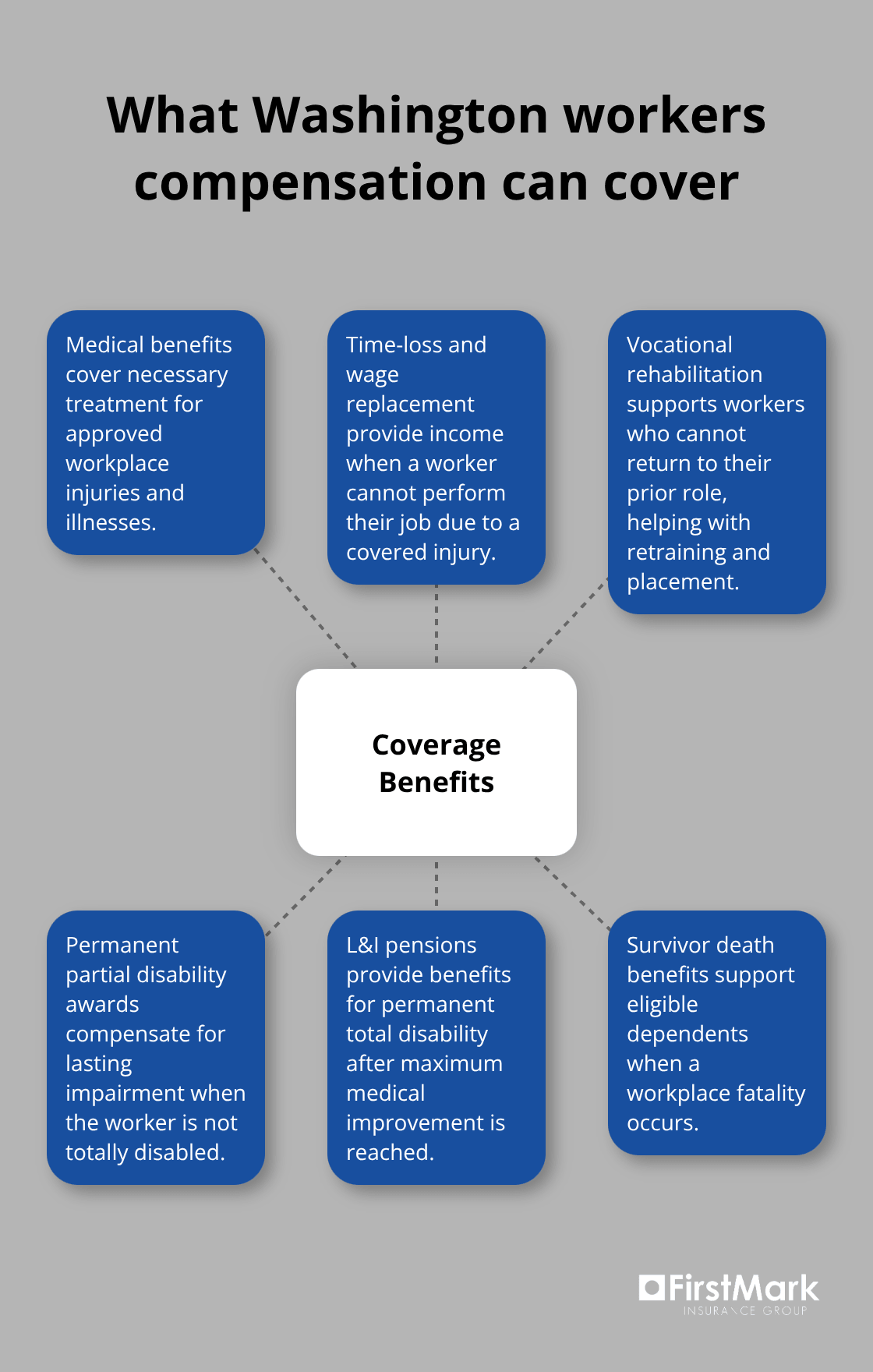

Washington’s workers compensation system covers medical benefits, time-loss and wage replacement, travel reimbursement for medical appointments, vocational rehabilitation for workers unable to return to their previous role, permanent partial disability awards, L&I pensions for permanent total disability, and survivor death benefits for fatalities. The system does not cover injuries occurring outside work, injuries caused primarily by the worker’s violation of a safety rule you explicitly communicated, or pre-existing conditions unrelated to the workplace incident. Medical benefits flow separately from time-loss wages, meaning a worker might receive treatment coverage while their wage replacement claim remains under review, or vice versa.

Managing Claims Timeline and Independent Medical Examinations

Claims typically resolve within 60 days if documentation is complete and the injury is straightforward, though complex cases involving disputed causation or permanent disability can extend to 6 months or longer. If L&I schedules an Independent Medical Examination, the worker should contact an experienced workers compensation attorney beforehand to protect their interests, since IME findings can restrict benefits or determine whether the worker reaches maximum medical improvement. IME outcomes may include findings of exaggeration, injury outside work, preexisting conditions, light-duty requirements, or maximum medical improvement status.

Your Obligations as an Employer

Your role as an employer includes addressing injuries promptly, refusing to discourage workers from filing claims, and avoiding any discrimination or harassment related to claim filing. All of these carry legal penalties under Washington employment law and L&I regulations. You must not retaliate against workers for reporting injuries or filing claims, and you must cooperate fully with L&I investigations and requests for documentation throughout the claims process.

Final Thoughts

Contractor workers compensation in Washington demands your attention because the rules carry real financial consequences and L&I enforces them consistently. You now understand that a 1099 form does not exempt workers from coverage, that your experience mod rate directly controls what you pay, and that the 2026 premium increase of 4.9% amplifies the cost of misclassification. Audit your current worker classifications against L&I’s six-part test, document how each worker meets or fails each criterion, and correct any gaps before an audit forces retroactive payments.

Your mod rate represents the one premium factor you can actively influence through injury prevention and claims management. Implement a safety program that reduces incidents, report injuries promptly to L&I, and maintain detailed documentation throughout the claims process. These actions lower your costs while protecting your workforce simultaneously.

Professional guidance simplifies contractor workers compensation compliance and aligns your coverage with your actual business needs. Contact FirstMark Insurance Group to review your current classification structure and coverage options. A thorough assessment now prevents far costlier corrections later.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation