Owning a Ferrari, Lamborghini, or McLaren brings unique insurance challenges that standard auto policies can’t handle. These high-performance vehicles require specialized coverage due to their extreme values and rare components.

At FirstMark Insurance Group, we see exotic car insurance claims that highlight why traditional policies fall short. Your million-dollar supercar needs protection that matches its extraordinary nature.

What Makes a Car Exotic and Why Insurance Differs

Insurance companies define exotic cars through specific criteria that extend beyond simple price tags. Vehicles with horsepower that exceeds 500, limited production runs under 10,000 units annually, or manufacturer’s suggested retail prices above $100,000 typically qualify. Ferrari, Lamborghini, McLaren, Bugatti, and Koenigsegg models automatically fall into this category, while high-performance variants of mainstream brands like the Porsche 911 Turbo S or Audi R8 also qualify.

Replacement Parts Create Coverage Complexity

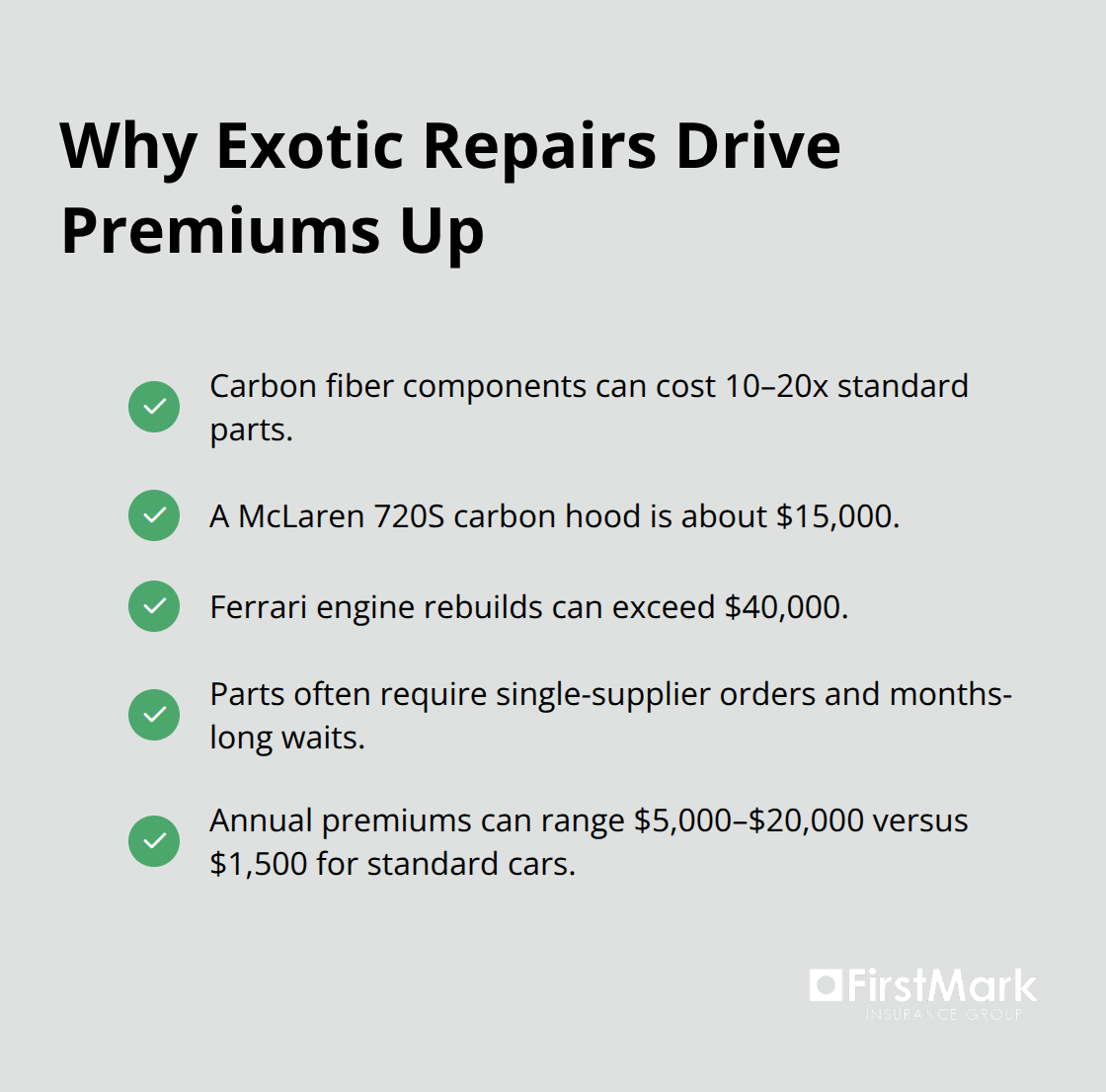

Exotic vehicles require specialized components that cost 10 to 20 times more than standard car parts. A replacement carbon fiber hood for a McLaren 720S costs approximately $15,000, while a Ferrari engine rebuild can exceed $40,000. These parts often come from single suppliers with months-long wait periods (sometimes extending beyond six months for rare components). Insurance companies factor these extended repair times and inflated costs into premium calculations, which results in annual policies that range from $5,000 to $20,000 compared to $1,500 for conventional vehicles.

Certified Technician Shortage Drives Up Claims

Only factory-certified technicians can properly service exotic vehicles, which creates a nationwide shortage of qualified repair facilities. Lamborghini operates fewer than 50 authorized service centers across the United States, while McLaren maintains just 25 locations. This scarcity forces owners to transport damaged vehicles hundreds of miles for proper repairs, which adds towing and storage costs to claims. Exotic car claims regularly include transportation expenses that exceed $3,000 alone.

Limited Production Numbers Affect Availability

Manufacturers produce exotic cars in extremely limited quantities, which directly impacts parts availability and repair complexity. Bugatti produces fewer than 80 vehicles annually worldwide, while Koenigsegg manufactures approximately 20 cars per year. This limited production means replacement parts often require custom fabrication or direct factory orders (with lead times that can stretch beyond 12 months). These factors combine to create insurance challenges that standard policies simply cannot address, which leads us to examine the specific coverage options that exotic vehicle owners need.

Key Coverage Options for Exotic Vehicles

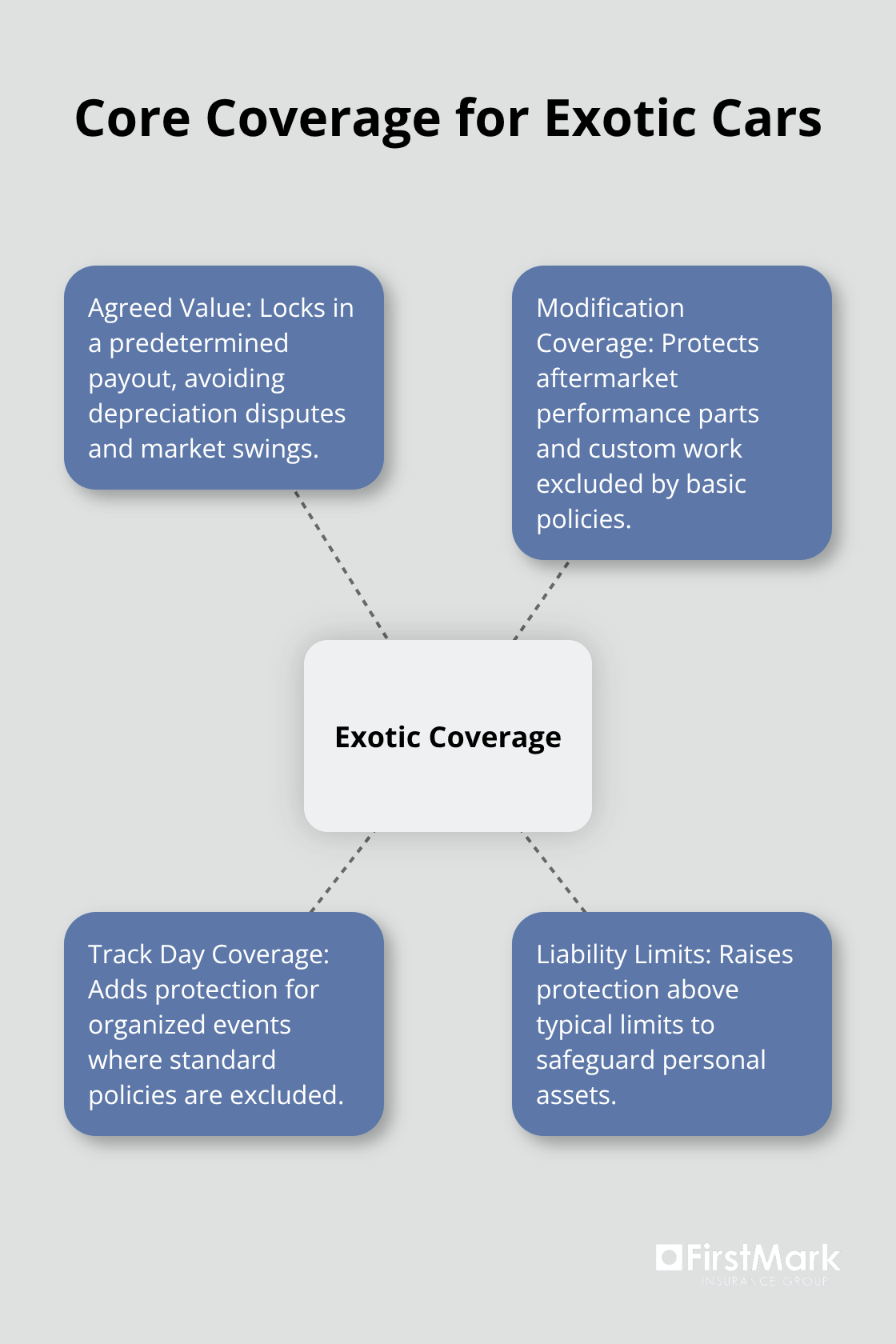

Agreed value policies provide the only reliable protection for exotic vehicles because they guarantee a predetermined payout amount regardless of market fluctuations or depreciation disputes. Unlike actual cash value coverage that pays current market value minus depreciation, agreed value policies lock in your vehicle’s worth at policy inception. A 2019 Ferrari 488 Pista originally valued at $350,000 might receive only $280,000 under actual cash value coverage after three years, but agreed value coverage pays the full agreed amount. This difference becomes even more pronounced with limited production vehicles that actually appreciate over time.

Custom Modifications Need Specialized Protection

Standard exotic car policies exclude aftermarket modifications, which creates significant coverage gaps for owners who invest in performance upgrades. A McLaren 720S with $50,000 in custom carbon fiber aero components, upgraded turbos, and ECU tuning receives zero compensation for these modifications under basic coverage. Specialty modification coverage adds 15-20% to your premium but protects investments in custom exhausts, suspension systems, and body modifications. Track-focused modifications like roll cages, racing seats, and fire suppression systems need separate coverage endorsements that cost approximately $500-800 annually per $10,000 in modifications.

Track Day Coverage Fills Critical Protection Gaps

Most exotic car policies automatically exclude coverage during competitive events, track days, and racing activities, which leaves owners completely exposed during high-performance activities. Progressive and State Farm specifically void coverage the moment your vehicle enters a racing facility, while specialty insurers like Hagerty offer track day coverage for an additional 25-40% premium increase. This specialized coverage protects against collision damage, mechanical failure, and liability claims that occur during organized events. Without track coverage, a single incident during a Cars and Coffee track session could result in a $200,000+ out-of-pocket expense for a damaged Lamborghini Huracán.

Liability Limits Must Match Vehicle Value

Exotic car owners face unique liability exposure that standard policy limits cannot address adequately. When your McLaren 765LT causes an accident, the other party’s medical bills and property damage claims often exceed typical $100,000 liability limits (especially in multi-vehicle collisions). Specialty insurers recommend liability coverage for exotic vehicle owners. This increased protection costs an additional $300-500 annually but prevents personal asset exposure in serious accidents.

These specialized coverage options work together to protect your investment, but premium costs vary dramatically based on several key factors that insurers evaluate when calculating your rates.

Factors That Impact Your Premium Costs

Vehicle Value Forms the Foundation for Premium Calculations

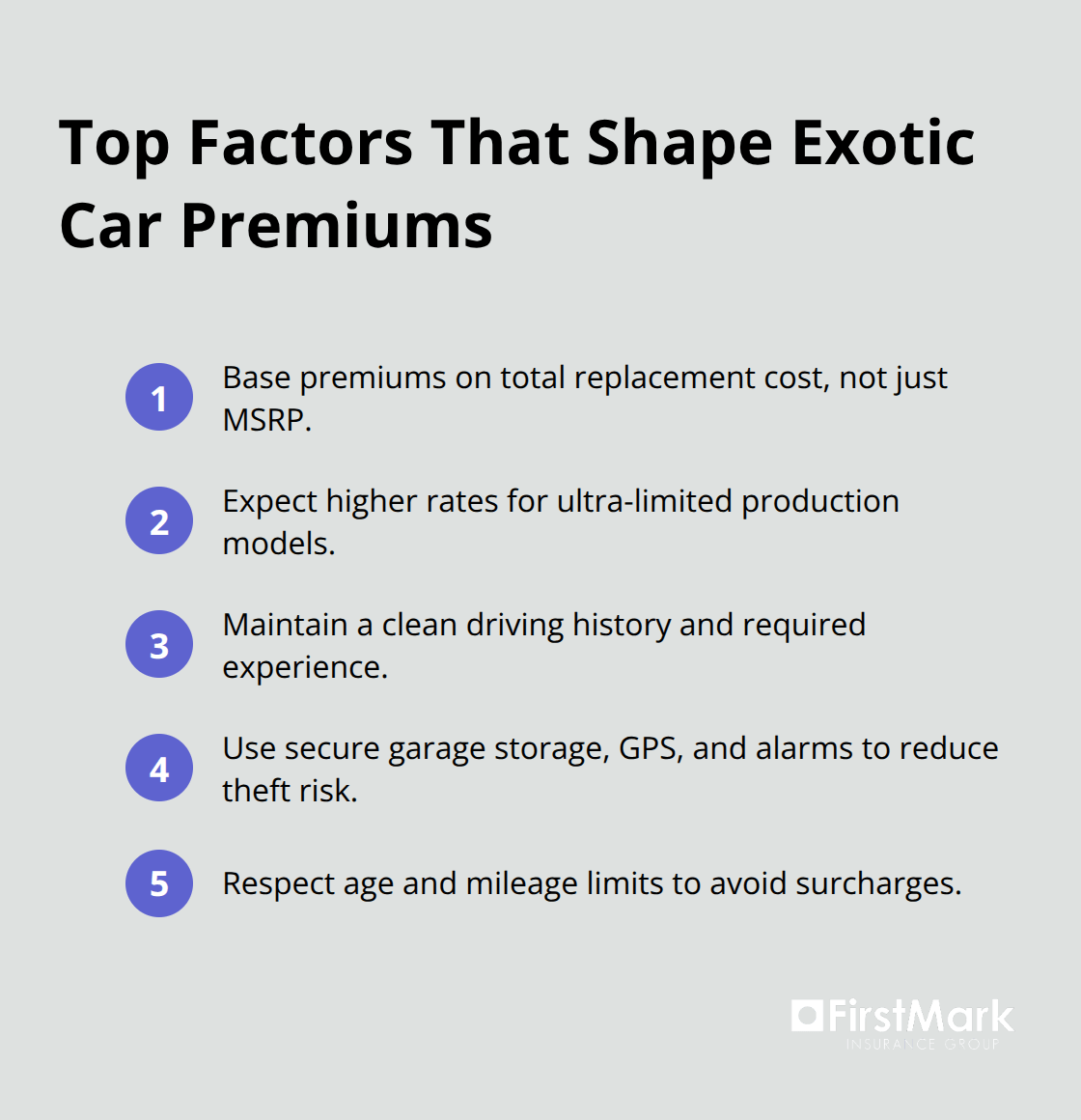

Insurance companies base exotic car premiums on replacement cost calculations that extend far beyond simple market value. A 2023 McLaren Artura with a $233,000 MSRP requires $280,000 in total loss coverage when you factor in taxes, registration fees, and delivery costs. Limited production vehicles command even higher premiums because insurers cannot rely on standard depreciation models.

Pagani produces only 40 Huayra models annually, which means replacement costs remain unpredictable and parts availability creates extended repair timelines. Insurance companies charge 15-25% higher premiums for vehicles with production runs under 1,000 units compared to mass-produced exotics like the Porsche 911 Turbo S.

Driver History and Experience Requirements Shape Eligibility

Specialty insurers often have specific eligibility requirements including minimum driver age and experience before they approve exotic car coverage. Progressive rejects applications from drivers with DUI convictions within seven years, while Hagerty requires proof of defensive course completion for drivers under 25. Insurance companies analyze your vehicle portfolio as a risk indicator. Owners who maintain daily driver vehicles alongside their exotic cars receive 10-15% premium discounts because insurers view limited exotic car usage as lower risk exposure. Single violations can increase premiums by 20-30%, while at-fault accidents trigger immediate policy reviews and potential coverage cancellation.

Security Measures Directly Reduce Premium Costs

Proper storage and security systems provide the most effective method for premium reduction on exotic car insurance. Garage storage requirements are non-negotiable for most policies, while additional security features create measurable premium reductions. GPS systems reduce theft coverage costs by 8-12%, while comprehensive alarm systems with smartphone integration provide 5-10% discounts. Some insurers offer 15-20% premium reductions for vehicles stored in climate-controlled facilities with 24-hour security. Geographic location significantly impacts these calculations, as each state sets its own rules for what information insurance companies can use when pricing auto insurance.

Age and Mileage Restrictions Affect Coverage Options

Insurance companies impose strict age and mileage limitations that directly impact premium calculations. Most exotic car policies require drivers to be at least 25 years old, while some specialty insurers set the minimum age at 30 for vehicles exceeding $500,000 in value. Annual mileage restrictions typically cap usage at 2,500-5,000 miles per year, with excess mileage penalties that range from $0.50 to $2.00 per mile. Vehicles driven more than 7,500 miles annually face premium increases of 25-40% because insurers view higher mileage as increased accident exposure and accelerated depreciation risk.

Final Thoughts

Exotic car insurance demands specialized coverage that standard auto policies cannot deliver. Agreed value policies shield your investment from depreciation disputes, while modification coverage protects custom upgrades that can exceed $50,000. Track day protection covers critical gaps that void standard coverage during performance events.

Premium costs mirror the unique risks these vehicles present. Limited production numbers, specialized parts that cost 10-20 times more than standard components, and certified technician shortages push annual premiums between $5,000 and $20,000. Your record, storage security, and mileage restrictions directly affect these costs (with violations potentially increasing rates by 20-30%).

Specialty insurance providers offer the expertise that mainstream insurers often lack in high-value vehicle protection. These specialists understand exotic car ownership complexities and provide coverage options that match your vehicle’s extraordinary nature. At FirstMark Insurance Group, we help you navigate insurance complexities and find coverage that fits your specific needs at competitive rates.