Insurance premiums don’t have to break your budget. Smart policyholders save hundreds of dollars annually by taking advantage of available discounts.

We at FirstMark Insurance Group see clients reduce their home and auto insurance costs by 20-40% through strategic discount stacking. The key lies in knowing which discounts exist and how to qualify for them.

Which Home Insurance Discounts Cut Your Premiums Most

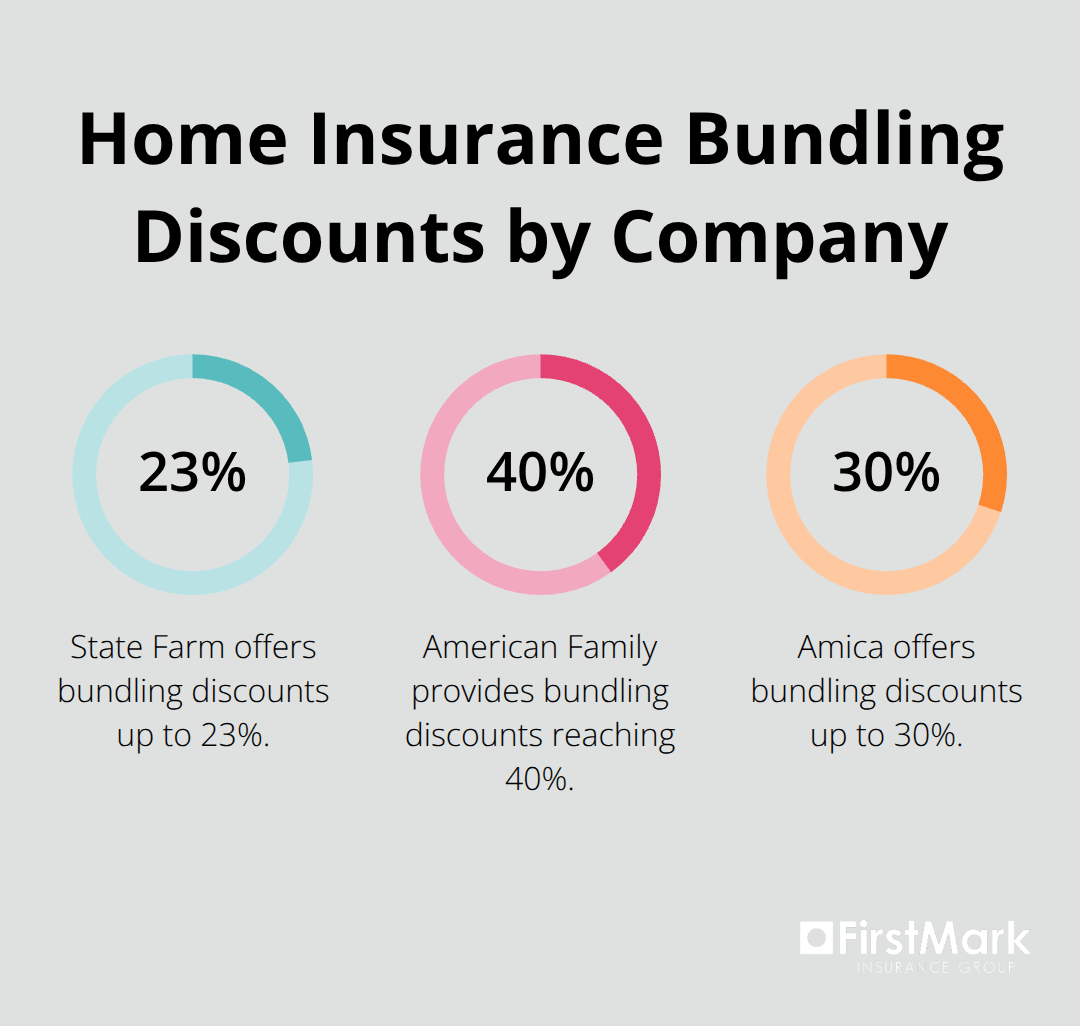

Multi-policy bundling delivers the biggest savings opportunity for homeowners. State Farm leads with bundling discounts that reach 23%, which saves customers approximately $787 annually. American Family offers bundling discounts up to 40%, while Amica provides discounts that reach 30%. The average bundling discount across insurers sits at 14%, which translates to $466 in annual savings. These discounts apply when you combine home insurance with auto, which creates substantial cost reductions that compound over time.

Security Features That Actually Lower Premiums

Home security systems generate measurable discounts, but specific features matter most. Smoke detectors, burglar alarms, and fire extinguishers typically reduce premiums by 5-10%. Impact-resistant windows can lead to insurance discounts potentially up to 45%, but require documentation and proof of proper installation. Fortified homes (designed for severe weather events) receive preferential rates from most insurers. Non-smoker households qualify for fire risk reduction discounts across major carriers.

Claims-Free Status Pays Real Dividends

Claims-free discounts reward policyholders who avoid claims for extended periods. Most insurers offer these discounts after three to five consecutive claim-free years. Loyalty discounts increase with policy tenure, though annual rate shopping remains essential for competitive prices. Full premium payments generate 5-10% discounts on average. Paperless billing adds another small discount layer (typically 2-3%).

New Construction and Green Home Benefits

New home discounts apply to recently constructed properties that meet current building codes. These homes reflect lower risk profiles for insurers due to updated electrical systems and modern materials. LEED certified properties may qualify for discounted homeowner’s insurance, tax breaks and other incentives. Builders from insurer-approved contractor networks can trigger repair discounts for future claims.

Auto insurance discounts work differently but offer equally significant savings opportunities.

Which Auto Insurance Discounts Save You Most Money

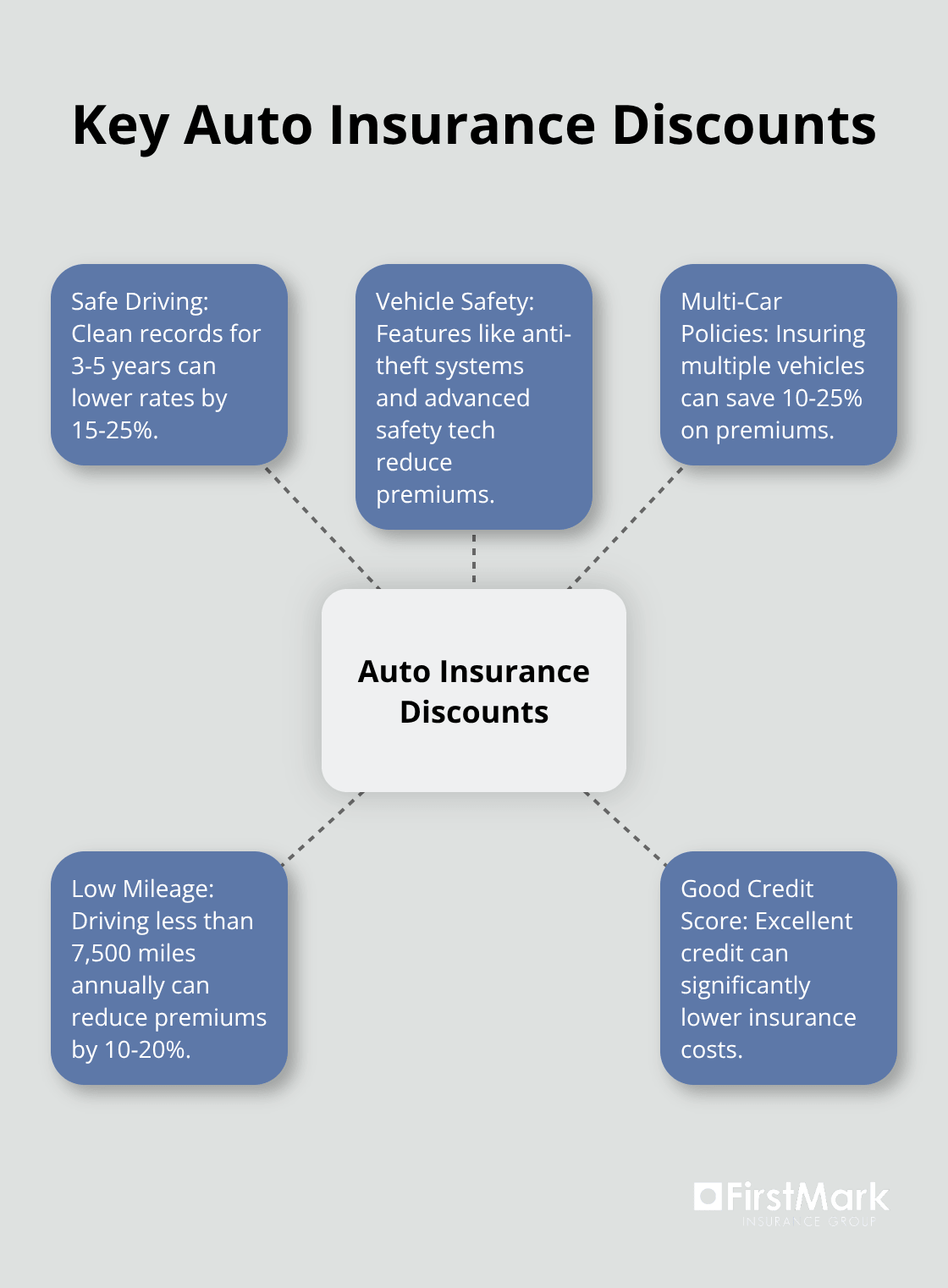

Safe drivers access the most substantial auto insurance discounts available today. State Farm’s Drive Safe & Save program monitors driver behavior and rewards consistent safe practices with significant premium reductions. Defensive driving course completion typically yields 5-10% premium reductions across major carriers, with some insurers offering larger discounts for recent graduates. Clean records without accidents or violations for three to five years qualify drivers for preferred rates that can be 15-25% lower than standard prices.

Vehicle Safety Features That Insurance Companies Reward

Anti-theft systems and advanced safety features directly impact premium calculations. Vehicles equipped with anti-lock brakes, airbags, and electronic stability control receive safety discounts from most insurers. Anti-theft devices (car alarms, steering wheel locks, and GPS tracking systems) generate premium reductions of 5-15%. Modern vehicles with automatic emergency braking, blind spot monitoring, and collision avoidance systems qualify for additional safety technology discounts.

Multi-Car and Low Mileage Advantages

Multi-car policies create substantial savings opportunities, with most insurers offering 10-25% discounts when you insure multiple vehicles. Low mileage drivers who log fewer than 7,500 miles annually often qualify for usage-based discounts that can reduce premiums by 10-20%. Annual mileage verification through odometer readings or telematics devices helps insurers calculate accurate risk profiles and corresponding discount rates.

Credit Scores Impact Your Auto Insurance Costs

Credit history significantly affects auto insurance prices in most states, with poor credit resulting in premium increases of 20-50% compared to excellent credit scores. Good credit becomes essential for access to the lowest available rates. Payment history, credit utilization, and length of credit history all factor into insurance scoring models that determine final premium costs (along with traditional risk factors like age and location).

Smart discount strategies require more than just knowing what discounts exist – you need a systematic approach to maximize your total savings across both policies. Professional agents can help you identify all available discounts and compare rates across multiple providers to ensure you’re getting the best possible deal.

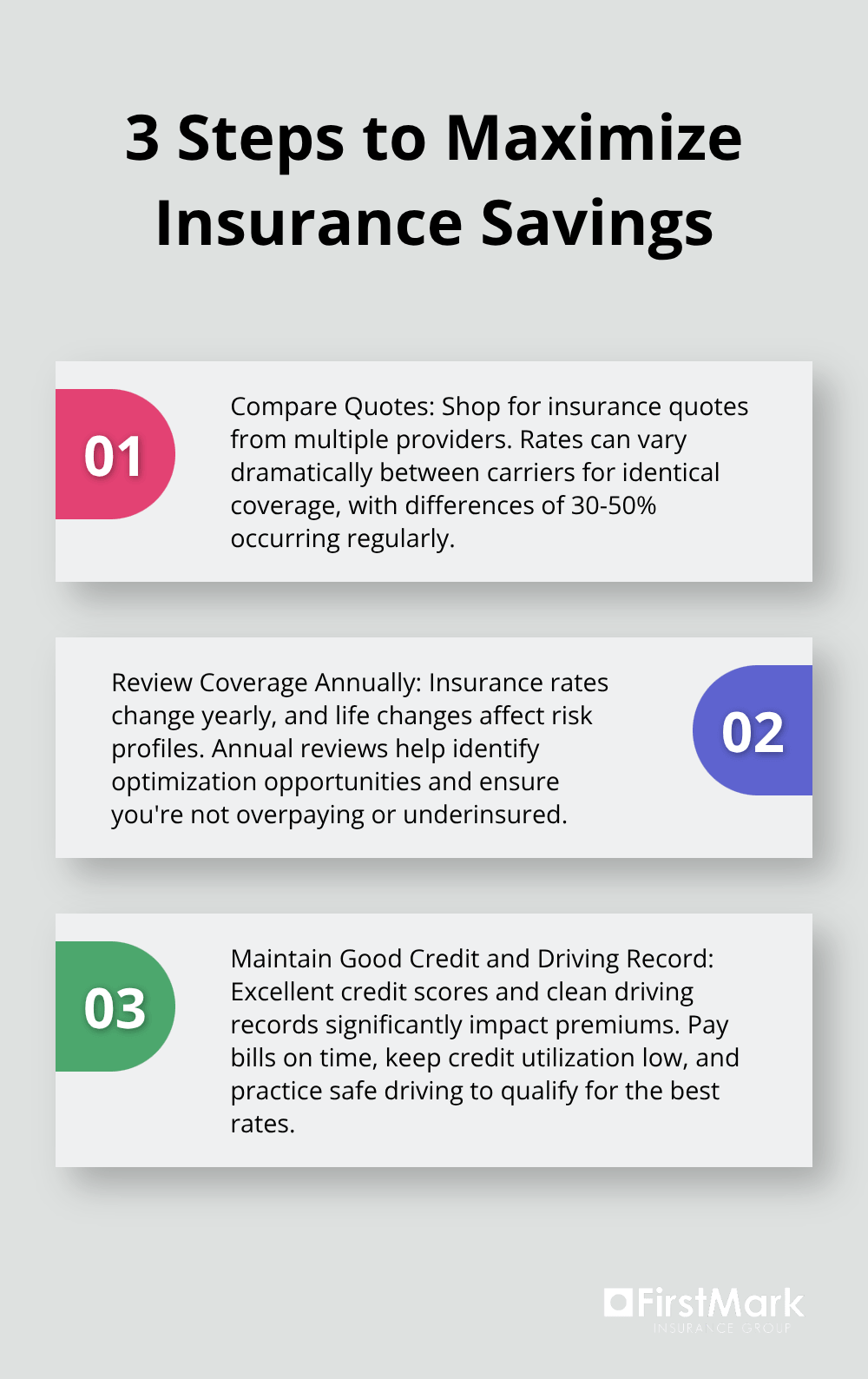

How Do You Actually Maximize Insurance Savings

Compare Quotes from Multiple Providers

You must shop for insurance quotes from multiple providers to reduce your premiums effectively. The National Association of Insurance Commissioners data shows rates vary dramatically between carriers for identical coverage. Auto-Owners offers the lowest bundled coverage at $1,878 annually, while other major carriers charge significantly more for comparable policies. State Farm provides the highest bundling discounts at 23%, but their base rates might still exceed competitors after discount application. You should obtain quotes from at least three different insurers to establish accurate price comparisons, as rate differences of 30-50% between carriers occur regularly.

Review Your Coverage Annually

Insurance rates change annually, and policyholders who skip annual reviews miss significant savings opportunities. Credit scores fluctuate, records improve, and life changes affect risk profiles that determine premium calculations. Home values shift due to market conditions, which requires coverage adjustments to avoid overpayment for unnecessary limits or underinsurance gaps. Vehicle depreciation reduces the need for comprehensive coverage on older cars, while new safety features on replacement vehicles qualify for additional discounts. Professional agents track these changes and identify optimization opportunities that self-service customers typically overlook.

Maintain Excellent Credit Scores

Credit scores impact insurance premiums in most states, with drivers with bad credit scores paying an average of $1500 more than those with perfect scores. Payment history accounts for 35% of your credit score calculation, which makes on-time insurance premium payments essential for favorable rates. Credit utilization below 30% of available limits improves scores and reduces insurance costs. Length of credit history contributes 15% to credit scores (so maintain older accounts for better insurance rates). Single accidents can increase premiums by 15-25% for three to five years depending on the carrier and violation severity.

Keep Your Driving Record Clean

You must maintain consistent safe practices to avoid premium increases. Traffic violations and accidents stay on your record for three to five years with most insurers. Defensive courses can reduce premiums by 5-10% and may remove points from your record. Clean records without violations qualify drivers for preferred rates that run 15-25% lower than standard prices. Some insurers offer accident forgiveness programs that prevent your first accident from affecting your rates (though these programs often cost extra).

Seasonal Coverage Adjustments

Consider adjusting coverage based on seasonal usage patterns for recreational vehicles and watercraft. You can reduce RV insurance to comprehensive-only coverage during winter storage months, then restore full coverage when ready for travel season. Similarly, boat insurance premiums can be optimized through seasonal adjustments and available discounts that reduce annual costs significantly.

Final Thoughts

Home and auto insurance discounts reduce your premiums by 20-40% when you apply them strategically. Multi-policy bundling generates the largest savings, with State Farm offering 23% discounts and American Family reaching 40%. Security features, claims-free records, and safe driving habits create additional layers of savings that compound over time.

The discount landscape changes frequently as insurers adjust their programs and introduce new offerings. Rate variations of 30-50% between carriers make annual shopping essential, even with existing discounts. Credit scores, driving records, and coverage needs shift throughout the year (which affects your qualification for various discount programs).

Experienced agents help you navigate these complex discount structures effectively. We at FirstMark Insurance Group guide families through insurance complexities and help identify all available discounts while we compare offerings from top providers. Request quotes from multiple carriers, document your safety features, and maintain clean records to maximize your home and auto insurance discounts year after year.