Your valuable art collection represents more than just aesthetic beauty-it’s a significant financial investment that standard homeowners insurance won’t adequately protect.

We at FirstMark Insurance Group understand that insuring fine art and collectibles requires specialized coverage tailored to your unique pieces. The right insurance strategy protects against theft, damage, and market fluctuations that could devastate your collection’s value.

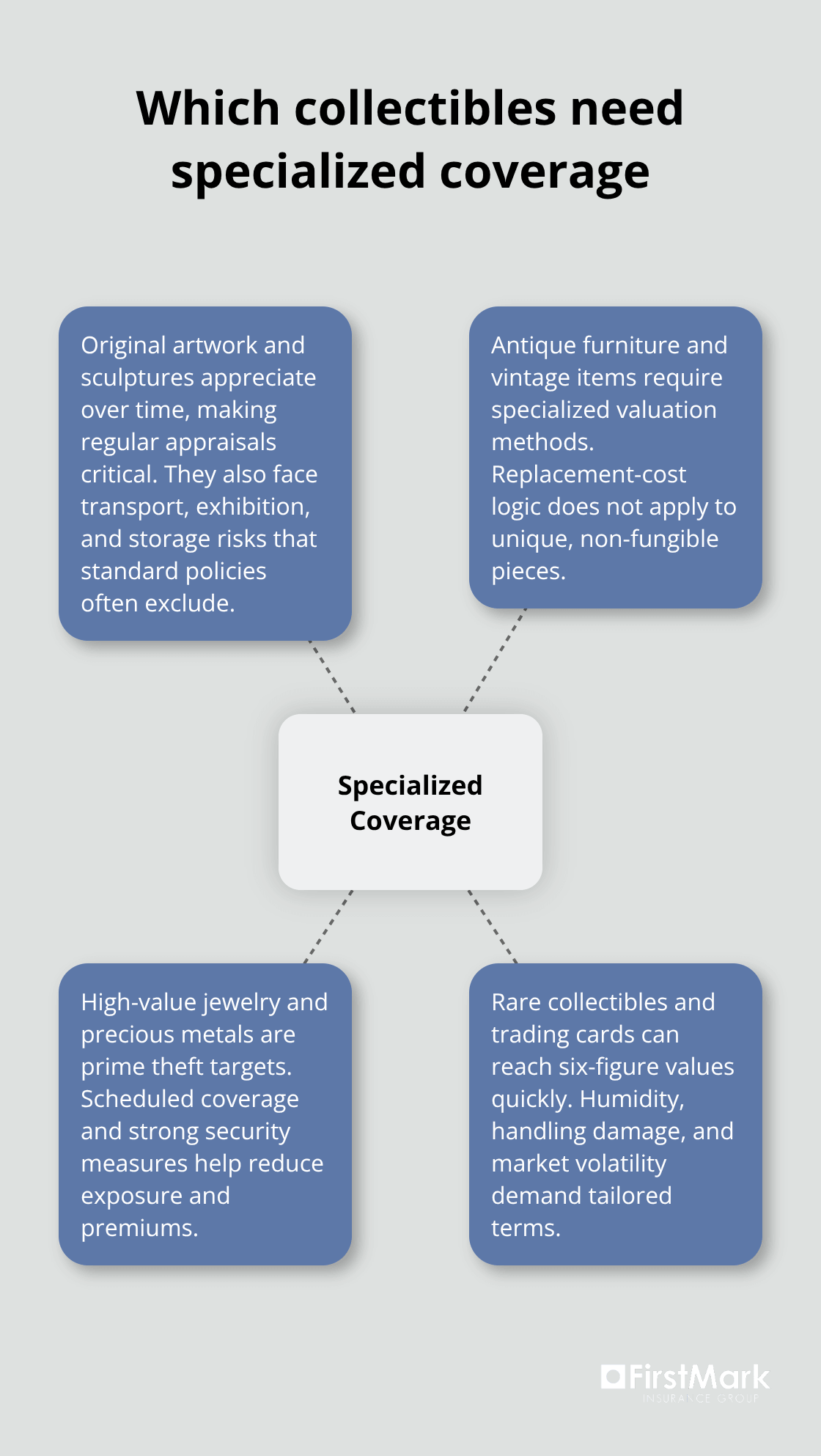

Which Collectibles Require Specialized Coverage

Standard homeowners policies impose severe sub-limits on valuable items, typically capping coverage at $1,000 to $5,000 for artwork, regardless of actual value. The Insurance Information Institute reports that approximately 1 in 5 U.S. homeowners have valuable items that are underinsured, which creates dangerous coverage gaps for collectors.

Original Artwork and Sculptures

Contemporary pieces from artists like Warhol and Banksy appreciate dramatically over time, which makes regular appraisals essential. Paintings and sculptures face unique risks during transportation, exhibition, and storage that standard policies exclude entirely. Professional-grade climate control prevents environmental damage that could destroy decades of investment growth.

Antique Furniture and Vintage Collections

Antique furniture, rare books, and vintage items require specialized valuation methods since replacement costs cannot apply to these unique items that cannot be replaced with identical pieces. The collectibles market has seen certain items appreciate significantly in recent years. Age-related deterioration and restoration needs create coverage complexities that general policies cannot address.

High-Value Jewelry and Precious Metals

Jewelry theft claims spike during holiday seasons and travel periods, which makes comprehensive coverage non-negotiable for valuable pieces. Precious metals and gemstones require separate scheduled coverage with current market prices, as commodity values fluctuate rapidly. Security measures like safes and alarm systems can reduce premiums while they protect against the most common loss scenarios.

Rare Collectibles and Trading Cards

Trading cards, stamps, and rare coins have experienced explosive growth in recent years (with some items reaching six-figure valuations). These items face unique risks from humidity, handling damage, and market volatility that standard policies ignore. Art collections, jewelry, and collectibles that exceed $10,000 per item require professional grading and authentication services for proper coverage documentation.

The next step involves understanding the specific coverage options available to protect these valuable collections effectively.

What Coverage Options Protect Your Art Collection

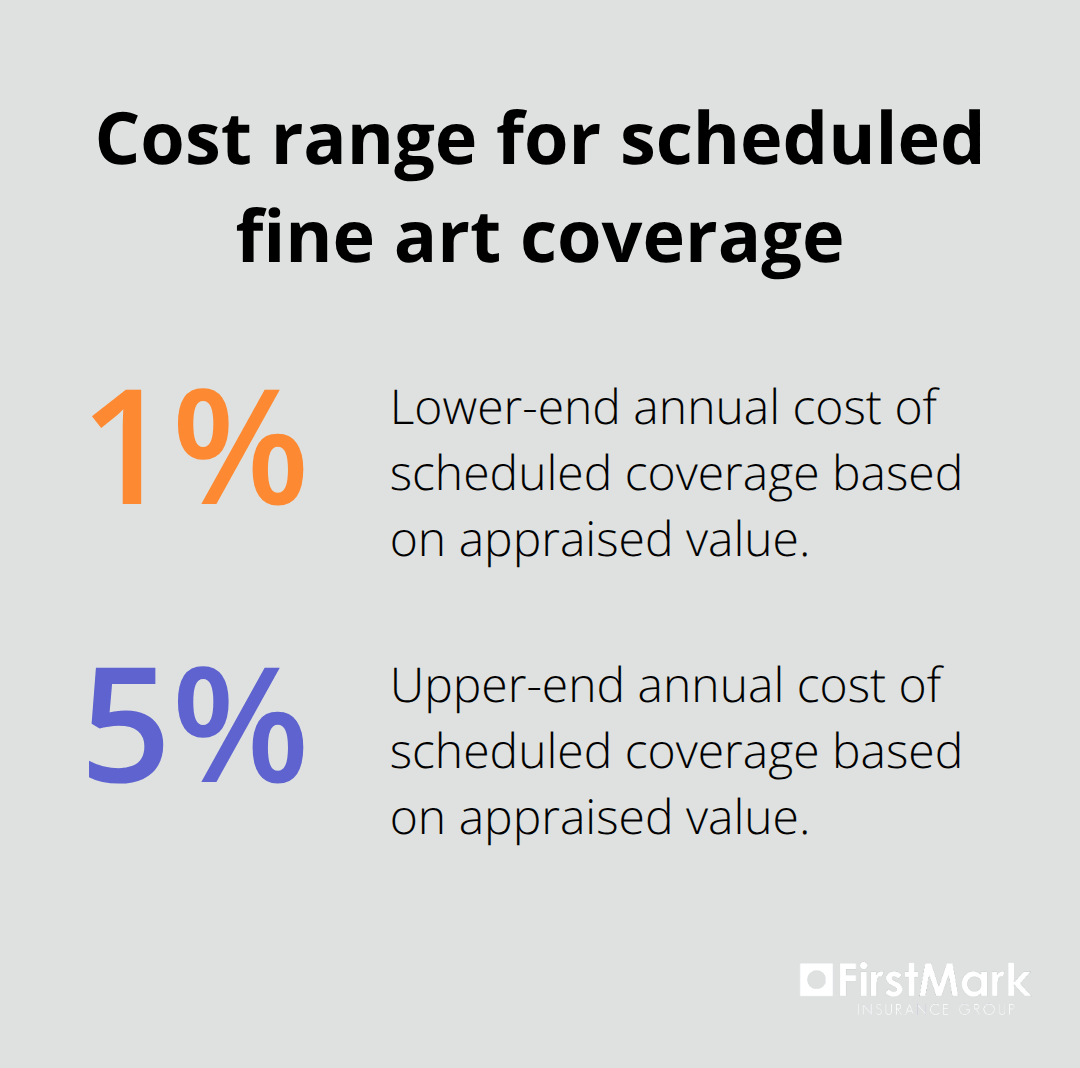

Standard homeowners insurance creates dangerous gaps for art collectors through restrictive sub-limits and exclusions that leave valuable pieces vulnerable. Scheduled personal property coverage addresses this problem by listing specific items with individual coverage amounts based on professional appraisals. This approach provides agreed-value protection, which means you receive the scheduled amount regardless of market fluctuations at claim time. Scheduled coverage typically costs 1% to 5% of the artwork’s appraised value annually, which makes it affordable protection for serious collectors.

Scheduled Coverage vs Blanket Policies

Scheduled policies require itemization of each piece with detailed descriptions, photographs, and current appraisals updated every three to five years. Blanket fine arts policies offer broader coverage limits without individual item schedules, but they require current market value assessments at claim time. Collectors increasingly choose higher blanket limits because they provide flexibility for acquisitions and market appreciation. Blanket policies work best for collectors who frequently buy and sell pieces, while scheduled coverage suits stable collections with established values.

Standard Homeowners Policy Limitations

Homeowners policies impose severe restrictions that make them inadequate for serious collectors. Coverage typically caps at $1,000 to $5,000 for all artwork combined (regardless of actual value). Most homeowners policies exclude damage that occurs during transit, exhibition, or professional storage. These policies also exclude mysterious disappearance and accidental breakage scenarios that commonly affect valuable collections.

Fine Arts Floater Benefits

Fine arts floater policies eliminate homeowners restrictions by providing worldwide coverage that follows your collection anywhere. These specialized policies cover risks that homeowners insurance explicitly excludes, including mysterious disappearance, accidental breakage, and gradual deterioration from environmental factors. Floater policies also extend coverage to newly acquired pieces automatically for 30 to 90 days (depending on the insurer), which gives collectors time to schedule new acquisitions properly.

Professional appraisal requirements and proper documentation form the foundation for securing this specialized coverage effectively.

How Do You Secure Proper Insurance for Your Collection

Professional appraisal from USPAP-compliant certified appraisers forms the foundation of adequate fine art insurance coverage. The Appraisers Association of America requires specific documentation standards that insurance companies accept without question. Schedule appraisals every three to five years because art market values fluctuate significantly, and outdated valuations leave collectors dangerously underinsured.

Professional Appraisal Requirements

Retail Replacement Value appraisals work best for insurance purposes since they reflect current market conditions rather than historical purchase prices. Appraisers who specialize in your specific art category provide more accurate valuations than generalists, which directly impacts your coverage limits and claim settlements. Professional appraisers must hold current certifications and maintain active membership in recognized professional organizations to meet insurer standards.

Documentation Standards That Insurers Accept

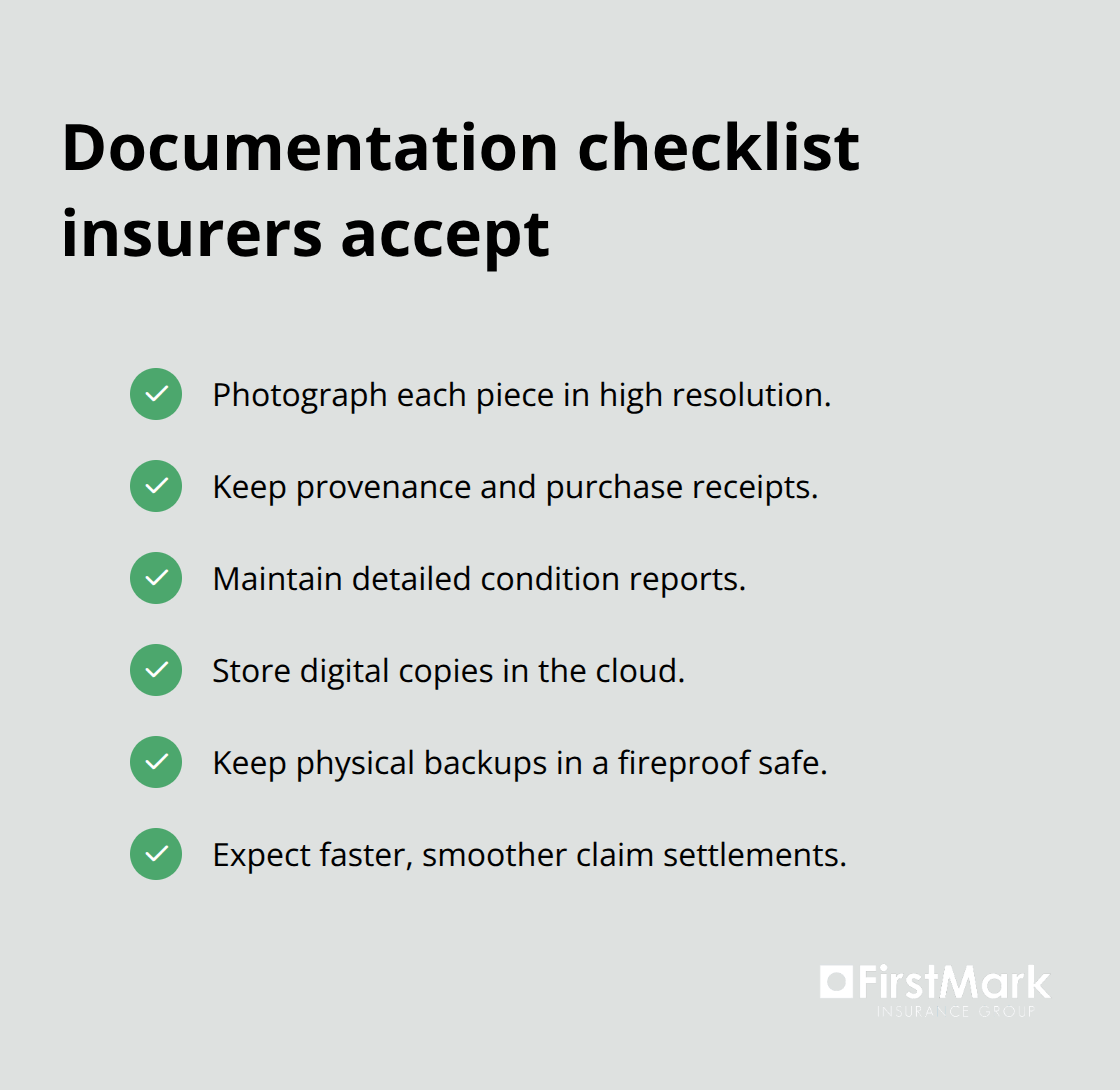

Create detailed inventory records with high-resolution photographs from multiple angles, provenance documentation, and purchase receipts for every piece in your collection. Insurance companies require condition reports that note existing damage or restoration work to prevent claim disputes later. Store digital copies of all documentation in cloud-based systems with physical backups in fireproof safes (or bank safety deposit boxes). Collectors with comprehensive documentation receive faster claim settlements and fewer coverage disputes.

Inventory Management Best Practices

Update inventory records immediately after acquisitions, sales, or condition changes to maintain accurate coverage levels. Professional conservation reports document any restoration work or condition deterioration that affects market value. Maintain separate files for each piece that include purchase invoices, exhibition history, and any expert authentication certificates. Digital asset management systems help organize thousands of images and documents that insurers require for proper coverage verification.

Selecting Insurance Providers With Art Expertise

Choose insurers with dedicated fine arts departments rather than general property insurers who lack specialized knowledge. Specialty art insurers offer broader coverage definitions and understand unique risks that general insurers exclude or misunderstand. Compare deductible options carefully because higher deductibles reduce premiums significantly (while lower deductibles provide better claim protection). Security requirements vary dramatically between insurers, so evaluate alarm system, climate control, and secure storage facility requirements before selecting coverage. Request references from other collectors and verify the insurer’s claims payment history for art-related losses through state insurance department records.

Final Thoughts

Professional appraisals every three to five years protect against market fluctuations that could leave collections underinsured by hundreds of thousands of dollars. Scheduled coverage provides agreed-value protection, while blanket policies offer flexibility for active collectors who frequently acquire new pieces. Documentation standards determine claim success rates through high-resolution photographs, provenance records, and condition reports that streamline settlements.

Security measures like climate control and alarm systems reduce premiums while they protect investments from environmental damage and theft. Geographic location impacts costs significantly, with high-risk areas that require enhanced protection strategies. Digital inventory management systems with cloud storage and physical backups protect against data loss that could complicate claims.

Insuring fine art and collectibles demands expertise that general insurance agents often lack. We at FirstMark Insurance Group specialize in complex coverage scenarios that protect valuable collections from devastating losses. Contact our experienced team to discuss your specific collection needs and secure proper protection for your investments.