Foreclosed homes often appear as bargain opportunities, but the risks of buying a foreclosed home can quickly turn a deal into a financial nightmare. These properties typically come with hidden problems that standard home purchases don’t face.

We at FirstMark Insurance Group see buyers who underestimate the complexity of foreclosure purchases. The potential savings rarely justify the extensive risks involved.

What Financial Traps Await Foreclosure Buyers

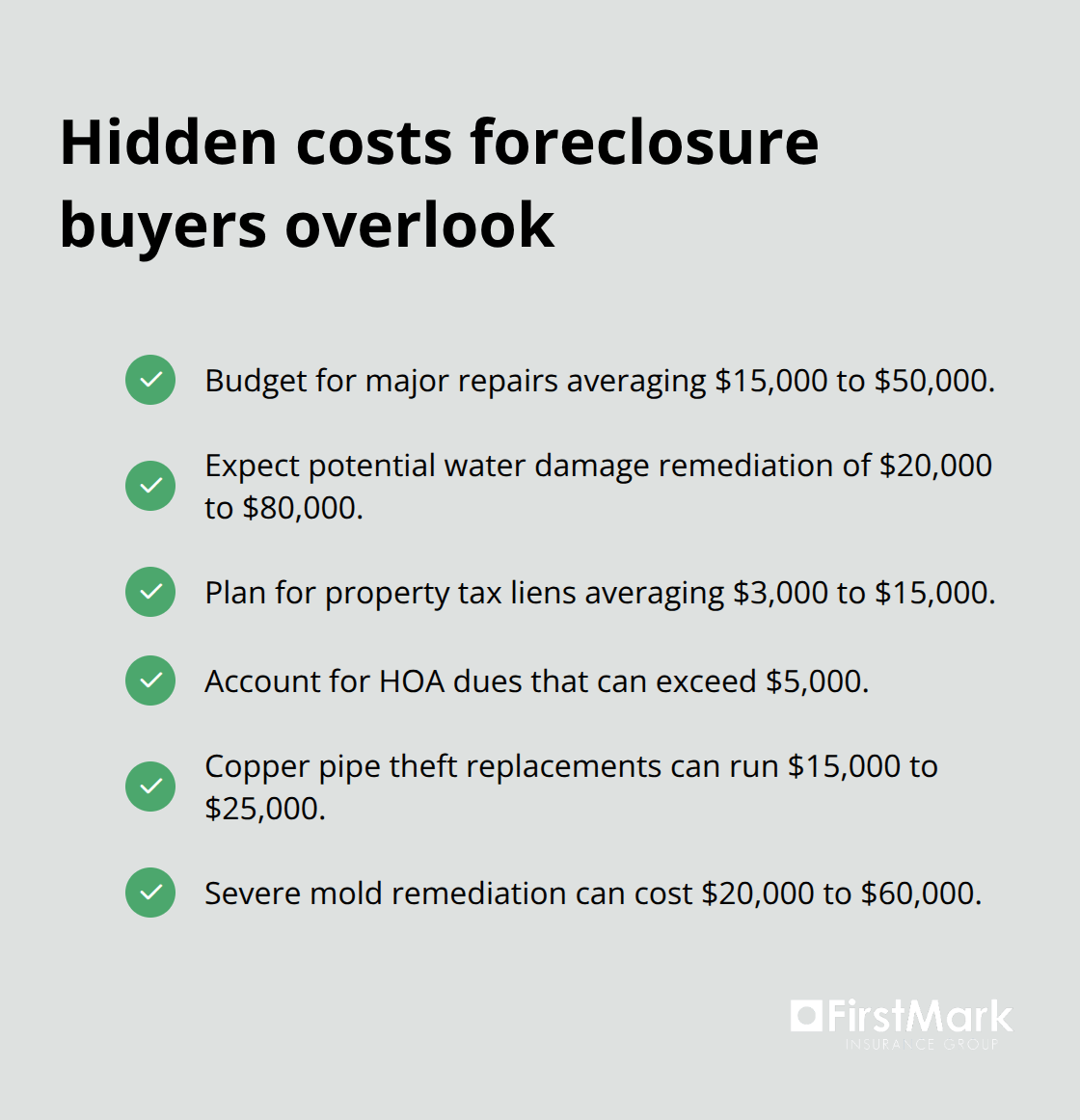

The financial risks of foreclosed properties extend far beyond the purchase price. According to the National Association of Realtors, foreclosure buyers face repair costs that average $15,000 to $50,000, with some properties that require over $100,000 in renovations. These homes often hide serious structural issues like foundation cracks, roof damage, and electrical systems that fail because previous owners couldn’t afford to maintain them. Water damage from burst pipes or neglect can cost $20,000 to $80,000 to remediate properly.

Outstanding Debts Follow the Property

Many foreclosed homes carry hidden financial burdens that transfer to new owners. Property tax liens that average $3,000 to $15,000 commonly attach to foreclosed properties, while homeowners association dues can accumulate to $5,000 or more.

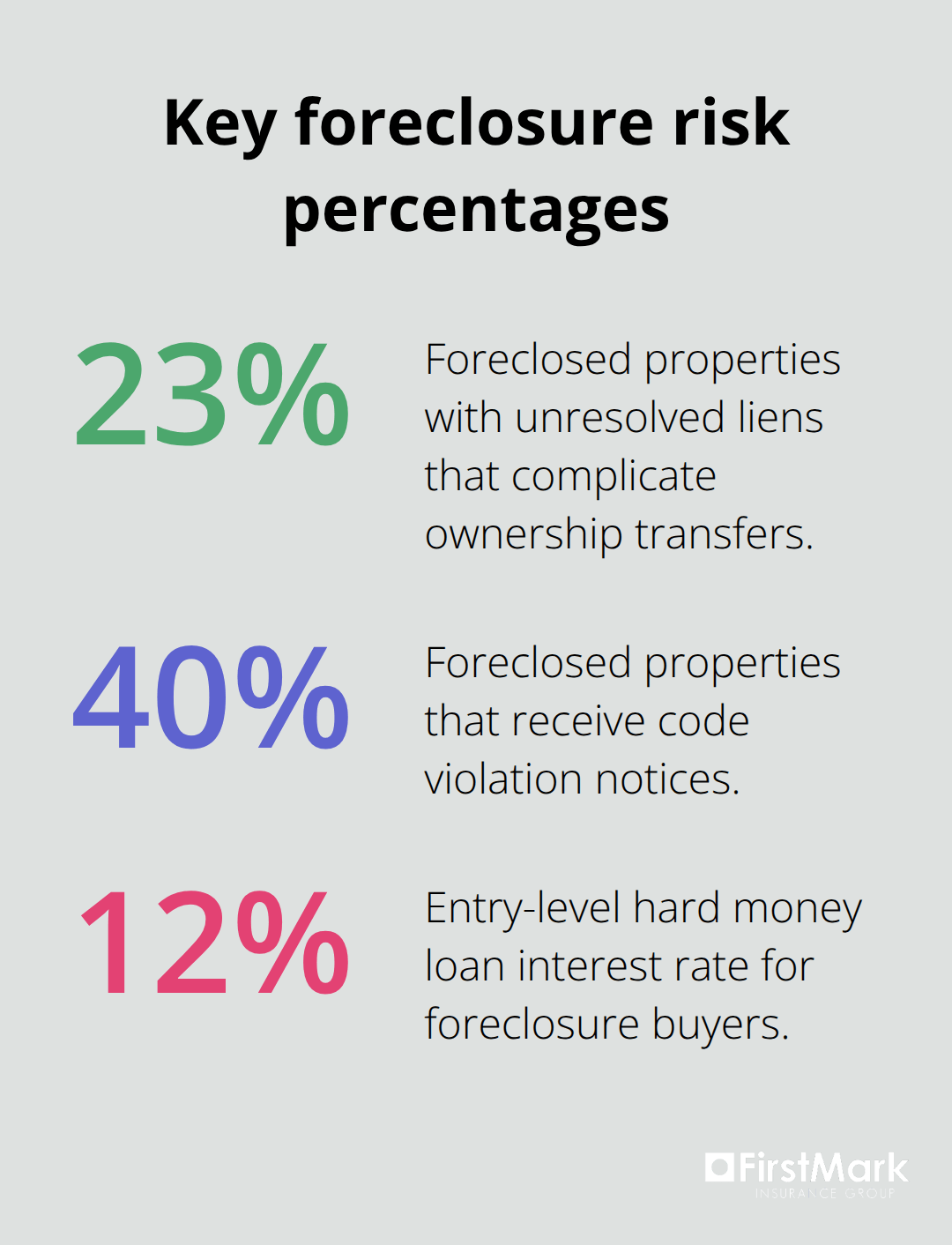

Municipal code violations create additional costs for properties with neglected maintenance. Title companies report that 23% of foreclosed properties have unresolved liens that complicate ownership transfers.

Cash Requirements Lock Out Most Buyers

Foreclosure auctions typically require 100% cash payments within 24 to 48 hours, which eliminates finance options for most buyers. Even bank-owned properties face restrictions from lenders, with many lenders who refuse mortgages on homes that need extensive repairs. Hard money loans charge 12% to 18% interest rates with 2 to 5 point origination fees (dramatically increasing acquisition costs). FHA 203k rehabilitation loans offer alternatives but require properties to meet minimum safety standards that many foreclosures fail to achieve.

Insurance Complications Add More Costs

Standard homeowners insurance policies often exclude coverage for vacant properties, which leaves foreclosed homes vulnerable during the purchase process. Insurance companies frequently deny coverage for homes with existing damage or code violations (common in foreclosed properties). Buyers must secure specialized vacant property insurance at rates 50% to 300% higher than standard policies. These insurance gaps create additional financial exposure that compounds other foreclosure risks, making legal complications another major concern for potential buyers.

What Legal Nightmares Hide in Foreclosure Titles

Title Defects Create Expensive Legal Battles

Title defects create significant challenges for foreclosed properties, leading to complex legal battles that last years and cost tens of thousands in attorney fees. Chain of title problems emerge when banks fail to properly document ownership transfers during the foreclosure process. This leaves gaps that title companies refuse to insure.

Mechanics liens from unpaid contractors surface regularly in foreclosure purchases. Divorce decree complications and forged signatures in previous transactions add more legal risks. Title insurance companies charge premiums 25% to 40% higher for foreclosed properties. Many exclude coverage for pre-existing defects that buyers inherit.

Eviction Battles Drain Time and Money

Former owners who refuse to vacate create immediate legal challenges. These situations cost buyers $5,000 to $15,000 in legal fees plus months of delays. Squatters who occupy abandoned foreclosed homes establish tenant rights in many states. This requires formal eviction proceedings that take 30 to 90 days.

Some states grant redemption periods that allow previous owners to reclaim properties up to one year after foreclosure sales. This creates uncertainty for new buyers. Professional eviction services charge $1,500 to $3,500 per case. Property damage during contested evictions averages $8,000 to $20,000.

Inspection Limits Force Blind Purchases

Foreclosure auctions prohibit property inspections. This forces buyers to purchase homes sight unseen with no recourse for hidden defects. Bank-owned properties typically allow limited walk-through inspections but forbid invasive tests of electrical, plumbing, or structural systems.

Property disclosures go missing, which eliminates seller liability for known defects (unlike traditional home sales where sellers must reveal material problems). The absence of seller warranties means buyers assume full responsibility for all repairs from day one. Environmental hazards like asbestos or lead paint cost $10,000 to $30,000 to remediate. These legal complications pale in comparison to the physical deterioration that awaits buyers who take possession of neglected properties.

What Physical Damage Awaits in Foreclosed Properties

Vandalism and Neglect Create Massive Repair Bills

Foreclosed properties suffer extensive damage from vandalism and years of neglect that previous owners couldn’t afford to address. The National Association of Home Builders reports that vacant foreclosed homes experience break-ins at rates 300% higher than occupied properties. Thieves steal copper pipes, which costs $15,000 to $25,000 to replace throughout an average home. Appliance theft, HVAC unit removal, and stripped electrical wires add another $10,000 to $35,000 in replacement costs.

Broken windows from break-ins allow weather damage that destroys floors, walls, and personal property left behind. Water intrusion creates mold growth that costs $20,000 to $60,000 to remediate properly in severe cases. Squatters often damage properties further by removing fixtures, punching holes in walls, or starting fires for warmth.

Outdated Systems Fail Safety Standards

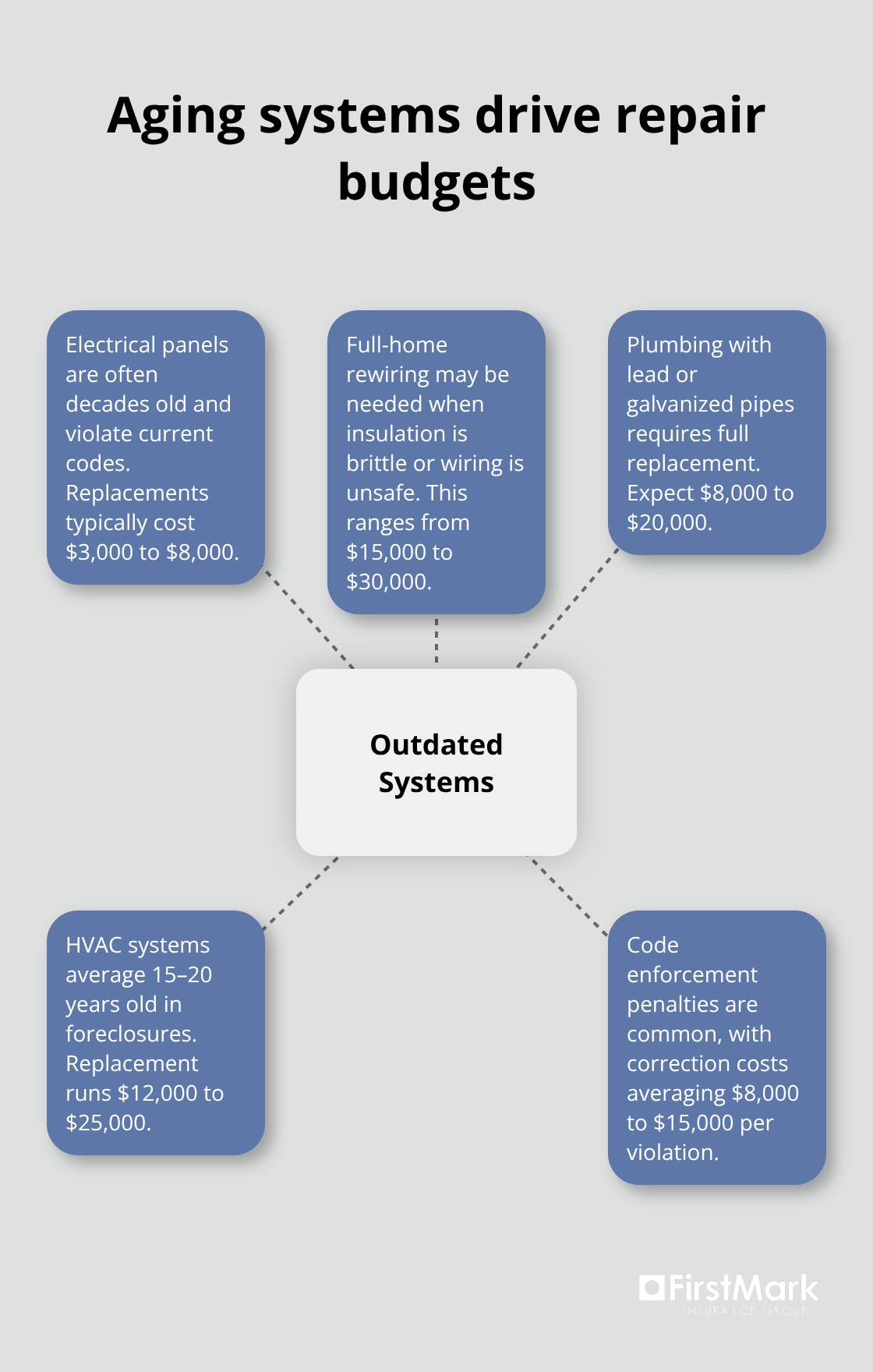

Electrical systems in foreclosed properties frequently violate current codes, with panels that haven’t been updated since the 1970s or 1980s. The National Fire Protection Association links outdated electrical systems to 51,000 house fires annually.

Homeowners pay $3,000 to $8,000 to replace electrical panels, while rewiring entire homes ranges from $15,000 to $30,000.

Plumbing systems often contain lead pipes or galvanized steel that requires complete replacement at $8,000 to $20,000. HVAC systems average 15 to 20 years old in foreclosed properties (with replacement costs from $12,000 to $25,000). Code enforcement departments issue violation notices on 40% of foreclosed properties, with correction costs that average $8,000 to $15,000 per violation.

Warranty Protection Disappears Completely

Foreclosed properties come with zero warranty protection that leaves buyers financially exposed for every defect. Traditional home sales include seller warranties that cover major systems for 30 to 90 days after purchase. Banks that sell foreclosed properties explicitly disclaim all warranties and sell homes “as-is” without exception.

Home warranty companies often refuse coverage for foreclosed properties due to their poor condition (or charge premiums 200% to 400% higher than standard rates). Buyers assume full responsibility for all repairs from day one, including problems that surface weeks or months after purchase.

Final Thoughts

The risks of buying a foreclosed home create financial exposure that extends far beyond the purchase price. Repair costs average $15,000 to $50,000, hidden liens reach $15,000, and legal complications cost thousands in attorney fees. Physical damage from vandalism and neglect compounds these problems with mold remediation costs that reach $60,000 and complete system replacements that total $75,000 or more.

Professional guidance becomes essential when you navigate foreclosure purchases. Real estate agents experienced in distressed properties, qualified inspectors, and title attorneys help identify problems before they become costly surprises. We at FirstMark Insurance Group recommend that you secure specialized insurance coverage early in the process (as standard policies exclude vacant properties and damaged homes).

Foreclosed properties might still offer value for cash buyers with construction experience who can accurately estimate repair costs. Investors with $100,000 or more in renovation budgets and six months for repairs sometimes find profitable opportunities. FirstMark Insurance Group helps buyers understand insurance requirements for distressed properties and find coverage that protects their investment throughout the renovation process.